Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 7 of 2014–15

Administration of Contact Centres

Published

Wednesday 26 November 2014

Portfolio

Treasury

Entity

Australian Taxation Office

Contact

Please direct enquiries relating to reports through our contact page.

Sector

Taxation

Treasury

The objective of the audit was to assess how effectively and efficiently the Australian Taxation Office managed contact centres as part of its overall service delivery.

Summary

Introduction

1. The Australian Taxation Office (ATO) is responsible for administering Australia’s taxation and superannuation systems. In 2013–14, it collected $321.7 billion in net revenue from taxpayers, incurred operating expenses of $3.6 billion and had around 23 600 employees.1 One of the ATO’s goals is to provide a contemporary and tailored service to its clients, recognising that ‘people expect convenient and accessible service in their dealings with a contemporary service organisation’.2 Providing a highly accessible service is important given the revenue raising and superannuation responsibilities of the ATO.

2. The ATO primarily engages with its clients in the following ways to meet their information needs: by telephone, including self-help automated response calls and using free call 1300 numbers from any fixed local telephone line; by correspondence; in person at ATO shopfronts; or online.3 Over recent years, almost half of the contact that clients have had with the ATO was telephone contact.4 The majority of these incoming calls to the ATO’s contact centres are via the general information line, with separate contact numbers established for specific client groupings, such as taxation practitioners or Indigenous Australians.5 In determining how to engage with clients, the ATO typically first develops the content to address their information needs for each distinct issue, and then decides how to disseminate this information through each of the four main communication channels outlined above.

3. As a major channel for clients to contact the ATO, it is important that contact centres provide a high level of client service. While they handle a range of contacts, such as correspondence, they mainly respond to telephone calls. In 2013–14, there was an increase of over 200 000 calls to around 8.2 million calls offered (that is, the number of calls made to the ATO) compared to 2012–13. Around 7.7 million calls were answered in 2013–14, compared to around 7.0 million in 2012–13.6

4. The ATO currently operates its own contact centres, as well as using three commercial providers7, to respond to calls to its general information and tax practitioner 1300 telephone numbers. The outsource providers deliver most of the ATO’s ‘surge’ capacity to handle calls during the peak tax period from July to October. The ATO centres are in eight locations, with the outsource centres in five locations—all of which are based in Australia. These 13 centres operate as a single, virtual contact centre, with incoming calls directed to the next available customer service representative (CSR) wherever they may be located.8 On the basis of call complexity, some calls cannot be resolved at the initial point of contact and may need to be escalated to other more qualified staff for a response. In 2013−14, the ATO contact centres handled 3.5 million calls (including escalated calls) while the outsource providers handled 4.5 million calls (including some calls that were subsequently escalated).9

5. The ATO’s eight contact centres and arrangements with outsource providers in the remaining five centres are managed by the ATO’s Customer Service and Solutions business and service line (BSL). A number of other BSLs also provide telephony services to the public, including the Client Account Services, Debt, Superannuation, and Private Groups and High Wealth Individuals BSLs. The ATO refers to these as ‘boutique’ contact centres. The calls handled by these centres are more specialised or are in response to letters sent to clients by these BSLs. These BSLs may also make outbound calls in relation to campaigns that they are conducting.

Audit objective, criteria and scope

6. The objective of the audit was to assess how effectively and efficiently the ATO managed contact centres as part of its overall service delivery strategy. To form an opinion against the audit objective, the ANAO adopted the following high-level criteria:

- contact centres are effectively integrated with other ATO client communication channels, such as the online and on-site channels;

- contact centres are supported by effective business and administrative arrangements;

- contact centres provide a high level of client service; and

- contact centres are managed efficiently.

7. The audit principally focused on the ATO’s handling of incoming telephone calls by contact centres.

Overall conclusion

8. The provision of high quality and accessible services to clients underpins the ATO’s promotion of compliance with Australia’s extensive systems of taxation and superannuation. A key component of the ATO’s approach to engaging with clients is its network of 13 contact centres that, in 2013–14, handled 10 million inbound telephone calls10—representing almost half of its 20.7 million client contacts in that year.11 While the ATO is aiming to make online contact with clients the preferred communication channel by 2020, contact centres are likely to remain an important channel for large numbers of clients in the absence of any action to reduce the demand for these services.

9. Contact centres are a major communication channel for clients to contact the ATO and have generally been managed effectively. Overall, the arrangements established for telephone contact provide clients with ready access to a broad range of call services, with the handling of inbound calls resulting in relatively high levels of overall client satisfaction over many years.12 The ATO has generally sound organisational arrangements to manage calls, although an overarching client communication channel strategy is yet to be established. While not being in a position to readily demonstrate the efficiency of its contact centre operations, there is evidence to indicate that the ATO has achieved value for money from the use of outsource providers and it has also maintained a strong focus on monitoring and reducing the costs of its own contact centres.

10. Until 2012, the ATO had a distinct client communication strategy in place covering the four key channels—contact centres, correspondence, online and shopfronts. This strategy has not been updated or replaced since reaching its nominal expiry date in 2012. While a draft digital strategy was prepared in July 2014 for online services, this strategy focuses on the ATO’s digital presence and does not provide or reference a detailed plan for the provision of high quality and accessible services through other channels, including call services. Accordingly, there would be merit in the ATO developing a strategy that more fully encompasses all service channels and provides a plan for transitioning to the preferred online channel environment. As the management of the four service channels is assigned to a number of groups and BSLs across the organisation, there is also scope for the ATO to adopt organisational arrangements that better support the coordinated delivery of client engagement services across the channels.

11. To efficiently handle call volumes and effectively address the needs of clients, the ATO directs calls to staff with relevant skills and knowledge. In general, calls of a specialised nature are handled by ATO contact centres, with the more straightforward calls increasingly being directed to outsource providers. Outsourcing has been particularly effective in enabling the ATO to manage significant fluctuations in call workloads, particularly during ‘Tax Time’ from July to October each year. The ATO has also made effective use of technology, including in managing periods of high call volumes, such as providing opportunities for callers to receive a call back when their call reaches the front of the queue.

12. As well as relatively high levels of overall satisfaction with contact centres, client satisfaction surveys indicate reasonably high levels of satisfaction across most of the major elements of service, including the time taken to resolve a query (84 per cent in 2013–14) and the overall quality of information provided (86 per cent in 2013). The main exception has been a reasonably significant level of dissatisfaction with call waiting times, with only 57 per cent of respondents satisfied with the length of waiting times in 2013–14.13 At present, the ATO’s call answering service commitment for its general information line only relates to Tax Time. Using service commitments that measure the extent to which the ATO meets call wait times throughout the year would better enable it to manage call wait times and enhance client satisfaction.

13. In recent years, the ATO has taken a number of steps to improve the efficiency of its contact centre operations. These steps have included changes to the skill levels of contact centre staff and better support for CSRs to improve first contact resolution rates (that is, the percentage of calls resolved by the CSR who first answers the call), with the ATO reporting a first response resolution rate of around 80 per cent over the past two years. These results need to be viewed with some caution, however, as not all calls included in the rate have been satisfactorily resolved. For example, calls that cannot be answered because a caller is unable to establish proof of identify are treated as being resolved when, from the client’s perspective, the matter has not been resolved as they need to call again. As well as improving its measurement of first contact resolution rates, there is scope for the ATO to implement a consistent methodology for calculating call handling costs.14

14. To improve the ATO’s management of contact centre operations, the ANAO has made two recommendations aimed at better coordinating the management of the four key client communication channels, including contact centres, and improving reporting of contact centre performance.

Key findings by chapter

Role of Contact Centres in Australian Taxation Office Service Delivery (Chapter 2)

15. Contact centres are an integral part of the ATO’s service delivery strategy. They mainly handle incoming calls from individual taxpayers, superannuants and tax agents. As indicated in paragraph 3, the volume of incoming calls handled by the ATO contact centres continues to increase, similar to the experience of other large organisations.15 Despite this increase in call demand, the ATO’s aim is for online—rather than contact centres—to be its preferred channel to interact with clients.

16. In this light, the ATO has introduced a number of initiatives to increase the take-up of online services and so moderate the growth in the volume of incoming telephone calls. These initiatives include:

- increasing the number of transactions that a client can complete online;

- requiring tax agents to undertake transactions online, rather than over the telephone with the assistance of a contact centre CSR, where this option is available; and

- encouraging clients to register for an ATO online account through the myGov online portal that is managed by the Department of Human Services, where they can obtain information on their dealings with the ATO, such as progress in the processing of their annual income tax return or perform a number of transactions, such as advising of a change of address.

17. The ATO is also taking steps to reduce the need for clients to contact the ATO. These include helping clients more easily meet their taxation reporting obligations16 and the use of so-called ‘natural systems’, that is, systems such as financial accounting software that businesses use to meet many of their taxation obligations.

18. While the ATO is developing a digital service delivery strategy, this strategy does not include a detailed plan outlining how the ATO will meet its objective of increasing the take-up of online services and integrate services efficiently and effectively across all channels—not just digital services. It is important that the ATO’s channel strategy outlines further improvements to the performance of call services, particularly given the likely continued importance of this communication channel for the foreseeable future.

19. As the management of service delivery channels is currently assigned to a number of groups and BSLs across the ATO, no single BSL is responsible for ensuring that the delivery of service is seamless and consistent and for managing an overall ATO channel strategy. While the ATO has commenced consolidation of some service delivery functions17, there would be benefit in exploring options to better coordinate the delivery of services.

20. As the entry-point to online services, the ATO’s website needs to help facilitate the take-up of online services and, as the ATO’s future preferred service delivery channel, be managed as a key part of the ATO’s service delivery arrangements. While some improvements were made to the website in 2013, further opportunities exist to assist clients to more easily locate the information that they are seeking, for example, providing stepped-through guidance in obtaining answers to questions, without having to call the ATO for assistance.

Operation of Australian Taxation Office Contact Centres (Chapter 3)

21. A key challenge for most contact centres is the appropriate streaming of calls—that is directing the caller to a CSR that is best qualified to respond to the caller’s issue. The ATO has sound processes in place for directing calls based on the caller’s selection from a menu of options about the nature of the matter for which they are seeking assistance. In the medium term, there is greater scope for the ATO to use voice recognition technology to more quickly and accurately direct calls within the organisation.

22. To enable calls to be directed to CSRs with the requisite level of capability, the ATO operates a tiered skilling model. As part of this model, subject areas are grouped into three tiers based on the level of complexity of the subject, with staff allocated to a tier based on their capability. A review of ATO contact centres in 2012 by an external consultant found that this model was more effective than a call handling model based on individual taxation or superannuation subject matter levels.

23. Depending on subject matter expertise, tier classification and other considerations, CSRs are grouped into specific call handling teams within a contact centre. These teams typically have between 15 and 17 CSRs, including team leaders, which is slightly higher than industry standards.18 The number of teams within a centre varies, depending on workloads at different times of the year and other factors, such as skill levels within the ATO. Some of the ATO centres are relatively small and, while there is scope to consolidate centres, some centres already have a single manager and shared support staff, which reduces the extent of potential savings.

24. The ATO has taken a number of measures to help contact centre staff respond to calls, including a scripting and referencing system called the Script Manager and Reference Tool (SMART). This system, which the outsource providers have indicated provides appropriate support to contact centre staff, gives a step-by-step guide to answering queries from clients. The ATO also monitors calls in real-time and can take timely remedial action to respond to unexpected increases in call demand, such as blocking calls if the wait times are excessive.

25. The ATO’s approach to forecasting call demand is in line with industry practice, with long-term forecasts initially prepared and subsequently refined and used to determine staff scheduling requirements. While the ATO’s call demand forecasting is relatively accurate, the accuracy is less for escalated calls. As noted earlier, in 2014 the ATO consolidated client forecasting capability for all contact types (calls, online, in-person and in writing) in the Customer Service and Solutions BSL to achieve greater consistency in forecasting and to generate efficiencies.

26. To support and oversee the operation of the outsource providers, the ATO has appointed support staff, set call volume answering and service output targets, incorporated financial performance incentives and regularly reviews provider performance. Service credits (deductions against the next monthly invoice) are imposed where a provider fails to meet service targets and a contract can be terminated where a provider consistently fails to meet specified ‘critical’ service levels.19

27. The ATO has implemented sound arrangements to monitor and review the quality of call handling in the 13 main contact centres. However, the number of calls reviewed each month (around three calls per CSR per month)20 is much less than for industry generally21 and of other agencies examined by the ANAO. The extent of these differences suggests that there may be scope for the ATO to increase the number of calls reviewed for each CSR each month, bearing in mind the likely benefits to the quality of call handling and the cost of undertaking the additional reviews. There is also scope to include escalated calls to the ‘boutique’ centres in the contact centre review arrangements to provide greater assurance regarding the quality of call handling across ATO operations.

Performance of Australian Taxation Office Contact Centres (Chapter 4)

28. The ATO commissions research organisations to conduct a number of client surveys each year that provide information on ATO contact centre performance against the ATO’s service commitments, including monthly contact centre satisfaction surveys. The surveys indicate that, in 2012–13, between 80 and 90 per cent of respondents were satisfied with the helpfulness of ATO staff, and around 75 per cent of respondents were satisfied with the level of accuracy of the information provided. Over 70 per cent of respondents were satisfied with how the ATO kept clients informed and with the professionalism of ATO staff.

29. Arrangements implemented by the ATO to meet the needs of the diverse range of clients who seek assistance from the organisation on a daytoday basis include encouraging clients from non-English speaking backgrounds to use the Translating and Interpreting Service (operated by the Department of Immigration and Border Protection) and a dedicated helpline for Indigenous clients—primarily targeted towards those clients from remote areas. The annual cost to the ATO of providing translation services to its clients is around $2.5 million. In 2013–14, there were 61 261 calls requiring language assistance, which equates to around $41 per call. There were also 24 359 calls answered by the Indigenous helpline in 2013–14. The community organisations consulted by ANAO considered that the arrangements established by the ATO generally work well, but that there was scope for some improvement.22

30. The ATO does not have a consistent methodology for calculating the cost of its main contact centres and does not calculate the cost of calls handled by its ‘boutique’ centres. To help identify opportunities to further improve the efficient operation of contact centres, there would be merit in the ATO developing a consistent approach for calculating call handling costs across all of its contact centres. However, using information provided by the ATO, the combined average costs per call handled by the eight contact centres managed by the Customer Service and Solutions BSL (including the cost of the Translating and Interpreting Service and direct frontline support costs) were calculated as $23.50 in 2012–13 and $22.35 in 2013–14. The cost per second of calls handled by the ATO contact centres was higher than the cost of calls handled by the outsourced providers (around three cents a second, compared to around two cents a second for the outsourced providers in 2013–14).23 However, part of this difference is explained by the higher seniority of ATO staff required to handle the more complex calls taken or supported by the ATO contact centres and other factors, such as the outsource centres’ higher rate of escalation or transfer of calls to more qualified staff for resolution than ATO centres (21 per cent for the outsource centres compared to 12 per cent for the ATO centres in 2013–14).

31. To improve efficiency and client satisfaction, the ATO has implemented arrangements to increase first contact resolution of calls. The setting of first contact resolution improvement targets would provide insights into the effectiveness of these arrangements. Using the ATO’s current methodology for calculating first contact resolution rates, first contact resolution for its 13 main contact centres increased from 77 per cent in 2012–13 to 79 per cent in 2013–14.24 Outsourcing the handling of around 58 per cent of calls has also helped the ATO to manage varying call workloads, such as for Tax Time, and represents an effective use of resources whereby the outsourced centres handle the less complex calls and the ATO centres handle most of the more complex calls. Retaining a significant in-house capacity mitigates the risk to the ATO of outsourcing and provides scope to increase this capacity, if needed.

32. In terms of non-financial measures of performance, the ATO has two service commitments related to the timely provision of telephone services, reflecting the level of service that the ATO considers it can provide having regard to available resources. These are to:

- answer 80 per cent of general telephone enquiries from taxpayers within five minutes during the peak July to October Tax Time period; and

- answer 90 per cent of telephone enquiries from tax practitioners within two minutes.

33. The restriction of the first of these commitments to Tax Time was introduced in 2013–14. As a result, the ATO does not measure its performance in relation to responding to general telephone enquiries from taxpayers outside of Tax Time. In contrast, the 10 other organisations examined by the ANAO had measures that applied throughout the year and typically the measures provide for the majority of calls to be answered within two to three minutes. The ATO almost met the general commitment (79 per cent) in 2013−14 and met the 90 per cent target for tax practitioner enquiries.

34. While it is pragmatic to set service commitments having regard to available resources, client surveys and complaints data revealed significant dissatisfaction, despite the ATO meeting, or almost meeting, its service commitments. For this reason and to promote better practice, there would be merit in the ATO developing performance standards that reflect reasonable call wait times for its business and benchmarking its performance in answering calls in a timely manner against measures used by comparable organisations.

Summary of agency response

35. The ATO’s summary response to the proposed report is provided below, while the full response is provided at Appendix 1.

The ATO welcomes this audit and considers the report supportive of our overall approach to managing contact centres.

The audit acknowledges the progress made and strategies underway to achieve channel shift in line with whole-of-government policy.

The audit communicates a view that all client interactions should be managed by the same area within the ATO to ensure consistent service provision and we agree that this comment should be further explored.

While finding the ATO’s approach to managing contact centres to be generally effective, the ATO acknowledges that the audit identifies a number of opportunities for improvement in our operations.

Recommendations

|

Recommendation No. 1 Para 2.27 |

To help deliver seamless, consistent and efficient services across all communication channels and to increase the take-up of online services, the ANAO recommends that the ATO: develops an overarching cross-channel strategy that details how the ATO plans to transition to an improved online service environment, while also continuing to provide and improve the performance of other service channels; adopts organisational arrangements that better support the coordinated delivery of services; and further develops its website to better support the delivery of online services. ATO response: Agreed. |

|

Recommendation No. 2 Para 4.47 |

To help identify opportunities for further efficiency improvements in the operation of contact centres, the ANAO recommends that the ATO develops a consistent approach for calculating call handling costs, including the cost of telephony handling by its ‘boutique’ contact centres. ATO response: Agreed. |

1. Introduction

This chapter provides background information on the Australian Taxation Office and the operation of its contact centres, and also outlines the audit approach and structure of the report.

Background and context

1.1 The Australian Taxation Office (ATO) is responsible for administering Australia’s taxation and superannuation systems. It seeks to build confidence in its administration by helping people understand their rights and obligations, improving ease of compliance and access to benefits, and managing non-compliance with the law. In 2013–14, the ATO collected $321.7 billion in net revenue from taxpayers, incurred operating expenses of $3.6 billion, and had around 23 600 employees.25

1.2 The ATO’s mission is to ‘contribute to the economic and social wellbeing of Australians by fostering willing participation in our tax and superannuation systems’.26 One of the ways that the ATO seeks to do this and to also help clients obtain the information they need is by endeavouring to provide a ‘convenient and accessible’ service to its clients in line with the community’s expectations of a contemporary service organisation.27

1.3 The ATO engages with its clients in a number of ways, as summarised in Table 1.1. It also uses the print and digital media to inform the community about taxation changes and how to communicate with the agency, as well as calling and writing to clients about their taxation and superannuation affairs. In determining how to engage with clients, the ATO typically first develops the content to address their information needs for each distinct issue, and then decides how to disseminate this information through each of the four main communication channels.

Table 1.1: ATO inbound service dealings with clients (2012–13 and 2013–14)

|

Channel |

Details |

Number |

Percentage of total contacts in 2013–14 |

|

On call (telephone) |

Over the telephone, through free ‘local call’ 1300 numbers to access ATO products and services from anywhere in Australia. |

Around 7.7 million inbound telephone calls answered in 2013–14, an increase of around 700 000 calls from the 7 million calls answered in 2012‒13. |

39% |

|

Interactive voice recognition selfhelp calls. |

Around 2.3 million self-help automated response calls, compared to 2.6 million calls in 2012−13. |

7% |

|

|

In writing |

Direct correspondence by letter and fax. |

Around 6 million inbound correspondence in 2013–14, compared to around 5.8 million in 2012–13. |

30% |

|

Online |

Online services allow members of the public to access information and a range of services from an agency’s website. ATO clients can update their details, examine the progress of income tax returns and, using SuperSeeker, review their superannuation accounts and, among other things, find lost super. |

Around 4.5 million uses of online services in 2013–14, compared to over 3.2 million uses in 2012–13. |

22% |

|

On-site |

In person at ATO shopfronts around Australia. |

Around 403 000 shopfront visits in 2013–14, compared to around 439 000 visits in 2012–13. |

2% |

Source: ATO.

Note: Table 1.2, later in this section, provides additional information on the number of calls offered, answered, abandoned and blocked.

1.4 Around 46 per cent of all inbound client contacts delivered through ATO service channels in 2013‒14 were through ATO contact centres—accessed over the telephone, through seven dedicated information lines28, the ATO switchboard, a 24 hour self-help automated response line or a number of other dedicated telephone lines for issues such as the lodgement of complaints.29

1.5 The ATO is increasingly seeking to provide an integrated customer service framework that facilitates the use of online and automated self-help services, where possible, and provides access to ATO officers when needed. It encourages taxpayers and other clients to make use of its online services, such as for lodgement of income tax and goods and services tax returns. The Taxpayers’ Charter sets out the manner in which the ATO will conduct itself when dealing with taxpayers, including offering taxpayers a professional service and assistance.30

ATO contact centres

1.6 Contact centres are an essential part of the service delivery frameworks of all large organisations. While such organisations have a number of channels through which their customers can access their services, including increasingly through online access to services, the telephone remains a major channel for client contact with government service agencies. As shown in Table 1.1, in 2013‒14, 39 per cent of client contact with the ATO was from inbound phone calls and seven per cent was from self-help automated response calls.

1.7 Contact centres handle a range of contacts, such as correspondence, but mainly respond to telephone calls. Contact centres and inbound telephony services are managed by the Customer Service and Solutions (CS&S) business and service line (BSL). However, a number of other BSLs also provide telephony services to the public, including the Client Account Services, Debt, Superannuation, and Private Groups and High Wealth Individuals BSLs. The calls handled by these ‘boutique’ centres are more specialised or are in response to letters sent to clients by these BSLs. These BSLs may also undertake outbound calls in relation to campaigns that they are running.

1.8 The ATO currently uses staff in its own contact centres, as well as three commercial providers—Serco Australia Pty Ltd, Stellar Asia Pacific Pty Ltd and Datacom Connect Pty Ltd—to respond to calls to its general information and tax practitioner 1300 numbers. The ATO centres are in eight locations and the outsource centres are in five locations.31

1.9 The outsource providers supply most of the ATO ‘surge’ capacity to handle calls during the peak tax period—‘Tax Time’—from July to October. In Tax Time 2013, the ATO’s CS&S managed contact centres handled 42 per cent of calls and the outsource providers handled the remaining 58 per cent of calls.32

Call volumes

1.10 Additional information on the number of inbound calls to the ATO over the three years from 2011–12 to 2013–14 is provided at Table 1.2. There was an increase of around four per cent (over 200 000) in the number of calls offered33 in 2013–14, after being relatively stable at around eight million calls a year in the previous two years. The number of calls answered in 2013–14 was higher than in the previous two years, with the number of blocked calls increasing considerably in 2013–14 compared to the previous year, reflecting an ATO business decision to block calls rather than have callers wait for an extended period.34

Table 1.2: Inbound calls to the ATO (2011–12 to 2013–14)

|

Inbound calls |

2011–12 |

2012–13 |

2013–14 |

|

Calls offered |

7 972 274 |

7 891 523 |

8 228 506 |

|

Calls answered |

7 025 944 |

6 968 951 |

7 651 782 |

|

Calls abandoned |

946 330 |

922 572 |

576 724 |

|

Calls blocked |

289 977 |

356 920 |

623 881 |

|

Percentage of calls offered that were abandoned |

11.9% |

11.7% |

7.0% |

|

Calls blocked as a percentage of total calls (offered and blocked) |

3.5% |

4.3% |

7.0% |

Source: ATO.

Notes:

The figures for 2011–12 and 2012–13 are not the same as those shown in the ATO’s annual report for those years because the annual report figures included calls that were escalated to other ATO officers as separate calls. From 1 July 2013, the ATO adopted full industry service methodology for call metrics, which does not treat such calls as separate calls.

The figures in this table are for the ATO as a whole. The figures for 2013–14 exclude incoming calls from the Telephone Interpreter Service from November 2013 to June 2014, calls from ATO shopfronts and other calls to the ATO (356 957 calls offered, 325 845 calls answered and 31 112 calls abandoned), which are included as incoming calls in the ATO’s 2013−14 annual report. This is to provide consistency with figures for 2011–12 and 2012–13, which did not count these calls as incoming calls.

The numbers of calls answered by the mainstream contact centres operated by the 13 CS&S contact centres, as distinct from the ATO as a whole, were 6 052 588 in 2011–12, 5 692 137 in 2012–13 and 6 234 794 in 2013–14. For consistency with earlier year figures, the 2013–14 figures again exclude 325 845 calls from the Telephone Interpreter Service from November 2013 to June 2014, calls from ATO shopfronts and calls to the ATO switchboard.

1.11 The larger percentage of calls that were blocked and an increase in the number of calls answered in 2013–14 has contributed to a significant reduction in the number of abandoned calls in that year.

1.12 To help manage call waiting times for ATO clients when call volumes are high and reduce the number of abandoned calls, the ATO established an automatic call-back facility to all contact centre sites in June 2008. This facility allows callers to leave their name and contact number and hang up instead of remaining in the queue. Callers maintain their position in the queue and receive a call back when a customer service representative (CSR) becomes available. If the client answers the call, he or she will be provided with the option to accept the call and, upon acceptance, will be transferred to a CSR. The ATO also offers the caller the option of a callback at a later time. The caller then receives a system generated phone call at the caller’s selected time.

Service types

1.13 There are a number of ways that a person can call the ATO to obtain information about tax and superannuation matters, including general information lines, self-help services and information services targeted at certain demographics. The ATO also provides a complaints hotline.

Information lines

1.14 Calls to the information lines may be handled and finalised by CSRs or, if they cannot be handled by these staff, by staff in the relevant BSLs or the outsource centres. Although contact centre staff are in 13 different locations, the 13 centres are operated as a single, virtual contact centre, with calls being directed to the next available CSR, wherever they are located.

24 hour self-help service

1.15 The self-help automated response telephony service is available to taxpayers 24 hours a day and seven days a week. There are separate support lines for businesses and individuals. These services allow taxpayers to complete a variety of tasks, including: checking their income tax return; lodging tax refund claims or short tax returns; ordering forms or publications; and setting up payment arrangements. Most self-help services use a speech recognition system to help guide callers to the information they are seeking.

Services for diverse populations

1.16 The ATO uses the Translating and Interpreting Service, operated by the Department of Immigration and Border Protection, to assist non-English speakers and provide them with the option to speak to an ATO officer in their preferred language. The service also provides guidance and advice for new migrants who may have a limited understanding of the Australian taxation system. A specialist telephone helpline for Indigenous Australians covering a wide range of income tax matters is also provided.

1.17 Taxpayers who are deaf, hearing impaired or have speech impediments can access a national relay service, which allows taxpayers to type and read an entire conversation via a TTY (teletypewriter) or internet relay.

Complaints hotline

1.18 Where callers have a complaint about the ATO, they can call the ATO complaints hotline. These calls are answered by specially trained staff in the contact centres and, if they cannot be resolved at that point, are referred to specialist complaints handling staff in the relevant areas of the ATO.

International perspective

1.19 In relation to the performance of revenue (taxation) agencies’ call services in other countries, two recent audits that have examined aspects of contact centre performance.

United States

1.20 In December 2013, the United States Government Accountability Office (GAO) released an audit report reviewing the performance of the Internal Revenue Service (IRS) in processing tax returns in the 2013 tax filing season and its ability to provide efficient and effective services to taxpayers. The tax filing season is when the IRS processes most tax returns through services that include telephone, correspondence and website assistance for tens of millions of taxpayers. The GAO found that, although the IRS was able to process more tax returns electronically and had expanded its website services, it was unable to cope with the demand for telephone and other correspondence services. The percentage of callers who received assistance was 76 per cent in 2010, and this dropped to 68 per cent in 2013. The average time taxpayers waited for their calls to be answered had progressively increased from 8.6 minutes in 2008 to 15.5 minutes in 2013.

1.21 The GAO recommended that the IRS develop a strategy that re-defines the telephone and correspondence services that are required, based on an assessment of demand and resources. The GAO also recommended that the IRS take steps to better balance demand for services with available resources.

United Kingdom

1.22 In December 2012, the National Audit Office (NAO) in the United Kingdom reviewed whether Her Majesty’s Revenue and Customs (HMRC) was able to achieve value for money in its customer service and support for taxpayers. It specifically focused on the HMRC’s performance in handling telephone calls. HMRC’s customers include individuals, businesses, tax agents, charities and benefits claimants. Most customers contact HMRC by phone, with many also using the HMRC’s website to locate information or to file tax returns.

1.23 In 2011–12, HMRC received 79 million calls from taxpayers and, of these, 74 per cent were answered, while in 2010–11 HMRC received 122 million telephone calls of which 48 per cent were answered. Despite this improvement, the NAO found that call waiting times could be significantly reduced. The average call waiting time had increased from 107 seconds in 2009‒10 to 282 seconds in 2011‒12. The NAO recommended that the HMRC set a target for the percentage of calls answered within a specified time and consider setting targets to monitor: the quality of advice for complex queries; performance in resolving queries at first contact; website functionality; and face-to-face contact.

Previous audits and reviews

Previous audits

1.24 The ANAO conducted a performance audit of the then Department of Social Security’s teleservice centres operations in 1995‒96 (Audit Report No. 9 1995‒96 Teleservice Centres). It then released a guide and accompanying handbook on the operation of contact centres in December 1996, which was informed by the earlier audit.35

1.25 An ANAO audit of ATO shopfronts in 2010‒11 (Audit Report No. 50 2010‒11, Administration of Tax Office Shopfronts) found, among other things, that, shopfronts provided a range of services to the public that were being delivered effectively. The audit did, however, note a high level of unanswered calls to the Indigenous hotline.

Previous reviews

1.26 In November 2012, the Joint Committee of Public Accounts and Audit, in its report on its annual hearing with the Commissioner of Taxation in September 201236, noted the ATO’s response to anecdotal evidence from the general public and constituents of slow response times when interacting with government agencies via the telephone.

1.27 The Commonwealth and Taxation Ombudsman, in his annual report for 2012‒13, also reported on some matters affecting contact centres, including the quality of information provided to ATO clients by contact centre staff. For example, some taxpayers who received larger than expected income tax refunds as a result of a systems error contacted the ATO and contact centre staff incorrectly advised that the refunds were accurate. The Ombudsman reported that clients should be able to rely on information provided by contact centre staff.37

Audit objective, criteria, scope and methodology

Audit objective and criteria

1.28 The objective of the audit was to assess how effectively and efficiently the ATO managed contact centres as part of its overall service delivery strategy.

1.29 To form an opinion against the audit objective, the ANAO adopted the following high-level criteria:

- contact centres are effectively integrated with other ATO service channels, such as the online and on-site channels;

- contact centres are supported by effective business and administrative arrangements;

- contact centres provide a high level of client service; and

- contact centres are managed efficiently.

Audit methodology

1.30 During the course of the audit, the audit team visited a number of the ATO’s contact centres, including outsource centres. As part of benchmarking the ATO’s services with those of other organisations, the audit team also met or spoke with representatives from a number of centres operated by other government agencies and the private sector.38

1.31 The audit team also:

- examined policy documents, guidelines, procedures and operational documents;

- interviewed staff in the contact centres and in relevant offices in the ATO;

- analysed operational data on contact centres, including the cost of the centres and average call handling costs;

- listened to calls or recordings of calls to determine how well they were handled;

- met with commercial organisations operating four ATO outsource centres39; and

- consulted with key external stakeholders to discuss issues relating to the ATO’s management of its contact centres.

1.32 The audit had regard to the industry standards for contact centres issued by the Australian Teleservices Association. These standards have five categories of criteria, which are broken down into 41 sub-categories to define the processes, policies and procedures that need to be in place to allow a contact centre to achieve its goals. The five high-level categories are: planning; infrastructure and environment; people; process; and achievement and performance.

1.33 The audit was conducted in accordance with the ANAO audit standards at a cost of approximately $312 000.

Report structure

1.34 The structure of the report is outlined in Table 1.3:

Table 1.3: Structure of the report

|

Chapter |

Overview |

|

|

2. |

Role of Contact Centres in Australian Taxation Office Service Delivery |

Examines the role of contact centres in the ATO’s service delivery approach and their integration with other service channels. |

|

3. |

Operation of Australian Taxation Office Contact Centres |

Examines the operation of the ATO’s contact centres, including the extent to which they are supported by business and administrative arrangements. |

|

4. |

Performance of Australian Taxation Office Contact Centres |

Examines the level of service provided by, and the efficiency of, ATO contact centres. |

Source: ANAO.

2. Role of Contact Centres in Australian Taxation Office Service Delivery

This chapter examines the role of contact centres in the ATO’s service delivery approach and their integration with other service channels.

Introduction

2.1 One of the goals of the ATO is to provide a ‘contemporary and tailored service’ to its clients, recognising that ‘people expect convenient and accessible service in their dealings with a contemporary service organisation’.40 Providing a highly accessible service is important, given the ATO’s revenue raising and superannuation responsibilities. In those cases where clients cannot readily obtain information about their taxation obligations, there is a risk that they will fail to comply with their obligations and taxation revenues will be less than they should be.

2.2 A guide released in 2006 by the Australian Government Information Management Office (AGIMO) in the Department of Finance, emphasised the importance of agencies having a strategy in place to manage service delivery to their clients through the most appropriate channel. The guide noted that the benefits of a channel strategy include:

- the alignment of customer needs, services, channels and agency priorities;

- improved cost efficiency of service delivery across multiple channels;

- seamless, integrated and consistent delivery of services across channels; and

- informed and prudent future channel investments.41

2.3 The ANAO examined the ATO’s service channel strategy and the role played by contact centres in reducing the need for clients to contact the ATO, as well as the ATO’s management of service delivery.

Service channel strategy

2.4 The ATO interacts with its clients through a number of channels, with these channels and their relative importance summarised earlier in Table 1.1 (in Chapter 1). As indicated in Table 1.1, calls to the ATO accounted for almost half of client interactions with the ATO in 2013–14.

2.5 The ATO has stated that its aim is for online to be the preferred channel to interact with clients and, when escalation or direct contact is necessary, it will offer different kinds of personalised services (for example call-backs, webchat where a website user can ask a question and receive an answer, personal appointments or case conferencing).42 The ATO is developing a digital service delivery strategy. However, unlike the previous channel strategy that reached its nominal expiry date in 2012, the digital strategy does not meaningfully cover all channels. Nor does it provide, or link to, a detailed plan about how the ATO will meet its objective of making online services the preferred channel, or how to integrate services efficiently and effectively across all channels. An overarching channel strategy would assist the ATO to articulate how it intends to transition to an improved online service environment, while also continuing to provide and improve the performance of all service channels.

2.6 While online services are likely to continue to grow, on-call (telephone) services provided by contact centres are likely to remain the preferred method of interacting with the ATO for a large proportion of clients for the foreseeable future, unless the ATO takes other action to reduce the demand for call services. This is reinforced by:

- an AGIMO survey of e-government services (which it defined as services provided through the Internet and by telephone), which reported that, while the use of e-government services had remained stable between 2008 and 2011, with around two-thirds (65 per cent) of respondents using e-government services in 2011, the use of the telephone had also increased from 30 per cent to 38 per cent between 2009 and 201143; and

- ATO data shows that, while the take-up of online services is increasing, so are the numbers of calls to the ATO. The overall number of inbound telephone calls to the ATO increased from around 8.0 million in 2011−12 and 2012–13 to around 8.2 million in 2013–14 (see Table 1.2).44

2.7 To substantially improve the take-up of online services and so reduce the strong reliance on contact centres, the ATO will need to make it easier for its clients to use online services. In this context, the ATO’s draft Digital Strategy indicates that:

It is expected that direct contact will only be required in exceptional circumstances …

Unnecessary phone interactions for simple routine enquiries will be eliminated or replaced with online options, freeing up our telephony staff to deal with more complex enquiries …

Direct telephony support will be provided for priority services at times that meet client demand (e.g. evening and weekend access for individuals during Tax Time).45

2.8 The ATO has started to advise tax practitioners that they will need to undertake some activities (such as change of address), where they are able to do so, through the online tax agents’ portal. This approach recognises that, while the ATO aims to provide a high level of service for tax practitioners, it is increasingly difficult to absorb the associated cost in a constrained resource environment.46 This approach also recognises that some tax practitioners require more than simple encouragement to change the way that they have operated in the past. One way of increasing the take-up of online services is to limit the level of on-call assistance to those enquiries or transactions that can be completed online. The ATO is also working with the Department of the Treasury to seek government support for legislative change that will allow the Commissioner to direct the use of digital channels, although any such changes would need to be managed carefully.

2.9 An effective channel strategy is one that helps ATO clients readily meet their taxation and superannuation obligations. For some clients, contacting the ATO by telephone will be the most effective option. Clients who use the ATO’s online services may also wish to call the ATO to clarify information. While continuing to take steps to increase the take-up of online services, it is important that the ATO continues to provide a high level of customer service through its contact centres, and this needs to be recognised in an overarching ATO channel strategy.

Improving online services

2.10 Increasing the take-up of online services and thereby reducing the demand for call services requires a comprehensive set of measures to make it easier for clients to complete their transactions or obtain the information they are seeking online.

2.11 The ATO’s website is often the first place that people will visit to obtain information about taxation or superannuation requirements. As the entrypoint to online services, it needs to be organised in such a way that it helps facilitate the take-up of online services and be managed as part of the ATO’s service delivery arrangements. However, based on monthly surveys of clients who have called the ATO, 44 per cent of clients who called between July 2013 and March 2014 indicated that they had accessed the ATO website before calling. This suggests that the number of calls is likely to have been less had these callers been able to obtain the information they needed online.

2.12 While major changes were made to the website in 2013, there is scope to further improve the accessibility of information on the website. Opportunities for improving the ATO’s website include:

- making it easier to locate answers to questions (for example, by providing a tool similar to that used by CSRs to help them respond to client enquiries (see paragraphs 3.26 and 3.27 in Chapter 3) to enable clients to ‘drill down’ through a series of menus to obtain answers to their questions;

- stating requirements in plain English and giving examples; and

- providing online support (for example, web-chat services).

2.13 In 2013, the ATO increased the number of transactions that could be completed online. In addition to obtaining information on the progress of returns, clients can now update their details online, make payment arrangements, display their memberships of superannuation funds and transfer money between superannuation funds. The ATO has also taken some steps to make it easier for clients to use online services. For instance, in May 2014, the ATO integrated its online services with myGov, which is an online portal managed by the Department of Human Services that provides online access to a growing range of government services.47 To encourage greater take-up of ATO myGov accounts, the portal is being promoted by contact centre staff and is a requirement for some services, such as online lodgement of income tax returns.48 Users of the ATO’s myGov account can obtain information on a number of matters, such as progress in the processing of their annual income tax return, or perform a number of transactions, such as a change of address.

2.14 From 2015, the ATO also plans to use the myGov online inbox, a central and secure inbox where users can receive messages from myGov services, to send clients online letters, statements and other types of important information. The mailbox will enable the ATO to reduce the amount of correspondence it currently sends by mail and to quickly send clients confirming information while they are speaking to a CSR. This, in turn, could reduce further calls to the ATO to clarify correspondence clients have received.49

Reducing the need to contact the ATO

2.15 Most clients contact the ATO because of a need to comply with a taxation or superannuation requirement. These contacts may include the lodgement of an income tax return or a business activity statement, or be in response to a letter from the ATO in relation to a taxation audit or where the ATO is seeking information from the client. In such instances, there may be a need for the client to clarify these requests or provide requested information.

2.16 The ATO is examining ways of reducing the need for clients to contact the ATO. For example, from 2014 the ATO’s new myTax application can reduce the burden for compliant individuals with relatively straightforward taxation returns by pre-populating the tax return using information held by the ATO and asking the taxpayer to confirm or amend this information. The ATO estimates that there are around 1.5 million taxpayers for whom the myTax application would be suitable. As noted at paragraph 2.13, the ATO is also increasingly making it easier for clients to obtain information or transact their business online.

2.17 In this regard, the ATO is seeking to use ‘natural systems’, that is, systems such as financial accounting software that businesses use, to make it easier for clients to meet many of their taxation reporting obligations. As part of the ‘standard business reporting’ arrangements, the ATO is working with accounting software developers to promote the development of ‘one touch payroll’ in their software, which would enable businesses to perform all payroll transactions (payment of wages or salary, tax instalments and superannuation contributions) at the touch of a button.50 Paying all ATO employee-related obligations together as part of normal payroll transactions would avoid the need for businesses to provide separate returns to the ATO (at differing reporting periods). Businesses would also be better positioned to manage their ATO obligations, ultimately reducing defaults on payments to the ATO and to superannuation funds. This would, in turn, avoid the need for businesses to contact the ATO to obtain agreement to payment plans and other remedial measures.

2.18 As part of its strategy for using natural systems to help businesses to meet many of their taxation and superannuation reporting obligations, the ATO is also exploring the development of a common chart of accounts. This would facilitate annual reporting in accordance with accounting standards and reporting for taxation and superannuation purposes. If successfully implemented, these steps would also help to reduce the need for taxpayers to contact the ATO.

ATO’s management of service delivery

2.19 Aligning customer needs, services, channels and agency priorities as well as providing a seamless, integrated and consistent delivery of services across channels requires agencies to have an integrated approach to managing their various service delivery channels. These service delivery challenges require clear levels of responsibility and arrangements that promote effective and efficient service delivery.

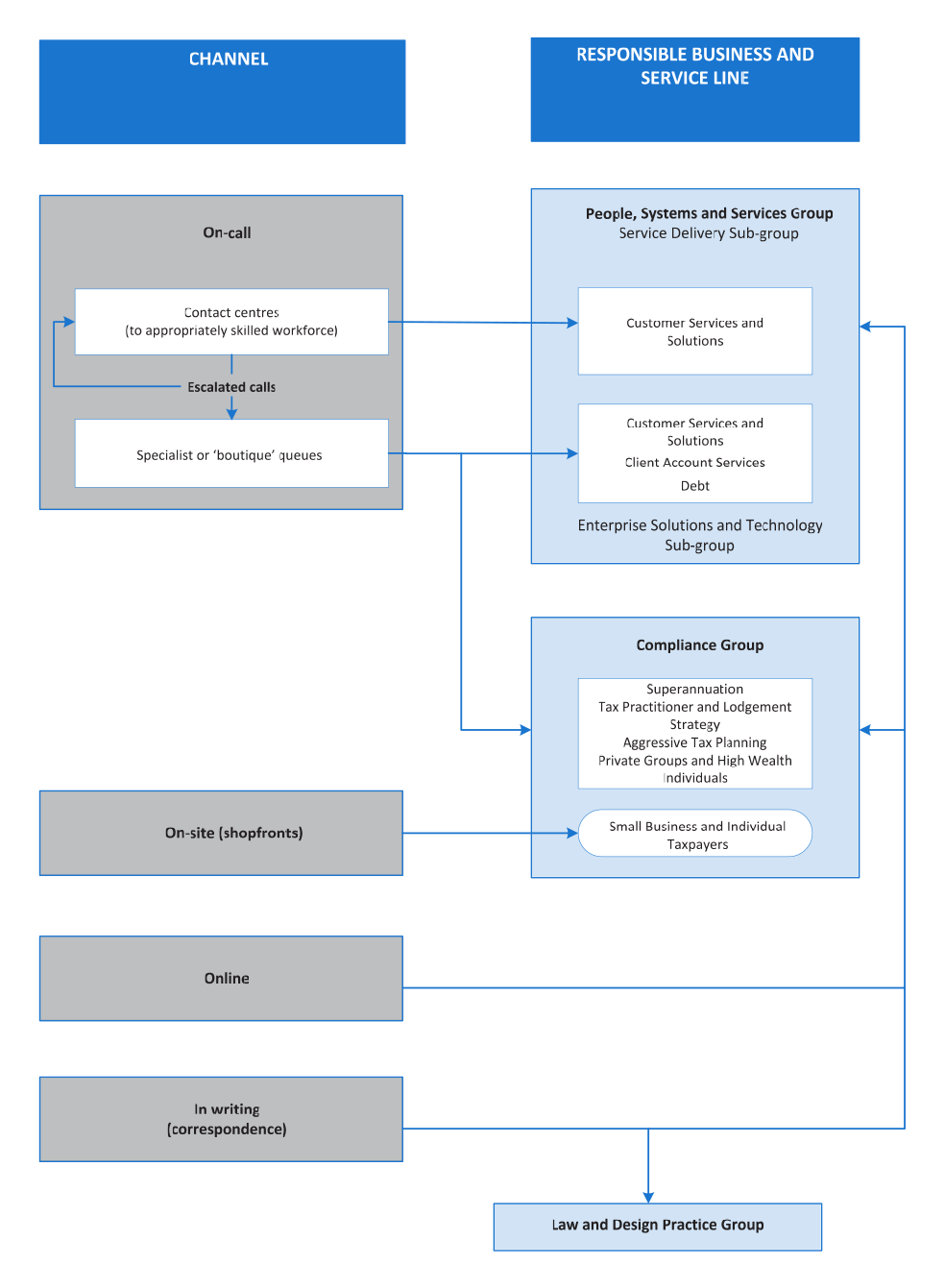

2.20 Currently the management of service delivery channels is allocated across a number of groups and business and service lines (BSLs) in the ATO, as shown in Figure 2.1. As a result of the allocation of responsibility across the ATO for the various service delivery channels, there is no single BSL with responsibility for: ensuring that the delivery of service is seamless and consistent; and managing the ATO’s channel strategy. However, cross-channel service improvements are considered by a Service Improvement Steering Committee, which is chaired by the Second Commissioner, People Systems and Services Group. This committee meets bi-monthly.

2.21 The current service delivery arrangements have also led to a duplication of responsibilities, for example, in service delivery workforce planning. The ATO has commenced the consolidation of some of these functions and, in 2014, it merged the various areas that were responsible for forecasting client demand into a single unit. It is also considering merging other functions, including service delivery workforce planning.

Figure 2.1: Organisational responsibility within the ATO for service delivery channels

Source: ANAO analysis of ATO data.

2.22 Supporting shopfronts presents similar issues to supporting on-call services. The ATO has, therefore, given preliminary consideration to the future of shopfronts and where management responsibility for these might best be located within the office. In particular, consideration is being given to locating the shopfronts in shared facilities with other agencies. For this reason, it has deferred further consideration of possible changes to the management of shopfronts within the ATO. In the event that shopfronts were to be located in shared facilities with other agencies, it will be important that the ATO management arrangements support the effective delivery of services by the shopfronts to ATO clients, consistent with the service delivery of other channels.

Conclusion

2.23 While the ATO interacts with its clients through a number of channels, its stated aim is for online to be the preferred channel. In this light, the ATO is developing a digital service strategy, although the strategy does not cover all channels. An overarching channel strategy would assist the ATO to transition to an online service environment, while also continuing to provide and improve the performance of other service channels—in particular call services. Such a strategy would enable the ATO to assign responsibility for the overall management of service delivery channels. Presently, the management of service delivery channels is assigned to a number of groups and BSLs, with scope for the ATO to adopt organisational arrangements that better support the coordinated delivery of client engagement services across all channels.

2.24 Notwithstanding the increased take-up of online services, the number of calls to the ATO is also increasing. It is expected that call services provided by contact centres will continue to be the preferred method of interaction for a large proportion of clients for the foreseeable future, unless action is taken to reduce the demand for call services. The ATO, therefore, needs to continue to deliver a high level of service through its on-call channel, while taking steps to increase the take-up of online services by improving accessibility and ease of use for clients.

2.25 The ATO is endeavouring to reduce the need for clients to contact the ATO in an effort to decrease the volume of calls. It is making it increasingly easier for businesses to obtain information or complete transactions through natural systems, such as financial accounting software.

2.26 As the entry-point to online services, it is important that the ATO’s website helps facilitate the take-up of online services. Improvements were made to the website in 2013, however further scope exists to assist clients to more easily locate the information they are seeking.

Recommendation No.1

2.27 To help deliver seamless, consistent and efficient services across all communication channels and to increase the take-up of online services, the ANAO recommends that the ATO:

- develops an overarching cross-channel strategy that details how the ATO plans to transition to an improved online service environment, while also continuing to provide and improve the performance of other service channels;

- adopts organisational arrangements that better support the coordinated delivery of services; and

- further develops its website to better support the delivery of online services.

ATO response: Agreed.

2.28 A long-term channel strategy will help connect the broader programs being managed across the ATO. A clear and supported channel strategy will assist the ATO in achieving the desired longer term channel shift goals. Specifically:

- a formal cross channel strategy would allow all parts of the ATO to contribute in a coordinated fashion with clear and visible outcomes, demonstrating progress;

- current organisational arrangements could be assessed to determine any other service-delivery elements that could be joined or at the least best practice approaches shared; and

- the ATO website continues to be a focus area, recognising that this is a key deliverable to support the organisational channel shift goals.

3. Operation of Australian Taxation Office Contact Centres

This chapter examines the operation of the ATO’s contact centres, including the extent to which they are supported by business and administrative arrangements.

Introduction

3.1 Managing contact centres in a large organisation, such as the ATO, is a complex undertaking, with contact centre CSRs required to respond efficiently and effectively to a broad range of enquiries from ATO clients around Australia. The level of call demand will also fluctuate, depending on the taxation and superannuation obligations of ATO clients at different times of the year. For instance, a peak period for the ATO in terms of call demand for individual taxpayers is July to October of each year, when taxpayers are expected to lodge their annual income tax returns.

3.2 In this context, the effective operation of contact centres51 requires the ATO to:

- have a service model that enables calls to be directed to CSRs with the necessary skills to respond to the specific issues;

- have an appropriate organisational structure under which call services are delivered;

- be in a position to manage workload by accurately forecasting the number of calls that are likely to be received and tailor resources to meet expected call demand;

- have arrangements in place to support staff to efficiently and effectively respond to queries from callers;

- provide effective oversight of outsource providers;

- have arrangements in place to determine whether a quality service is being provided;

- have arrangements in place to respond to incidents that adversely affect business continuity; and

- have implemented measures to promote the health and wellbeing of staff working in contact centres.

Call handling service model

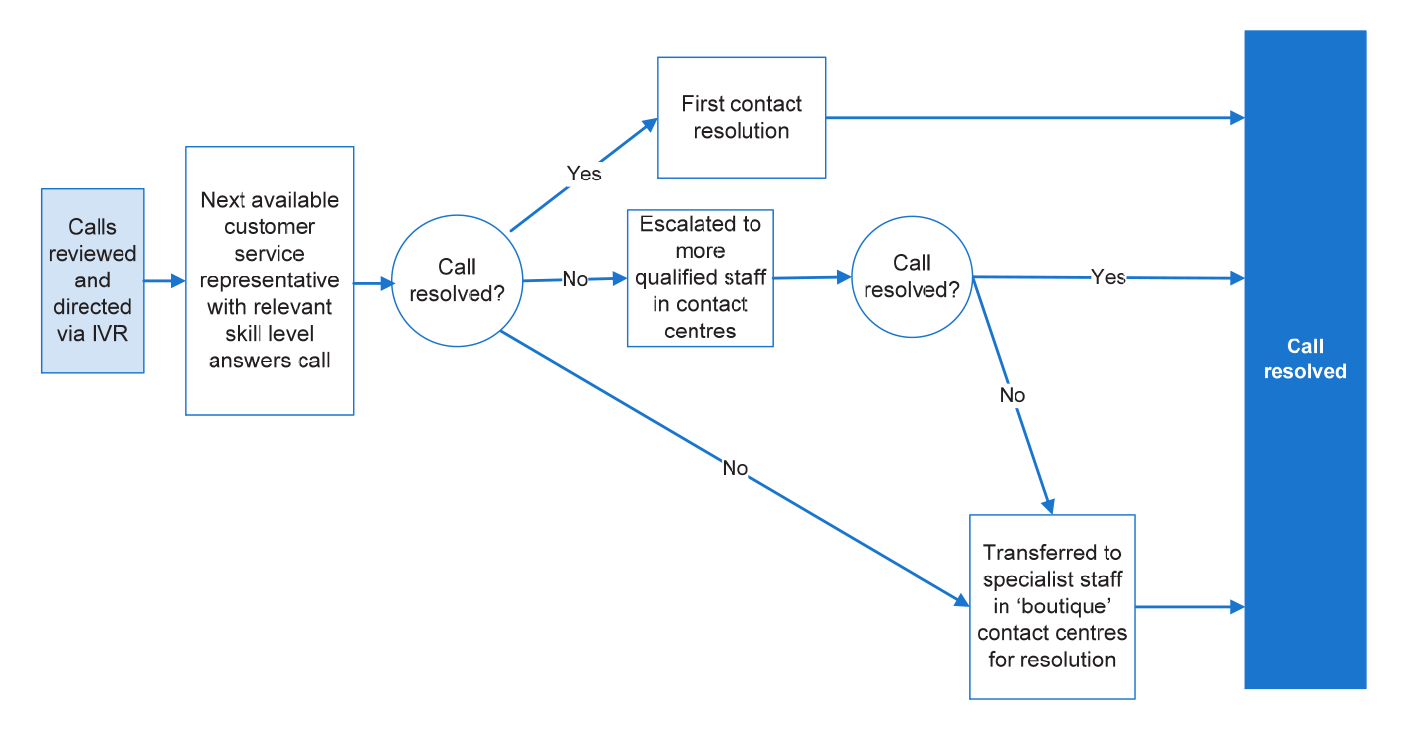

3.3 When a person calls the ATO, they are asked to select from a number of options in the ATO’s interactive voice response (IVR) unit.52 This is to enable the call to be directed to a contact centre staff member who is skilled to answer the caller’s enquiry. Some calls may still need to be directed to other CSRs, either because the nature of the enquiry may require more specialised support or because a call concerns a number of different matters, some of which the initial CSR is not qualified to answer.

3.4 More complex calls are escalated or transferred to specialists in contact centres operated by individual BSLs. The ATO refers to these centres as ‘boutique’ contact centres.53 In some cases, the contact centre CSR will speak to the CSR to whom the call is being escalated. Where this is not possible, the call may be put into the relevant queue to be answered by the next available operator. A CSR can also register details of an enquiry into the ATO’s customer relationship management system and arrange for an appropriately skilled officer to call the person back at a later time. These are termed ‘non-phone escalations’. The process for handling incoming calls is depicted in Figure 3.1.

Figure 3.1: Process for handling inbound calls to the ATO

Source: ANAO analysis of ATO data.

Note: Escalation and transfer of calls may include non-phone escalations (see paragraph 3.4).

3.5 A key challenge for most contact centres is the appropriate streaming of calls—that is directing the caller to a CSR that is best qualified to respond to the caller’s issue. IVR menu-based systems have a limited capacity to do this, with the ATO investigating the use of voice recognition technology, where the system recognises words spoken by the caller, to more accurately direct calls.

3.6 In the meantime, the ATO has introduced voice recognition technology to assist with caller identification, called ‘Voiceprint’.54 While this can improve caller identification, and as a result reduce the time required to identify callers, it is not currently being used to direct calls to customer service representatives.55 The United Kingdom’s tax administration also introduced a similar system in December 2013. It uses speech recognition to determine the caller’s requirements and provide the most appropriate response or direct the call to a suitable adviser. Such a system may reduce the need for calls to be escalated, because the call would automatically be channelled to the CSR with the necessary skills. The ATO is considering the merits of these types of systems.

3.7 Following a substantial investment in new technology over recent years, calls to ATO contact centres can be directed to the next available CSR, whether they are located in an ATO or an outsourced centre. The ATO’s network architecture also provides the capacity for the ATO to use its infrastructure to support the call services of other agencies. In this regard, the ATO has entered into an arrangement with AUSTRAC (the Australian Transaction Reports and Analysis Centre) to provide call services. The outcomes from this arrangement have the potential to provide useful information for other agencies considering the joint provision of call services.

Organisational structure of contact centres

Size and composition of call handling teams

3.8 As outlined earlier, the ATO contact centre network consists of 13 centres, eight of which are ATO operated centres and the remaining five are outsource centres. When a call is received, it is directed to the next available CSR in any of these centres with the required skills, as indicated by the caller’s IVR selection. There were 1206 ATO full-time equivalent (FTE) staff answering calls in 2013–14 (compared to 1157 FTE in 2012–13).56

3.9 Typically, CSRs are grouped into different call handling teams within a contact centre, each with between 15 and 17 CSRs, including team leaders. The size of these teams is slightly higher than the average number of agents per team leader or supervisor (13:1) in Dimension Data’s Global Contact Centre Benchmarking Report.57 The largest of the ATO operated centres visited during the audit had nine teams and the smallest had four teams.58 These centres are supported by a team that quality assures calls as part of the national quality assurance process and provides training, coaching and service consultancy support to staff handling calls. Contact centre management includes an attendance manager, whose role includes: negotiating staff rostering; helping to reduce unplanned leave; and addressing the work-related health issues of staff on long-term sick leave.

3.10 The outsource centres have a similar structure to the ATO-operated centres, but the number and size of their teams vary greatly, depending on the number of calls that they are expected to handle at different times of the year. For instance, outsource centres handle most of the increase in calls arising from the Tax Time income tax return lodgment period from July to October each year. One of the centres indicated that it will have between 16 and 18 teams during Tax Time and another centre around 13 teams. At other times of the year, they have smaller numbers of teams.

3.11 The size of a team needs to have regard to the level of support required for individual team members, both in responding to calls and in addressing development needs. The number of teams in a centre also has to have regard to the overhead costs involved, including management and quality development. Some of the ATO’s centres are relatively small, with five or six teams, and there may be scope to consolidate some smaller centres to save costs. However, for these centres, some management overheads are allocated across more than one centre59 and the ATO advised that these centres also have experienced staff, many with skills in specialised areas. These factors may reduce the extent of potential savings.

Tiered skilling model

3.12 The ATO uses a tiered skilling model, in which subject areas are grouped into three tiers based on the level of complexity.60 Each CSR would be expected to have an understanding of routine matters within the subject areas. However, other matters require more specialised knowledge and these calls must, therefore, be answered by CSRs who have the requisite knowledge. Under the tiered skilling model, each CSR has an approved skills requirement to respond to certain calls, with each section of the explanatory material ‘badged’ with the skill set relevant to the call type/skill requirements.

3.13 A May 2012 review of the ATO’s contact centres by an external consultant, discussed in paragraph 3.23, found that the tiered skilling model was more effective than a call handling model based on individual taxation or superannuation subject matter levels. It found that the tiered skilling model reduced costs61, improved customer experience due to a lower percentage of transfers and provided greater flexibility in staff rostering. While finding that the tiered skilling model was effective, the external consultant recommended that the ATO continue to prioritise and align existing specialist and complex calls, review the routing of calls and further broaden its skill model. The ATO has responded to the review’s recommendation to align specialist contact centres by migrating the Small Business and Individual Taxpayers BSL’s ‘boutique’ telephony work to the CS&S BSL in March 2014 and is planning also to transfer the telephony work of the Tax Practitioner Lodgement Strategy BSL to the CS&S BSL.

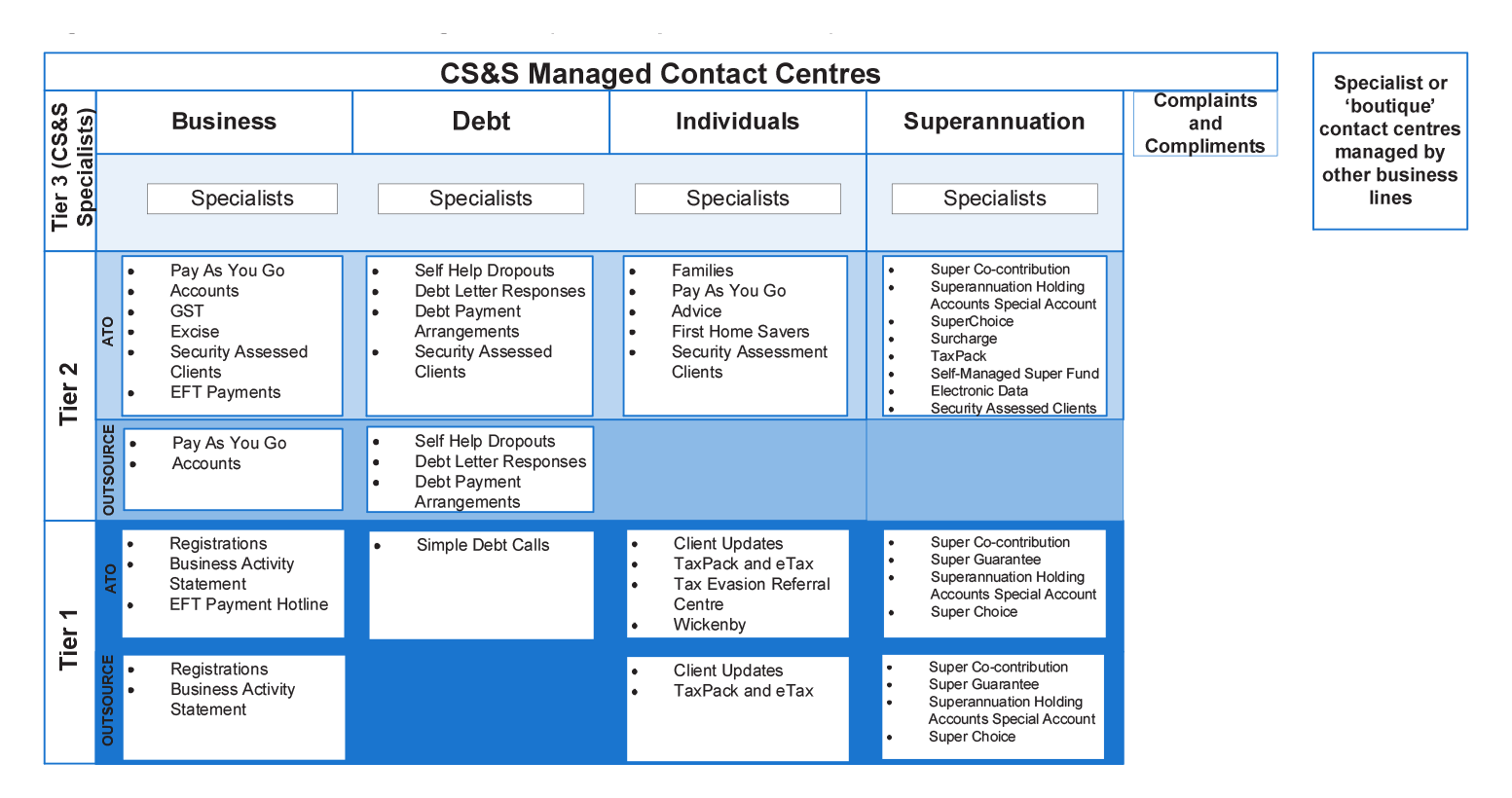

3.14 The ATO also conducted an internal review of the contact centre service model in 2013, which recommended improving the consistency of its service outcomes by reducing skill gaps.62 The ATO has now updated the skills and training required by staff in order to meet service levels and refined the skills configurations of its telephone service model. The ATO explored six options with varying skilling configurations.63 The configuration that has been adopted by the ATO is shown at Figure 3.2. Under this model, CSRs are skilled in one or more of the business, debt and individuals taxation modules or one or more of the superannuation modules.

Figure 3.2: ATO tiered skilling model (as at September 2014)

Source: ANAO adaptation of ATO data.

Workload management

3.15 A major challenge for any organisation with a large network of contact centres is to prepare credible forecasts of call demand, to ensure that it has adequate available resources to handle these calls and roster available staff. It is also important to have regard to the requirement for CSRs to have regular breaks for occupational health safety considerations.

Forecasting call demand

3.16 The ATO has a Forecasting Unit, which is responsible for developing forecasts of call demand. Long-term (12 to 24 months) forecasts of call demand are initially prepared. These are then refined, with medium-term (three to six months) and short-term (one week to nine weeks) forecasts subsequently prepared. The long-term forecasts assist in resource planning, including identifying any resource gaps and determining annual resource allocations for the contact centres, as well as the recruitment and training of staff, both in the ATO operated contact centres and the outsource contact centres. The short-term forecasts are used in the scheduling of staff.

3.17 The ATO recognises that many calls are generated in response to the actions that it takes (such as letters to clients or the legal obligations of clients). To help manage and accurately forecast call demand, CS&S is consulted about changes the ATO proposes to make, particularly where clients will be advised of the option to call the ATO. As part of this process, BSLs are required to complete a telephone clearance form, which outlines the change involved, the importance of the change and the process to be followed. Within CS&S, the Forecasting Unit is primarily responsible for assisting in determining the resource implications of, and resource planning for, ATO campaigns.

3.18 The ATO consolidated its forecasting functions across the service delivery sub-group in early 2014. Prior to this, the Forecasting Unit only prepared forecasts of call demand and visits to shopfronts. BSLs, such as Debt, Client Account Services, Small Business and Individual Taxpayers, and Tax Practitioner and Lodgment Strategy, prepared their own forecasts. The consolidation of forecasting functions is expected to lead to greater consistency in the way in which forecasting is carried out and to some efficiencies by bringing together the capability that previously existed in the different areas.

3.19 In 2013–14, the number of Tier 1 calls offered was close to the number of calls budgeted for the mainstream contact centres.64 However, the number of escalated calls was different to the budgeted levels, with the number of Tier 2 calls received (3.36 million) being 13 per cent higher than budgeted (2.97 million) and the number of Tier 3 calls received being 21 per cent lower than budgeted (307 773 compared to 387 392 calls). For all tiers (that is the number of Tier 1 calls received plus the number of calls escalated to Tiers 2 and 3), the number of calls (8.8 million) was five per cent higher than forecast (8.4 million) calls.65 The ATO refines its demand forecasts during the year as more accurate information becomes available.

Scheduling of contact centre staff

3.20 Call demand forecasts are used to prepare detailed work management plans down to the officer level for ATO contact centre staff. Outsource centres are also provided with details of the numbers of calls that they are expected to handle. It is then the responsibility of the outsource centres to schedule staff to meet the specified numbers of expected calls.

3.21 The ATO uses a proprietary workforce management software product to help manage its contact centre workforce. Restrictions and requirements, such as expected call loads, average handling times and staff leave can be entered into the system. The ATO will then produce a demand and resourcing profile in 15 minute increments for a four week period, designed to support the forecast workload (prepared by the Forecasting Unit). The available resources of the outsource contact centres (dependent on the agreed workload capacity for each centre) are factored into these workforce management calculations.

3.22 The ATO’s 2011 Enterprise Agreement requires an employee and their manager to agree on the employee’s regular hours within the bandwidth specified in the Agreement (7.45 am to 6.15 pm) to enable the ATO to meet its 8:00 am to 6:00 pm client service window. In accordance with this agreement, staff preferences from the preferential rostering system are added directly into the workforce management system by staff and are applied to the required resourcing profile to calculate coverage levels. The system can be used to produce a four-week schedule, four weeks in advance, to determine coverage. This provides time for negotiations between management and staff in each contact centre to fill any gaps in service provision and achieve full coverage. If required, for example because of unplanned leave or other staff needs, the schedule can be altered up until the day before it is operational.

3.23 The Enterprise Agreement provides that, in reaching an agreement about an employee’s regular hours, the needs of both the employee and clients should be considered and that a manager can require an employee to work all or part of their regular hours. However, in practice, the ATO does not require an employee to work a certain number of hours to meet gaps in service provision. Instead the ATO relies on negotiating with staff to change their preferences. The ANAO was advised by some ATO contact centre managers that this process was time-consuming and that some staff consistently declined to change their preferences (mainly relating to late shifts). A 2012 review of the ATO’s contact centres by an external consulting firm also found that the ATO’s current preferential rostering arrangements inhibit the optimal utilisation of staff.66 There would be merit in the ATO reviewing its current rostering arrangements to help ensure the optimal utilisation of contact centre staff.

Real-time management of calls