Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 16 of 2014–15

Audits of the Financial Statements of Australian Government Entities for the Period Ended 30 June 2014

Published

Thursday 18 December 2014

Portfolio

Across Entities

Entity

Across Entities

Contact

Please direct enquiries relating to reports through our contact page.

This report complements the interim phase report published in June 2014 (Audit Report No.44 2013–14), and provides a summary of the final audit results of the audits of the financial statements of 251 Australian Government entities, including the Consolidated Financial Statements for the Australian Government.

Summary

1. The Auditor-General Act 1997 establishes the mandate for the Auditor-General to undertake financial statement audits of all Australian Government entities including Commonwealth entities and Commonwealth companies.1 The Auditor-General Act 1997 also provides the authority for financial statement and other specified audits to be undertaken by arrangement in accordance with section 20 of that Act.

2. The preparation of audited financial statements in compliance with legislative requirements is a key element of the financial management and accountability regime applicable to Australian Government entities. It is generally accepted in both the private and public sectors that a good indicator of the effectiveness of an entity’s financial management is the timely finalisation of its annual financial statements, accompanied by an unmodified audit opinion. Australian Government entities, in cooperation with the Australian National Audit Office (ANAO), devote considerable effort to achieving timeliness in financial reporting.

3. Financial statement audits are an independent examination of the financial accounting and reporting of public sector entities. The results of the examination are presented in an auditor’s report, which expresses the auditor’s opinion on whether the financial statements as a whole and the information contained therein fairly present each entity’s financial position and the results of its operations and cash flows. The accounting treatments and disclosures reflected in the financial statements by the entity are assessed against relevant Accounting Standards and legislative reporting requirements.

4. In addition to undertaking financial statement audits, the ANAO tables two reports annually addressing the outcomes of the financial statement audits of public sector entities. The first of these, Audit Report No. 44 2013–14 Interim Phase of the Audits of the Financial Statements of Major General Government Sector Agencies for the Year Ending 30 June 2014, outlined the ANAO’s assessment of audit findings relating to the internal controls of major entities, including governance arrangements, information systems and control procedures. The findings summarised in that report are the results of the interim phase of the financial statement audits of major General Government Sector agencies.

5. This report complements the interim phase report referred to above, and provides a summary of the final audit results of the audits of the financial statements of all Australian Government entities, including the Consolidated Financial Statements for the Australian Government2.

6. The audit findings in this report have been reported to the management of each entity, and to the responsible Minister(s).

Accounting and auditing framework developments

7. While the Public Sector Reporting Framework remained relatively stable in 2013–14, a major change was the introduction of new rules on fair value measurement and disclosure. The new requirements are outlined in Australian Accounting Standard AASSB 13 Fair Value Measurement that applies to reporting periods beginning after 1 January 2013.

8. There are ongoing initiatives by both Australian and international standard setters to explore opportunities to simplify disclosures in financial statements to make them more useful to users. A number of other projects are also underway that have implications for the public sector including those relating to the disclosure of transactions with related parties, reporting of service performance and new accounting rules for grants, taxes and appropriations.

9. In February 2014, the International Auditing and Assurance Board released A Framework for Audit Quality that aims to raise awareness of key aspects of audit quality.

Summary of audit findings

10. The ANAO is responsible for the audits of the financial statements of all Australian Government entities. For the 2013–14 financial year, the Auditor-General and senior staff under delegation, issued 251 auditor’s reports, all of which were unmodified. Eight of these reports included an emphasis of matter3; and 154 contained a reference to other legal and regulatory requirements5.

11. The reference to other legal and regulatory requirements mainly referred to actual or potential breaches of section 83 of the Constitution. A breach of section 83 of the Constitution occurs if payments are not made in accordance with conditions required by law. Where potential breaches have been reported, relevant agencies have indicated that the circumstances giving rise to this issue would continue to be investigated and legislative amendments developed where appropriate.

12. The auditor’s report on the Consolidated Financial Statements also referred to the High Court’s decision on Commonwealth expenditure in Williams v Commonwealth [2014] 288 HCA 23, and to the disclosure that the Australian Government will continue to monitor and assess risk and decide on any appropriate actions to respond to risks of expenditure not being consistent with constitutional requirements.

Consolidated financial statements

13. The Consolidated Financial Statements that present the consolidated whole of government financial results inclusive of all Australian Government controlled entities, as well as the General Government Sector financial report, were signed by the Minister for Finance on 20 November 2014.

14. The operating result attributable to the Australian Government disclosed in the 2013–14 Consolidated Financial Statements was a deficit of $43.0 billion (2012–13: deficit of $3.8 billion). At 30 June 2014, the reported fiscal balance was a deficit of $42.2 billion (2012–13: deficit of $28.0 billion) and the reported negative net worth position was $264.3 billion (2012–13: negative $210.5 billion). These outcomes reflect the financial effect of government policies and the economic environment for the year ended 30 June 2014 and the associated movement in assets and liabilities as at the financial year end, particularly as a result of the decrease in the long term government bond rate that is used to discount significant assets and liabilities.

15. The Consolidated Financial Statements provide explanations of variances between the original budget and 2013–14 actuals as part of the audited set of Australian Government financial statements. Commentary on these variances is provided in chapter 3 of this report.

16. The auditor’s report on the 2013–14 Consolidated Financial Statements was issued on 20 November 2014 and expressed the opinion that the statements give a true and fair view of the Australian Government’s and the General Government Sector’s financial position as at 30 June 2014 and their financial performance and cash flows for the year then ended. As mentioned above, the auditor’s report included a reference to the aggregate position relating to actual and potential breaches of section 83 of the Constitution and to the High Court’s most recent decision on Commonwealth expenditure in Williams.

Entity financial statements

17. As indicated above, no auditors’ reports of Australian Government entities were modified in 2013–14. This is a good result and reflects well on the integrity of financial reporting by all Australian Government entities.

18. There was a small increase in the number and significance of issues arising from the final phase of all 2013–14 financial statement audits of individual entities finalised by 30 November 2014. The 32 significant and moderate audit findings reported in 2013–14 was a small increase on the 30 findings reported in 2012–13. Issues that are common across a number of entities that were identified in the final audit phase that required attention by entities were in respect of: controls in entities’ IT environments, such as the management of user access and the segregation of duties (this issue has been identified consistently for a number of years); quality assurance and financial reporting, particularly the preparation of entity financial statements (these issues increased noticeably in 2013–14); and asset management processes including the valuation of assets and the reporting of inventory.

19. Our audits also found that generally entities had made good progress in addressing and resolving issues identified during the 2013–14 interim audit phase and previous audits.

20. The ANAO continues to include an assessment of compliance in relation to annual appropriations, special appropriations, special accounts and the investment of public moneys in its financial statement audits. There continues to be a high level of compliance in most of these areas. However, as mentioned above, the auditor’s report on the financial statements of a number of entities continued to mention actual or potential breaches of section 83 of the Constitution, and referred to the note disclosure in each entity’s financial statements. The financial statements of a number of entities also referred to the Australian Government’s intention to continue to have regard to developments in case law, including the High Court’s decision on Commonwealth expenditure in Williams.

Commentary on financial statement related matters

Analysis of entities’ financial statements

21. An analysis of material entities’ operating results identified that, consistent with previous years, entities overall were appropriately managing their finances for the three year period ending 30 June 2014.

22. An analysis of the balance sheet positions of material entities as at 30 June 2014 identified that the majority of entities continued to have a strong balance sheet position. Nevertheless, the analysis of a small number of entities, in particular, should continue to monitor their financial position and improve it, where practicable.

Machinery of Government changes

23. The scale of the Machinery of Government (MoG) changes flowing from the Administrative Arrangements Order of 18 September 2013, was significant. Over 13 000 staff were affected and appropriations of approximately $1 billion were transferred between entities.

24. Implementation of MoG changes can be complex and very resource intensive, requiring entities to manage a broad range of issues while at the same time continuing to deliver government services. Discussions with entities identified that a number of initiatives had been taken that contributed positively to the implementation of the MoG changes, including the identification of lessons learned. The ANAO has made a number of suggestions to assist with the management of future machinery of government changes.

Preparation of entity financial statements

25. A majority of entities’ 2013–14 financial statements were finalised in the period July to September 2014, a situation consistent with previous years. There was, however, a noticeable slippage in overall timeframes in which the financial statements were completed, with less entities meeting the deadline for audit cleared statements and 15 per cent more statements being signed in the period September to November 2014, compared with 2013. This contributed to late adjustments being made to the 2013–14 Final Budget Outcome and to a compressed timeframe for the preparation and audit of the 2013–14 Consolidated Financial Statements.

26. There was also deterioration in the 2013–14 financial statements preparation processes in a small number of entities. Areas that required improvement included quality assurance processes, adherence to timetables and the quality of supporting working papers. The 2013 MoG changes also affected the timetable for the preparation of the 2013–14 financial statements in a small number of entities.

Future audit coverage

27. The ANAO will continue to work closely with entity audit committees and management with the aim of assisting entities to continue to meet their financial management responsibilities, including addressing areas where improvements are warranted.

1. Introduction

This chapter provides background to the audits of the financial statements of Australian Government entities, sets out the structure of this report and acknowledges the contribution of staff of the ANAO and entities in the preparation of this report.

Background

1.1 Each year the results of the annual financial statement audit work undertaken by the ANAO are reported to the Parliament in two reports. This report provides the results of the audit of the financial statements of all Australian Government entities and the Consolidated Financial Statements of the Australian Government for the financial year ended 30 June 2014. The results of the interim phase6 of the audits of major agencies were reported in Audit Report No. 44 2013–14 Interim Phase of the Audits of the Financial Statements of Major General Government Sector Agencies for the year ending 30 June 20147. These reports also discuss contemporary issues and practices impacting on public sector entities’ financial reporting responsibilities, and the ANAO’s responsibilities.

1.2 The preparation of audited financial statements in compliance with legislative requirements is a key element of the financial management and accountability regime applicable to Australian Government entities. It is generally accepted in both the private and public sectors that a good indicator of the effectiveness of an entity’s financial management is the timely finalisation of its annual financial statements, accompanied by an unmodified audit opinion. Australian Government entities in cooperation with the ANAO devote considerable effort to achieving timeliness in financial reporting.

1.3 The ANAO conducts its financial statement audits in accordance with the ANAO Auditing Standards that incorporate the Australian Auditing Standards. An audit performed in accordance with the Australian Auditing Standards is designed to provide reasonable assurance that a financial report, taken as a whole, is free from material misstatement whether due to fraud or error. Reasonable assurance as defined in the Australian Auditing Standards means a high, but not absolute, level of assurance. It is reached when the auditor has obtained sufficient appropriate audit evidence to reduce audit risk (that is, the risk that the auditor expresses an inappropriate opinion when the financial report is materially misstated) to an acceptably low level. However, reasonable assurance is not an absolute level of assurance, as an audit has inherent limitations. This is because most of the audit evidence on which the auditor draws conclusions and bases the auditor’s opinion is persuasive rather than conclusive.8

1.4 The report is organised as follows:

- Chapter Two Financial Reporting and Auditing Frameworks provides commentary on recent developments in the financial reporting and auditing frameworks relevant to the Australian Government and its reporting entities.

- Chapter Three The Audit of the Consolidated Financial Statements outlines the results of the audit of the Consolidated Financial Statements of the Australian Government, which includes the whole of government and the General Government Sector financial reports, of the Australian Government for the year ended 30 June 2014.

- Chapter Four Commentary on Financial Statement Related Matters provides an analysis of entities’ operating results and balance sheets, and a discussion of the 2013 Machinery of Government (MoG) changes.

- Chapter Five Summary of Audit Results includes: a summary of issues included in the auditors’ reports on entities’ 2013–14 financial statements including a commentary on actual and potential breaches of section 83 of the Constitution in a number of entities and the High Court’s most recent decision on Commonwealth expenditure in Williams; a summary of other audit findings identified in the 2013–14 audits; and a commentary on the preparation of entities’ 2013–14 financial statements and the 2013–14 Certificate of Compliance process.

- Chapter Six Results of Financial Statement Audits by Portfolio summarises the results of the 2013–14 financial statement audits of individual Australian Government entities. The chapter is structured in accordance with the portfolio arrangements established by the Administrative Arrangements Order (AAO) of 18 September 2013, as amended on 3 October 2013. For reporting purposes, this reflects the portfolio arrangements that existed on 30 June 2014. A comprehensive table of the MoG changes that took effect on 18 September 2013 is at appendix 1, and a summary of MoG changes is included in relevant portfolio sections.

1.5 A glossary of commonly used accounting terms is [available here].

Acknowledgements

1.6 I would like to acknowledge the professionalism and commitment of my staff in finalising the audits of 251 entities’ financial statements in the tight timeframes required. This work has enabled the tabling of this report in a timely manner for the information of the Parliament. I would also like to acknowledge the important role that Audit Committees, Chief Financial Officers and other entity staff involved in financial statement preparations continue to play. Their effort in providing information and assistance to the ANAO is much appreciated.

2. Financial Reporting and Auditing Frameworks

This chapter provides commentary on recent developments in the financial reporting and auditing frameworks relevant to the Australian Government and its reporting entities.

Introduction

2.1 The Australian Government’s financial reporting framework is based, in large part, on standards made independently by the Australian Accounting Standards Board (AASB). This framework is designed to support decision‐making by, and accountability to, the Parliament. The financial reporting and auditing frameworks that applied for 2013–14 are illustrated in appendices 3 and 4 of this report.

2.2 The AASB bases its accounting standards on the International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB). Because IFRS are designed primarily for use by for‐profit organisations, the AASB amends the IFRS to reflect the unique transactions and events of the public and not‐for‐profit private sectors. In doing so, it takes into account standards issued by the International Public Sector Accounting Standards Board (IPSASB). The Minister for Finance may prescribe additional financial reporting requirements for Australian Government entities other than companies; prior to 2014–15 this was achieved through the Finance Minister’s Orders (FMOs) for financial reporting9.

2.3 Major changes to Australian Accounting Standards effective in 2013–14 included new requirements on fair value measurement and disclosure, and an option to remove certain disclosures from financial statements. To date, this option has not been endorsed by the Minister for Finance for application by Australian Government entities.

2.4 Major developments in accounting standards internationally will continue to be a significant driver of changes to Australian Accounting Standards. At the international level, there have been new standards on revenue and financial instruments. In addition, significant proposed changes to accounting for leases are well progressed.

2.5 The audits of the financial statements of Australian Government entities are conducted in accordance with ANAO Auditing Standards, which are made by the Auditor-General under section 24 of the Auditor-General Act 1997. The ANAO Auditing Standards incorporate, by reference, the auditing standards made by the Australian Auditing and Assurance Standards Board (AUASB). The AUASB bases its standards on those made by the International Auditing and Assurance Standards Board (IAASB).

2.6 The international and Australian standards for auditing financial statements were subject to a major revision and re-issue which concluded in 2009. This ‘Clarity Project’ was a comprehensive program to enhance the clarity of the standards. The first major change since 2009 is in relation to the standard on using the work of internal audit. This change takes effect from 2014–15.

Recent changes to the Australian public sector reporting framework

Fair value measurement

2.7 Prior to 2011, accounting standards required, or allowed, entities to present their assets and liabilities at fair value in the balance sheet. However, the guidance on measuring fair value was high level, spread among several standards, and sometimes inconsistent.

2.8 In 2011, the IASB issued an accounting standard on fair value measurement. This standard clarifies the definition of fair value, provides a single framework for measuring fair value and enhances the associated disclosures. The AASB subsequently issued AASB 13 Fair Value Measurement, replicating the IASB standard. AASB 13 applies to reporting periods beginning on or after 1 January 2013.

Differential financial reporting – reduced disclosure requirements

2.9 In 2010, the AASB issued AASB 1053 Application of Tiers of Australian Accounting Standards, which applies to reporting periods beginning on or after 1 July 2013. AASB 1053 distinguishes two tiers of reporting requirements. Entities in the first tier must prepare financial statements in accordance with the full suite of Australian Accounting Standards. Federal, state and territory governments are included in this tier. Entities in the second tier would still present the same primary financial statements but with substantially reduced note disclosure. Government controlled entities may opt for either tier, subject to the requirements of their regulator. This provides an opportunity to reduce the reporting burden for the majority of government entities.

2.10 The Minister for Finance, who performs the role of regulator for Australian Government entities, currently requires all Australian Government entities to apply the first tier reporting requirements.

2.11 Particularly in the context of identifying opportunities to reduce compliance requirements, the ANAO considers that the differential reporting regime provides an opportunity to reduce the administrative workload of Australian Government entities and make financial reports easier to read, while still preserving sufficient disclosures to satisfy the needs of the Parliament.

Budgetary Reporting

2.12 The Australian Government prepares its financial statements under AASB 1049 Whole of Government and General Government Sector Financial Reporting. AASB 1049 requires governments to compare their financial results to their original budgets as presented to the Parliament, and to explain major variances where they are relevant to assessing performance and accountability.

2.13 The AASB has extended the budget reporting requirements to all not-for-profit entities in the General Government Sector (GGS). This change is contained in AASB 1055 Budgetary Reporting, issued in 2013 and applying to reporting periods beginning on or after 1 July 2014.

Future changes in the public sector reporting framework

2.14 There are ongoing initiatives by both Australian and international standard setters to explore opportunities to simplify disclosures in financial statements to make them more useful to users. In 2014, the AASB published a staff paper10 proposing ways in which entities can reduce unnecessary disclosures in their financial statements. Similarly, in 2013 the IASB commenced work to review disclosures in existing standards to identify and assess conflicts, duplication and overlaps11.

2.15 Further changes to the framework are expected over the next few years, as projects by Australian and international accounting standard setters lead to new accounting standards for both the public and private sectors.

2.16 Projects specific to the public sector include: disclosure of transactions with related parties; reporting of service performance; and new accounting rules for grants, taxes and appropriations. Projects aimed primarily at the private sector, but with public sector implications, include major revisions to the accounting standards on financial instruments, revenue recognition and leasing.

Recent developments in auditing financial statements

A Framework for Audit Quality

2.17 In February 2014, the IAASB released A Framework for Audit Quality. The objectives of the framework include raising awareness of the key elements of audit quality, encouraging key stakeholders to explore ways to improve audit quality and facilitating greater dialogue between key stakeholders on the topic. The framework describes the input, process and output factors that contribute to quality at the engagement, audit firm and national levels and demonstrates the importance of appropriate interactions among stakeholders (including how those charged with governance can influence the quality of an audit) and the importance of various contextual factors.

Changes in Australian Auditing Standards

2.18 As reported in Audit Report No.44 2013–14, Interim Phase of the Audits of the Financial Statements of Major General Government Sector Agencies for the year ending 30 June 2014, the AUASB has substantially revised ASA 610 Using the Work of Internal Auditors. The revision provides a more robust framework for evaluating and, where appropriate, using the work of an entity’s internal audit function. To help preserve external auditor independence, the revision includes an express prohibition on using internal auditors to perform audit procedures under the direction, supervision and review of the external auditor. The revised standard applies to reporting periods commencing on or after 1 January 2014.

2.19 There have been no other substantive changes to Australian Auditing Standards affecting the audit of entities’ 2014–15 financial statements.

Future changes in auditing financial statements

Auditor reporting

2.20 At its September 2014 meeting, the IAASB approved new and revised auditor reporting standards aimed at enhancing the value of auditor reporting on financial statements. The IAASB plans to release the standards in January 2015. The AUASB is aiming for a single public exposure of draft standards based on the finalised IAASB standards in mid-2015.

2.21 The most important change arising from the new and revised standards is the introduction of a new standard, ISA 701, Communicating Key Audit Matters in the Independent Auditor’s Report. This ISA will apply to audits of the financial statements of listed entities and also to circumstances when the auditor otherwise decides or is required by law to communicate key audit matters in the auditor’s report.

2.22 The purpose of communicating key audit matters is to enhance the communicative value of the auditor’s report by providing greater transparency about the audit that was performed. Communicating key audit matters provides additional information to intended users of the financial statements to assist them in understanding those matters that, in the auditor’s professional judgment, were of most significance in the audit of the financial statements. Communicating key audit matters may also assist intended users of the financial statements to understand the entity and the areas of significant management judgment in the audited financial statements.

Other changes to the auditing standards

2.23 The standard-setting Boards are also working on other new and revised auditing standards, including in relation to the auditor’s responsibility for other information published with the audited financial statements and the auditing of financial statement disclosures.

Conclusion

2.24 Ongoing developments in accounting and auditing frameworks and standards continue to have an impact on the financial reporting responsibilities of public sector entities and on the ANAOʹs auditing methodology. The ANAO will continue to assist Australian Government entities through client seminars and publications that explain new regulatory and accounting requirements.

2.25 While there were few changes in Australian Accounting Standards during 2013–14, significant changes to the financial reporting framework are under way, both internationally and in Australia. A number of the proposed changes will affect the Australian public sector over the next few years, particularly in relation to the reporting of financial instruments and lease accounting.

2.26 Enhancing audit quality and auditor communication continue to be the top priorities of international auditing standard boards.

3. The Audit of the Consolidated Financial Statements

This chapter outlines the results of the audit of the Consolidated Financial Statements of the Australian Government, which includes the whole of government and the General Government Sector financial reports for the year ended 30 June 2014, and the Australian Government’s financial outcome for 2013–14.

Background

3.1 Government accountability and transparency is supported by the preparation and audit of the Australian Government’s Consolidated Financial Statements (CFS). The CFS and the associated financial analysis provide information to assist users in assessing the annual financial performance and position of the Australian Government.

3.2 The CFS are one source of information on the Government’s financial performance and position. Other information sources include the Budget and Budget updates presented to Parliament12, the Final Budget Outcome13 and Intergenerational reports14. These various sources provide information on a range of policy and financial matters, including the medium-term and intergenerational effect of decisions.

3.3 The application of AASB 1049 Whole of Government and General Government Sector Reporting, has resulted in the closer harmonisation of the statistical and accounting standards for the reporting of budget and financial statement information. As a result, comprehensive and consistent financial information is presented in both the Budget Papers and the CFS. AASB 1049, by incorporating elements of the conceptual and accounting framework on which the Australian Bureau of Statistics’ Government Finance Statistics (GFS) is based, provides a single framework for financial reporting by governments in Australia.

3.4 The CFS present the consolidated whole of government financial results inclusive of all Australian Government controlled entities, as well as the General Government Sector (GGS) financial report. The 2013–14 CFS are prepared in accordance with the regulations of the Financial Management and Accountability Act 199715 and the requirements of the Australian Accounting Standards as mentioned above. The CFS operating statement and balance sheet are prepared on an accrual basis16, with the cash flow statement prepared on a cash basis.

3.5 Since 2009–10 the CFS has incorporated both the whole of government and GGS financial reports required by AASB 1049, and the 2013–14 CFS again includes both of these reports. The CFS and the auditor’s report can be accessed from the Department of Finance’s website17.

3.6 This chapter discusses the auditor’s report on the 2013–14 CFS, the high level impact of the economic conditions and associated government measures and decisions on the Australian Government’s financial position as represented in the CFS and the significant disclosures included in the CFS. The commentary in this chapter has focussed on the financial results at the consolidated whole of government level rather than at the GGS level. Significant variances between the actual GGS results and the original GGS budget presented to Parliament are discussed in paragraphs 3.29 and 3.30.

Auditor’s Report

3.7 The CFS were signed by the Minister for Finance on 20 November 2014 and an unmodified auditor’s report was issued on the same day.

3.8 The auditor’s report on the 2013–14 CFS, which includes the GGS report, expressed the opinion that the statements presented a true and fair view of the financial operations and position of the Australian Government.

3.9 A report on other legal and regulatory requirements was included in the auditor’s report following the opinion on the 2013–14 CFS to draw attention to the note disclosure included in the CFS in respect of:

- actual and potential breaches of section 83 of the Constitution. Further information on this matter is included at paragraphs 3.24 and 3.25;

- payments made under the National School Chaplaincy and Student Welfare Programme that were held by the High Court18 to be invalid on the grounds that they were not supported by a Commonwealth constitutional head of power. Further information on this matter is included at paragraph 3.26; and

- the Australian Government continuing to have regard to developments in case law, including the High Court’s most recent decision on Commonwealth expenditure in Williams v Commonwealth [2014] HCA 23, and that the Australian Government will continue to monitor and assess risk and decide on any appropriate actions to respond to risks of expenditure not being consistent with constitutional or other legal requirements.

Australian Government’s financial outcome for 2013–14

3.10 The reported 2013–14 operating result19 attributable to the Australian Government was a deficit of $43.0 billion (2012–13: deficit of $3.8 billion), the fiscal balance20 was a deficit of $42.2 billion (2012–13: deficit of $28.0 billion) and the reported negative net worth21 position was $264.3 billion (2012–13: negative $210.5 billion). These outcomes reflect the financial effect of government policies and the economic environment for the year ended 30 June 2014 and the associated movement in assets and liabilities as at the financial year end, particularly as a result of the decrease in the long term government bond rate22 that is used to discount significant assets and liabilities. Further information on the significant movements between 2012–13 and 2013–14 in the operating statement and the balance sheet is provided in the commentary that is published with the audited CFS, and is discussed below.

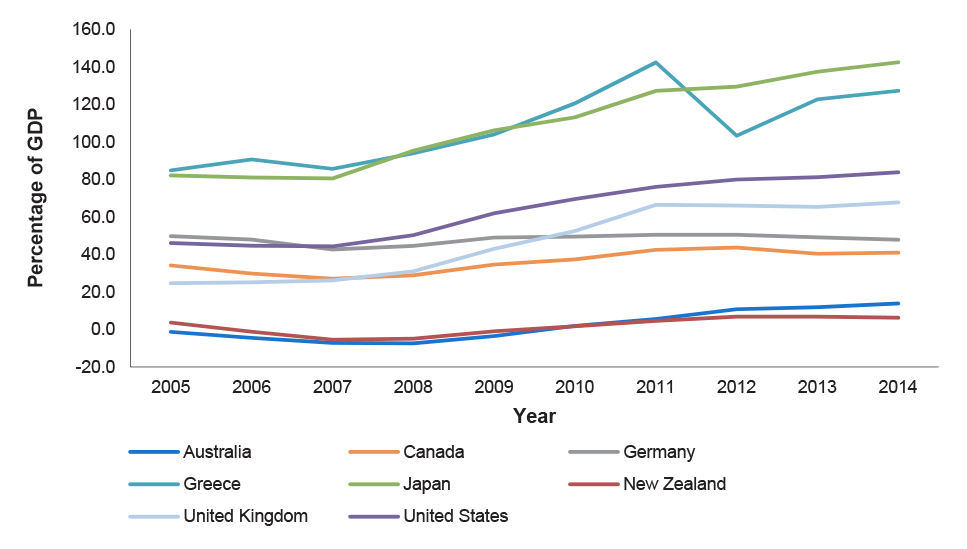

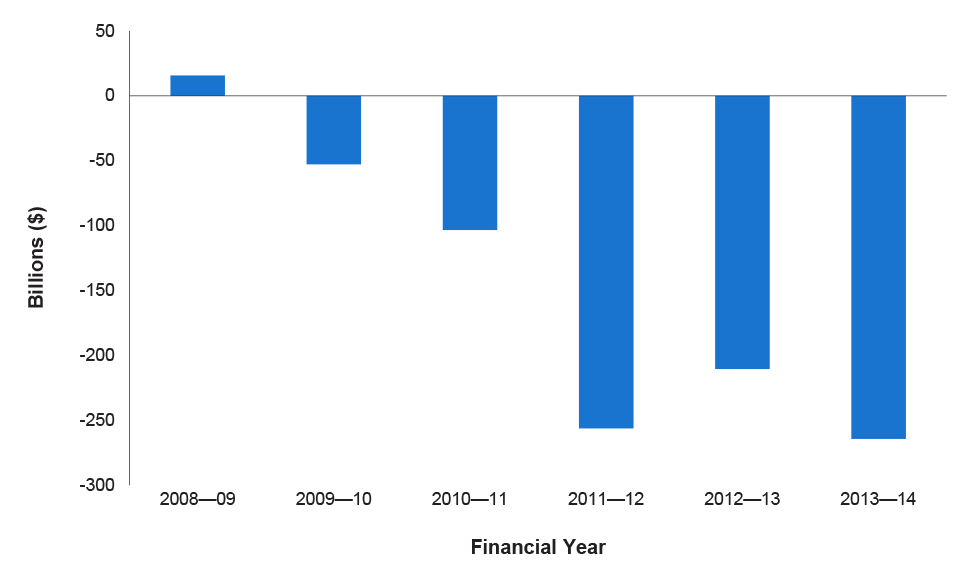

3.11 The following charts show the net financial liabilities of the Australian Government’s General Government Sector as a percentage of gross domestic product relative to some other OECD23 countries, and the Australian Government’s negative net worth. These charts show that, in broad terms, the Australian Government is in a sound financial position relative to the governments of many other countries although there continues to be rising levels of interest bearing liabilities.

Figure 3.1: General Government net financial liabilities24 as a percentage of gross domestic product25

Source: OECD Economic Outlook 95 database at http://www.oecd.org/statistics/.

Figure 3.2: Australian Government’s net worth

Source: Consolidated Financial Statements from 2008–09 to 2013–14.

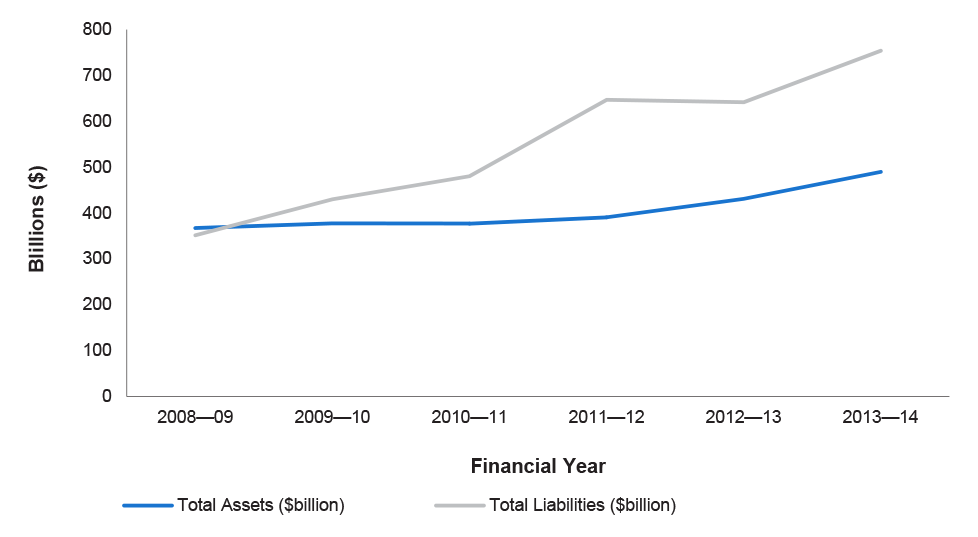

3.12 There was a deterioration in the Australian Government’s net worth in 2013–14 and net worth remains in a negative position as total liabilities continue to exceed total assets (see Figure 3.3).

Figure 3.3: Australian Government’s total assets and total liabilities

Source: Consolidated Financial Statements from 2008–09 to 2013–14.

3.13 The significant movements in the CFS affecting the operating statement and the balance sheet of the Australian Government are explained below.

Operating statement

3.14 Total revenue of the Australian Government increased by $15.7 billion in 2013–14 to $386.2 billion. The movement in revenue reflected a $14.6 billion increase in taxation revenue, primarily as a result of:

- an increase in income tax on individuals and other withholding taxation, reflecting growth in personal non-wage income;

- an increase in the goods and services tax (GST) in line with the overall growth in consumption of items subject to the GST;

- an increase in excise and customs duty revenue consistent with an increase in the volume of imported goods subject to customs duty and the introduction of a 12.5 per cent excise on tobacco from 1 December 2013;

- a relatively small increase in company tax, primarily reflecting weaker corporate profitability and the resolution of outstanding dispute matters; and

- a decrease in taxation from superannuation, due to lower than expected taxable contributions and earnings and the resolution of some outstanding disputed matters.

3.15 Total non-taxation revenues increased by $1.1 billion in 2013–14, primarily due to:

- greater revenue from sales of goods and services, mainly associated with increases in Australia Post revenue as a result of growth in its parcel business; Medibank Private health insurance revenue; immigration visa application fees due to a CPI increase on visa application charges from 1 July 2013; and housing inventory sales by Defence Housing Australia. These revenue increases were partially offset by decreases in revenue relating to fees for the guarantee of large deposits and wholesale funding as these schemes wind down and unclaimed monies under the Banking Act 1959, Life Insurance Act 1995 and Corporations Act 2001, resulting from legislative changes in 2012–13 which reduced the time before which unclaimed monies are transferred to the Commonwealth, as well as changes to the administrative arrangements for managing unclaimed monies under the Corporations Act 2001;

- an increase in dividend income, primarily relating to the Future Fund’s investment portfolio;

- a decrease in other revenue, primarily as a result of a decrease in revenue from unclaimed superannuation accounts as a result of changes in 2012–13 to the legislation surrounding the operation of lost superannuation accounts; and

- a decrease in interest income primarily in the Australian Government Nation Building Funds’ and the Future Fund’s investment portfolios and the Australian Office of Financial Management’s residential mortgage backed securities investments. These decreases were partially offset by an increase in interest from Australian dollar securities held by the Reserve Bank of Australia.

3.16 The Australian Government’s total expenses increased by $25.5 billion in 2013–14. The major causes of this increase were:

- increased direct personal benefits, grants and subsidies expenses, primarily relating to increases in:

- assistance to the aged, jobseekers, people with disabilities, carers and family tax benefit recipients due to payment indexation arrangements;

- grants to state and territory governments, primarily for general revenue assistance, road investment, rail transport, Government and non-Government school support, healthcare services; non-profit institutions, mainly relating to home support, indigenous education, child care, indigenous land and housing, well-being and community safety; local government for road infrastructure; and the multi-jurisdictional sector, primarily relating to higher education support and the university superannuation programme;

- mutually agreed write downs26, mainly relating to penalty and interest charges, by the Australian Taxation Office;

- subsidy expenses primarily due to the stronger uptake of the research and development tax incentive, the fuel tax credits scheme and carbon pricing free permits associated with the carbon pricing scheme; and

- increased operating expenses, primarily due to:

- increased expenses relating to the supply of goods and services, particularly in relation to Defence sustainment costs; the costs associated with detention centres and settlement; claims processed by Medibank Private; payments related to the Medicare Benefits Scheme which funds access to medical services; payments for pharmaceuticals and pharmaceutical services; and the costs of Australia Post services. These increases were partially offset by a decrease in supplier expenses across a number of entities;

- higher wages and salaries, primarily due to an increase in separation and redundancy programs across a number of entities;

- increased depreciation and amortisation expenses in line with the increase in non-financial assets; and

- decreased service costs of the Australian Government’s unfunded superannuation liabilities. The service cost captures the movement in the superannuation liability that results from employee service in the reporting period. As the calculation of the amount is based on a present value, it is sensitive to changes in the discount rate used for the calculation27. The longer the length of service, the greater the impact of discount rate changes. Under the relevant accounting standard, AASB 119 Employee Benefits, the discount rate used in the calculation of the service cost is based on the interest rate at the start of the year.

- increased interest expenses, primarily reflecting the interest associated with the issue of Treasury Bonds and an increase in exchange settlement balances held with the Reserve Bank of Australia; and

- increased superannuation interest expenses, mainly attributable to the higher nominal interest on superannuation, which is based on a discount rate which was higher at the beginning of 2013–14 compared to 2012–13.

3.17 Other economic flows, which include asset and liability revaluation gains and losses, moved from a gain of $69.8 billion in 2012–13 to a loss of $21.2 billion in 2013–14. The primary drivers for this movement were:

- the effect of movements in the long term government bond rate28 used to calculate the Australian Government superannuation liability. Even small movements in the bond rate can cause significant movements in the valuation of the liability. Between 30 June 2013 and 30 June 2014 the bond rate decreased by 0.2 per cent whereas between 30 June 2012 and 30 June 2013 the bond rate increased by 1.2 per cent, resulting in a $13.0 billion negative flow in 2013–14 compared to a $50.4 billion positive flow in 2012–13;

- an unrealised loss from the re-measurement of Commonwealth Government securities as at 30 June 2014 as a result of the effect of lower interest rates; and

- a change in indexation arrangements for military superannuation.

3.18 The net acquisition of non-financial assets increased by $4.5 billion in 2013–14 to $9.0 billion, primarily as a result of an increase in the purchase of non-financial assets, mainly for Defence related acquisitions and the construction of the National Broadband Network. This increase was partially offset by a decrease in the sale of non-financial assets compared to 2011–12, particularly in relation to the sale of spectrum licences.

Balance sheet

3.19 The 2013–14 CFS reported a $53.8 billion decrease in the net worth position of the Australian Government from negative $210.5 billion in 2012–13 to negative $264.3 billion in 2013–14. This decline in the negative position was a consequence of a $112.7 billion increase in liabilities, partially offset by a $58.9 billion increase in assets as at 30 June 2014.

3.20 The value of the Australian Government’s financial assets at 30 June 2014 increased by $49.5 billion, compared to 30 June 2013. The primary reasons for this increase were:

- an increase in investments, loans and placements, mainly as a result of an increase in the Australian dollar securities and foreign exchange holdings of the Reserve Bank of Australia and an increase in investments held by the Future Fund, partially offset by a decrease in deposit investments by the Australian Office of Financial Management;

- an increase in equity investments as a result of an increased investment in listed equities and listed managed investment schemes by the Future Fund; and

- an increase in advances paid, primarily due to an increase in the value of student loans under the Higher Education Loan Program.

3.21 Total non-financial assets increased by $9.5 billion in 2013–14 primarily due to increases in:

- the non-financial assets held by NBN Co Limited due to the ongoing implementation of the National Broadband Network;

- buildings held, primarily due to the finance lease arrangements for the Single Living Environment and Accommodation Precinct (LEAP) project;

- specialist military equipment and explosive ordnance held by the Department of Defence;

- intangible assets, mainly due to water entitlement acquisitions by the Department of the Environment;

- the value of land, following formal revaluations of these properties; and

- the value of heritage and cultural assets held across a number of collection institutions, following formal revaluations of these assets.

3.22 Interest bearing liabilities increased by $82.2 billion in the 2013–14 year. This increase primarily related to:

- an increase in Commonwealth Government securities on issue, which is primarily driven by the need to fund the underlying cash deficit;

- an increase in deposits held, including the Reserve Bank of Australia exchange settlement balances;

- an increase in finance leases and right of use licences entered into by NBN Co Limited for its infrastructure assets and premises; and

- an increase in loans, primarily bills of exchange and promissory notes issued to the International Monetary Fund by the Department of the Treasury.

- The above increases were partially offset by the improved performance of derivative contracts entered into by the Future Fund to manage its investment portfolio.

3.23 Provisions and payables increased by $30.6 billion in 2013–14. The main causes of this movement were:

- an increase in the defined benefit obligations for Australian Government sponsored superannuation schemes at 30 June 2014, primarily due to the downwards movement in the long term government bond rate explained in paragraph 3.17 and an increase in the indexation arrangements for some military pensions;

- an increase in the value of Australian notes on issue in line with historical trends;

- an increase in other employee liabilities, mainly resulting from actuarial adjustments for claims under the Military Rehabilitation and Compensation Act 2004 and allowances for separation and redundancy programs across a number of entities; and

- an increase in subsidies payable, primarily due to claims on hand for various subsidies administered by the Australian Taxation Office.

- The above increases were partially offset by a decrease in supplier and grant payables across a number of entities.

Significant disclosures in the CFS

Actual and potential breaches of the Constitution

3.24 Note 1.27 to the CFS states that the Australian Government is aware of the risk of a breach of section 83 of the Constitution where payments are made from special appropriations and special accounts in circumstances where the payments do not accord with conditions included in the relevant legislation. Section 83 of the Constitution requires that no money shall be drawn from the Treasury of the Commonwealth except under an appropriation made by law.

3.25 Note 1.27 to the CFS provides information on the Australian Government’s continuing review during 2013–14 of its exposure to risks of not complying with statutory conditions on payments from special appropriations and special accounts. As disclosed in Note 1.27 to the CFS, payments were made in 2013–14:

- in breach of section 83 of the Constitution, totalling $3.3 million across ten entities; and

- potentially in breach of section 83 of the Constitution, totalling $1 024.5 million across eight agencies.

3.26 Note 1.27 to the CFS also discloses that during 2013–14, the High Court in Williams v Commonwealth [2014] 288 HCA 23 held that payments made under the National School Chaplaincy and Student Welfare Programme were invalid on the grounds that they were not supported by a Commonwealth constitutional head of power. Consequently, the payments made became debts owed to the Commonwealth. The Minister for Finance waived those debts, totalling $156.1 million, under section 34(1)(a) of the Financial Management and Accountability Act 1997 on 19 June 2014.

3.27 Further, Note 1.27 to the CFS also discloses that the Australian Government continues to have regard to developments in case law, including the High Court’s most recent decision on Commonwealth expenditure in Williams v Commonwealth [2014] 288 HCA 23, and that the Australian Government will continue to monitor and assess risk and decide on any appropriate actions to respond to risks of expenditure not being consistent with constitutional or other legal requirements.

3.28 The ANAO’s auditor’s report on the CFS included a report on other legal and regulatory requirements in respect of these matters. Further details on the breaches identified by each entity are included in chapter 6 of this report.

Significant differences between original budget and actual results

3.29 Australian Accounting Standard AASB 1049 requires significant variances between the original budget presented to the Parliament and the actual results to be disclosed in the audited financial statements. These explanations are included at Note 44 to the CFS. The Australian Government only presents a budget at the GGS level, and not at the whole of government level therefore variances between budget and actual are only presented for the GGS.

3.30 The main variances explained in this note relate to:

- a decrease of $17.5 billion in actual revenue compared to the amount of revenue expected at the time the original budget was presented to Parliament in May 2013;

- a $13.5 billion increase in actual expenses compared to the original budgeted amount;

- a $12.7 billion increase in other economic flows compared to the original budget;

- an increase of $0.9 billion in the net acquisition of non-financial assets compared to the original budget;

- a $87.6 billion decrease in the net worth position when compared to the original budget; and

- a $30.9 billion larger GFS cash deficit position than the position that was included in the original budget.

Events after balance sheet date

3.31 Note 39 to the CFS discloses one significant event that occurred after the balance sheet date of 30 June 2014. This concerned the sale of Medibank Private that at 30 June 2014 was a company limited by shares and whollyowned by the Commonwealth of Australia. On 26 March 2014 the Australian Government announced a decision to proceed with the sale of Medibank Private through an initial public offering. The Medibank Private Share Offer prospectus was released on 20 October 2014. At the time of the signing of the CFS, it was expected that Medibank Private would be listed on the Australian Stock Exchange on 25 November 2014.29

Future Accounting Standard requirements specific to the CFS

Ministerial remuneration

3.32 The 2013–14 CFS has continued the approach of prior years of incorporating disclosure of ministerial remuneration in Note 6 to the CFS. The disclosure includes Cabinet Ministers that served at any time during the financial year, including those who served under the former Government that ceased on 18 September 2013. The disclosure is provided at the aggregate level only and details of individual Cabinet Ministers’ remuneration are not included.

3.33 In this context, at its May 2014 meeting the Australian Accounting Standards Board (AASB) decided to remove the not-for-profit public sector exemption from AASB 124 Related Party Disclosures with effect from 2016–17. From that time, Ministers would be considered ‘key management personnel’, and their remuneration, in aggregate, would need to be reported in the CFS for the following categories:

- short-term employee benefits;

- long-term employee benefits;

- post-employment benefits; and

- termination benefits.

3.34 Comparative year disclosure for 2015–16 will also need to be included in the 2016–17 CFS.

Defence weapons platforms

3.35 AASB 1049 requires the CFS to apply the principles and rules in the ABS GFS Manual, where this does not conflict with the Australian Accounting Standards. The Australian Accounting Standards allow these assets to be measured at fair value or at cost. The ABS GFS manual requires property, plant and equipment, which includes Defence Weapons Platforms (DWPs), to be recorded at market value. As a result, the fair value basis, providing reliable measurement is possible, is the measurement approach that should be adopted in the CFS. In December 2012, a pronouncement from the Australian Accounting Standards Board was released that granted an extension of transitional relief from the adoption of AASB 1049 as it relates to DWPs. The transitional relief extended the date of implementation to the 2014–15 financial year. The Australian Government is progressing its consideration of this matter.

4. Commentary on Financial Statement Related Matters

This chapter provides an analysis by the ANAO of material entities’ operating results and balance sheet position and commentary on Machinery of Government changes.

Analysis of entities’ financial statements

4.1 Integral to the ANAO’s financial statement audits is an understanding of the entity being audited and its environment. A key part of this process is identifying the main factors that influence an entity’s financial results. While this is undertaken for each individual entity, analysis of the total population of entities can provide insights into any systemic issues that bear on the financial performance and the financial position of entities generally.

Operating results analysis

4.2 The responsibilities of Australian Government entities are established by legislation, or determined by government, and include responsibilities for functions such as policy development, regulatory oversight and/or service delivery. In performing these responsibilities, entities are expected to manage, efficiently and effectively, the public resources made available to them.

4.3 A key measure of an entity’s financial management is its operating result for the year. Nevertheless, the operating result is not the sole measure of performance of a public sector entity as circumstances can result in an entity incurring deficits in the course of meeting its responsibilities. A history of significant deficits could, however, suggest the need for additional funding, elimination of non-value adding costs, reductions in service levels and/or improved entity financial management.

4.4 Against this background, the ANAO continued its practice of undertaking an analysis of the operating results of all material entities over a three year period. This year the analysis covered the period 2011–12 to 2013–14. This analysis is based on reported surpluses or deficits after adjusting for the amount of unfunded expenses30, where relevant. This approach highlights the full cost of operations, regardless of the particular funding model in place.

4.5 The ANAO grouped material entities into four categories, which are explained in Table 4.1 below.

Table 4.1: Operating results categories

|

Category |

Explanation |

|

D1 |

Averaged a deficit/loss for the last three years and had two or three deficits/losses greater than five per cent of total expenses. |

|

D2 |

Averaged a deficit/loss for the last three years and had one or zero deficits/losses greater than five per cent of total expenses. |

|

S1 |

Averaged a surplus/profit for the last three years less than five per cent of total expenses. |

|

S2 |

Averaged a surplus/profit for the last three years equal to or greater than five per cent of total expenses. |

Source: ANAO analysis

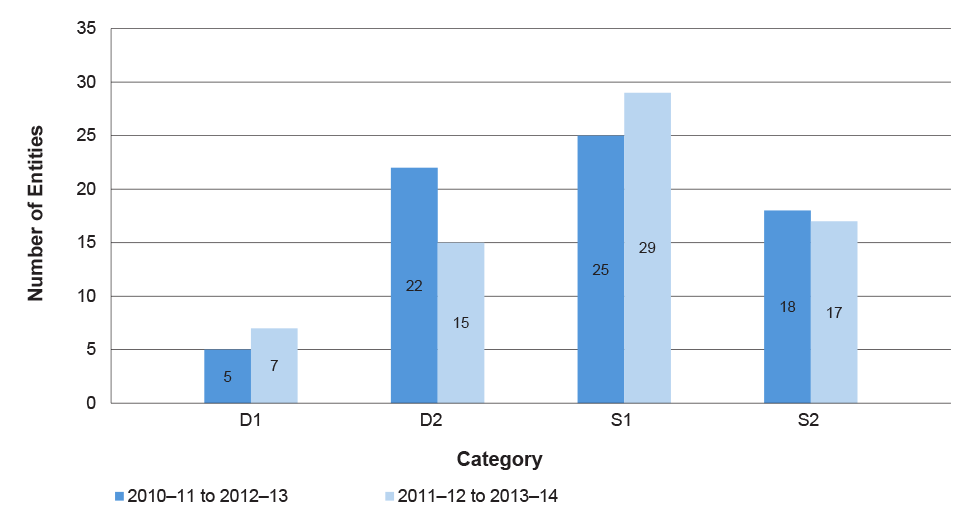

4.6 Figure 4.1 presents the results of the ANAO analysis of entities’ operating results in the periods 2010–11 to 2012–13 and 2011–12 to 2013–14.

Figure 4.1: Material entities by operating results category*

* Two entities classified as material but consolidated into other material entities and one entity with a limited history of financial information have been excluded from this analysis.

Source: ANAO analysis.

Reported material entities by operating results category

4.7 Significantly, and consistent with past results, the ANAO’s analysis identified that 44 material entities (approximately 65 per cent of the total) made small surpluses/profits or deficits/losses over the three year period; these entities are grouped in categories D2 or S1 (see Figure 4.1). The high percentage of entities in these categories suggests that, overall, entities have been appropriately managing their finances for the period under analysis. A tightening budget environment is likely to increase budget pressures on individual entities.

4.8 Entities that averaged a deficit/loss over the three years, and incurred at least two annual deficits/losses over that period greater than five per cent of expenses, are grouped in category D1. Seven entities (approximately ten per cent of entities analysed) were in this category. As mentioned above, there can be particular circumstances that result in an entity incurring deficits, including the influence of external factors, and a brief explanation of the reasons why these entities have incurred deficits over the period covered by the analysis is provided below:

- the NBN Group has incurred losses in its start‐up phase, as anticipated in its business plan projections;

- the High Court of Australia and the Australian Rail Track Corporation as both entities revalued downwards some of their physical assets;

- the Albury-Wodonga Development Corporation has experienced losses on the sale of assets as part of its winding up;

- the Australian Nuclear Science and Technology Organisation has not been fully funded for significant costs associated with the decommissioning of nuclear reactors;

- the Department of Agriculture experienced lower revenue due to a decline in trade volumes associated with biosecurity activities; and

- Comcare incurred higher expenses as a result of an increase in its liabilities for workers compensation, mainly due to a change in the composition of claims and claimants receiving benefits for longer periods, and also due to some changes in the methodology and economic variables used to measure these liabilities.

4.9 Seventeen entities (approximately 25 per cent of the total) incurred an average annual surplus/profit greater than five per cent of expenses. These entities are grouped in category S2. In nine cases31, these surpluses/profits arose from the commercial operations of for‐profit entities or the quasi‐commercial operations of not‐for‐profit entities.

4.10 In respect of the other eight entities32 in category S2 there were a range of reasons for the surpluses/profits, including the receipt of donated assets, a reduction in expenses resulting from efficiency measures, drawing on reserves to meet peak expenditures, and increased primary producer levy receipts due to higher production.

4.11 In 2013–14, material entities generated, in aggregate, $22.7 billion in surpluses/profits. In contrast, the operating result of the Australian Government as a whole was a deficit of $43.0 billion, as reported in paragraph 3.10. As such, the aggregate results of material entities are not the major factor contributing to the operating results of the Australian Government; changes in the level of taxation revenue and transfer payments are much more significant33.

Balance sheet analysis

4.12 While an entity’s operating result is an important aspect of its financial management, it is also important that an entity actively manages its underlying financial position, maintaining asset levels to support entity operations and ensuring that sufficient cash will be available to meet liabilities as they fall due.

4.13 Under Australian Accounting Standards, a distinction is made between those assets and liabilities that a government entity controls (departmental) and those that it administers on behalf of the Government (administered). An entity does not have full discretion over the use of administered assets, due to legislation or government policy, and is not required to settle administered liabilities from its own resources. While a large proportion of Australian Government assets and liabilities are administered34, significant levels of assets and liabilities are departmental. As at 30 June 2014, Australian Government entities held $299.3 billion in departmental assets and $163.8 billion in departmental liabilities.

4.14 Determining the appropriate level of assets and liabilities for an entity is dependent on each entity’s particular circumstances. Judgements are necessarily influenced by the responsibilities of the entity, past entity decisions on resource allocation and the funding models put in place by government35.

4.15 Consistent with past practice, the ANAO undertook an analysis of the balance sheet positions of material Australian Government entities as at 30 June 2014. While it is necessary to have regard to the public sector context, the following two aspects of entity balance sheets are important measures and are therefore focussed on in this analysis:

- Liquidity: the extent to which an entity’s liabilities are covered by cash or other financial assets. An entity where liabilities significantly exceed its financial assets may need a future injection of cash from government to meet those liabilities.

- Gearing: the extent to which an entity’s total assets are funded by debt rather than equity. An entity with high gearing may be running down its asset base and may also need a future injection from government.

4.16 The ANAO grouped material entities into the following categories:

Table 4.2: Balance sheet categories

|

Category |

Explanation |

|

B1 |

Entities where financial assets were at least 50 per cent of total liabilities and where equity was at least 25 per cent of total assets. These entities have the strongest balance sheets. |

|

B2 |

Entities where financial assets were less than 50 per cent of liabilities or where equity is less than 25 per cent of total assets. These entities had weaker balance sheets, either in liquidity or gearing terms. |

|

B3 |

Entities where financial assets were less than 50 per cent of liabilities and where equity was less than 25 per cent of total assets. These entities are the most likely to need additional funding in the future. |

Source: ANAO analysis.

4.17 Results of the ANAO analysis are shown in Figure 4.2.

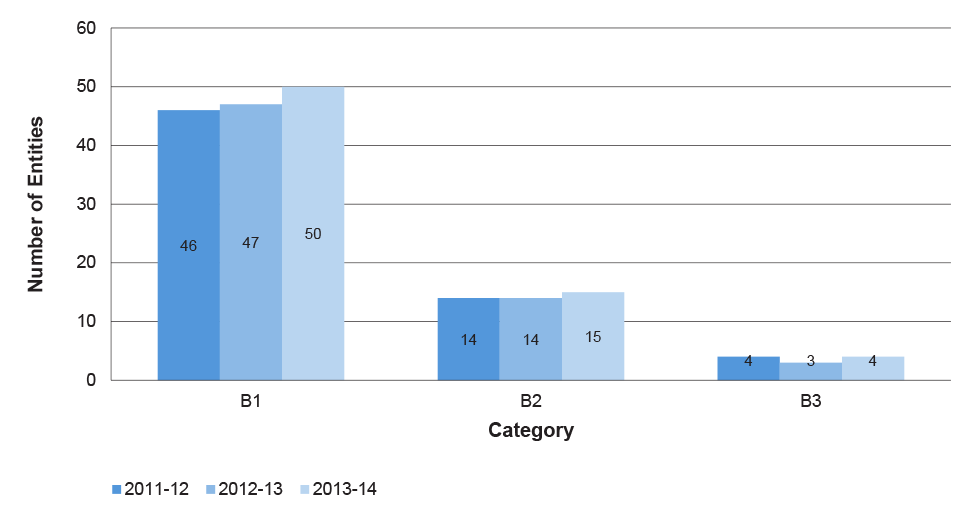

Figure 4.2: Material entities by balance sheet category*

* Two entities classified as material but consolidated into other material entities have been excluded from this analysis.

Source: ANAO analysis.

4.18 At 30 June 2014, material entities’ financial assets collectively were 163 per cent of liabilities, and equity was 59 per cent of total assets. This was broadly comparable to the situation at 30 June 2013. This suggests that the overall balance sheet position of material entities remains satisfactory.

4.19 It is also encouraging to observe that the large majority of entities continued to fall into category B1, which indicates a relatively strong balance sheet position. Fifteen entities were in category B2 and four in category B3. Similar to the position in 2011–12 and 2012–13, three of the entities in category B3 (the Australian Taxation Office, the Defence Materiel Organisation and the Australian Bureau of Statistics) are large government entities whose operations are dependent on Government policy and on continued funding by the Parliament. On this basis, and provided that appropriate attention is given to liquidity issues in the future, these entities are not at high risk of experiencing liquidity problems. Nevertheless, with a tightening fiscal outlook, it is important that entities in this category continue to monitor their financial position and improve it, where practicable. The remaining entity, the Department of the Environment had a significant unfunded liability relating to the rehabilitation of its Antarctic sites; the Government’s general policy is to provide cash to meet agency rehabilitation liabilities at the time the work is undertaken. The Department of the Environment has indicated that the Australian Government is committed to maintaining Australia’s ongoing physical presence in the Antarctic and the possible cessation of research activities and the requirement for funding to undertake the rehabilitation of its Antarctic sites is remote.

4.20 While the above analysis suggests that entities’ balance sheets are generally sound, the analysis is based on benchmarks developed by the ANAO. There would be benefit in government developing performance targets or benchmarks against which entities’ financial performance can be assessed. In addition, entities could benchmark their balance sheets over time and against like entities, as a measure of their financial management and to enhance their accountability.

Machinery of government changes

4.21 The implementation of the Machinery of Government (MoG) changes as a result of a new Administrative Arrangements Order (AAO) of 18 September 201336, following the change of government in September 2013, involved a significant change management process on the part of many entities. Successful implementation of MoG changes requires effective communication between all the parties affected by the changes, the full cooperation and commitment of both central and line agencies and sound project management arrangements to be developed and implemented in a timely manner. Where the MoG changes affect areas such as governance arrangements, appropriations, IT systems, internal controls and financial reporting, the ANAO takes these into account in developing its audit approach as part of the annual financial statement audits of Australian Government entities.

Scale of the MoG changes

4.22 The scale of the 2013 MoG changes was significant. In all, three departments were abolished, two new departments were established, one entity was integrated into an existing department, nine departments were renamed and a large number of functions and programs were transferred between departments. The most significant changes were:

- the responsibility for Indigenous Affairs policies, programs and service delivery, the Office of Women, and Office of Best Practice Regulation and Deregulation were transferred to the Department of the Prime Minister and Cabinet;

- the Department of Industry, Innovation, Climate Change, Science, Research and Tertiary Education became the Department of Industry and a number of the former department’s functions were transferred to other departments;

- the abolition of the Department of Education, Employment and Workplace Relations and the creation of the Departments of Education and Employment;

- the abolition of the Department of Regional Australia, Local Government, Arts and Sport with the functions of that department being transferred to a number of other departments; and

- the integration of Ausaid functions into the Department of Foreign Affairs and Trade.

4.23 The APSC 2013–14 annual report reported that over 13 000 staff were affected by the MoG changes with the transfer of staff between entities effected through determinations made by the Minister Assisting the Prime Minister for the Public Service under section 24(3) of the Public Service Act 199937. Appropriations totalling approximately $1 billion were transferred between entities through determinations under section 32 of the FMA Act. Other appropriation adjustments were made through Appropriation Bills at the 2013–14 Additional Estimates and Supplementary Additional Estimates.

Implementing MoG changes

4.24 Implementing MoG changes can be complex and very resource-intensive as entities need to manage a range of issues including: reaching agreement on the staff and appropriations to be transferred; establishing communication mechanisms with both ‘gaining’ and ‘losing’ staff; connecting gaining staff to existing IT networks and disconnecting departing staff from IT systems; arranging accommodation requirements for staff being transferred; and negotiating the most effective way to maintain the delivery of services in both the short and longer term, particularly arrangements for the processing of employee entitlements and program payments.

4.25 Resolution of these matters requires entities to work cooperatively and openly and to make judgements in the longer term interests of the Australian Public Service so that the delivery of government services is not put at jeopardy.

4.26 By their very nature, entities affected by such changes will often have little or no notice of the specific changes that are determined by government. This is particularly the case in circumstances where there is a change of government, as occurred on 7 September 2013.

4.27 The Implementing Machinery of Government Changes Guide (the Guide), which was jointly issued by the Australian Public Service Commission (APSC) and the Department of Finance (Finance), emphasises that:

A key to achieving good results in implementing MoG changes is for agencies to take a whole-of-government approach. The need to take a cooperative and collegiate approach underpins the whole-of-government process whereby agencies are encouraged to work across organisational barriers to achieve Government objectives. In the implementation of MoG changes this means undertaking negotiations with a view to achieving the best outcome from a whole-of-government perspective rather than the best outcome for individual agencies. It is expected that agencies will communicate openly with one another, and with central agencies, to achieve the best outcome for the APS.

4.28 While there is no overall timeframe within which entities are required to implement the MoG changes, the Guide also states that:

While the transfer of staff under section 72 of the PS Act are unlikely to be completed by the time the new AAO is made, the Prime Minister expects agency heads to implemxent AAO changes cooperatively and as soon as possible, if necessary by administrative means such as issuing new delegations.

4.29 As mentioned earlier, entities will often have little or no notice of the specific changes made by government, although in some cases, potential MoG changes can be foreshadowed by policy announcements made by political parties. This requires all entities to be agile and responsive when the details of the changes are known and to devote sufficient resources to the task of implementing the changes within agreed timeframes. Entities are also expected to implement changes in a way that has minimal impact on the efficient delivery of government policy and programs, while at the same time meeting relevant legislative and policy requirements and respecting the interests of APS staff.

4.30 In regard to the transfer of staff and appropriations, the Guide indicates that ‘the general principle of ‘staff follow function’ applies to MoG changes, as do the principles of ‘finances follow function’ and ‘records follow function’. The guide also states that:

While identification of program funding and related staff can be relatively straightforward, mapping of support functions (e.g. corporate service areas) or mapping of functions or programs that have been split can be more problematic. Agencies should recognise the need for cost sharing (e.g. sharing of fixed costs) and reach agreement that will meet the test of reasonableness.

Observations

4.31 Generally, the entities affected by MoG changes established a steering or implementation committee, supported by one or a number of working groups and identified senior staff members who were assigned responsibility for settling implementation issues. These committees included representatives of both gaining and losing entities. In some cases entities dedicated staff and applied formal project management arrangements to the implementation of the MoG changes in recognition of the scale and complexity of the changes.

4.32 Implementation of the MoG changes was assisted by the availability of the Guide referred to in paragraph 4.27 above and the preparation of a detailed Financial Management Checklist by Finance that outlined a range of issues relating to financial management that are affected by MoG changes.38

4.33 Discussions with a number of entities involved in implementing the MoG changes confirmed that there were often difficulties in reaching agreement on the staff and appropriations to be transferred in relation to corporate functions, accommodation and systems, particularly in view of the fixed costs involved. Negotiations in relation to these matters were often protracted and strained relations between entities. At times, ‘gaining’ entities sought extensive documentation from ‘losing’ entities to enable them to undertake their own due diligence; this inevitably was very resource intensive for the entities concerned and at times created a lack of trust between the staff involved in the negotiations. Entities also suggested to the ANAO that, in at least some cases, negotiations were predicated on the basis of achieving the best outcome for the entity, rather than considering the best outcome from a whole-of-government perspective. Entities suggested to the ANAO that a tightening budgetary environment had contributed to this situation and contributed to entities taking a more detailed approach to negotiations rather than adopting a more global perspective.

4.34 Nevertheless, entities advised the ANAO that their responsibilities for the delivery of government policy and programs had not been adversely affected by the MoG changes.

4.35 Discussions with Finance, the APSC and a number of affected entities identified a number of initiatives that the entities involved advised had contributed positively to the implementation of the MoG changes.

4.36 In relation to Finance and the ASPC, these initiatives included:

- the availability of a revised Implementing Machinery of Government Changes Guide;

- Finance producing a checklist for CFO’s referred to above;

- the conduct of planning discussions between Finance and entity Chief Financial Officers on issues likely to affect entities prior to the announcement of the MoG changes by the Government, and ongoing consultation during the implementation of the changes;

- Finance adopting a revised approach to the transfer of appropriations that involved the transfer of interim amounts of annual appropriations to enable the continued operation of government programs, with the settling of agreed appropriation transfers at a later date39; and

- Finance adopting a mediation role to facilitate agreement on the transfer of appropriations between entities and taking a triage approach to the resolution of issues so that priority was given to higher priority issues and tasks.

4.37 In relation to entities affected by the MoG changes, these initiatives included:

- the development of agreed principles or protocols between gaining and losing entities designed to assist in settling the transfers of appropriations;

- agreements between entities on the utilisation of systems and staff that resulted in minimal impact on business as usual functions. One of the main ways this was achieved was for the gaining entity to continue to utilise the systems of the losing entity in delivering services in the short or longer term. In some cases, this also involved staff remaining in the existing accommodation during a transition period;

- the assignment of dedicated staff to manage the transition, at least for an initial period, in recognition of the number and complexity of the issues involved;

- the preparation by some entities of ‘lessons learned’ reports that involved an analysis of the processes followed in the implementation of the MoG changes and the identification of matters that were well managed and lessons learnt.

Preparation and audit of entity financial statements

4.38 As part of the audit of the 2013–14 financial statements of Commonwealth entities, the ANAO considered the effect that any MoG changes had on the preparation of entity financial statements. In most instances, MoG changes had been settled well before entities commenced the preparation of their 2013–14 financial statements and, as a result, they had little or no effect on the financial statement preparation process. In a small number of entities, the preparation of the 2013–14 financial statements was adversely affected by delays in settling matters relating to the MoG changes. In some cases, it was not evident that entities had given sufficient attention to the early identification and resolution of matters that remained outstanding, including the accounting treatment for particular transactions and the verification of the balances of employee entitlements transferred from other entities. A general discussion on the preparation of entities’ 2013–14 financial statements is at paragraphs 5.50 to 5.60 of chapter 5 and details of audit findings in relevant entities is included in chapter 6 of this report.

Conclusion

4.39 It is encouraging to note that a number of entities have sought to identify lessons learnt from the implementation of the 2013 MoG changes. It is evident from discussions with entities that some approaches followed by entities were more successful than others, and it is important that entities continue to work together with the aim of implementing future machinery of government changes as efficiently and effectively as possible.

4.40 While recognising that more guidance and assistance has been available to entities than previously, the ANAO suggests that there is scope for central and line entities to: