Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Corporate

Audit Quality Report 2022–23

Published

Monday 11 December 2023

Contact

Please direct enquiries through our contact page.

Quality in the delivery of the ANAO’s audit services is critical in supporting the integrity of our audit reports and maintaining the confidence of the Parliament and public sector entities. The ANAO corporate plan is the ANAO’s primary planning document. It outlines our purpose; the dynamic environment in which we operate; our commitment to building capability; and the priorities, activities and performance measures by which we will be held to account. The ANAO quality management framework and plan complements the corporate plan. It describes the ANAO’s system of quality management and reflects the ANAO’s responses to identified quality risks.

The ANAO Quality Management Framework is the ANAO’s established system of quality management to provide the Auditor-General with reasonable assurance that the ANAO complies with the ANAO Auditing Standards and applicable legal and regulatory requirements, and reports issued by the ANAO are appropriate in the circumstances.

This audit quality report sets out the Auditor-General’s evaluation on the implementation and operating effectiveness of the ANAO Quality Management Framework. The report:

- provides transparency in respect of the processes, policies, and procedures that support each element of the ANAO Quality Management Framework;

- outlines ANAO performance against benchmarks on audit quality indicators; and

- outlines the ANAO’s performance against the quality assurance strategy and deliverables set out in the Quality Management Framework and Plan 2022–23.

Auditor-General’s conclusion on the system of quality management

As Auditor-General, I am responsible for the evaluation of the Australian National Audit Office (ANAO) Quality Management Framework.

My evaluation is based on the matters outlined in the accompanying ANAO Audit Quality Report 2022–23. The ANAO has undertaken remediation procedures where the ANAO quality assurance review program identified significant findings that were deemed to be departures from the ANAO Auditing Standards (see paragraph 3.85). Through the completion of remediation procedures and enhanced documentation that met the ANAO Auditing Standards, I am satisfied that the deficiencies have been appropriately remediated at the time of this evaluation. The ANAO has also designed and implemented remedial actions that strengthen the quality management framework in response to opportunities for improvement identified in our quality assurance review program, including root cause analysis.

Based on my evaluation, I have concluded that the ANAO Quality Management Framework was operating effectively for the period ended 30 June 2023, and provides reasonable assurance that:

- The ANAO and its personnel fulfill their responsibilities in accordance with AUASB standards and applicable legal and regulatory requirements, including the Auditor-General Act 1997 and the Australian National Audit Office Auditing Standards 2023, and conduct engagements in accordance with such standards and requirements; and

- Engagement reports issued by the ANAO are appropriate in the circumstances.

Grant Hehir

Auditor-General

8 December 2023

1. Introduction

Audit quality reporting

1.1 The purpose of the Australian National Audit Office (ANAO) is to support accountability and transparency in the Australian Government sector through independent reporting to the Parliament, and thereby contribute to improved public sector performance.

1.2 The quality of ANAO audit work is reliant on the strength of its independence and quality management framework. A sound quality management framework supports delivery of highquality audit work and enables the Auditor-General to have confidence in the opinions and conclusions contained in the reports prepared for the Parliament. This facilitates the confidence of the Parliament that the ANAO operates with independence and that the audit approach meets the auditing standards set by the Auditor-General.

Framework for quality

1.3 The ANAO is established under the Auditor-General Act 1997 (the Act). Section 24 of the Act requires the Auditor-General to set auditing standards that are to be complied with by persons performing functions under the Act. The ANAO Auditing Standards set under this provision incorporate standards issued by the Auditing and Assurance Standards Board (AUASB) and relevant auditing and assurance standards issued by standard-setting bodies other than the AUASB as appropriate. Specific to quality assurance, this includes:

- Until 15 December 2022 — ASQC 1 Quality Control for Firms that Perform Audits and Reviews of Financial Reports and Other Financial Information, Other Assurance Engagements and Related Services Engagements (AQSC 1); and

- From 15 December 2022 onwards — ASQM 1 Quality Management for Firms that Perform Audits or Reviews of Financial Reports and Other Financial Information, or Other Assurance or Related Services Engagements (ASQM 1).

1.4 The ANAO defines audit quality as the provision of timely, accurate and relevant audits, performed independently in accordance with the Auditor-General Act, ANAO Auditing Standards and methodologies, which are valued by the Parliament. Delivering quality audits results in improved public sector performance through accountability and transparency.

Purpose of the audit quality report

1.5 Until 15 December 2022, the ANAO established and maintained a system of quality control that complied with ASQC 1, which is detailed in the ANAO Quality Assurance Framework 2022–23. On 15 December 2022 the new and revised Australian Quality Management Standards issued by the AUASB including ASQM 1 were operative and the ANAO implemented a revised system of quality management.1

1.6 Together, the systems of quality control and quality management were designed to provide the ANAO with reasonable assurance that:

- the ANAO and its staff fulfill their responsibilities in accordance with the ANAO Auditing Standards and applicable legal and regulatory requirements, and conduct engagements in accordance with such standards and requirements; and

- reports issued by the ANAO are appropriate in the circumstances.

1.7 This Quality Report provides transparency in respect of the processes, policies, and procedures that support each element of audit quality as described in the ANAO Quality Assurance Framework and ANAO Quality Management Framework, and reports on the 2022–23 audit quality indicators. These indicators assess ANAO performance against benchmarks for the year ended 30 June 2023.

Audit quality indicators

1.8 Audit quality indicators (AQIs) are reliable quantitative measures regarding the audit process. AQIs are considered alongside relevant qualitative information to identify insights into factors that may influence audit quality. Measuring AQIs can strengthen audit quality through assisting in understanding the root causes of quality inspection findings and informing discussions about auditing processes and appropriate benchmarks. This in turn leads to improved audit planning, execution, and communication and, where root causes are identified, improved remediation procedures that address the drivers of quality deficiencies.

1.9 The ANAO measures 10 AQIs and has identified benchmarks for each of these AQIs against which performance is considered. The identified benchmarks are not targets, but provide context for consideration of the results of the AQIs along with qualitative information and prior year results. Four AQIs are measures from the Australasian Council of Auditors-General (ACAG) annual macro benchmarking survey in which most Australian audit offices, including the ANAO, participate. The purpose of the survey is to provide comparable information and benchmarks to audit offices across Australasia. ANAO benchmarks for the AQIs derived from the ACAG macro benchmarking are developed using past results of comparable audit offices2 taken from this survey and adjusted to calculate a three-year rolling average. The remaining six AQIs and related benchmarks are derived from ANAO Audit Manual policy requirements, the ANAO Workforce Plan and leadership expectations regarding independence and audit quality. The Quality Assurance Framework and Plan 2022–23 outlines the source of each of the benchmarks.

2. Executive summary

2.1 The ANAO employed 405 staff as at 30 June 2023. ANAO staff come from a range of disciplines including commerce, accounting, finance, economics, public policy, law, science, social sciences, and information technology.

2.2 The ANAO tabled 45 reports in Parliament in 2022–23. These reports included 40 performance audits, two reports on the financial statements of Australian Government entities, the Major Projects Review, one information report, and a report on the audits of performance statements for the reporting period 2021–22. In 2022–23 the ANAO issued 247 opinions on mandated financial statements audits, conducted a further 41 audits by arrangement and issued six performance statements audit opinions. In 2022–23 the ANAO also issued four Audit Insights products, which communicate lessons on themes arising in the ANAO’s audit work, such as procurement and performance reporting.

2022–23 Audit quality indicator results

2.3 The ANAO measures and reports against 10 AQIs.3 Table 2.1 summarises the 2022–23 ANAO results against each AQI.

Table 2.1: Summary of 2022–23 ANAO results against each Audit quality indicator

|

Audit quality indicator |

Element of system of quality management |

2022–23 ANAO result |

|

Compliance with independence requirements |

Relevant ethical requirements |

Not consistent with benchmark |

|

Material restatements resulting from a prior period error |

Engagement performance |

Not consistent with benchmark |

|

Turnover of audit personnel |

Resources |

Not consistent with benchmark |

|

Training hours per audit professional |

Resources |

Consistent with benchmark |

|

Staffing leverage |

Resources |

Consistent with benchmark |

|

Engagement Executive and manager audit workload |

Resources |

Consistent with benchmark |

|

Staff audit workload |

Resources |

Consistent with benchmark (Financial statements and performance statements) Not consistent with benchmark (Performance audit) |

|

Technical accounting and auditing resources |

Resources |

Not consistent with benchmark |

|

Quality assurance review coverage |

Monitoring and remediation |

Consistent with benchmark |

|

Internal quality review results |

Monitoring and remediation |

Not consistent with benchmark |

2.4 The ANAO’s 2022–23 results against benchmarks indicate that there are opportunities to improve the implementation of the quality management framework. The ANAO has assessed each of the areas where the results were not in line with the benchmark to understand the drivers for the results and develop action items to strengthen the framework. The assessment and actions are summarised below:

- The instances of non-compliance with independence requirements in the ANAO Audit Manual related to contracted firms not following ANAO approval process policies related to the provision of other services to the entities they were contracted to audit. In the case of two firms this was the first identified breach of policy and the Group Executive Director (GED) Professional Services and Relationships Group (PSRG) wrote to the relevant relationship partners regarding the breach. In the third case, this was the third identified breach of the firm. The Deputy-Auditor General wrote to the Assurance Managing Partner to advise of the breach. The ANAO has held discussions with the firms to ensure that the policy requirements are understood by the firms involved.

- The analysis of material restatements to correct prior period errors did not indicate that there were deficiencies in the ANAO quality management framework, despite being inconsistent with the benchmark. While no further action is necessary this year, the ANAO intends to include prior period errors in future root cause analysis programs to ensure that the drivers of prior period errors are understood in a timely manner following the completion of the audit cycle. This will allow for any required actions and learnings to be implemented earlier.

- Staff turnover continues to remain a risk area to audit quality. Additionally, over the past two years ANAO total staff numbers have increased from 318 at 30 June 2021 to 405 as at 30 June 2023 (27% increase). The ANAO Workforce Plan 2022–25 responds to quality risks around resourcing and staff turnover through its focus on building workforce capability to undertake a higher target of performance audits and performance statements audits.

- Increased time charged to coaching and mentoring new starters contributed to the lower staff workload numbers charged to performance audits. The support through coaching and mentoring has been a focus for the ANAO in performance audit, particularly for new audit managers. Increased time for coaching and mentoring in financial statements audits was also an action item in response to root cause analysis performed in 2021–22.

- No action is considered necessary for the technical and accounting and auditing resources result being inconsistent with the benchmark as the ANAO is comfortable with the extent of resources dedicated to technical accounting and auditing activities to support audit quality.

- To address the increased number of unsatisfactory audits identified in the ANAO’s internal quality review program the ANAO conducted a root cause analysis to address the drivers of the quality findings with targeted action items developed.

2.5 Chapter 3 outlines the results of the 2022–23 audit quality indicators under each element of the ANAO Quality Assurance Framework with further explanations of the results and the impacts on audit quality.

2.6 The ANAO will continue its focus on the implementation of quality management activities and make further enhancements to the quality framework in 2023–24 as set out in the ANAO Corporate Plan, with particular emphasis on:

- monitoring compliance with ASQM 1, ASQM 2 Engagement Quality Reviews, and ASA 220 Quality Management for an Audit of a Financial Report and Other Historical Financial Information;

- continuing to expand our root cause analysis program — in particular, expanding the program to include analysing results from quality assurance reviews of performance statements audit and performance audit files, as well as continuing to expand the existing program for analysing results from financial statements audit quality assurance reviews;

- continuing to refine the performance statements audit manual and methodology; and

- refining the methodology associated with auditing efficiency and ethics, including reviewing application of the efficiency methodology in practice and monitoring implementation of the ethics methodology.

Quality Assurance Plan and deliverables for 2022–23

2.7 The Quality Assurance Framework and Plan 2022–23 set out 26 key deliverables. Progress against these deliverables as at 30 June 2023 was:

- 19 deliverables completed;

- five deliverables in progress; and

- two deliverables did not proceed.

2.8 The status of deliverables as at 30 June 2023 is discussed further in Chapter 4.

3. Elements of the ANAO Quality Management Framework

3.1 This chapter outlines the activities conducted by the ANAO in 2022–23 under each element of the ANAO Quality Assurance Framework (extant to 15 December 2022) and the ANAO Quality Management Framework (extant from 15 December 2022). It also includes the results of the 2022–23 audit quality indicators against benchmarks.

Responsibilities for the system of quality management

3.2 The Auditor-General is ultimately responsible and accountable for the system of quality management in place for all assurance and related activities undertaken by the ANAO.

3.3 The Deputy Auditor-General is operationally responsible for ensuring that the system of quality management satisfies the requirements of the ANAO Auditing Standards. In 2022–23 the Deputy Auditor-General was assisted with this role by the Group Executive Directors (GEDs) of each of the ANAO’s six business groups:

- Financial Statements Audit Services Group (FSASG);

- Performance Audit Services Group (PASG);

- Performance Statements Audit Services Group (PSASG);

- Systems Assurance and Data Analytics Group (SADA);

- Professional Services and Relationships Group (PSRG); and

- Corporate Management Group (CMG).

3.4 The Auditor-General is supported and advised by the Executive Board of Management (EBOM) in achieving the ANAO’s purpose. The Deputy Auditor-General, the GEDs of the six business groups and the Chief Financial Officer (CFO) are members of EBOM.

The Quality Committee

3.5 Governance for audit quality is provided through the Quality Committee (a sub-committee of EBOM). The role of the Quality Committee includes monitoring the implementation of the ANAO Quality Management Framework and Plan. The Quality Committee is comprised of representatives from all ANAO business groups and is chaired by the PSRG GED.

3.6 The Quality Committee met four times during 2022–23 and reported on its activities to EBOM. In 2022–23 the Quality Committee, in accordance with its terms of reference:

- reviewed the findings of external and internal reviews in relation to quality;

- monitored the ANAO’s progress in addressing the findings and recommendations made in external and internal reviews;

- monitored and reported to EBOM on the implementation, operating effectiveness and efficiency of the Quality Management Framework, having regard to the findings of external and internal reviews and the audit quality indicators;

- advised the Auditor-General on whether the operation of the Quality Management Framework provides reasonable assurance that the ANAO’s quality objectives are being achieved;

- monitored the strategic and operational risks associated with quality; and

- considered and endorsed proposed amendments to the ANAO Audit Manual that substantially impact the conduct of an audit prior to the Auditor-General’s approval.

3.7 A summary of the Quality Committee membership and meetings attended in 2022–23 is provided in Table 3.1.

Table 3.1: Quality Committee membership and meetings attended 2022–23

|

Member |

September 2022 |

December 2022 |

March 2023 |

June 2023 |

|

PSRG GED (Chair) |

✔ |

✔ |

✔ |

✔ |

|

PASG GED (Deputy Chair) |

✔ |

✘ |

✘ |

✔ |

|

FSASG SED (Senior Executive Director) |

Pa |

✔ |

✔ |

✔ |

|

CMG GED |

✔ |

P |

P |

✔ |

|

SADA GED |

✔ |

P |

✔ |

✔ |

|

PASG Executive Director (ED) |

✔ |

✔ |

✔ |

P |

|

FSASG ED |

P |

✔ |

✔ |

✔ |

|

PSASG ED |

✔ |

✔ |

✔ |

✘ |

Note a: P in the table = Proxy, the Quality Committee member was unable to attend the Committee meeting; a nominated proxy attended on their behalf.

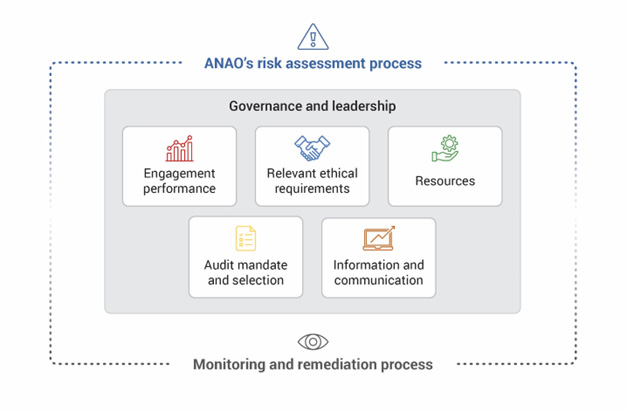

The ANAO’s risk assessment process

3.8 The ANAO has designed and implemented a risk management framework which shapes our strategic direction, contributes to evidence-based decision-making and is embedded into business-as-usual practices. Risk management is integrated into our governance structure and is supported by the Enterprise Risk Register, which sets out the ANAO’s strategic and operational risks.

3.9 From 15 December 2022 onwards, the ANAO has established the quality objectives required by ASQM 1 and one additional ANAO-specific quality objective.4 We have designed and implemented a Quality Risk Assessment process to identify and assess risks that may affect the achievement of those quality objectives, and to support the design and implementation of responses to address those risks. The process is informed by the ANAO Enterprise Risk Register.

3.10 The process of risk assessment is iterative. The ANAO’s quality objectives and quality risks are reviewed on an annual basis to support the annual review of the Quality Management Framework. The annual review takes into account the Auditor-General’s evaluation of whether the Quality Management Framework provides reasonable assurance that the ANAO’s quality objectives are being achieved.

Governance and leadership

Commitment to quality through culture, actions and behaviours

3.11 The Auditor-General sets the tone at the top and demonstrates a leadership commitment to audit quality and culture by articulating the importance of quality in ANAO Executive discussions, monthly EBOM meetings, and all staff communications including town hall meetings and the Auditor-General’s monthly messages to staff. Through this communication, the Auditor-General promulgates his expectation that all ANAO staff take a shared responsibility for quality and view the monitoring activities as an opportunity to continuously improve.

3.12 GEDs reinforce the Auditor-General’s expectations and focus on audit quality through group staff meetings, cohort forums and communications. Engagement Executives support quality in their portfolio of audits by providing direction to audit teams, by reviewing audit work, and through increased involvement in critical areas of judgement, significant risk and difficult or contentious matters.

3.13 The ANAO Corporate Plan 2022–23 includes quality as one of the four key capability areas that the ANAO invests in to support the ANAO in achieving its purpose. Audit quality is a shared responsibility for all staff and each business group plan includes the ‘quality’ capability and outlines the activities, and measures of success, that each group is responsible for leading or supporting.

Leadership responsibility, and roles and responsibilities

3.14 The ANAO Audit Manual assigns specific responsibilities for quality to senior leaders.

- The PSRG GED is responsible for the ANAO audit methodology, which supports compliance with the ANAO Auditing Standards.

- The FSASG, PASG, PSASG and SADA GEDs are responsible for the delivery of quality audit services within their respective business units.

- The FSASG, PASG, PSASG and SADA Engagement Executives are responsible for quality within their portfolio of audits and supporting the GEDs in the delivery and management of quality audit services.

- The CMG GED is responsible for the design, execution and maintenance of policies supporting the Quality Management Framework in respect of human resources, IT security and support, external communications, and learning and development.

- The PSRG and CMG GEDs are jointly responsible for the design and implementation of the ANAO Academy.

3.15 The ANAO organisational structure is consistent with the assignment of roles and responsibilities for quality set out above and in the ANAO Audit Manual and Quality Management Framework.

3.16 The fulfilment of leadership responsibilities is assessed in quality assurance (QA) reviews through review of Engagement Executive involvement in an audit. Any issues in leadership responsibilities are highlighted in the reports to EBOM as part of the results of the QA review program. The results of QA reviews conducted in 2022–23 are set out below from paragraph 3.83 onwards.

Resource needs consistent with commitment to quality

3.17 The ANAO takes a strategic approach to resourcing and workforce management to position and strengthen its workforce to achieve its purpose, which includes achieving audit quality. Investment is made in people through recruitment; learning and development; and managing, leading and supporting employees. The ANAO’s policies on human resources are further discussed below from paragraph 3.42 onwards.

Relevant ethical requirements

3.18 ANAO staff act in accordance with the Australian Public Service (APS) values and the Code of Conduct set out in the Public Service Act 1999. The ANAO core values are respect, integrity and excellence — values that align with the APS values and address the unique aspects of the ANAO’s business and operating environment. The ANAO values promote audit quality by encouraging staff to perform their duties objectively, impartially and in the best interests of the Parliament. The ANAO holds itself to high standards to ensure independence and accountability across all levels of the organisation.

Independence

3.19 In audit engagements, it is in the public interest and required by the ANAO Auditing Standards that auditors are independent of the entity subject to audit. Independence comprises both independence of mind and independence in appearance and is fundamental to the ANAO’s ability to act with integrity, to be objective and to maintain an attitude of professional scepticism. The Auditor-General emphasises the importance of maintaining the independence and integrity of the ANAO in staff communications, including town hall meetings and the Auditor-General’s monthly messages to staff.

3.20 Under the ANAO independence policies, suspected or actual contraventions of the independence requirements of legislation, APES 110 Code of Ethics for Professional Accountants (including Independence Standards) or ANAO policy requirements must be reported immediately to the responsible GED.

Table 3.2: Audit Quality Indicator – Compliance with independence requirements

|

Compliance with independence requirements – Breaches of independence requirements (excluding documentation deficiencies) |

||

|

Benchmark |

2022–23 |

2021–22 |

|

0 |

3 |

0 |

3.21 During 2022–23 three instances were identified where firms who were contracted by the ANAO to undertake a financial statements audit breached the ANAO Audit Manual policies regarding requesting ANAO approval to provide other services to entities they were contracted to audit. (Policies regarding other services are further discussed from paragraph 3.26 below.) In two instances the firms detected the breach and advised the ANAO that they had not complied with the ANAO policy requirement to obtain prior approval from the ANAO to conduct the other services. In the third instance, the ANAO identified that the firm did not obtain prior approval from the ANAO for an increase in fees for the other services. The ANAO assessed the circumstances of each case and determined that the provision of the other services did not cause the ANAO to breach APES 110 as the other services would have been approved if the firm requested in advance of providing the services. In the case of two firms this was the first identified breach of policy and the PSRG GED wrote to the relevant relationship partners regarding the breach. In the third case, this was the third identified breach of the firm. The Deputy-Auditor General wrote to the Assurance Managing Partner to advise of the breach.

3.22 As part of our quality assurance program, the ANAO monitors compliance with independence policies, including documentation requirements. Compliance with independence requirements is also monitored annually by ANAO Internal Audit. Table 3.3 provides the results from the monitoring of compliance with the ANAO independence documentation requirements.

Table 3.3: Compliance with ANAO independence documentation requirements

|

|

2022–23 |

2021–22 |

|

Number of audits selected for internal independence reviews annually. |

FSASG – 26 PASG – 13 PSASG – 3 |

FSASGa – 23 PASG – 15 PSASG – 1 |

|

Number of instances identified where independence declarations were not completed |

FSASG – 7 PASG – 4 PSASG – 0 |

FSASG – 5 PASG – 4 PSASG – 2 |

Note a: Prior to 1 July 2022, FSASG was named Assurance Audit Services Group (AASG). In this report, FSASG is used throughout for consistency.

3.23 The monitoring of independence requirements identified instances where required individual audit team member declarations had not been completed. The number of instances of non-compliance with independence documentation requirements increased from the prior year for FSASG, was stable for PASG and decreased for PSASG. Analysis of the instances of non-compliance identified that each instance was not a breach of independence but was a documentation deficiency. The ANAO has a strong focus on independence and ensuring that the audit file contains a complete record of auditor independence. The results of the quality assurance program are reported to the responsible Engagement Executive, the Quality Committee and EBOM. Further, the importance of completing independence declarations is emphasised in technical update training sessions.

Rotation of key audit personnel

3.24 The ANAO independence policies set key audit personnel rotation requirements for financial statements audits to safeguard against the threat to independence that may arise from a long association with an auditee. While the rotation requirements are specific to financial statements audits, all ANAO staff participating in audits must comply with independence requirements in respect of long association with the auditee.

3.25 Key audit personnel rotation was undertaken in 2022–23 in accordance with the ANAO’s independence policies. All Engagement Executives and Engagement Quality Reviewers qualifying for rotation were either rotated or an extension was approved by the FSASG GED in line with the ANAO independence policies. In the 2022–23 financial statements audit cycle, the Engagement Executives on 10 audits were rotated in line with key audit personnel rotation requirements and approvals for extension were obtained for three audits. The ANAO’s rotation requirements are more demanding than the requirements of APES 110, and all extensions for Engagement Executives were compliant with APES 110.

Other services

3.26 The ANAO contracts private sector firms to undertake audits on behalf of the Auditor-General. The Audit Manual requires contracted firms to request approval from the ANAO to provide other services to auditees.

3.27 In 2022–23 the ANAO approved 36 requests from contracted firms to provide other services to ANAO auditees. One request to provide other services was not approved as the proposed service was not consistent with ANAO Audit Manual policies and the requirements of APES 110. The proposed service included undertaking a fraud risk assessment and supporting the development of the entity’s fraud control plan, which the audit team would consider in assessing the likelihood of a risk of material misstatement due to fraud and in understanding and evaluating the internal control environment, which created a self-review threat.

Gifts and benefits monitoring

3.28 ANAO employees must report any offered gift or benefit (whether accepted or refused) in the gifts and benefits register.

3.29 The data collected through the internal gifts and benefits register is reported to EBOM, and deidentified information is reported publicly on the ANAO website to promote transparency.

Audit mandate and selection

3.30 The Auditor-General publishes an Annual Audit Work Program (AAWP) in July each year which outlines the proposed audit activities to be undertaken in the financial year. From the 85 potential topics included in the 2022–23 AAWP, 28 audits were commenced, of which 11 audits have been tabled and 17 remain underway as at 30 June 2023. An additional seven audits were added to the 2022–23 AAWP in February 2023 as the result of a further review of topics following the October 2022 Federal Budget. Three of these additional audits were underway as at 30 June 2023.

3.31 The ANAO provided a draft of the 2023–24 AAWP to the Parliament for consultation through the JCPAA, consistent with the Auditor-General’s requirement to have regard to the audit priorities of the Parliament. The JCPAA identified 21 audit priority topics and suggested one new topic for the program. Of these 22 topics:

- 16 were included, in whole or in part, in the 2023–24 AAWP; and

- six were topics that had already commenced and were therefore not included in the final program.

3.32 The ANAO tabled 45 reports in Parliament in 2022–23. These reports included 40 performance audits, two reports on the financial statements of Australian Government entities, the Major Projects Review, one information report, and a report on the audits of performance statements for the reporting period 2021–22. In 2022–23 the ANAO issued 247 opinions on mandated financial statements audits and conducted a further 41 audits by arrangement. The ANAO also issued audit opinions on the performance statements of six Commonwealth entities in accordance with a request from the Finance Minister, and in January 2023, the ANAO commenced the audits of ten entities’ 2022–23 performance statements, an increase of four entities from the 2021–22 performance statements audit program.

Engagement performance

Consultation

3.33 The ANAO Audit Manual includes policies requiring consultation on difficult or contentious matters.

3.34 The ANAO has a Qualifications and Technical Advisory Committee (QTAC), which provides a forum for Engagement Executives to consult on difficult or contentious matters and, where necessary, resolve differences of opinion on audit related matters.

3.35 In 2022–23 QTAC was consulted on 27 matters (13 matters in 2021–22). The increase in matters dealt with in 2022–23 was attributable to increases in the number of:

- performance statements audited, including three first time audits; and dealing with new and complex matters not yet considered by the committee;

- matters relating to the appropriateness of the going concern basis of accounting; and

- modified opinions, and emphasis of matter and other matter paragraphs, on prior year audits, which are required under the ANAO Audit Manual to be referred to QTAC (irrespective of whether they are being considered in the current year).

3.36 There is a requirement in the ANAO Audit Manual to consult with the FSASG GED and PSRG when material errors or misstatements are detected that relate to prior year financial statements on which the ANAO has issued an unqualified auditor’s report. The number and impact of restatements for errors are generally considered a signal of possible areas of concern in the audit process. This indicator places restatements in context by focusing on their magnitude and overall impact on the financial statements. The restatements are assessed for materiality at the individual engagement level. The measure includes all financial statements audits, including non-mandated audits. Restatements that were below materiality or related to reclassifications or disclosures with no net impact on the financial result or position have not been included in the totals.

Table 3.4: Audit Quality Indicator – Material restatements resulting from a prior period error

|

Number and percentage of material restatements of financial statements resulting from a prior period errora |

||

|

Benchmark |

2022–23 |

2021–22 |

|

Number and % of material restatements: 0 |

2 (0.7%) out of 288 engagements Errors range from $419,481 to $12.99m net impact on the individual financial statements |

7 (2.9%) out of 242 engagements Errors range from $15,510 to $320.6m net impact on the individual financial statements |

Note a: The financial statements audit cycle for 30 June year end reports is 1 October to 30 September. Therefore the 2022–23 results in the table above record the number of restatements identified in 2021–22 financial statements audits which are finalised within the 2022–23 reporting period.

3.37 The number of restatements of financial statements resulting from prior period errors was above benchmark but represents a decrease from the prior year. The larger of the two restatements related to the incorrect designation of prior period Commonwealth funding as contributed equity rather than a grant. The second restatement related to the incorrect recognition of software assets in the prior period.

3.38 The cause of material restatements is assessed by the ANAO to identify if there are indicators of deficiencies in audit quality. The ANAO is satisfied that the restatements do not indicate systemic deficiencies in audit processes. Material restatements of financial statements resulting from a prior period error is a topic that the ANAO will consider in the continued expansion of the root cause analysis program over financial statements audits.

Engagement quality review policies and monitoring of compliance

3.39 An Engagement Quality Reviewer (EQR) is required under ANAO Audit Manual policy to be appointed to certain audits, including high risk audits and audits of entities determined to be public interest entities (PIEs).5 The EQR provides an objective evaluation of the significant judgements made by the audit team and conclusions reached in formulating the audit report.

3.40 Reviews conducted as part of the ANAO Quality Assurance Program consider compliance with the EQR policy including assessments of whether an EQR was required to be appointed, if an appointed EQR met the eligibility criteria and if the documentation of that involvement throughout the audit was in accordance with the ANAO Audit Manual requirements.

3.41 In 2022–23, ten financial statements engagements were rated as high risk and an EQR was appointed. In 2022–23, ten financial statements audits were assessed as PIEs, and three of these audits were assessed as high-risk engagements. EQRs were appointed to all PIE audits, with the exception of one audit where approval was obtained by the Auditor-General to appoint a second reviewer rather than an EQR. This exception was made as the Auditor-General was the signing officer. Four performance statements audits were rated as high-risk audits and an EQR was appointed. One performance audit tabled in 2022–23 was rated as a high-risk audit and an EQR was appointed.

Resources

Human resources

Qualified personnel

3.42 The ANAO’s human resources policies and procedures support the selection of employees who have the necessary integrity, capability and competence to perform the work required.

3.43 The degree and nature of the changes in an audit team from year to year are an input in determining the readiness and ability of the team to perform a quality audit. Some level of attrition is expected but a comparatively high rate of turnover or frequent auditor transfers within the office may adversely affect audit quality. The benefit of retaining an audit team’s experience with a particular auditee needs to be carefully balanced with the benefit of adding new auditors who may provide a fresh look at audit issues.

Table 3.5: Audit Quality Indicator – Turnovera of audit personnel

|

Turnover of audit personnel (average annual turnover rate expressed in percentages) |

||

|

Benchmark |

2022–23 |

2021–22 |

|

15-20% |

FSASG staff: 23.3% PASG staff: 26.7% SADA staff: 14.1% PSASG staff: 8.5% |

FSASG staff: 27.1% PASG staff: 15.0% SADA staff: 20.3% PSASG staff: 10.8% |

Note a: Movement between business areas within the ANAO are not counted as turnover in this table; only departures from the ANAO are reported.

3.44 In 2022–23, the turnover rate for FSASG decreased from prior year but remains above the benchmark, while turnover for PASG increased and is now also above the benchmark. Turnover for SADA and PSASG have decreased and are below the benchmark.

3.45 Attrition in the profession, whether in public or private sector auditing, is typically high. As set out in the 2022–23 ANAO Corporate Plan, the ANAO will focus on identifying opportunities and mechanisms to support retention across the ANAO. In 2023–24, the ANAO will continue to implement the initiatives set out in the ANAO Workforce Plan 2022–25, which outlines how we will attract, develop and retain a highly capable workforce to ensure we remain suitably skilled to deliver on our purpose to the Parliament.

Performance and career development

3.46 The ANAO recognises that its reputation relies on high performing individuals. It is important that staff are trusted for their expertise, are effective at engaging others, and contribute to maintaining a supportive and productive workplace. The ANAO’s Performance and Career Development Policy and Procedures have been designed to facilitate high performance across the ANAO, which in turn supports the ANAO to achieve its business and quality objectives and support high audit quality.

3.47 The ANAO performance assessment cycle is from 1 November to 31 October. The results for the performance cycle ending 31 October 2022 are reported in the ANAO Annual Report in Appendix C and 99 per cent of our staff were rated as meeting expectations or higher (31 October 2021: 99 per cent).

Learning and development

3.48 As a learning organisation with a focus on audit quality, the ANAO supports staff with continuous learning and development.

3.49 Regular technical update training sessions are provided to audit staff. Technical updates cover new auditing and accounting standard requirements, financial reporting framework developments, and changes in audit policy and methodology. In 2022–23, 10 technical update sessions were held for FSASG staff, five were held for PASG staff, seven for PSASG staff and 12 for SADA staff.

3.50 In 2022–23, the ANAO delivered a webinar to contractor firms that conduct financial statements audits on behalf of the ANAO to communicate public sector specific audit considerations and lessons learnt from quality assurance reviews.

Table 3.6: Audit Quality Indicator – Training hours per audit professional

|

Training hours per audit professional (average annual hours of continuing professional education by audit service group) |

||

|

Benchmark |

2022–23 |

2021–22 |

|

20 hours |

FSASG and PSASG staff: 119 hours PASG staff: 97 hours |

FSASG and PSASG staff: 112 hours PASG staff: 117 hours |

3.51 The ANAO exceeded the benchmark training hours per audit professional in 2022–23.

3.52 The benchmark for 20 hours of professional development is derived from ANAO Audit Manual policy, which requires that all ANAO staff, including non-audit professionals, complete a minimum of 20 training hours annually. However, many ANAO audit staff are members of professional bodies that have higher continuing professional development requirements and, in practice, average annual training hours at both the ANAO and comparable audit offices significantly exceeds 20 hours. As a result, 2022–23 will be the final year in which the ANAO reports its performance on this AQI against a 20-hour benchmark and, beginning in 2023–24, the benchmark will be increased to 80 hours.6

3.53 The training hours captured in this AQI include all forms of learning and development including internal and external training, the graduate development program and ANAO Talent Management Program. The total training hours reported for audit staff have decreased relative to prior year due to a lower number of graduates commencing during the year compared to 2021–22. However, training hours remain well above the benchmark due to all new starters commencing with the ANAO who required a higher level of training. The graduate development program accounted for 13 per cent of total training hours. In addition to the training hours captured in the AQI, ANAO staff receive on-the-job training, and the ANAO has focused on implementing mentoring and coaching for lateral hires, particularly at the audit manager level.

3.54 The ANAO continues to have a strong focus on learning and development and, as set out in the 2022–23 ANAO Corporate Plan, has been increasing its focus on internal training through a refreshed, integrated learning program – the ANAO Academy. The ANAO Academy is designed to uplift and refine both the technical and non-technical skills required of our people. The Academy encompasses a complete learning and development curriculum tailored to our unique role within the Australian Government sector, the specialist capability required to deliver our audit work, and the leadership potential we will need for the future.

3.55 ANAO staff are also required to complete mandatory e-learning courses.7 A summary of the completion of mandatory e-learning courses as at 30 June 2023 is provided in Table 3.7.

Table 3.7: Staff completion of mandatory e-learning courses

|

2022–23 |

2021–22 |

|

FSASG staff: 99% PASG staff: 97% PSASG staff: 89% SADA staff: 96% PSRG staff: 96% CMG staff: 88% Total ANAO staff: 95% |

FSASG staff: 100% PASG staff: 99% PSASG staff: 100% SADA staff: 96% PSRG staff: 100% CMG staff: 99% Total ANAO staff: 99% |

3.56 Information on the completion of mandatory e-learning courses is regularly reported to the EBOM and GEDs.

Staff workloads

3.57 ANAO polices for the allocation of Engagement Executives and staff to audits ensure that engagement teams have the appropriate level of expertise and time to perform their role. Under these policies the workload and availability of Engagement Executives is monitored to ensure they have sufficient time to adequately discharge their responsibilities. The following audit quality indicator provides information about the time FSASG and PSASG Engagement Executives spend on in-house audits.

Table 3.8: Audit Quality Indicator – Staffing leverage

|

Staffing leverage (ratio of engagement leader hours charged to in-house financial statements and performance statements audit work to lower level audit staff hours) |

||

|

Benchmark |

2022–23 |

2021–22 |

|

0.08 |

FSASG – 0.09 PSASG – 0.18 Total – 0.10 |

FSASG – 0.09 PSASG – 0.19 Total – 0.10 |

3.58 The engagement leader is the Engagement Executive who has direct responsibility for the conduct of an audit and who is either the signing officer or who makes recommendations to the signing officer in respect of the audit opinion. Engagement leaders are responsible for oversight of the audit and the audit team, which will include less experienced staff. Sufficient time to oversee the work of the audit staff is critical to quality.

3.59 In 2022–23, the ratio of engagement leader hours is consistent with the prior year and exceeded the benchmark set by the ANAO. Engagement leader hours in PSASG remained significantly above the benchmark. PSASG was established by the ANAO on 1 July 2021 to conduct performance statements audits, and the performance statements audit program continued to expand in 2022–23. Engagement Executive involvement in these audits is typically high as a result of the new approach and methodology and complexity of issues arising in the audits.

3.60 Table 3.9 sets out the percentage of time spent by the senior members of the audit team including Engagement Executives, Audit Managers and Engagement Quality Reviewers.

Table 3.9: Audit Quality Indicator – Engagement Executive and manager audit workload

|

Engagement Executive and manager audit workload (hours charged by audit staff who are classified as an Engagement Leader, Manager, Engagement Quality Reviewer or higher as a percentage of total hours charged to audits) |

||

|

Benchmark |

2022–23 |

2021–22 |

|

FSASG and PSASG: 22% PASG: 38% |

25% 34% |

25% 32% |

3.61 Excessive workloads could prevent Engagement Executives and audit managers from giving adequate and focused attention to an audit engagement. This measure can provide perspective on the involvement of senior personnel in audits. The lower the amount of senior time, the greater the risk that senior staff will have insufficient time to supervise and review staff work and evaluate audit judgements. Inadequate levels of supervision raise the risk of less effective audit procedures and a reduction in audit quality.

3.62 The Engagement Executive and manager workload was consistent with the benchmark and with the prior year result for financial statements and performance statements audit staff. The performance audit Engagement Executive and manager workload increased from prior year but is lower than the benchmark. The ANAO methodology for capturing Engagement Executive and audit manager workload excludes EL1 level staff. In 2022–23 there were 16 EL1 audit managers in performance audit who are not captured in this result.

Table 3.10: Audit Quality Indicator – Staff audit workload

|

Staff audit workload (chargeable hoursa per full-time equivalent professional) |

||

|

Benchmark |

2022–23 |

2021–22 |

|

FSASG and PSASG: 1,200 hrs PASG: 1,100 hrs |

1,272 1,009 |

1,189 996 |

Note a: Chargeable hours refers to the number of hours charged to audits.

3.63 An excessive workload increases the risk that staff may have insufficient time to appropriately perform the necessary audit procedures and steps that deliver a quality audit. Staff may become less effective when working long hours. The requirement that audit team members have sufficient time to perform a quality audit is set out in the new and revised Australian Quality Management Standards, including ASQM 1.

3.64 In 2022–23, staff audit workload for financial statements and performance statements audit staff increased from prior year but remains in line with the benchmark. The workload measure for performance audit staff also increased from the prior year but remains below the benchmark. As noted in paragraph 3.53, the increased numbers of new starters who required a higher level of training impacted the hours charged to audit. The focus on coaching and mentoring from experienced staff also impacted on the staff audit workload as the time spent coaching and mentoring new starters is not captured in the audit time. Hours charged to mentoring and coaching staff by performance audit staff during 2022–23 increased by 50% compared to 2021–22.

3.65 The objective of the ANAO resourcing model and policies is to ensure that staff have sufficient capacity to undertake a quality audit, and Engagement Executives and audit managers have sufficient time to not only undertake appropriate review and supervision, but also to coach and mentor staff to improve staff capability and development.

Internal and external specialists and technical resources

3.66 PSRG provides internal professional services such as technical accounting and audit support, quality assurance and legal services. Access to technical accounting and auditing resources enables audit teams to consult on complex matters identified during an audit. As set out in paragraphs 3.33 and 3.34, QTAC also provides a forum for consultation on complex matters; PSRG acts as secretariat to QTAC.

3.67 Table 3.11 shows the ANAO expenditure on technical accounting and auditing resources, including PSRG accounting and audit technical and legal staff costs and methodology support and training expenditure.

Table 3.11: Audit Quality Indicator – Technical accounting and auditing resources

|

Technical accounting and auditing resources (percentage of total office expenditure allocated to technical resources) |

||

|

Benchmark |

2022–23 |

2021–22 |

|

2.0% |

2.6% |

2.4% |

3.68 The expenditure on technical resources in 2022–23 has increased from prior year and is above the ACAG benchmark. The increase is attributable to:

- additional methodology support and training related to the implementation of the revised auditing standard ASA 315 Identifying and Assessing the Risks of Material Misstatement; and

- increase in PSRG staff providing technical resources required to support the continued expansion of the performance statements audit program.

3.69 In addition to the resources captured in the AQI above, to further support the delivery of quality audits, the ANAO also uses external subject matter and technical experts where a specific need has been identified, including:

- the engagement of audit firms to conduct financial statements audits when specialist industry knowledge is not readily available in-house; and

- the engagement of auditor experts in both financial statements and performance audits as required.

Technological resources

3.70 The ANAO SADA group supports audit evidence-gathering and analysis through providing Information Technology (IT) and data specialists with audit capability for analysing the IT environment, IT general and application controls, system-generated reports, and data. In previous years, SADA developed several standardised data analytics solutions to provide a standard, data-driven approach to some of the common areas of financial statements audit testing to improve the efficiency of audit procedures, while enhancing audit quality. In 2022–23, this included a new enhanced standardised data analytics solution for the testing of appropriations which was piloted in 2021–22.

3.71 The standardised data analytics solutions have been designed to support teams in executing the procedures by providing standardised data requests and templates and identifying exceptions and risk areas for further investigation. This allows teams to spend more time focusing on judgements and conclusions rather than developing their own processes. PSRG reviews and approves the standardised solutions to ensure alignment with the ANAO’s audit methodology.

Intellectual resources

3.72 ANAO auditors apply a robust methodology which includes the ANAO Audit Manual and standardised tools and templates to assist in the consistent application and documentation of audit procedures. Application of this methodology ensures compliance with the ANAO Auditing Standards and provides for consistent quality across audits.

3.73 The ANAO Audit Manual, methodology and supporting tools and templates are reviewed on an annual basis. The review process incorporates any improvements or amendments arising from changes in the ANAO auditing standards, responses to findings from quality monitoring processes and audit staff consultation. In 2022–23, key updates to the methodology included:

- revision of the ANAO Audit Manual to incorporate the requirements of the new and revised quality management standards, including:

- enhanced policies addressing leadership responsibility for quality, engagement quality reviews, and monitoring and remediation; and

- new policies addressing technological and intellectual resources and the evaluation of the ANAO Quality Management Framework.

- finalisation of a performance statements audit manual;

- development of a methodology for auditing ethics;

- commencement of a review of the performance audit methodology for audits of efficiency; and

- implementation of the revised auditing standard ASA 315 – Identifying and Assessing the Risks of Material Misstatement.

Information and communication

Information systems

3.74 The ANAO uses a number of information systems which supports its system of quality management and the performance of engagements, including:

- TeamMate – the ANAO’s project management software, which is used to retain an electronic version of the audit file;

- E-Hive – the ANAO’s enterprise document management system;

- Saviom – the ANAO’s enterprise resource management and workforce planning system;

- Aurion Timekeeper – the ANAO’s time recording system;

- Learning Management System;

- SharePoint – the ANAO intranet;

- ANAO website;

- data analytics tools and e-discovery tools; and

- Microsoft applications such as Excel and Teams.

3.75 CMG is the systems owner of the information systems used to support the ANAO’s system of quality management. CMG is responsible for resolving issues affecting systems.

3.76 Change across the ANAO is supported by a structured approach to strategic planning, governance, risk management and change management. Changes implemented in 2022–23 included:

- A new learning management system, facilitating staff access to both the ANAO’s in-house learning and development content and third-party applications such as LinkedIn Learning;

- High-capacity data storage and discovery tools to enhance data analytics, modelling and automation;

- Cybersecurity initiatives, including the implementation of security controls to increase the ANAO’s cyber resilience; and

- Migration of selected applications into the ANAO’s Azure environment to realise efficiencies.

Communication within the ANAO

3.77 The ANAO encourages collaboration and information-sharing between staff in accordance with the Auditor-General Act and the Protective Security Policy Framework. ANAO audit manual policies and processes support collaboration between audit service groups.

3.78 New starter and induction training programs are designed to provide new starters with all necessary information relevant to their duties. In 2022–23, 78 per cent of new starters completed mandatory new starter training within one month of commencing. For ANAO staff more generally, regular technical updates inform staff about any changes to aspects of the system of quality management, including changes to Audit Manual policies, methodology and templates (see paragraph 3.49).

Communication with external parties

3.79 The ANAO communicates with external parties including auditees, service providers, Parliament, the Australasian Council of Auditors General8 and the International Organisation of Supreme Audit Institutions.9

3.80 The ANAO communicates with Financial Statement and Performance Statement preparers and Audit Committee Chairs by holding two forums for each of these groups annually.

3.81 ANAO representatives attend, as observers, audit committee meetings of Commonwealth entities and Commonwealth companies. Engagement Executives are also responsible for communicating with the accountable authority of an entity.

3.82 The ANAO provides all relevant ANAO policies and templates to contracted service provider firms via the GovTeams contractor community page. Additionally, annual webinars communicate changes to policies, templates and requirements (see paragraph 3.50) and regular notifications communicate the release of new information. For contract staff, onboarding processes include mandatory online modules specifically designed to set out expectations for contractors. Additionally, the ANAO Audit Manual makes clear that the requirements which apply to contractors are consistent with those which apply to ANAO staff.

Monitoring and remediation process

Internal and external quality assurance reviews

3.83 A key element of the ANAO Quality Management Framework is the monitoring of compliance with policies and procedures through internal and external QA reviews of the ANAO’s audits and other assurance engagements. The monitoring program is designed to provide the Auditor-General with assurance that engagements comply with the ANAO Auditing Standards, relevant regulatory and legal requirements, and ANAO policies; and that reports issued are appropriate in the circumstances. PSRG is responsible for delivering the monitoring program, including the coordination of external reviews. PSRG reports to EBOM, the Quality Committee and the ANAO Audit Committee on the results of each quality assurance review and other monitoring activities.

3.84 Monitoring activities conducted in 2022–23 were:

- annual quality assurance reviews of completed audits (ten financial statements audits, two performance audits and one performance statements audit reviewed);

- real-time quality reviews of four in-progress financial statements audits and one inprogress performance statements audit;

- external review of two completed financial statement audits conducted by the Australian Securities and Investments Commission (ASIC); and

- biennial external peer review of two completed performance audits performed by the Office of the Auditor General New Zealand (OAG NZ).

Internal quality assurance reviews

3.85 The ANAO selects audits and other engagements for QA review in accordance with the requirements of the ANAO Audit Manual to provide coverage of all responsible Engagement Executives at least once every three years. The 2022–23 results in relation to quality assurance review coverage are provided in Table 3.12. The results reflect internal quality assurance reviews, including complete real-time reviews, and external reviews conducted by ASIC and OAG NZ but does not include focused real-time reviews and internal audit compliance reviews.

Table 3.12: Audit Quality Indicator – Quality assurance review coverage

|

Quality assurance review coverage (percentage of Engagement Executives and contracted firms subject to review annually) |

||

|

Benchmark |

2022–23 |

2021–22 |

|

FSASG – in house: 33% |

35% |

47% |

|

FSASG – contracted firm: 33% |

33% |

29% |

|

PASG: 33% |

33% |

38% |

|

PSASG: 33% |

33% |

33% |

3.86 In 2022–23 the coverage of Engagement Executives for in-house financial statements audits, performance audits and performance statements audits were in line with the policy requirements which form the basis of the AQI benchmark. The coverage for contracted firms for financial statements audits was also in line with the benchmark.

3.87 Table 3.13 provides the number of audit files reviewed in the ANAO quality review program that were rated as unsatisfactory.

Table 3.13: Audit Quality Indicator – Internal quality review results

|

Internal quality review results (number of audit files rated as ‘Unsatisfactory’ in the ANAO Annual Inspection Program) |

||

|

Benchmark |

2022–23 |

2021–22 |

|

No. of engagements: 0 |

5 |

1 |

3.88 In 2022–23, four completed financial statements audit files reviewed were determined to be unsatisfactory. Three of the audit files did not contain sufficient appropriate audit evidence to support the conclusions issued and, in the remaining unsatisfactory audit file, a significant finding was identified in the work performed over the implementation and operating effectiveness of IT general controls. The ANAO selects audits for quality review with a bias towards higher risk audits or indicators of potential audit quality deficiencies in addition to the cyclical coverage outlined in paragraph 3.83. Two of the unsatisfactory audit files were selected for review based on concerns with the quality of work undertaken by two contracted audit firms.

3.89 The completed performance statements audit file reviewed was also determined to be unsatisfactory. A significant finding was identified related to the documentation of audit work where the performance statements audit team relied on work conducted by the financial statements audit team. The performance statements audit file did not contain sufficient information to document the nature, timing and extent of the procedures performed and the final agreed audit strategy.

3.90 Remediation procedures were completed in all unsatisfactory financial statements and performance statements audits to determine that the audit conclusions were appropriate despite the deficiencies identified. The remediation procedures included enhancing audit documentation to capture significant judgements made during the audit and the redesign and completion of a substantive analytical review in one audit. Following review of the remediated audit documentation, the ANAO is satisfied that all financial statements audit, performance audit and performance statements audit conclusions subject to monitoring were appropriate. As a result, in 2022–23 the ANAO met the target for performance measure 17 reported in the ANAO Annual Report (‘The ANAO independent quality assurance program indicates that audit conclusions are appropriate’).

Table 3.14: Summary of quality assurance review findings in the annual inspection program

|

|

2022–23 |

2021–22 |

|

FSASG – Completed audits |

10 2021–22 audits inspected 6 significant findings 17 moderate findings 28 minor findings |

10 2020–21 audits inspected 1 significant finding 16 moderate findings 41 minor findings |

|

FSASG – Real time review |

4 2021–22 audits inspecteda No significant findings 1 moderate finding 5 minor findings |

8 2020–21 audits inspectedb No significant findings 8 moderate findings 10 minor findings |

|

PASG |

2 audits inspected (tabled year to 31 March 2023) No significant findings 10 moderate findings 8 minor findings |

3 audits inspected (tabled year to 31 March 2022) No significant findings 11 moderate findings 13 minor findings |

|

PSASG – Completed audits |

1 2021–22 audit inspected 1 significant finding 3 moderate findings 3 minor findings |

1 2020–21 audit inspected No significant findings 4 moderate findings 8 minor findings |

|

PSASG – Real time review |

1 2021–22 audit inspected No significant findings No moderate findings 4 minor findings |

2 2020–21 audits inspected No findings identified Observations made only |

Note a: Of the four real time reviews, two were complete reviews and two were focused reviews. A complete review assesses the audit file as a whole, whereas a focused review is targeted at a particular type of procedure.

Note b: Of the eight real time reviews, one was a complete review and seven were focused reviews.

3.91 A high number of findings from quality reviews, particularly when these are repetitive, indicates issues with audit quality. Timely identification and appropriate remediation of issues is necessary to facilitate improvements in audit quality.

3.92 The identified areas for improvement in financial statements audits related to the design and execution of substantive analytical procedures, execution of procedures and documentation related to auditing accounting estimates, audit procedures over appropriations and documentation of IT audit testing approaches and judgements. In addition to the performance of remedial procedures on the unsatisfactory audits, in 2023–24 the ANAO will be undertaking further actions to address these areas of improvement, including a review of induction procedures for contractors and new starters, additional monitoring of training attendance and resourcing, and enhancements to procurement and contract management procedures to place additional emphasis on quality.

3.93 The identified areas for improvement in performance audits related to compliance with independence policy requirements, record-keeping, assessing the completeness and accuracy of auditee-generated information and engagement with the SADA group. In 2022–23 the ANAO commenced the root cause analysis of findings raised in the PASG completed audits review. The report was finalised in August 2023. Follow-up actions designed to address the root causes of findings will be implemented in 2023–24. (Root cause analysis is further discussed from paragraph 3.99 below.)

3.94 The quality assurance reviews over performance statements audits identified areas where policy or guidance, or clearer methodology procedures, are needed regarding effective engagement with other ANAO audit teams when performance statements audit teams rely on the work conducted by other teams, effective and timely audit planning, and documentation of audit judgements. In addition to remedial procedures, in 2023–24 the ANAO will address the opportunities for improvement by requiring more senior staff involvement in engagement with other audit teams, enhancing arrangements for monitoring of complex procedures, and introducing enhanced documentation requirements.

External and internal audits and external quality assurance and peer reviews

3.95 The Act establishes the position of the Independent Auditor, who may conduct a performance audit of the ANAO at any time. The most recent Independent Auditor report, Performance Audit of Attraction, Development and Retention of Capability, was tabled in Parliament on 15 August 2022. The Independent Auditor found that the ANAO had effective strategies, plans and processes in place to identify, quantify, attract, develop and retain the necessary capability required, and that there were appropriate governance arrangements in place. The Independent Auditor also made four recommendations to the ANAO. The ANAO publishes the status of recommendations made in Independent Auditor reports on the ANAO website.

3.96 In 2022–23, the ANAO continued the arrangement, initiated in 2017–18, with ASIC to conduct an annual external independent review of the ANAO’s financial statements audit files. This is similar to the review work conducted by ASIC on external auditors in the private sector. The reviews are valued by the ANAO as they provide external scrutiny and the ANAO recognises the important role that openness to evaluation plays in building a culture focused on quality, learning and continuous improvement. This year, two audits of financial statements for the year ended 30 June 2022 were reviewed. These reviews were conducted using ASIC’s methodology for reviewing private sector audits. In respect of the file reviews, ASIC made a finding on the extent of procedures performed over management inputs and assumptions related to the recognition and measurement of capitalised work in progress and raised an ‘other matter’ related to a substantive analytical review. The reports from the ASIC annual review are published on the ANAO website.

3.97 In 2022–23, the Office of the Auditor-General New Zealand (OAG NZ) conducted a peer review over two performance audits. The ANAO and the OAG NZ have a longstanding arrangement to conduct reciprocal performance audit peer reviews annually on a rotating basis. COVID-19 and travel restrictions prevented the reviews from being conducted in 2020 and 2021 and the reviews were undertaken concurrently in 2022. The OAG NZ’s peer review of the ANAO’s work identified opportunities for improvement regarding IT Audit Executive review of key documents and working papers, timely file finalisation and documentation of materiality considerations. The report on the results of the peer review is published on the ANAO website alongside the previous NZ OAG peer review reports.

3.98 In 2022–23, the ANAO’s internal auditor conducted a review on compliance with selected ANAO Audit Manual policies, including completion of independence declarations, agreement of scope of work with the SADA group, sign-off of planning documentation prior to interim work, use of risk assessment and test program templates, sign-off of planning meeting minutes and discussion of fraud risks. Four low risk recommendations were made. Each was rated low risk. Recommendations were made regarding communicating and messaging on the importance of independence declaration sign-offs, timely review of planning, sign-offs of planning meeting minutes, and updates to methodology guidance on documentation of SADA involvement and results of work performed.

Root cause analysis

3.99 The conduct of root cause analysis on deficiencies to determine their nature, severity and effect on the system of quality management is a requirement of ASQM 1.10 The ANAO has been undertaking root cause analysis of deficiencies identified in in-house financial statements audit files for several years prior to the entry into force of ASQM 1. The ANAO is expanding its root cause analysis program to meet the requirement of the new standards that all deficiencies be subject to root cause analysis.

3.100 In 2022–23, the ANAO continued to use root cause analysis of significant findings and thematic findings from the inspections of 2021–22 financial statements audit files to identify the root cause of findings and determine the most appropriate remedial actions. The root cause analysis was completed concurrently with the finalisation of the inspections. Follow-up actions arising from the analysis included review of induction processes for contractors and new starters, review of resource allocation processes, and revisions to procurement processes and contract terms to incorporate audit quality considerations.

3.101 Root cause analysis over the thematic findings identified in the performance audit quality assurance review will be conducted in 2023–24 to understand the underlying drivers of identified deficiencies and develop targeted follow-up actions. Any findings arising from the quality assurance review of 2022–23 performance statements audits will also be subject to root cause analysis.

Remediation

3.102 The results of internal and external quality assurance reviews, root cause analysis, external and peer reviews, and relevant internal and external audits are reported to EBOM. The report includes the recommended follow-up actions to address any identified findings, recommendations or observations. The follow-up actions are assigned to responsible officers with timeframes for completion.

3.103 The ANAO Quality Committee is responsible for monitoring the ANAO’s progress in addressing the findings and recommendations arising from external or internal quality assurance reviews, including assessing the prioritisation of active follow-up actions, and reports on this to EBOM. Table 3.15 details the status of findings arising from internal and external reviews.

Table 3.15: Summary of quality assurance review findings in the annual inspection program

|

Category |

Opening position 1 July 2022 |

New follow-up action items |

Resolved follow up action items |

Closing position 30 June 2023 |

|

FSASG |

20 |

28 |

32a |

16 |

|

PASG |

6 |

13 |

6 |

13 |

|

PSASG |

8 |

8 |

10 |

6 |

|

ANAO |

1 |

2 |

2 |

1 |

|

Total |

35 |

51 |

50 |

36 |

Note a: Includes two related action items which were merged, and which are counted as one resolved item.

3.104 The ANAO Audit Committee reviews the outcomes of internal and external quality assurance reviews. The Audit Committee also monitors the progress of ANAO action items to address recommendations from external reviews and internal audits. In 2022–23, the Audit Committee reviewed five internal quality assurance review reports, one root cause analysis report, the external ASIC quality assurance review report, the NZ OAG peer review report and internal audit reports.

3.105 Findings from monitoring processes are communicated to ANAO audit staff and contract firms, through technical updates (see paragraph 3.49) and the annual contractor webinar (see paragraphs 3.50 and 3.82), to allow all staff to implement lessons learnt and to foster continuous improvement.

Complaints and allegations

3.106 The ANAO Audit Manual sets policies and processes for the formal management of any complaints or allegations that the work performed by the ANAO does not comply with applicable standards, requirements, systems of quality management or independence policies.

3.107 During 2022–23 the ANAO received no complaints or allegations.

4. Quality assurance strategy and deliverables for 2022–23

4.1 The key deliverables for 2021–22 were set out in the Quality Assurance Framework and Plan 2022–23. The achievement of the strategy and deliverables are set out below in Table 4.1.

Table 4.1: 2022–23 Quality Assurance Framework and Plan deliverables

|

Quality framework element |

High level objectives |

Brief scope of work |

Target completion date |

Outcome |

|

All elements |

To ensure that the ANAO Quality Assurance Framework is compliant with the new Quality Management Standards to be incorporated into the ANAO Auditing Standards |

Implement enhancement to the ANAO Quality Assurance Framework in compliance with ASQM 1, ASQM 2 and ASA 220 (Revised) |

15 December 2022 |

Completed 23 March 2023 |

|

Engagement performance

|

To ensure that the ANAO audit methodology is compliant with the ANAO Auditing Standards

|

Annual audit manual review - financial statement audits |

31 March 2023 |

Completed 12 May 2023 |

|

Annual audit manual review - performance audits |

30 April 2023 |

Not completed as at 30 June 2023 Completed 6 July 2023 |

||

|

Annual audit manual review – performance statements audit |

31 March 2023 |

Completed 12 May 2023 |

||

|

Annual financial statement audit methodology and template updates |

30 November 2022 |

Completed 7 November 2022 |

||

|

Annual assessment of performance audit methodology and template updates |

30 April 2023 |

Not completed as at 30 June 2023 Completed 13 September 2023 |

||

|

Annual performance statements audit methodology and template updates |

30 November 2022 |

Completed 6 December 2022 |

||

|

Annual communication template updates |

30 June 2023 |

Completed 30 April 2023 |

||

|

To ensure ANAO staff are supported in the application of ANAO audit methodology and ANAO Auditing Standards |

Financial statements audit peer review program |

31 October 2022 |

Completed 30 November 2022 |

|

|

To maintain a high level of audit quality by keeping ANAO staff knowledge up-to-date and fostering continuous improvement