Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 21 of 2005–06

Audit of Financial Statements of Australian Government Entities for the Period Ended 30 June 2005

Published

Wednesday 21 December 2005

Portfolio

Across Entities

Entity

across agency

Sector

Cross Government

The focus of this report is on the year end results of the financial statement audits of all general purpose reporting entities for the 2004–05 financial year. Financial management issues (where relevant) arising out of the audits and their relationship to internal control structures are also included in this report.

Summary

Introduction

The Auditor-General Act 1997 establishes the mandate for the Auditor-General to undertake financial statement audits of all Commonwealth entities including those of government departments, statutory authorities and government business enterprises.

Financial statement audits are an independent examination of the financial accounting and reporting of public sector entities. The results of the examination are presented in an audit report, which expresses the auditor's opinion on whether the financial statements as a whole and the information contained therein, fairly reflect the results of each entity's operation and its financial position. The disclosures and management representations made in the financial statements by the entity are assessed against relevant accounting standards, and legislative and other reporting requirements.

In addition to undertaking financial statement audits, the Australian National Audit Office (ANAO) delivers two reports annually to Parliament addressing the outcomes of the financial statement audit process. The first of these, Audit Report No.56 2004–2005 ‘Interim Phase of the Audit of General Government Sector Entities for the Year Ending 30 June 2005' provided an update of the ANAO's assessment of audit findings relating the internal control structures of major entities, including governance arrangements, information systems and control procedures through to March 2005. The findings summarised in that report arose from the interim phase of the financial statement audits of major Australian Government reporting entities. This interim phase of an audit program is designed to assess the reliance that can be placed on control structures to produce complete, accurate and valid information for financial reporting purposes.

This report, ‘Audits of the Financial Statements of Australian Government Entities' complements the first report mentioned above, and provides a summary of the final audit results of the audits of the financial statements of all Australian Government reporting entities, including the Consolidated Financial Statements for the Australian Government.

The audit findings in this report have been reported to the management of the entity, and to the responsible Minister(s).

Results of the audits of financial statements

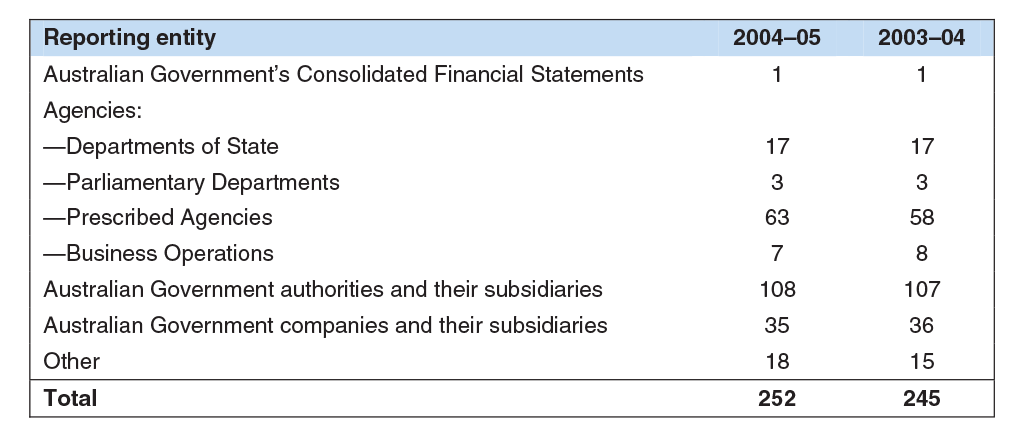

The ANAO is responsible for the audit of the financial statements of 252 Australian Government entities (refer to the following table). The total number reflects the net result of:

- the creation of a number of new entities;

- the reclassification of several entities in 2004–05; and

- the wind-up of several Australian Government authorities and companies.

Table 1 Type and number of entities audited

Source: ANAO analysis

For the 2004–05 financial year, the ANAO has issued 213 unmodified audit opinions (clear opinions); 4 ‘qualified' audit opinions; 3 audit reports containing an ‘emphasis of matter'; and 18 audit reports containing ‘other statutory matters'. At the date of this report, 14 sets of financial statements were still being audited. The above includes opinions issued on 4 entities that ceased operations during 2004–05.

The material portion of the Australian Government's revenues, expenses, assets and liabilities in the 2004–05 financial year are accounted for by a relatively small number of Australian Government entities, notably, the Departments of Defence, Family and Community Services, Health and Ageing, the Australian Office of Financial Management and the Australian Taxation Office.

The focus of this report is on the year end results of the financial statement audits of all general purpose reporting entities for the 2004–05 financial year. Financial management issues (where relevant) arising out of the audits and their relationship to internal control structures are also included in this report.

The report is organised as follows:

- Chapter One—Financial Reporting Framework—provides commentary on the structure of and issues in relation to the Australian Government's financial framework.

- Chapter Two—Results of the Audit of the Consolidated Financial Statements of the Australian Government—provides details of the audit of the Consolidated Financial Statements for 2004–05.

- Chapter Three—Summary Results of the Audits of Financial Statements—describes the final results of audits of the financial statements, and provides details of qualifications and any matters emphasised in audit reports.

- Chapter Four—Issues Arising from the Audits of Financial Statements—provides an overview of some of the issues and challenges involved in the timely preparation and audit of the financial statements of Australian Government entities.

- Chapter Five—Results of the Audits of Financial Statements by Portfolio—provides the detailed results of the individual financial statement audits and any additional significant control matters identified since Audit Report No.56, 2004–2005. It is structured in accordance with the portfolio arrangements established by the Administrative Arrangements Order of 16 December 2004. For reporting purposes, this reflects the portfolio arrangements, which existed at 30 June 2005.

- Chapter Six—Results of the Review of Triple Bottom Line Reporting—provides details of the results of audit procedures undertaken to provide an opinion on the Triple Bottom Line Reports of the Department of Family and Community Services and the Department of the Environment and Heritage.