Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 17 of 2025–26

Audits of the Financial Statements of Australian Government Entities for the Period Ended 30 June 2025

Published

Thursday 18 December 2025

Portfolio

Across Entities

Entity

Across Entities

Contact

Please direct enquiries through our contact page.

Executive summary

Introduction

1. This report presents the results of the ANAO’s 2024–25 financial statements audits. This includes the results of the audits of 243 Australian Government entities, including the Australian Government’s Consolidated Financial Statements (CFS).

2. The assessments included in this report are as at 30 June 2025 and the entity names, responsibilities and portfolio allocations used in this report reflect the Administrative Arrangements Orders (AAOs) in place as at that date. Revised AAOs were subsequently made that transferred functions between entities.

Consolidated financial statements

Audit results

3. The Consolidated Financial Statements (CFS) presents the whole of government and the General Government Sector financial statements. The 2024–25 CFS were signed by the Minister for Finance on 23 November 2025, and an unmodified auditor’s report was issued on 25 November 2025.

4. Without modifying the audit opinion, the auditor’s report included an emphasis of matter which draws attention to the accounting policies that describe the inherent uncertainty associated with a number of the assumptions used in the calculation of the Department of Veterans’ Affairs’ (DVA) military compensation provisions and the sensitivity of the valuation of the provision to changes in these assumptions.

5. There were no significant or moderate audit issues identified in the audit of the 2024–25 CFS.

Australian Government financial performance and position

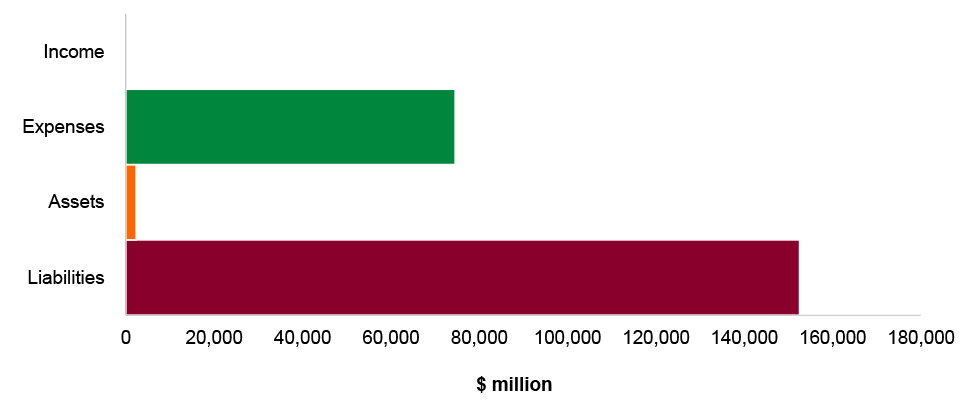

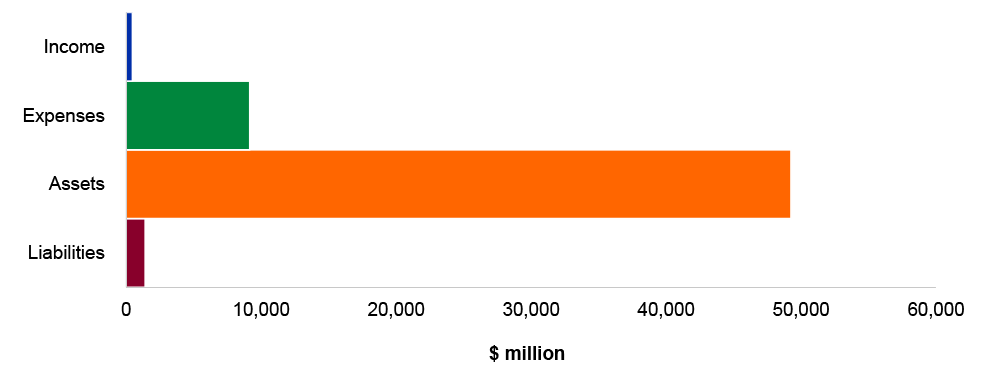

6. The Australian Government reported a net operating balance of a deficit of $41.2 billion ($10.1 billion surplus in 2023–24). The deficit is because expenses outpaced revenue growth in 2024–25. Revenue grew by $29.8 billion (4.1 per cent) while expenses grew by $81.1 billion (11.3 per cent). The largest contributors to the growth in expenditure in 2024–25 was the National Disability Insurance Agency’s participant expenses which increased by $4.5 billion from 2023–24, and DVA’s health care payments and provisions which increased by $22.0 billion from 2023–24.

7. The Australian Government’s net worth position deteriorated from negative $573.7 billion in 2023–24 to negative $632.4 billion in 2024–25 mainly due to a significant increase in liabilities associated with DVA’s military compensation provisions, which grew by $59.7 billion in 2024–25 (see paragraphs 2.1 to 2.19).

Financial audit results

Audit findings

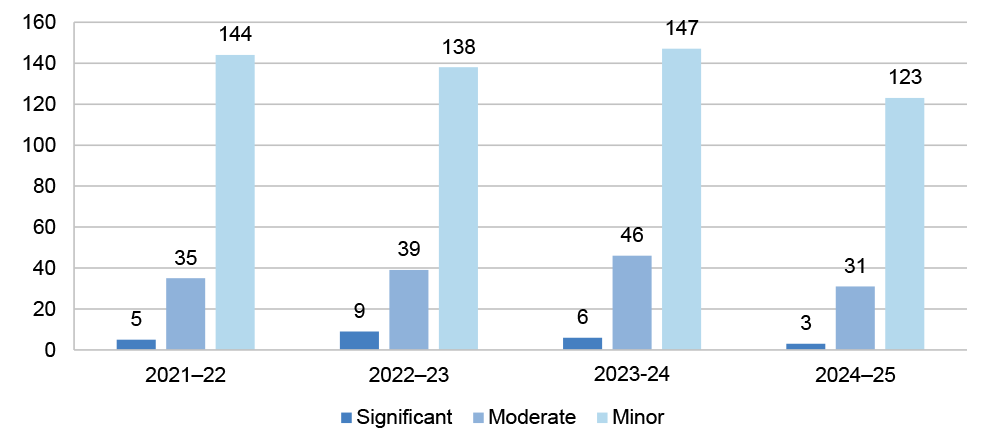

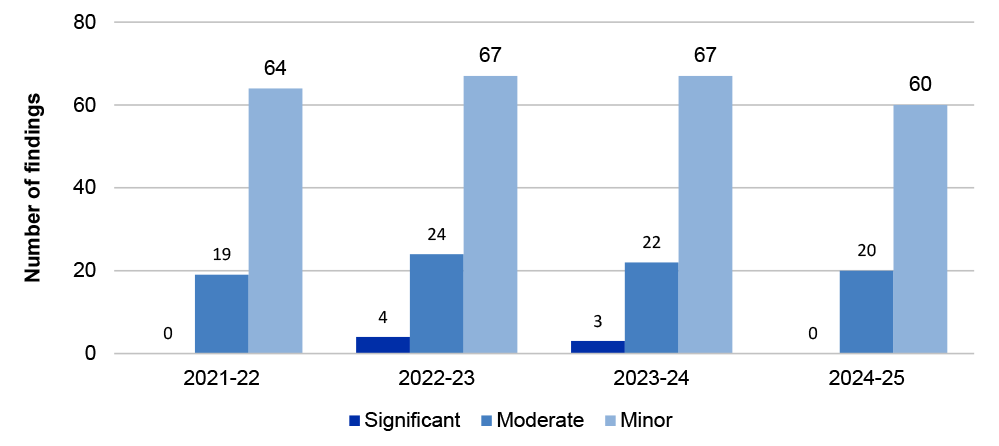

8. Across all financial statements audits, the number of audit findings identified by the ANAO has decreased from 2023–24. A total of 178 audit findings and legislative non-compliance were reported to entities at the conclusion of the 2024–25 financial statements audits (2023–24: 214). These comprised three significant (2023–24: six), 31 moderate (2023–24: 46) and 123 minor (2023-24: 147) audit findings, and 21 instances of legislative non-compliance (2023–24: 15).

9. The three significant audit findings related to compliance and quality assurance frameworks and the accounting and control of non-financial assets and were reported for the Department of the House of Representatives, the Royal Australian Mint, and Services Australia.

10. Seven of the instances of legislative non-compliance related to significant legislative breaches and were reported for the Australian Centre for International Agricultural Research, the Australian Pesticides and Veterinary Medicines Authority, the Department of Health, Disability and Ageing, the Department of the House of Representatives, the Northern Land Council, Tiwi Land Council, and Services Australia.

11. A further seven instances of legislative non-compliance related to incorrect payments of remuneration to key management personnel and/or non-compliance with determinations made by the Remuneration Tribunal and were reported for the Australian Renewable Energy Agency, the Australian Sports Commission, the Australian Fisheries Management Authority, Indigenous Business Australia, WSA Co Limited, the Australian Film, Television and Radio School, and the Australian Institute of Family Studies.

12. IT controls remain a key issue. Forty-five per cent of all audit findings identified by the ANAO related to the IT control environment, particularly IT security. Weaknesses in controls in this area can expose entities to an increased risk of unauthorised access to systems and data, or data leakage. The number of IT findings identified by the ANAO indicate that there remains room for improvement across the sector to enhance governance processes supporting the design, implementation and operating effectiveness of controls. These matters extend beyond technical IT concerns; they pose significant business risks to the security and the integrity of information systems. Addressing these fundamentals is essential in an environment where entities increasingly rely on technology, including artificial intelligence (AI).

Compliance with Section 83 of the Australian Constitution

13. Section 83 of the Australian Constitution (section 83) provides that no money shall be drawn from the Treasury of the Commonwealth except under appropriation made by law.

14. The Australian Government’s financial reporting framework requires entities to disclose in their financial statements whether a breach has occurred or may have occurred during the reporting period. During 2024–25, 11 entities (2023–24: 10 entities) reported breaches of section 83. (see paragraphs 3.67 to 3.71).

Quality and timeliness of financial statements preparation

15. The ANAO had issued 238 auditor’s reports as at 30 November 2025. The financial statements were finalised and auditor’s reports issued for 82 per cent (2023–24: 79 per cent) of entities within three months of financial year-end.

16. A quality financial statements preparation process will reduce the risk of inaccurate or unreliable reporting. Seventy-four per cent of entities delivered financial statements in line with an agreed timetable (2023–24: 71 per cent). The total number of adjusted and unadjusted audit differences decreased during 2024–25, although 28 per cent of audit differences remained unadjusted (2023–24: 38 per cent).

17. Improvements in the quality and timeliness of financial statements preparation supports observations made by the ANAO that financial reporting processes across the Australian Government sector continues to improve (see paragraphs 3.72 to 3.82).

Timeliness of annual reports

18. Annual reports inform the Parliament, the community and other stakeholders about the performance of entities. Annual reports are approved by the entity’s accountable authority before being provided to the minister and tabled in Parliament.

19. Annual reports that are not tabled in a timely manner before budget supplementary estimates hearings decrease the opportunity for the Senate to scrutinise an entity’s performance. For the 2024–25 reporting period, supplementary estimates hearings were held from 7 to 10 October 2025, and from 1 to 4 December 2025. Twelve per cent of entities tabled annual reports before the October hearings, and 90 per cent of entities tabled annual reports before the December hearings. Of the entities required to table an annual report, 10 per cent had not tabled an annual report as at 30 November 2025 (see paragraphs 3.11 to 3.24).

Fraud and Corruption control frameworks are largely in place

20. The Commonwealth Fraud and Corruption Control Framework 2024 (the Framework) came into effect on 1 July 2024. The Framework captures amendments to the Public Governance, Performance and Accountability Rule 2014, strengthening requirements for Australian Government entities to prevent, detect and deal with fraud and corruption.

21. The ANAO observed that all non-corporate and corporate Commonwealth entities had established a fraud and corruption control plan. Commonwealth companies are not bound by the requirements of the PGPA Rule, however, the ANAO observed that 20 per cent of all Commonwealth companies had adopted the requirements of the Framework as better practice. (see paragraphs 3.112 to 3.125).

Financial sustainability

22. The ANAO’s analysis concluded that the financial sustainability of the majority of entities was not at risk, however, 46 per cent of not-for-profit entities reported a deficit in 2024–25, and 33 per cent of for-profit entities reported a deficit in 2024–25 (see paragraphs 3.83 to 3.111).

1. Introduction

1.1 The ANAO prepares two reports annually that provide insights at a point in time to the financial statements risks, governance arrangements and internal control frameworks of Australian Government entities, drawing on information collected during our audits.

1.2 This report is the second of the two reports and focuses on the results of the 2024–25 financial statements audits, including the audit of the Australian Government’s Consolidated Financial Statements (CFS).

Entities included in this report

1.3 This report examines all Commonwealth entities, Commonwealth companies and their subsidiaries that are required to prepare annual financial statements. In 2024–25, this comprised 243 entities (2023–24: 244), including the CFS.

1.4 The assessments included in this report are as at 30 June 2025 and the entity names, responsibilities and portfolio allocations used in this report reflect the Administrative Arrangements Orders (AAOs) in place as at that date.1 Revised AAOs were made that subsequently transferred functions between entities.

1.5 Appendix 1 lists all entities that are included in this report.

ANAO financial statements audits

1.6 The Auditor-General Act 1997 establishes the mandate for the Auditor-General to undertake financial statements audits of all Australian Government entities. The Public Governance, Performance and Accountability Act 2013 (PGPA Act) requires Commonwealth entities, Commonwealth companies and their subsidiaries to prepare annual financial statements, and for the Auditor-General to audit and report on, those annual financial statements.2

1.7 The Australian Government’s financial reporting framework is primarily based on standards made independently by the Australian Accounting Standards Board (AASB).

1.8 The AASB bases its accounting standards on the International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board. As IFRS are designed primarily for use by private sector and for-profit organisations, the AASB amends the IFRS to reflect significant transactions and events unique to the public sector and not-for-profit private sector. In doing so, the AASB considers standards issued by the International Public Sector Accounting Standards Board (IPSASB).

1.9 The PGPA Act requires Commonwealth entities to apply Australian accounting standards when preparing financial statements. In addition to Australian accounting standards, the Minister for Finance prescribes additional financial reporting requirements for Commonwealth entities via the Public Governance, Performance and Accountability (Financial Reporting) Rule 2015 (FRR).

1.10 The audits of the financial statements of Australian Government entities are conducted in accordance with the ANAO Auditing Standards, which are made by the Auditor-General under section 24 of the Auditor-General Act 1997 (A-G Act). The ANAO Auditing Standards incorporate, by reference, the auditing standards made by the Australian Auditing and Assurance Standards Board (AUASB). The AUASB bases its standards on those made by the International Auditing and Assurance Standards Board (IAASB), an independent standard setting board of the International Federation of Accountants.

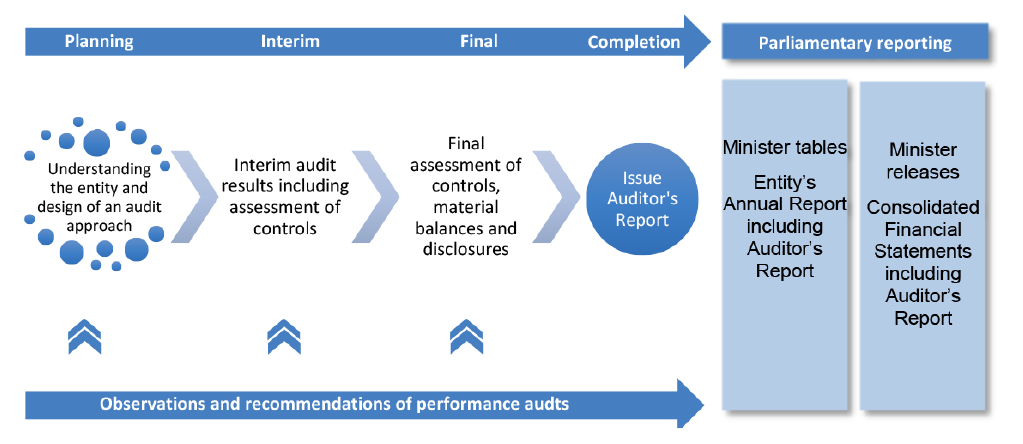

1.11 The ANAO conducts its financial statements audits in four phases: planning, interim, final and completion. Figure 1.1 outlines the key elements of each phase.

Figure 1.1: ANAO financial statements audit process

Source: ANAO.

Engagement Risk

1.12 The ANAO assesses engagement risk on an annual basis. Engagement risk includes the risks of material misstatement relating to a financial statements audit engagement, and other professional risks such as reputational and litigation risks. The determination of engagement risk provides a basis to determine whether additional quality management responses, in accordance with the Auditing Standards, are required.

1.13 Eight of the entities included in this report have been assessed as having a high engagement risk for 2024–25 (2023–24: 10 entities).

1.14 Table 1.1 shows entities with a high engagement risk rating for 2023–24 and 2024–25.

Table 1.1: Entities with a high engagement risk rating for 2023–24 and 2024–25

|

Entity |

Engagement Risk Rating 2023–24 |

Engagement Risk Rating 2024–25 |

|

Australian Rail Track Corporation Ltd |

High |

High |

|

Australian Taxation Office |

High |

High |

|

Department of Climate Change, Energy, the Environment and Water |

High |

Moderate |

|

Department of Defence |

High |

High |

|

Department of Health, Disability and Ageing |

High |

High |

|

Department of Home Affairs |

High |

High |

|

Inland Rail Pty Ltd |

High |

Moderate |

|

National Disability Insurance Agency |

High |

High |

|

NBN Co Limited |

High |

High |

|

Services Australia |

High |

High |

Key Audit Matters

1.15 Communicating Key Audit Matters (KAM) helps users of financial statements better understand those matters that, in the auditor’s professional judgement, were of the most significance in the audit of the financial statements3.

1.16 While ASA 701 Communicating Key Audit Matters in the Independent Auditor’s Report (ASA 701) requires KAM reporting only for listed entities, the Auditor-General considers including KAM to be good practice for financial statements auditing in the public sector and includes KAM in certain audit reports.

1.17 The ANAO has reported KAM in 2024–25 for the entities included in Auditor-General Report No. 39 2024–25 Interim Report on Key Financial Controls of Major Entities and the Consolidated Financial Statements (CFS). In 2024–25, a total of 60 KAM were reported across 27 entities, consistent with 2023–24. The majority of KAM related to the accuracy, valuation and allocation of assets and liabilities, including:

- advances, loans and other receivables, including accounting for concessional loans and expected credit losses;

- non-financial assets including property, plant and equipment and specialist military equipment, including investment properties;

- investments in listed or unlisted entities, foreign currency and other investment products;

- intangibles, including computer software;

- treasury bonds and notes (Australian Government Securities);

- leases; and

- provisions, including defined benefit superannuation funds, personal benefits and military compensation provisions.

1.18 Other KAM included: completeness and accuracy of expenses relating to personal benefits and grants; and completeness and accuracy of revenue relating to taxation, levies, customs duty, royalty and other revenue arising from fees and charges. Further details of the KAM reported to entities are included in the discussion of results of financial statements audits in Chapter 4.

Key Areas of Financial Statements Risk

1.19 The ANAO’s risk assessment process identifies key areas that have the potential to materially impact an entity’s financial statements. The ANAO’s risk assessment process considers the nature of the financial statements items, the results of recent ANAO performance audits and an understanding of the entity’s environment and governance arrangements, including its financial reporting regime and system of internal control.

1.20 The ANAO undertakes appropriate audit procedures on all material items and focusses audit effort on those areas that are assessed as having a higher risk of material misstatement. The ANAO also assesses the IT general and application controls for key systems that support the preparation of an entity’s financial statements.

Audit Findings

1.21 Audit findings are raised in response to the identification of a potential business or financial risk posed to an entity. Weaknesses in internal controls increase the possibility that a material misstatement of an entity’s financial statements will not be prevented or detected in a timely manner. The ANAO rates audit findings according to the potential business or financial management risk posed to the entity. The rating scale is presented in Table 1.2.

Table 1.2: Findings rating scale

|

Rating |

Description |

|

Significant (A) |

Issues that pose a significant business or financial management risk to the entity. These include issues that could result in a material misstatement of the entity’s financial statements. |

|

Moderate (B) |

Issues that pose a moderate business or financial management risk to the entity. These may include prior year issues that have not been satisfactorily addressed. |

|

Minor (C) |

Issues that pose a low business or financial management risk to the entity. These may include accounting issues that, if not addressed, could pose a moderate risk in the future. |

|

Significant legislative breach (L1) |

Instances of significant potential or actual breaches of the Constitution; and instances of significant non-compliance with the entity’s enabling legislation, legislation that the entity is responsible for administering, and the PGPA Act. |

|

Other non-compliance with legislation (L2) |

Other instances of non-compliance with legislation the entity is required to comply with. |

|

Non-compliance with subordinate legislation (L3) |

Instances of non-compliance with subordinate legislation, such as the PGPA Rule. |

2. The Consolidated Financial Statements

Background

2.1 Government accountability and transparency is supported by the preparation and audit of the Australian Government’s Consolidated Financial Statements (CFS). The CFS and the associated financial analysis provide information to assist users in assessing the financial performance and position of the Australian Government. The CFS is prepared by the Department of Finance (Finance) and issued by the Minister for Finance.

2.2 The CFS presents the consolidated whole of government financial results which includes the results of all Australian Government controlled entities, as well as the General Government Sector (GGS) financial statements. The 2024–25 CFS is prepared in accordance with section 48 of the Public Governance, Performance and Accountability Act 2013 (PGPA Act) and the requirements of the Australian Accounting Standards, particularly AASB 1049 Whole of Government and General Government Sector Financial Reporting (AASB 1049).

2.3 AASB 1049 requires, with limited exceptions, the principles and rules in the Australian Bureau of Statistics’ Government Finance Statistics (GFS) Manual to be applied in the preparation of the CFS where compliance with the GFS Manual does not conflict with Australian Accounting Standards.4

Key areas of financial statements risk

2.4 The ANAO’s 2024–25 audit approach identified five key areas of financial statements risk that had the potential to impact the Australian Government, and which were considered Key Audit Matters, as shown in Table 2.1.

Table 2.1: Key areas of financial statements risk

|

Relevant financial statement itema |

Key areas of risk |

Factors contributing to the risk assessment |

|

Taxation revenue $676.1 billion Australian Taxation Office |

High Accuracy of taxation revenue |

|

|

Superannuation liabilitiesb $313.2 billion Department of Defence Department of Finance |

High Valuation of superannuation liabilities |

|

|

Military Compensation liability $80.1 billion Department of Veterans’ Affairs Military Compensation provision $71.9 billion Department of Veterans’ Affairs |

High Valuation of Military Compensation Provision |

|

|

Specialist Military Equipment (SME) $93.7 billion Department of Defence Other plant, equipment and infrastructure $96.1 billion Numerous entities |

Moderate Valuation of specialist military equipment and other plant, equipment and infrastructure assets |

|

|

Australian Government Securities (AGS) $679.5 billion Australian Office of Financial Management (AOFM) |

Moderate Valuation and disclosure of Australian Government Securities |

|

Note a: Figures presented in Table 2.1 may differ from the financial statements of individual entities because of eliminations and adjustments at the CFS level or where the entities identified contribute a majority to the balance of the financial statement line item.

Note b: These are the main government entities responsible for administration and reporting of Australian Government superannuation liabilities. Liabilities also include schemes managed by other entities, such as the Australian Postal Corporation.

Source: ANAO 2024–25 audit results, and the CFS for the year ended 30 June 2025.

Audit results and observations

2.5 The 2024–25 CFS was signed by the Minister for Finance on 23 November 2025 and the Auditor-General’s unmodified auditor’s report was issued on 25 November 2025.

2.6 Without modifying the audit opinion, the auditor’s report included an emphasis of matter paragraph which draws attention to the accounting policies that describe the inherent uncertainty associated with a number of the assumptions used in the calculation of the Australian Government’s military compensation provisions and the sensitivity of the valuation of the provision to changes in these assumptions.

2.7 The military compensation provisions recognised by the Australian Government increased significantly from $92.3 billion in 2023–24 to $152.0 billion in 2024–25. There were a number of factors that contributed to this increase including new legislation, the Veterans Entitlements, Treatment, and Support (Simplification and Harmonisation) Act 2025 (the VETS Act), that was passed in February 2025.

2.8 There were no significant or moderate audit findings arising from the 2024–25 financial statements audit of the CFS.

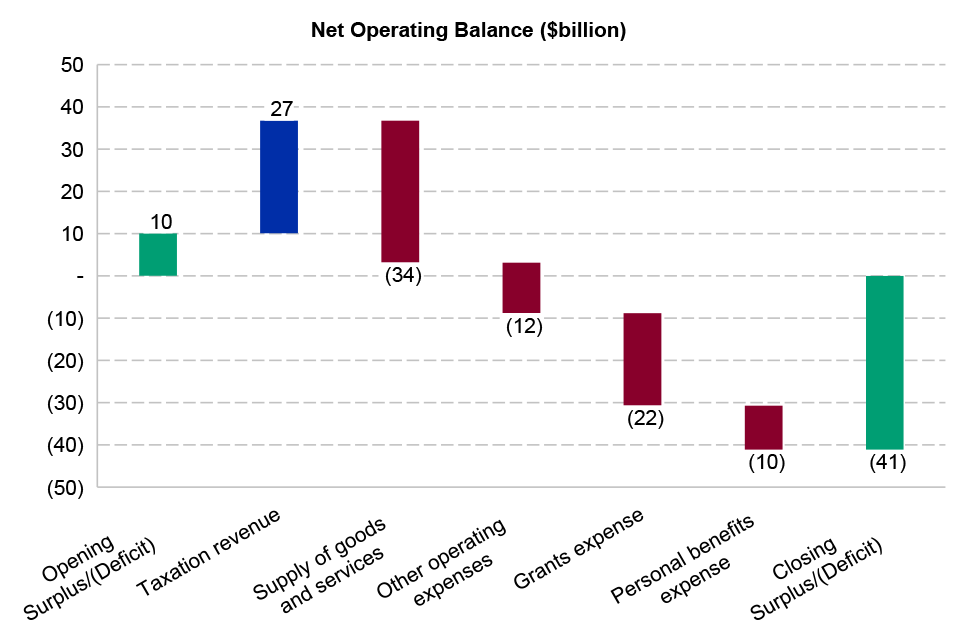

Australian Government’s financial outcome

2.9 Figure 2.1 presents the Australian Government’s net operating balance from 1 July 2024 to 30 June 2025.

Figure 2.1: Changes in the Australian Government’s net operating balance from 1 July 2024 to 30 June 2025

Source: ANAO analysis of the 2024–25 CFS.

2.10 The net operating balance was a deficit of $41.2 billion (compared to a surplus of $10.1 billion in 2023–24). A key contributor to the deterioration in the net operating balance is supply of goods and services expense which has increased by $34.6 billion from $201.9 billion in 2023–24 to $236.5 billion in 2024–25.

2.11 The primary driver for the Australian Government’s increase in total expenses is an increase of $22.0 billion in veterans’ health care payments and provisions due mostly to changes in legislation under which payments are made, increased costs, and other economic factors such as interest rates, inflation and risk factors.

2.12 The other reason for the increase in total expenses is the National Disability Insurance Agency’s (NDIA) participant expenses which have increased by $4.5 billion to $46.4 billion as a result of increases in participant numbers and average payments which have increased to $65,800 per participant in 2024–25 ($64,400 in 2023–24).

2.13 For further details on other key movements refer to the 2024–25 CFS commentary published on the Department of Finance’s website.5

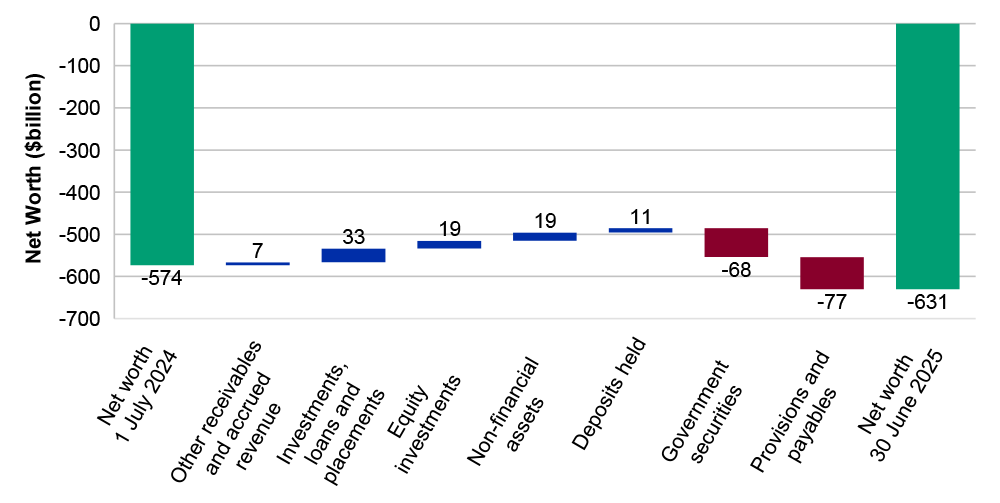

Figure 2.2: Changes in the Australian Government’s net worth from 1 July 2024 to 30 June 2025

Source: ANAO analysis of the 2023–24 CFS.

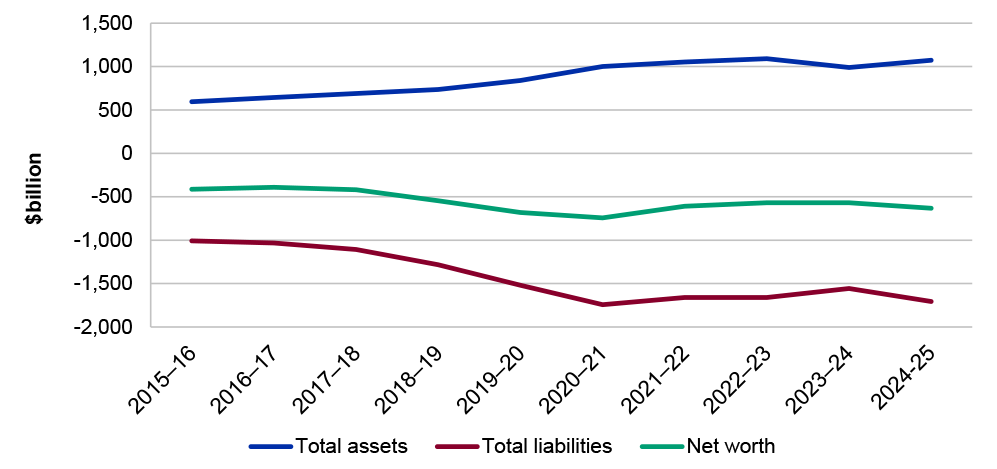

Figure 2.3: Australian Government’s total assets, total liabilities and net worth, from 2015–16 to 2024–25

Source: ANAO analysis of the 2015–16 to 2024–25 CFS.

2.14 During the period the Australian Government’s total assets increased by $83.8 billion from $989.6 billion to $1,073.4 billion while total liabilities increased by $142.5 billion from $1,563.3 billion to $1,705.8 billion. Overall, the Australian Government’s net worth position decreased further by $58.7 billion from a deficit of $573.7 billion to a deficit of $632.4 billion.

2.15 The deteriorating net worth position was mainly driven by increased provisions and payables owed by the Australian Government especially DVA’s military compensation provisions which have grown by $59.7 billion. A $23.4 billion portion of the increase is attributed to the VETS Act which expanded coverage, $21.5 billion for increased costs in meeting liabilities, $8.7 billion for net new exposure and $6.1 billion in other actuarial adjustments for interest rates, inflation and risk.

2.16 For further details on other key movements refer to the 2024–25 CFS commentary published on the Department of Finance’s website.6

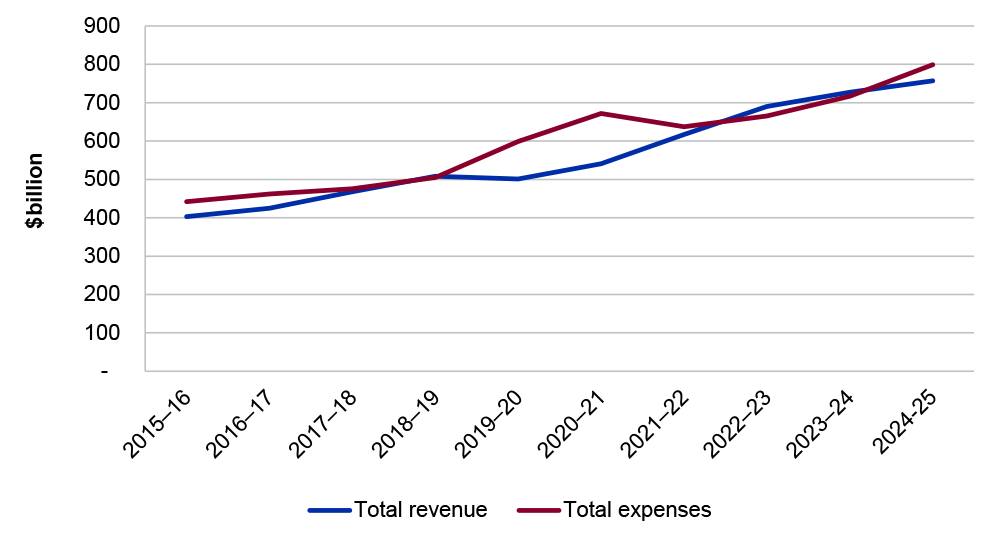

Figure 2.4: Australian Government’s total revenue and total expenses, from 2015–16 to 2024–25

Source: ANAO analysis of the 2024–25 CFS

2.17 Government securities are primarily issued to meet the financing needs, and to fund the operations of the Australian Government during periods when total expenses exceed total revenue. During the period from 2015–16 to 2021–22, the Australian Government’s expenses have been greater than the revenue it received. This briefly reversed from 2022–23 to 2023–24, however, in 2024–25, total expenses exceeded total revenue. Figure 2.4 above illustrates the trend of Australian Government revenue and expenses over the period 2015–16 to 2024–25.

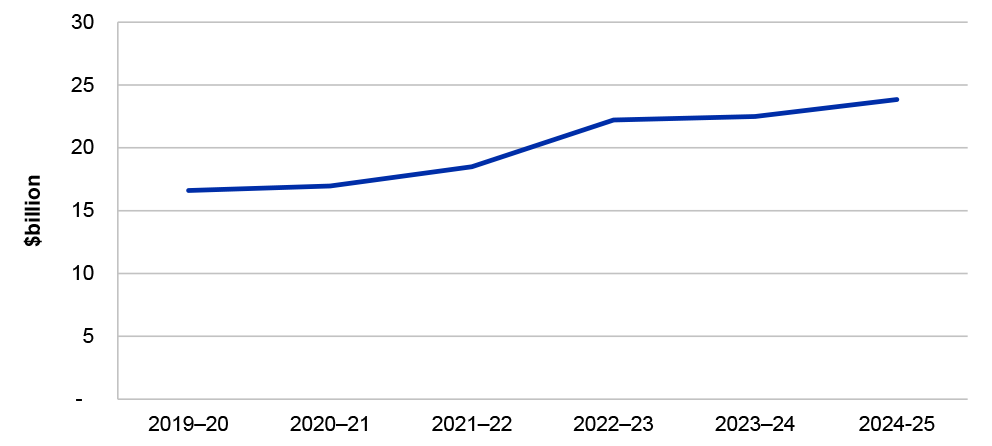

Figure 2.5: AOFM Government Securities Interest Paid from 2019–20 to 2024–25

Source: ANAO analysis of AOFM from 2019–20 to 2024–25.

2.18 The Australian Office of Financial Management (AOFM) is responsible for managing the Australian Government Securities, which totalled $887.0 billion (2023–24: $844.2 billion) for the GGS at 30 June 2025, comprised of Treasury Bonds, Treasury Indexed Bonds and Treasury Notes. The value of the Australian Government’s Securities is $679.5 billion (2023–24: $611.0 billion), which is lower due to the RBA holding a large portion of Australian Government Securities on issue.

2.19 Figure 2.5 demonstrates the interest paid by AOFM on Government Securities over the six-year period from 2019–20 to 2024–25. For 2024–25, new securities issued resulted in increased interest payments despite the weighted average market yield on Treasury Bonds (the major portion of Australian Government Securities) decreasing to 3.67 per cent (2023–24: 4.20 per cent).

Definitions used in this chapter

2.20 Table 2.2 below provides a glossary of the key fiscal aggregates and other terminology used in this chapter to explain the Australian Government’s net worth and financial performance.

Table 2.2: Definitions of terms used

|

Name |

Definition |

|

Net operating balance |

This is calculated as income from transactions minus expenses from transactions. It is equivalent to the change in net worth arising from transactions. |

|

Net worth |

The net worth of the Australian Government is defined as assets less liabilities. |

|

Government securities |

All securities issued by the Australian Government at tenders conducted by the AOFM. They comprise Treasury Bonds, Treasury Notes and Treasury Indexed Bonds. |

Source: Australian Bureau of Statistics (2015). Australian System of Government Finance Statistics: Concepts, Sources and Methods; AASB 101 Preparation of Financial Statements, paragraph 5 and 7; AASB 1049 Whole of Government and General Government Sector Financial Reporting, Appendix A; and Reserve Bank of Australia (2017). Glossary RBA. [Internet], available from https://www.rba.gov.au/glossary/ [accessed 22 October 2025].

3. Financial audit results

Summary of 2024–25 auditor’s reports

3.1 A financial statements audit is finalised when the auditor has formed an opinion on the financial statements, and that opinion has been expressed through a written report.

At 30 November 2025 the ANAO had issued 239 auditor’s reports on 2024–25 financial statements, including the Australian Government’s Consolidated Financial Statements (CFS). Two auditor’s reports were modified, reflecting the ANAO being unable to conclude that those financial statements were free from material misstatement.

Eighty-three per cent of auditor’s reports were signed within three months of year-end compared to 79 per cent in 2023–24.

Four auditor’s reports are yet to be issued due to those audits being ongoing at the date of this report.

Auditor’s reports issued

3.2 A comparison of the number and type of auditor’s reports issued by the Auditor–General and their delegates in 2023–24 and 2024–25 (as at 30 November 2025), including the CFS is summarised at Table 3.1.

Table 3.1: Summary of auditor’s reports issued and outstanding as at 30 November 2025 and 9 December 2024

|

Auditor’s report |

2024–25 |

2023–24 |

|

Unmodified |

237 |

240 |

|

7 |

13 |

|

Modified |

2 |

– |

|

Auditor’s reports issued |

239 |

240 |

|

Not yet issued |

4 |

6 |

|

Total number of financial statements audits |

243 |

246 |

Source: 2023–24 and 2024–25 ANAO auditor’s reports.

Emphasis of Matter

3.3 Emphasis of matter paragraphs are included in an auditor’s report when the auditor considers it necessary to draw users’ attention to a matter presented or disclosed in the financial statements that is fundamental to users’ understanding.7

3.4 The auditor’s report for the following seven entities (2023–24: 13) included emphasis of matter paragraphs: Seafarers Safety, Rehabilitation and Compensation Authority; Australian Sports Foundation Charitable Fund; Darwin Hotel Partnership; Gagudju Lodge Cooinda Trust; IBA Retail Property Trust; Tennant Creek Land Holding Trust; and the Performance Bond Fund Trust. Further details on each entity are included in Chapter 4.

Modified Opinion

3.5 An auditor’s opinion is modified in the auditor’s report when the auditor concludes that the financial statements are not free from material misstatement, or the auditor is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement.8

3.6 The auditor’s report for two entities (2023–24: 0 entities) contained a modification to the auditor’s opinion. These were the Royal Australian Mint, due to the ANAO being unable to obtain sufficient appropriate audit evidence regarding the carrying amount of the heritage and cultural assets because of inadequate accounting records, and the Department of the House of Representatives, due to the ANAO being unable to obtain sufficient appropriate audit evidence to determine whether the cash balance and appropriations note disclosures were free from material misstatement. Further details on each entity are included in Chapter 4.

Not yet issued

3.7 There were four entities for which the 2024–25 financial statements audit had not been finalised by the ANAO as at 30 November 2025. They were Anindilyakwa Land Council, Northern Territory Aboriginal Investment Corporation, Aboriginal Investment NT Trust, and the Australian Secret Intelligence Service. Further details are included in Chapter 4.

Timeliness of auditor’s reports

3.8 The ANAO’s 2025–26 Corporate Plan includes a performance measure ‘Percentage of mandated financial statements audit reports issued in time to meet entity annual reporting timeframes’, for which the target was set at 85 per cent within three months of the end of the financial year. This measure will report on the auditor’s reports issued in 2025–26, which predominantly relate to audits of 2024–25 financial statements.

3.9 Figure 3.1 shows that the finalisation of financial statements audits within three months of the reporting date has improved slightly from the prior year. Eighty-two per cent of auditor’s reports were issued within three months of the end of the reporting period compared to 79 per cent in the prior year. The primary reasons for the 85 per cent target not being met were: delays in the preparation of financial statements by some entities that resulted in delays in the audit process; unplanned staff absences in some audit teams; and changes to planned financial statements signing dates by audited entities.

3.10 The ANAO issued 96 per cent of 2024–25 auditor’s reports within two business days of the signing of the financial statements by the accountable authority (2023–24: 99 per cent).

Figure 3.1: Timeframes for auditor’s report signing from the end of financial year

Source: ANAO analysis.

Timeliness of annual reports

3.11 Annual reports inform the Parliament, the community and other stakeholders about the performance of entities. The publication of the annual report containing the audited financial statements is a key means to meet accountability and legislative obligations. For 2024–25, there were 189 entities required to present annual reports to the responsible minister under the PGPA Act.

3.12 Annual reports are approved by the entity’s accountable authority before being provided to the minister and tabled in Parliament. RMG 135 Annual reports for non-corporate Commonwealth entities9, and RMG 136 Annual reports for corporate Commonwealth entities10 state that annual reports are to be provided to the relevant minister by the 15th day of the fourth month after the end of the reporting period. RMG 137 Annual reports for Commonwealth companies11 states that Commonwealth company directors must give the annual report to the responsible minister the earlier of 21 days before the next annual general meeting after the end of the reporting period for the company or four months after the end of the reporting period for the company.

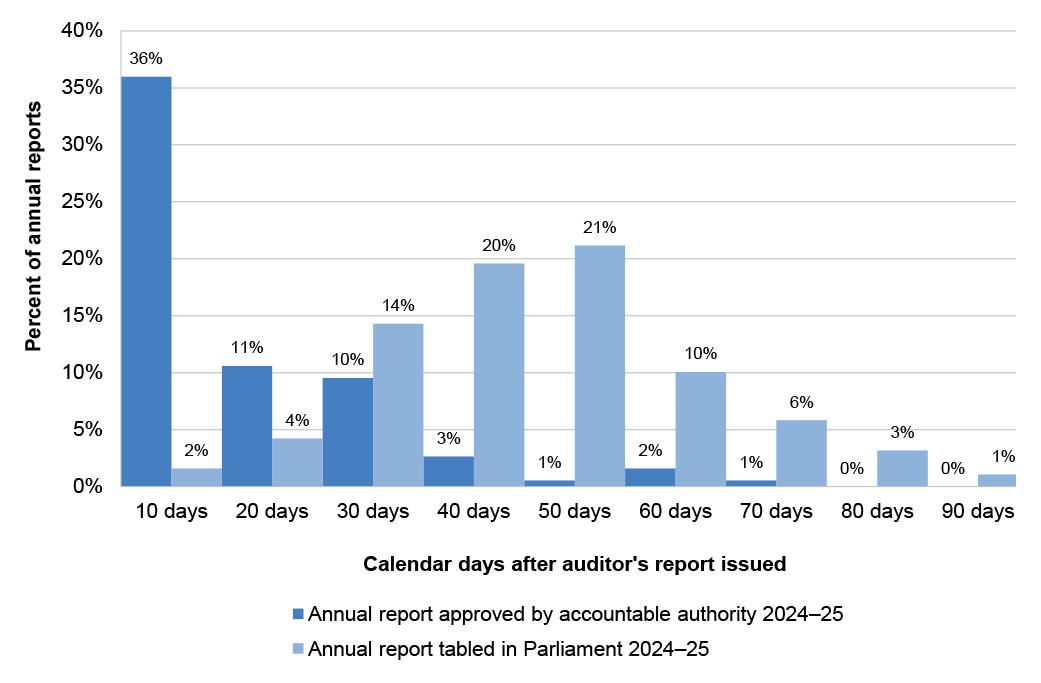

3.13 Figure 3.2 shows the time in days between the issue of the auditor’s report to the:

- approval of the annual report by the accountable authority; and

- tabling of the annual report in Parliament.

Figure 3.2: Timeframe for tabling 2024–25 annual reports from issuance of auditor’s report

Source: ANAO analysis of entity annual reports

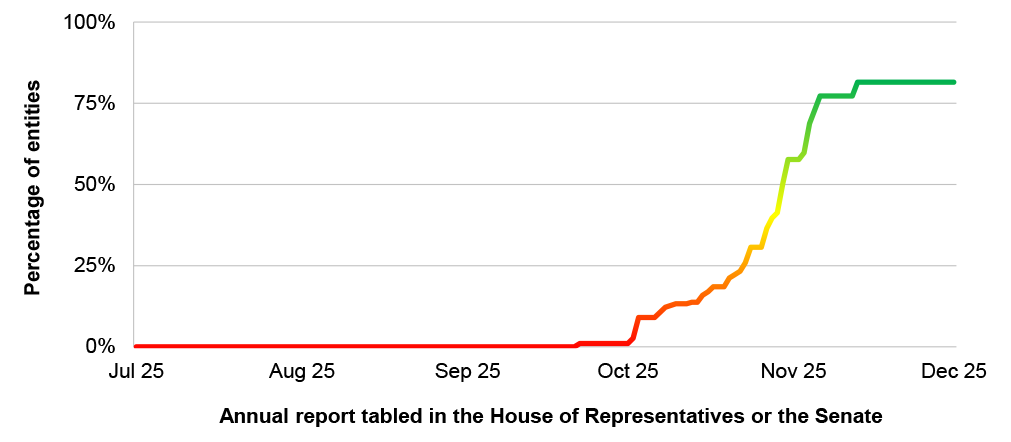

3.14 Figure 3.3 shows entities annual report tabling date in relation to the year ending 30 June 2025.

Figure 3.3: Entities annual report tabling date in relation to the year ending 30 June 2025

3.15 The analysis above shows that accountable authorities approved 36 per cent of annual reports within 10 days of the issue of the auditor’s report (2023–24: 54 per cent), with an overall average of 10 days (2023–24: 13 days). The average days between the accountable authority’s approval of the annual report and tabling in Parliament was 30 days (2023–24: 30 days).

3.16 Twenty per cent of annual reports were tabled within 30 calendar days from the issue of the auditor’s report (2023–24: 28 per cent). The tabling of annual reports in Parliament occurred on average 41 days after the auditor’s report was issued (2023–24: 43 days).

3.17 Annual reports should be tabled in Parliament to allow sufficient time for review before Senate supplementary budget estimates hearings. The RMGs on annual reports indicate that normally annual reports are tabled on or before 31 October and it is expected annual reports are tabled prior to the supplementary budget estimates hearings. 12

3.18 In 2024–25, supplementary budget estimates hearings were held from 7 to 10 October 2025, ahead of the 31 October deadline to table in Parliament. Additional supplementary budget estimates hearings were held from 1 to 4 December 2025. In 2023–24, supplementary budget estimates hearings were held from 4 to 8 November 2024.

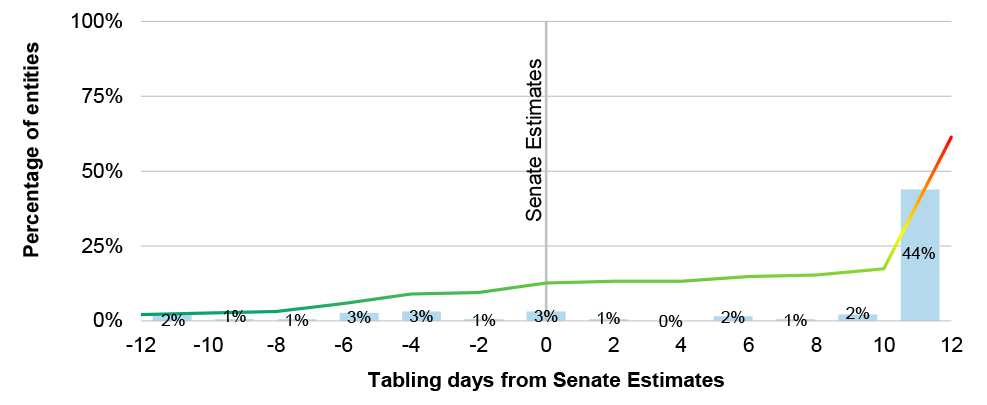

3.19 Figure 3.4 shows that 2024–25 annual reports were tabled by 5 per cent of entities greater than one week before the October supplementary budget estimates hearing dates for their portfolio.

Figure 3.4: Entities annual report tabling date in relation to the October 2025 supplementary budget estimates

Note: This graph does not add to 100 per cent as a result of entities that had not tabled an annual report as at 30 November 2025.

Source: ANAO analysis of entity tabled annual reports.

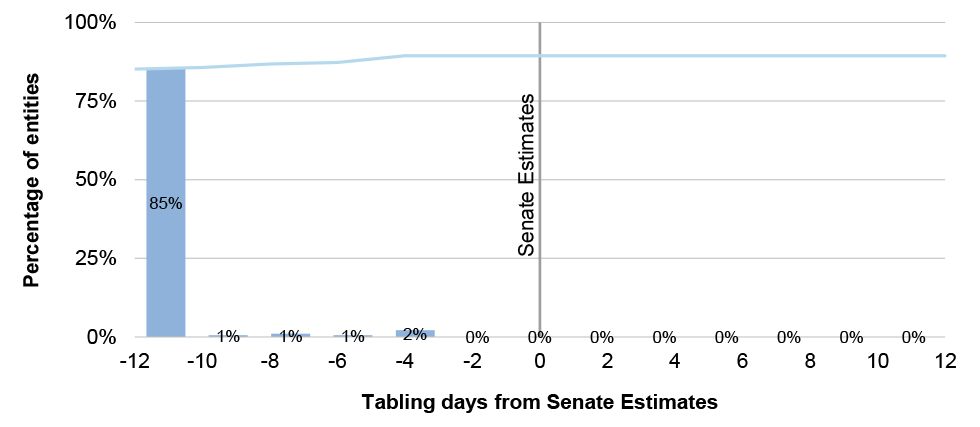

3.20 Figure 3.5 shows that 2024–25 annual reports were tabled by 88 per cent of entities greater than one week before the December supplementary budget estimates hearing dates for their portfolio.

Figure 3.5: Entities annual report tabling date in relation to the December 2025 supplementary budget estimates

Note: This graph does not add to 100 per cent as a result of entities that had not tabled an annual report as at 30 November 2025.

3.21 In 2023–24, supplementary budget estimates were held from 4 to 8 November, after the 31 October deadline to table annual reports in Parliament. In that year, 57 per cent of entities tabled an annual report with greater than one week before the hearings, and 93 per cent of entities had tabled annual reports before the entity’s portfolio hearing date.

3.22 In 2024–25, supplementary budget estimates hearings were held from 7 to 10 October 2025, ahead of the 31 October deadline to table in Parliament. For those hearings, 5 per cent of entities tabled an annual report with greater than one week before the hearings, and 16 per cent of entities had tabled annual reports before the entity’s portfolio hearing date.

3.23 Additional supplementary budget estimates hearings were held from 1 to 4 December 2025. For those hearings, 88 per cent of entities tabled an annual report with greater than one week before the hearings, and 91 per cent of entities had tabled annual reports before the entity’s portfolio hearing date.

3.24 There are 20 entities (11 per cent) that are required to table an annual report which had not done so as at 30 November 2025 – the date of this report (2023–24: 4 per cent at 9 December 2025).

Audit findings

3.25 Audit findings are raised in response to the identification of a potential business or financial risk posed to an entity. Often these risks arise from deficiencies within an entity’s internal control processes or frameworks.

3.26 Where the ANAO identifies one or more control deficiencies, the ANAO assesses whether, individually or in combination, the deficiencies constitute a significant deficiency and reports these to accountable authorities as audit findings. The ANAO applies professional judgement in determining whether a deficiency represents a significant control deficiency. The ANAO’s rating scale is presented in Table 1.2, in the Introduction to this report.

3.27 At the conclusion of the 2024–25 audits, the ANAO has identified the following.

Total audit findings have decreased

A total of 178 audit findings and legislative non-compliance were reported to entities in 2024–25 (2023–24: 214), comprising:

- Three significant (2023–24: 6), 31 moderate (2023–24: 46), 123 minor (2023–24: 147), and 21 instances of legislative non-compliance.

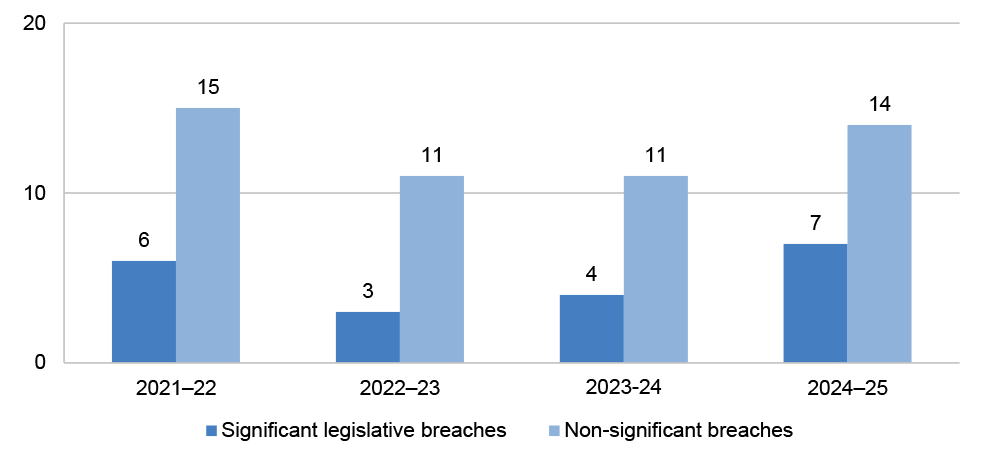

Legislative non-compliance has increased.

A total of 21 findings relating to legislative non-compliance were reported to entities in 2024–25 (2023–24: 15), comprising:

- Seven significant legislative breaches, including potential breaches of the Australian Constitution, and breaches of entities’ enabling legislation.

- Seven instances of incorrect remuneration payments made to key management personnel and/or non-compliance with Determinations made by the Remuneration Tribunal.

- Seven other instances of non-compliance with legislation with which entities are required to comply, or non-compliance with subordinate legislation.

IT control environment represents most findings

Forty-five per cent (2023–24: 43 per cent) of all audit findings identified relate to entities’ IT control environments.

The number of IT findings identified by the ANAO indicate that there remains room for improvement across the sector to enhance governance processes supporting the design, implementation and operating effectiveness of controls.

These matters extend beyond technical IT concerns; they pose significant business risks to the security and the integrity of information systems. Addressing these fundamentals is essential in an environment where entities increasingly rely on technology, including artificial intelligence (AI).

Trends in audit findings

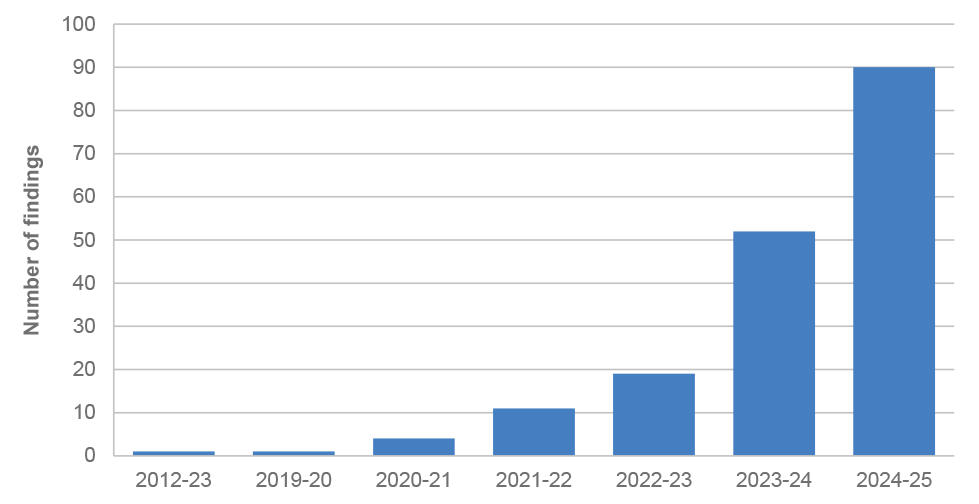

3.28 Figures 3.6 and 3.7 show a summary of all significant, moderate, minor and legislative findings identified by the ANAO for the period 2021–22 to 2024–25. For 2021–22, this included 248 entities, 244 entities in 2022–23, 244 entities in 2023–24, and 243 entities in 2024–25.

3.29 Unresolved audit findings are those findings that have been identified by the ANAO and are not yet addressed by the entity. When reporting an audit finding to an entity the ANAO details the implications, risk and recommendations to the entity for resolution. Each audit finding reported is classified by the level of risk that may be posed to the entity, or the entity’s financial statements, if unaddressed. As a result, entities should take action to address unresolved audit findings, and the particular weakness in internal control identified, in a timely manner which is commensurate with the level of risk identified.

Figure 3.6: Audit findings 2021–22 to 2024–25

Figure 3.7: Legislative non-compliance 2021–22 to 2024–25

Significant audit findings

3.30 Significant audit findings indicate issues that pose a significant business or financial management risk to the entity or are instances of significant non-compliance with legislation. This includes issues that could result in a material misstatement of the entity’s financial statements.

3.31 There were three significant audit findings, and seven significant legislative non-compliance at the conclusion of the 2024–25 audits (see Tables 3.2 and 3.3). Details of these significant audit findings are included in Chapter 4.

Table 3.2: Significant audit findings at the conclusion of the 2024–25 audits

|

Entity |

First identified |

Type of finding |

Description |

|

Department of the House of Representatives |

2024–25 |

Compliance and quality assurance frameworks |

Legal and accounting uncertainties relating to the management of the Pacific Parliamentary Partnership Fund. Refer to paragraphs 4.13.16 to 4.13.31. |

|

Royal Australian Mint |

2024–25 |

Accounting and control of non-financial assets |

Deficiencies in data integrity, valuation methodology, and documentation, in relation to asset valuations. Refer to paragraphs 4.16.83 to 4.16.99. |

|

Services Australia |

2022–23 |

Compliance and quality assurance frameworks |

Compliance with legislative requirements for the identification and recovery of debts relating to Medicare Compensation Recovery. Refer to paragraphs 4.15.31 to 4.15.68. |

Source: ANAO data

Table 3.3: Significant non-compliance with legislation at the conclusion of the 2024–25 audits

|

Entity |

First identified |

Description |

|

Australian Centre for International Agricultural Research |

2024–25 |

Potential breaches of section 83 of the Australian Constitution relating to payments of employee entitlements. Refer to paragraphs 4.8.24 to 4.8.30. |

|

Australian Pesticides and Veterinary Medicines Authority |

2024–25 |

Non-compliance relating to the administration of levies under the Agricultural and Veterinary Products (Collection of Levy) Act 1994. Refer to paragraphs 4.1.12 to 4.1.17. |

|

Department of Health, Disability and Ageing |

2024–25 |

Potential breaches of section 83 of the Australian Constitution relating to health care payments. Refer to paragraphs 4.9.6 to 4.9.34. |

|

Department of the House of Representatives |

2024–25 |

Potential breaches of section 61 of the Australian Constitution, and the PGPA Act relating to payments made from the Pacific Parliamentary Partnership Fund. Refer to paragraphs 4.13.16 to 4.13.31. |

|

Northern Land Council |

2012–13 |

Non-compliance with requirements of the Aboriginal Land Rights (Northern Territory) Act 1976 relating to the distribution of royalty monies to traditional owners. Refer to paragraphs 4.14.71 to 4.14.78. |

|

Services Australia |

2023–24 |

Breach of, and inconsistent application of, legislation that Services Australia is responsible for administering. Refer to paragraphs 4.15.31 to 4.15.68. |

|

Tiwi Land Council |

2023–24 |

Non-compliance with requirements of the Aboriginal Land Rights (Northern Territory) Act 1976 relating to the distribution of royalty monies to traditional owners. Refer to paragraphs 4.14.87 to 4.14.94. |

Source: ANAO data

Unresolved findings

3.32 Unresolved audit findings are those findings that have been identified by the ANAO and are not yet addressed by the entity. When reporting an audit finding to an entity the ANAO details the implications, risk and recommendations to the entity for resolution.

3.33 Each audit finding reported is classified by the level of risk that may be posed to the entity, or the entity’s financial statements, if unaddressed. As a result, entities should take action to address unresolved audit findings in a timely manner which is commensurate with the level of risk identified.

3.34 Fifty per cent of audit findings (89 findings) reported at the conclusion of the 2024–25 audits were findings unresolved from prior audits.

3.35 Figure 3.8 provides an analysis of the period in which the 89 unresolved audit findings were first identified by ANAO. Of the unresolved findings three per cent were first identified in 2020–21, ten per cent in 2021–22, 26 per cent in 2022–23, and 61 per cent in 2023–24.

Figure 3.8: Number of audit findings by period first identified by the ANAO

Source: ANAO data

Audit findings partially resolved, or the risk rating reduced

3.36 The ANAO may reassess the associated risk rating attributed to an audit finding when significant progress has been made to address the risks identified, and the reassessed risk rating better represents the overall risk to an entity.

3.37 During 2024–25, the ANAO reassessed 10 significant or moderate audit findings by reducing the associated risk rating (see Table 3.4). Further details on actions taken by entities to reduce the risk rating is included in Chapter 4.

Table 3.4: Significant and moderate findings partially resolved, or the rating reduced

|

Entity |

First identified |

Change in risk rating |

|

Australian Taxation Office |

2022–23 2021–22 |

One significant audit finding was revised to two moderate audit findings, and one moderate audit finding was revised to a minor audit finding. Refer to paragraphs 4.16.47 to 4.16.70. |

|

Australian Strategic Policy Institute |

2023–24 |

Moderate to minor, refer to paragraphs 4.4.63 to 4.4.69. |

|

Department of Health, Disability and Ageing |

2023–24 |

Moderate to minor, refer to paragraphs 4.9.6 to 4.9.34. |

|

Department of Industry, Science and Resources |

2023–24 |

Moderate to minor, refer to paragraphs 4.11.5 to 4.11.15. |

|

Department of Social Services |

2023–24 |

Significant legislative breach reassessed to other non-compliance with legislation, refer to paragraphs 4.15.6 to 4.15.30. |

|

National Disability Insurance Agency |

2023–24 2023–24 |

Two moderate audit findings were revised to minor audit findings, refer to paragraphs 4.9.62 to 4.9.80. |

|

Services Australia |

2021–22 2022–23 |

One significant audit finding was revised to a moderate audit finding, and one moderate audit finding was revised to a minor audit finding, refer to paragraphs 4.15.31 to 4.15.68. |

Resolved audit findings

3.38 The ANAO considers audit findings to be resolved when entities have implemented the agreed recommendations, and satisfactorily addressed the risks identified. During 2024–25, 150 audit findings were either fully resolved, or the risk rating was reduced.

3.39 The below case study sets out the Department of Defence’s approach to addressing a significant audit finding.

|

Case study 1. Department of Defence – Removal of System Access for Defence personnel and contractors |

|

During the 2022–23 audit, the ANAO identified 1,451 users whose access to the Defence Network was not disabled in accordance with Information Security Manual (ISM) requirements, which requires entities to remove or suspend access on the same day personnel (including contractors) no longer have a legitimate business requirement for the access. The ANAO also identified that a number of terminated employees continued to receive salary payments, in one case, for more than two months after termination. Additionally, the ANAO identified Defence did not have effective controls in place for removing access to the financial management information system (FMIS) when personnel or contractors remained within Defence, but their duties change and they no longer have a legitimate business requirement to access the system. This issue was raised a significant (category A) audit finding in 2022–23. In response to this audit finding, Defence established a dedicated project team, developed a user data reconciliation environment and engaged internal audit to address the risks identified by the ANAO. Defence approached the audit finding as business-wide issue and implemented solutions accordingly. By recognising the extent of the issue, and working as an organisation to resolve, Defence took clear accountability and demonstrated leadership in addressing this significant audit finding. During the 2024–25 audit, the ANAO recognised that Defence has resolved the issue of user access for former Defence personnel. As Defence continues to implement the agreed recommendations in full, the ANAO revised the risk rating of this finding from significant to minor. |

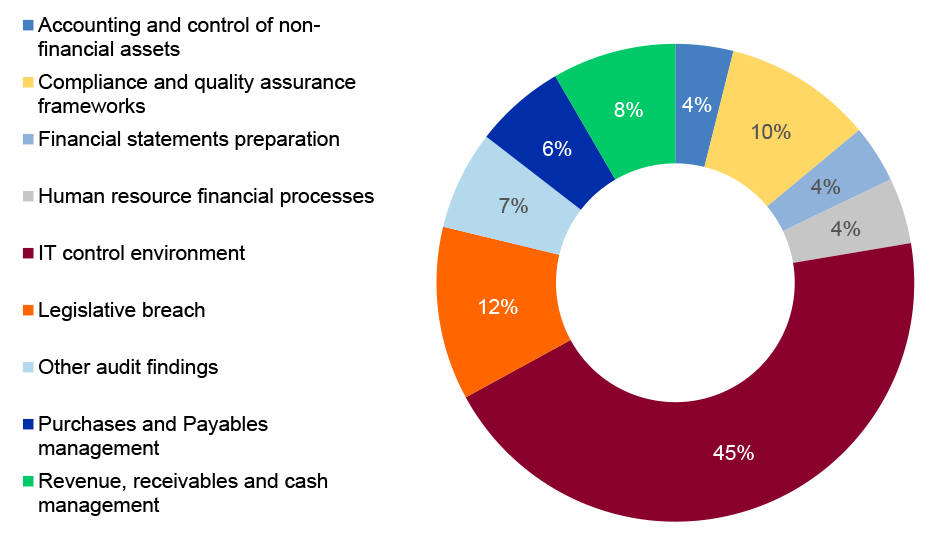

3.40 Figure 3.9 shows that 45% of all audit findings at the conclusion of 2024–25 audits related to the IT control environment. Legislative non-compliance accounted for 12% of audit findings, and 10% related to compliance and quality assurance frameworks.

Figure 3.9: Percentage of audit findings by category at the conclusion of 2024–25 audits

Information Technology control environment

3.41 The information technology (IT) control environment refers to the policies, procedures and controls that maintain the integrity of information and security of data in an entity and includes automated controls that may be relied upon in the financial statements audit. In 2024–25 findings related to the IT control environment represented the largest proportion of audit findings, a trend consistent with previous years, with 45 per cent of total findings relating to IT controls. Figure 3.10 shows the total number of IT control environment findings open at year-end for the years 2021–22 to 2024–25.

Figure 3.10: IT control environment findings open at year-end 2021–22 to 2024–25

Source: ANAO data

Developments in IT control findings since 2023–24

3.42 All three of the significant IT control environment findings that were open at the commencement of the 2024–25 audit cycle were reassessed at the 2024–25 interim audit phase to either moderate or minor findings. These include:

- a significant IT security finding at the Department of Defence, reassessed at interim as a result of actions including the reconciliation of data on terminated staff, internal audit activity and the implementation of new user access controls;

- a significant IT control finding at Services Australia being reassessed following implementation of multiple initiatives, including updates to policies, testing to confirm adherence to policies, staff training, updates to disaster recovery plans and changes to governance committees; and

- the ATO’s significant finding regarding change management being reassessed to two moderate findings, following a strengthening of relevant controls and partial implementation of automated deployment tools.

3.43 The net decrease in overall open findings from the prior year demonstrates that more findings were closed than opened during the cycle. Twenty-seven new IT control environment findings were raised in the 2024–25 audit cycle, representing 34 per cent of the total 80 open IT control environment findings. Figure 3.11 shows the age distribution of currently open IT control environment findings and their categorisation.

Figure 3.11: Current open findings by year raised and category

Source: ANAO data

3.44 The four oldest open IT control environment findings relate to IT security and were first reported in 2020–21. These findings are:

- Services Australia – the monitoring of super users’ activity for Medicare, Child Support, and Health related systems (moderate audit finding);

- Services Australia – the monitoring of super users’ activity for Centrelink related systems (moderate audit finding);

- Department of Veterans’ Affairs – the management of security risks relating to upgrades to the claims processing ICT system, Process Direct (moderate audit finding); and

- National Disability Insurance Agency – the timeliness of terminating user access for former staff (moderate audit finding).

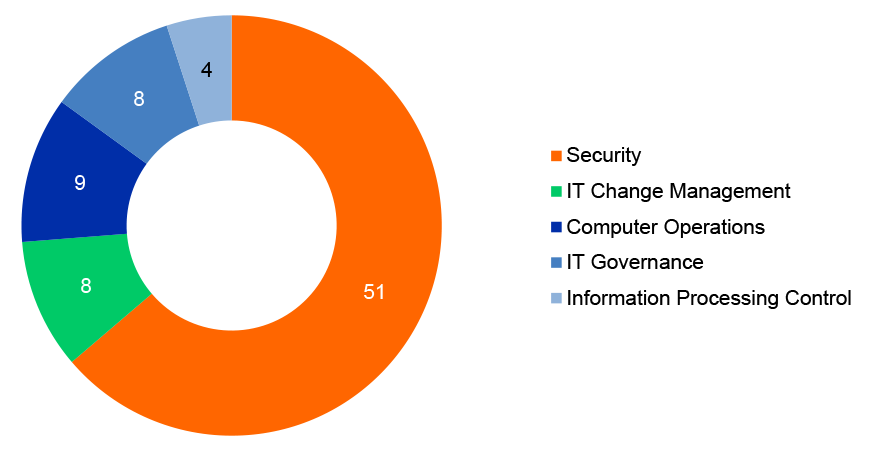

Key themes and issues

3.45 Figure 3.12 provides an overview of the categorisation of open IT control environment findings by theme. The majority (64 per cent) of IT control environment findings related to IT security in 2024–25.

Figure 3.12: Categorisation of 2024–25 IT control environment findings by theme as at year-end 2024–25

Source: ANAO data

3.46 Four findings related to Information Processing Controls, which help ensure that IT systems process data completely and accurately. The significant themes identified over the course of 2024–25 audits, and consistent with prior years, include:

- deficiencies in IT security, including issues such as insufficient monitoring of the activity of privileged users and removal of access from terminated staff;

- deficiencies in change management processes, particularly over segregation of duties between development activities and release management;

- issues relating to IT governance, which concerns the processes by which entities ensure their IT operations are aligned with business objectives; and

- deficiencies in computer operations, primarily relating to business continuity planning and testing, and the timeliness of resolving errors in scheduled processes.

3.47 These themes are discussed in further detail below. Details of specific entity findings are discussed further in Chapter 4.

IT security

3.48 Weaknesses in IT security controls have the potential to compromise an entity’s ability to maintain business operations, maintain the integrity and confidentiality of sensitive data, and reduce the confidence that data used for financial reporting is accurate. At the conclusion of 2024–25 financial statements audits, a total of 51 IT security findings (15 moderate, 36 minor) were open. Table 3.5 shows those entities with open moderate findings related to IT security at the conclusion of 2024–25 audits.

Table 3.5: Moderate IT security findings by entity as at year-end 2024–25

|

Entity |

Number of Moderate Findings |

|

Department of Veterans’ Affairs |

4 |

|

National Disability Insurance Agency |

3 |

|

Services Australia |

3 |

|

Department of Health, Disability and Ageing |

2 |

|

Department of Social Services |

2 |

|

Department of Climate Change, Energy, the Environment and Water |

1 |

|

Total |

15 |

Source: ANAO data

3.49 The ANAO observed that 49 of the 51 IT security findings related to management and monitoring of user access. User access management includes processes to authenticate, authorise and deauthorise access to IT systems to prevent inappropriate access, and ensure accountability of key operations. Additionally, access monitoring controls ensure that use of system access, and privileged access, is logged and reviewed. Issues with these controls threaten the reliability of data residing in significant IT systems that support key business processes.

3.50 IT security management continues to remain the most common area of weakness in the IT control environment, with 64 per cent of total IT control environment findings, and 75 per cent of the moderate IT control environment findings relating to this area. Focus is required by entities to ensure that the risks of unauthorised system access are being appropriately managed.

IT Governance

3.51 IT governance concerns the processes by which entities ensure their IT operations are aligned with business objectives. At the completion of 2024–25 audits, eight open findings (three moderate, five minor) related to IT governance. Those entities receiving moderate findings are shown in Table 3.6 below.

Table 3.6: Moderate IT governance findings by entity as at year-end 2024–25

|

Entity |

Number of Moderate Findings |

|

Snowy Hydro Limited |

1 |

|

Hearing Australia |

1 |

|

Services Australia |

1 |

|

Total |

3 |

Source: ANAO data

3.52 IT governance findings observed in 2024–25 related to:

- overarching issues with entities IT general controls and/or policies; and

- processes by which entities assured themselves of the effectiveness of the controls of third-party IT services on which they rely (such as cloud environments), with risks that entities were not adequately reviewing advisories from those third parties of control deficiencies that may have impacted business operations.

3.53 As entities incorporate increasingly advanced emerging technologies into their operations and leverage a variety of delivery models to optimise costs, the importance of effective governance and oversight arrangements becomes increasingly critical in ensuring the integrity of IT operations.

Change Management

3.54 Change management involves the appropriate authorisation, testing, review and maintenance of changes to key components of an IT system. Effective change management controls support the integrity of key business processes, while the absence of an effective change management framework may limit the ability to senior management to assure themselves that systems are operating as intended.

3.55 At the conclusion of the 2024–25 audits, there were eight unresolved audit findings relating to change management (two moderate, six minor). Table 3.7 shows those entities with open moderate change management findings at the conclusion of 2024–25 audits:

Table 3.7: Moderate IT change management findings by entity as at year-end 2024–25

|

Entity |

Number of Moderate Findings |

|

Australian Taxation Office |

2 |

|

Total |

2 |

Source: ANAO data

3.56 Across change management findings in the 2024–25 audits, the ANAO observed issues in the following areas:

- ineffective segregation of duties between developers and staff migrating changes to production environments, increasing the risk that inappropriate or inaccurate changes may be deployed without sufficient levels of testing or authorisation; and

- insufficient testing of programs that generate financial or management reports, increasing the risk that management decisions are made based on incomplete or inaccurate data.

Computer Operations

3.57 Computer operations involve the delivery of IT services to achieve business objectives. This includes the scheduling of IT processes to automate tasks requiring limited human involvement, and processes to ensure business continuity in the event of a critical incident that compromises an IT system. At the conclusion of the 2024–25 audits, there were nine unresolved audit findings relating to computer operations.

3.58 All nine findings were assessed as having a minor impact to financial statements assurance but have the potential for broader business impact. Seven related to the ability of entities to assure themselves that they are able to recover from a disaster, such as a significant IT outage or loss of critical data. A further two findings related to batch processing, and controls around scheduled tasks that process large volumes of financial transactions. Due to the significant volume of financial transactions typically processed through batch jobs, weaknesses in these controls have the potential to result in significant financial consequences.

Lessons for entities

3.59 Accountable authorities should seek their own assurance that IT control environments are effectively mitigating key business risks. Entities with more effective regimes regularly monitor and evaluate the effectiveness of key IT controls to ensure continued effectiveness in changing environments. A systematic approach to assessing the design, implementation and operating effectiveness of controls is key to ensuring successful IT risk management.

3.60 These matters extend beyond technical IT concerns; they pose significant business risks to the security and the integrity of information systems. Addressing these fundamentals is essential in an environment where entities increasingly rely on technology, including artificial intelligence (AI).

Legislative non-compliance

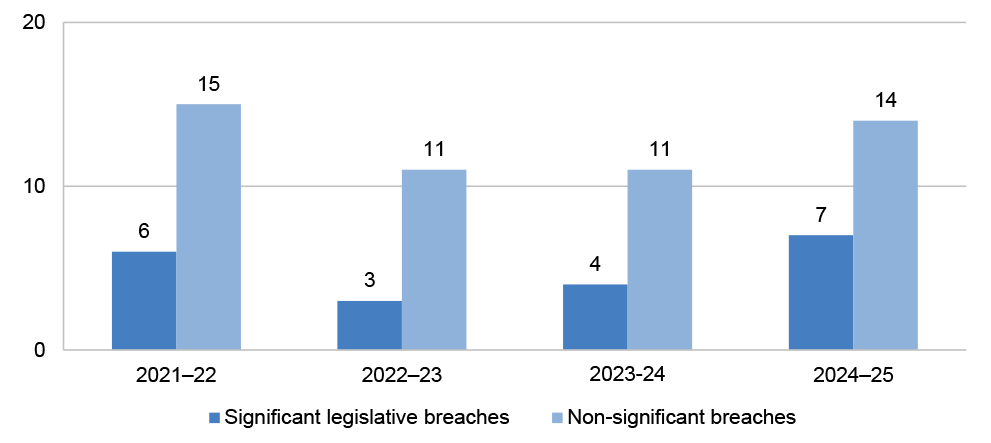

3.61 Significant legislative breaches include instances of significant potential or actual breaches of the Constitution; and instances of significant non-compliance with the entity’s enabling legislation, legislation that the entity is responsible for administering, and the PGPA Act. Figure 3.13 below illustrates legislative breaches identified by the ANAO between 2021–22 to 2024–25.

Figure 3.13: Legislative breaches 2021–22 to 2024–25

Source: ANAO data.

3.62 There were seven instances of significant legislative non-compliance reported during 2024–25. Two of the breaches were identified during 2024–25 and five were identified in prior years. The significant legislative breaches relate to the following entities:

- Australian Centre for International Agricultural Research: Potential breaches of section 83 the Constitution13;

- Australian Pesticides and Veterinary Medicines Authority: Legislative non-compliance relating to the administration of levies under the Agricultural and Veterinary Products (Collection of Levy) Act 1994;

- Department of Health, Disability and Ageing: Legislative non-compliance and governance risks in program payments;

- Department of the House of Representatives: Significant potential non-compliance with the Constitution and PGPA Act;

- Northern Land Council: Royalty Trust Account: The ANAO identified contracts where the distribution of royalty monies to traditional owners was not made within six months, as required under subsections 35(3) and 35(4) of the Aboriginal Land Rights (Northern Territory) Act 1976 ;

- Services Australia: Significant legislative matters in Services Australia’s program delivery; and

- Tiwi Land Council: Non-compliance with the Aboriginal Land Rights (Northern Territory) Act 1976.

3.63 The 14 other breaches primarily related to:

- non-compliance with determinations made by the Remuneration Tribunal for remuneration of key management personnel (incorrect payments); and

- other instances of non-compliance with sub-ordinate legislation

Key management personnel remuneration

3.64 The appropriateness of governance of key management personnel remuneration (KMP) has been a continued focus for the ANAO in 2024–25. Over the period 2021–22 to 2024–25 the ANAO has continued to identify legislative breaches relating to KMP remuneration.

3.65 The Australian Accounting Standards require entities to disclose key management personnel compensation in total14, regardless of amount or materiality. ANAO policy considers key management personnel disclosures material by nature due to the role that these personnel play in organisations and that these personnel set the ‘tone at the top’ of organisations.

3.66 Seven instances of legislative non-compliance related to incorrect payments of remuneration to key management personnel and/or non-compliance with Determinations made by the Remuneration Tribunal, they include:

- Australian Renewable Energy Agency – total remuneration paid to the CEO was more than amounts specified under the Remuneration Tribunal Determinations.

- Australian Sports Commission – total remuneration paid to Board members was more than amounts specified under the Remuneration Tribunal Determinations.

- Australian Fisheries Management Authority – total remuneration paid to key management personnel was more than amounts specified under the Remuneration Tribunal Determinations.

- Indigenous Business Australia – total remuneration paid to Board members was more than amounts specified under the Remuneration Tribunal Determinations.

- WSA Co Limited – an underpayment of Audit and Risk Committee member fees to one Director, and an overpayment to another Director.

- Australian Film, Television and Radio School – total remuneration paid to key management personnel was more than amounts specified under the Remuneration Tribunal Determinations.

- Australian Institute of Family Studies – total remuneration paid to key management personnel was more than amounts specified under the Remuneration Tribunal Determinations.

Compliance with Section 83 of the Australian Constitution

3.67 Section 83 of the Australian Constitution (section 83) provides that no money shall be drawn from the Treasury of the Commonwealth except under appropriation made by law.

3.68 The Australian Government’s financial reporting framework requires entities to disclose in their financial statements whether a breach of section 83 has occurred or may have occurred during the reporting period.15 Australian Government entities monitor their compliance with section 83 and are expected to obtain legal advice to determine the likelihood of a breach, and requirement for disclosure in their financial statements.

3.69 During 2024–25, 11 entities (2023–24: 10 entities) reported breaches of section 83 in their financial statements. These entities were the Australian Communications and Media Authority, the Australian Taxation Office, the Department of Agriculture, Fisheries and Forestry, the Department of Climate Change, Energy, the Environment and Water, the Department of Foreign Affairs and Trade, the Department of Social Services, the Department of Veterans’ Affairs, the Department of Education, the Department of Health, Disability and Ageing, Services Australia, and Department of the Treasury.

3.70 Section 83 breaches are characterised as either potential or actual breaches. The ANAO applies judgement to determine whether breaches of section 83 are reported to an entity as a significant legislative breach. Considerations include the nature of the breach, whether the control deficiencies that resulted in the breach have been appropriately addressed by the entity, are in the process of being addressed, and whether the breaches have been appropriately disclosed in the entity’s financial statements.

3.71 Case studies 2 and 3 highlight examples of section 83 breaches in 2024–25. Further information on the breaches across each of the 11 entities are included in each entity’s 2024–25 financial statements.

|

Case study 2. Department of the Treasury – Energy Bill Relief Extension Program |

|

The Department of the Treasury (Treasury) manages payments to States and Territories under the Federal Financial Relations Act 2009 (FFR Act). The FRR Act allows for an official to be authorised to assess National Partnership Agreement milestones on the Minister’s behalf. Since the Minister cannot legally delegate the power to approve payments, a written ministerial authorisation must be in place for the official to approve these payments. In 2024–25, Treasury identified eight payments, totaling $2.28 billion relating to the Energy Bill Relief Extension Program which were made without appropriate written ministerial authorisation in place for the official to approve the payments on the Minister’s behalf. Treasury appropriately disclosed these breaches in its 2024–25 financial statements. These breaches were identified by Treasury officials, and Treasury acted in response to this matter to prevent recurrence of this. As a result of the disclosure and action taken by Treasury, the ANAO did not raise a legislative breach finding. Rather, an observation on these breaches was raised with Treasury’s Accountable Authority as part of the finalisation of the 2024–25 Treasury financial statements audit. |

|

Case study 3. Various entities – Australian Government payments |

|

The Australian Government administers a variety of payments and financial support across Centrelink, Medicare, and other programs. In most cases, the eligibility criteria for these payments, and the determination of entitlement amounts, are reliant on information directly provided by payment recipients. If information provided is not accurate, or timely, the payment made may be incorrect and a debt will be raised to recover overpayments. Overpayments may constitute a breach of Section 83 if they were not made in line with the appropriation that governs the payment. In 2024–25, the Department of Social Services, the Department of Health, Disability and Ageing, the Department of Agriculture, Fisheries and Forestry, the Department of Employment and Workplace Relations, and the Department of Education disclosed potential section 83 breaches in relation to overpayments of a variety of Australian Government payments. In each case, overpayments are recorded as debts, and action is taken to recover these amounts. |

Quality and timeliness of financial statements preparation

A quality financial statements preparation process will reduce the risk of inaccurate or unreliable reporting. At the completion of 2024–25 audits the ANAO identified weaknesses, and reported audit findings on, the financial statements preparation process in seven entities (2023–24: 15).

Quality of financial statements

Two key indicators of the quality of the financial statements preparation process are the number and quantum of adjusted and unadjusted audit differences, and the timeliness of financial statements preparation.

The total number of adjusted and unadjusted audit differences decreased to 186 (2023–24: 209). 28 per cent of audit differences remained unadjusted (2023–24: 38 per cent).

Timeliness of financial statements preparation

Timeliness of financial statements preparation improved in 2024–25, with 74 per cent of entities providing financial statements for audit in-line with agreed timeframes (2023–24: 71 per cent).

Improvements in the quality and timeliness of financial statements supports observations made by the ANAO that financial reporting processes across the Australian Government sector continues to improve.

Effective audit committees, internal governance arrangements and financial reporting functions support the effective preparation of annual financial statements, providing accountability and transparency over the financial management of those entities.

3.72 The primary purpose of financial statements is to provide relevant and reliable information to users about a reporting entity’s financial position. Financial statements preparation is often a complex task, involving compliance with several requirements established by Australian Accounting Standards and the Public Governance, Performance and Accountability (Financial Reporting) Rule 2015.

3.73 To provide relevant and reliable financial information to the users, entities should prepare quality financial statements in a timely manner to support entities to meet legislative reporting obligations including the tabling of annual reports. The preparation of quality financial statements will be demonstrated by adherence to a well-defined financial statements preparation timetable with minimal adjustments required to financial statements throughout the audit process.

3.74 In concluding an audit, the ANAO reports on the quality of financial statements preparation to entities. The following measures are considered by the ANAO when assessing the quality of the financial statements preparation process:

- number and quantum of adjusted and unadjusted audit differences; and

- timeliness of financial statements preparation.

3.75 At the completion of the 2024–25 financial statements audits, the ANAO reported one moderate audit finding and six minor audit findings relating to processes supporting financial statements preparation (2023–24: two moderate and 13 minor findings).

Financial statements preparation

3.76 The ANAO assessed the timeliness of financial statements preparation. Timeliness in preparation was assessed by comparing the date of delivery of the financial statements to previously agreed timeframes. The timeframe was established by entities and agreed with audit teams for the delivery of financial statements.

3.77 Timeliness in financial statements preparation in 2024–25 overall improved compared to 2023–24, with delivery of financial statements:

- in line with the agreed timeframes achieved by 74 per cent of entities (2023–24: 71 per cent);

- a further eight per cent of entities delivered financial statements within two working days of the agreed timeframe (2023–24: 10 per cent); and

- nineteen per cent of entities delivered financial statements after two working days of the agreed timeframe (2023–24: 19 per cent).

Audit differences

3.78 The quality of financial statements preparation is also assessed by considering the number and value of audit differences identified. Throughout the financial statements audit process, audit differences other than those considered trivial are communicated to entities. Entities are encouraged to adjust all audit differences. The total number of individual audit differences identified in 2024–25 decreased compared with 2023–24. A total of 186 individual audit differences were identified in 2024–25 (2023–24: 209) which impacted the revenue, expenses, assets and equity balances reported. The ANAO also identified 236 audit adjustments associated with the presentation and disclosure of financial statements.

3.79 A key indicator of the quality of entity financial statements is whether audit differences identified are adjusted by entities. Of the 186 audit differences identified by the ANAO during 2024–25, 53 or 28 per cent remained unadjusted by entities (2023–24: 80 or 38 per cent). Of these unadjusted differences, 25 related to material entities (2023–24: 40).16

3.80 Table 3.8 shows that the net value impact of unadjusted audit differences compared to the prior year has decreased for revenue, expense and liabilities. There has been an increase net value impact compared to 2023–24 for assets.

Table 3.8: Total value of unadjusted audit differences ($ million)

|

|

2024–25 |

2023–24 |

||||

|

Debit impact |

Credit impact |

Net impact |

Debit impact |

Credit impact |

Net impact |

|

|

Revenue |

3.4 |

(7.1) |

(3.6) |

$18.4 |

$(13.5) |

$4.9 |

|

Expenses |

129.6 |

(99.5) |

30.1 |

$87.4 |

$(197.1) |

$(109.7) |

|

Assets |

224.5 |

(635.5) |

(411.0) |

$96.6 |

$(62.5) |

$34.1 |

|

Liabilities |

99.2 |

(2.2) |

97.0 |

$168.0 |

$(104.2) |

$63.8 |

|

Equity |

514.9 |

(227.3) |

287.6 |

$59.6 |

$(52.7) |

$6.9 |

|

Number of adjustments |

53 |

80 |

||||

Source: ANAO analysis of entity 2024–25 and 2023–24 closing reports.

3.81 The ANAO also considers the impact of the unadjusted audit differences on the CFS. Of the unadjusted differences identified in the 2024–25 financial statements audits, a total of three adjustments were reported to the preparer of the CFS, the Department of Finance (Finance) and was subsequently adjusted in the CFS.

3.82 The total value of adjusted audit differences has increased compared to 2023–24 for expenses, assets and equity. There was a decrease in adjusted audit differences relating to revenue and liabilities. Table 3.9 shows the net value impact of adjusted audit differences compared to 2023–24.

Table 3.9: Total value of adjusted audit differences ($ million)

|

|

2024–25 |

2023–24 |

||||

|

Debit impact |

Credit impact |

Net impact |

Debit impact |

Credit impact |

Net impact |

|

|

Revenue |

135.4 |

(42.1) |

93.3 |

186.4 |

(1,363.2) |

(1,176.8) |

|

Expenses |

397.6 |

(7,138.0) |

(6,740.4) |

3,235.6 |

(566.6) |

2,669.0 |

|

Assets |

191.4 |

(1,046.2) |

(854.8) |