Areas examined

The ANAO examined whether the corporate plans of the four selected entities were positioned as the entity’s primary planning document in line with the Government’s policy intent. The ANAO also examined:

- the systems and processes in the four entities for the development of their corporate plan;

- whether entity corporate plans met mandatory reporting requirements and reflected guidance provided by the Department of Finance (Finance); and

- the subsequent monitoring of achievements against these plans.

Conclusion

In line with the policy intent of the performance framework, one entity had positioned its corporate plan as the primary planning document and a second entity was working to do so. Two entities did not fully meet the policy intent.

The four entities are continuing to develop their processes for developing the corporate plan and two entities had developed arrangements for monitoring the implementation of their corporate plans. Two entities had less mature systems and processes for monitoring implementation.

Entities have completed two corporate plans under the Public Governance, Performance and Accountability Act 2013 (PGPA Act) and these findings could be expected in view of the relatively early stage of implementation of the corporate plan requirement. More active attention from senior management is required to further embed the requirements in the third cycle of corporate planning.

Opportunities for improvement

The ANAO’s review has identified opportunities for improvement relating to:

- systems and processes for developing the corporate plan;

- the content of mandatory sections of the plan; and

- systems and processes for monitoring and reporting on the implementation of the plan.

Introduction

2.1 The ANAO developed an assessment matrix (provided at Appendix 3) that was used to review:

- whether the corporate plan is positioned as the entity’s primary planning document;

- the maturity of the entity’s corporate plan; and

- the maturity of the processes followed by the enitites in developing their second corporate plan (for the 2016–17 planning cycle) under the PGPA Act and their monitoring of the implementation of these plans.

2.2 The ANAO’s review took into account that the corporate planning initiative establishes minimum standards and remains in the relatively early stage of implementation. It could therefore be expected that entity systems and processes will mature over time, as will the content of corporate plans. Further, the optimum or desirable maturity level for individual entities will depend on the entity’s particular circumstances and the expectations of senior management. The level of maturity of systems and processes and of the corporate plan itself is a decision to be made by an entity’s Accountable Authority.

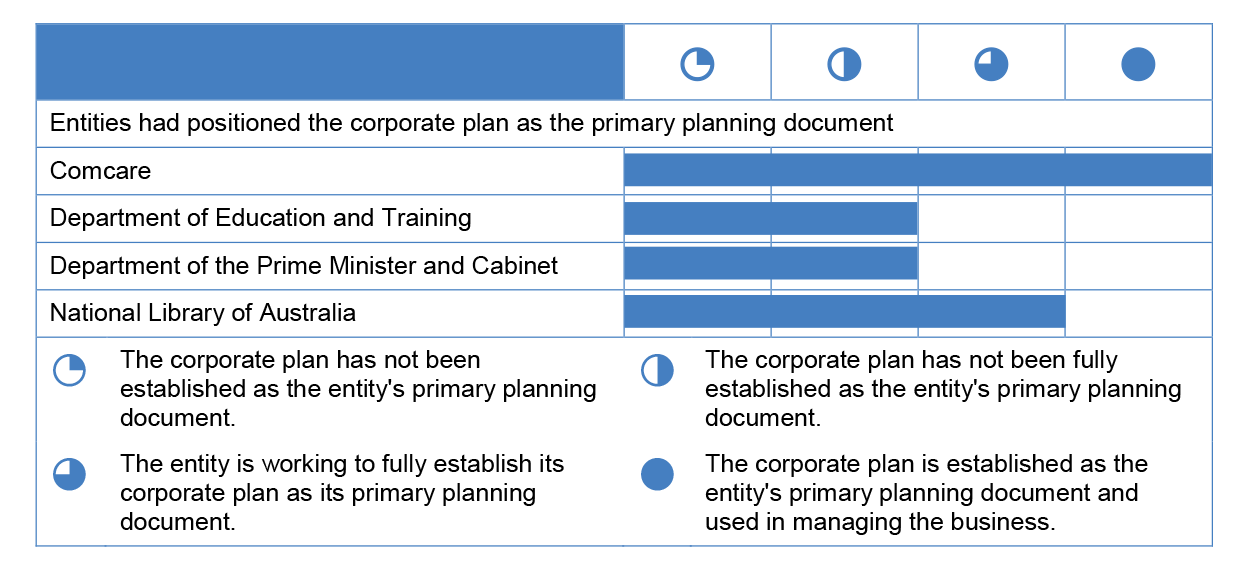

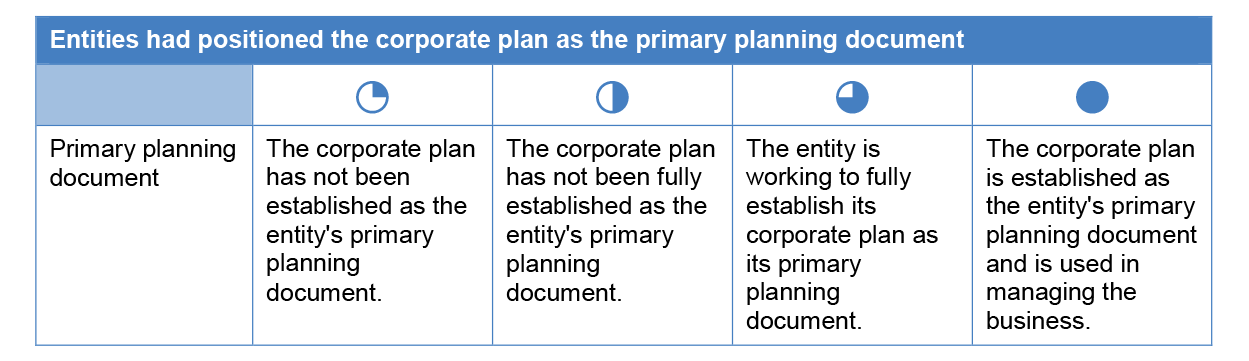

Were corporate plans positioned as the entities’ primary planning document?

Comcare had established its corporate plan as its primary planning document and was using it to manage its business. The National Library of Australia (NLA) was working to fully establish its corporate plan as its primary planning document. In the Department of Education and Training (Education) and the Department of the Prime Minister and Cabinet (PM&C) the corporate plan had not been fully established as the entity’s primary planning document.

2.3 Under the Enhanced Commonwealth Performance Framework, the corporate plan is intended to be an entity’s primary planning document. It is required to set out the purposes and activities that the entity will pursue and the results it expects to achieve, including a description of the environment and context in which the entity operates, and its planned performance measures, risk profile and capabilities over a minimum of four reporting periods.

2.4 The ANAO assessed the maturity of the selected entities’ 2016–17 corporate plans and supporting systems and processes, to assess whether entities had positioned their corporate plans as their primary planning documents. Specifically, the ANAO considered whether:

- planning frameworks incorporated entity corporate plans as the central element;

- entities monitored achievements against their plans to assist in driving business performance; and

- senior management was fully engaged in the development and monitoring of the plans.

2.5 The ANAO’s overall assessment of whether entities’ corporate plans (prepared for the 2016–17 planning cycle) were positioned as the entity’s primary planning document is presented in Figure 2.1.

Figure 2.1: Assessment of whether corporate plans were positioned as the entities’ primary planning document (2016–17 planning cycle)

Source: ANAO analysis.

2.6 Comcare had established its corporate plan as its primary planning document and was using it to manage its business. Comcare had fully integrated the corporate plan with other business planning and was monitoring its performance against the performance measures and other commitments included in the corporate plan.

2.7 The NLA was working to fully establish its corporate plan as its primary planning document and had revised its reporting to senior management and the governing Council to reflect the strategic priorities outlined in the corporate plan, and used its corporate plan to progressively enhance its performance measurement.

2.8 The corporate plan had not been fully established as the entity’s primary planning document in Education and PM&C. There was scope to further enhance systems and processes for monitoring performance against the performance measures and other commitments included in the corporate plan. Monitoring and reporting continued to be against performance measures included in other planning documents and those measures did not fully align with the measures included in the entity’s corporate plan. Both entities have advised the ANAO that they recognise that there needs to be stronger alignment between the corporate plan and business planning.

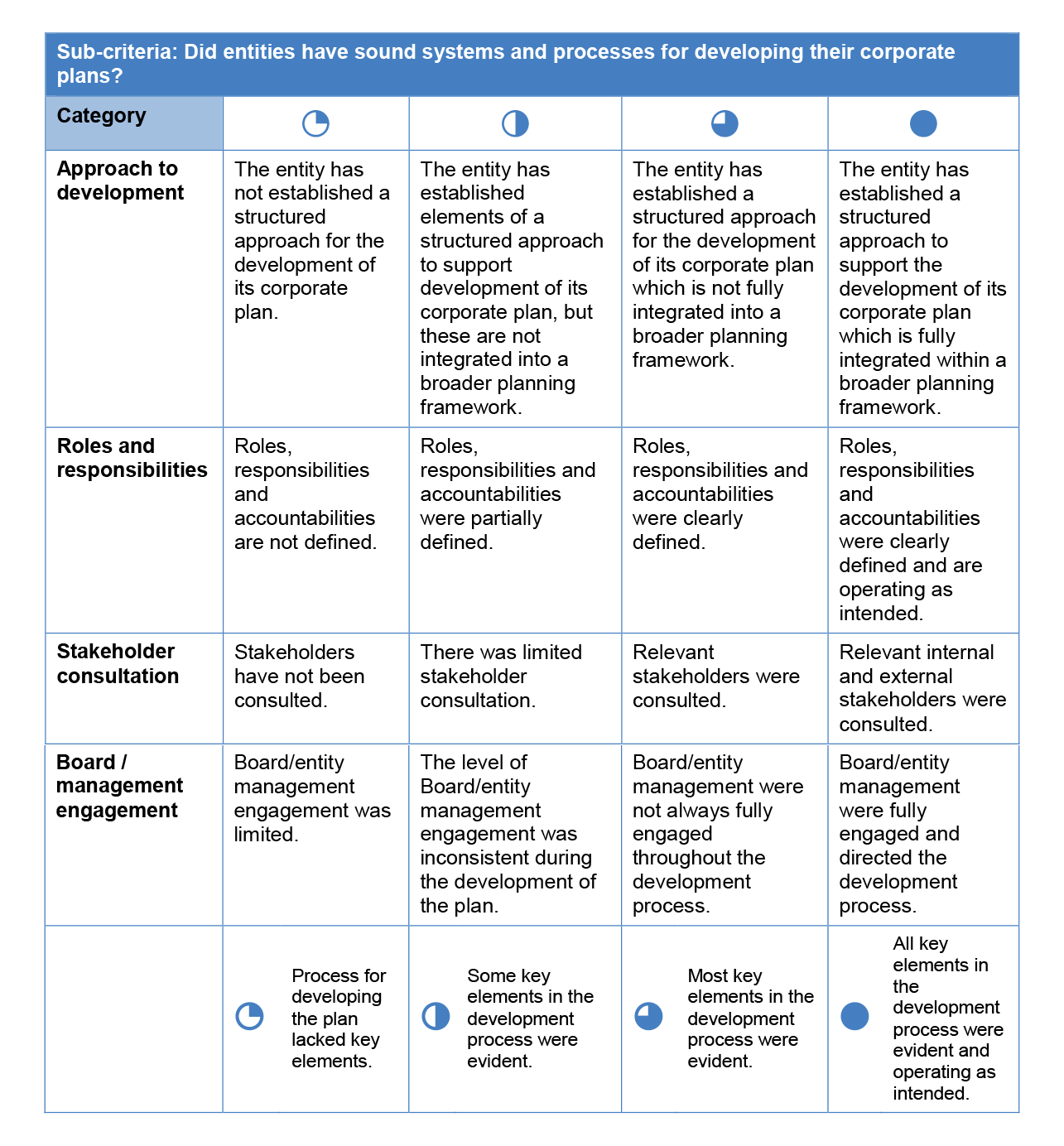

Did entities have sound systems and processes for developing their corporate plan?

The quality and implementation of relevant entity systems and processes was variable. There remains scope for the selected entities to strengthen the systems and processes used for developing their corporate plans. A more structured approach would involve:

- implementation of a documented process and schedule for development of the corporate plan (all entities);

- better integration within the entity’s broader planning framework (all entities);

- clearer definition of roles, responsibilities and accountabilities and the operation, as intended, of defined roles, responsibilities and accountabilities (all entities);

- development of strategies for more systematic engagement of stakeholders (all entities); and

- earlier and more systematic involvement of the entity’s executive management in the corporate planning process (Education and PM&C).

2.9 In reviewing the systems and processes of the selected entities in developing their corporate plan, the ANAO considered whether entities:

- established structured approaches to support the development of their plans;

- clearly defined roles, responsibilities and accountabilities;

- consulted internal and external stakeholders; and

- had fully engaged their senior management and/or Board.

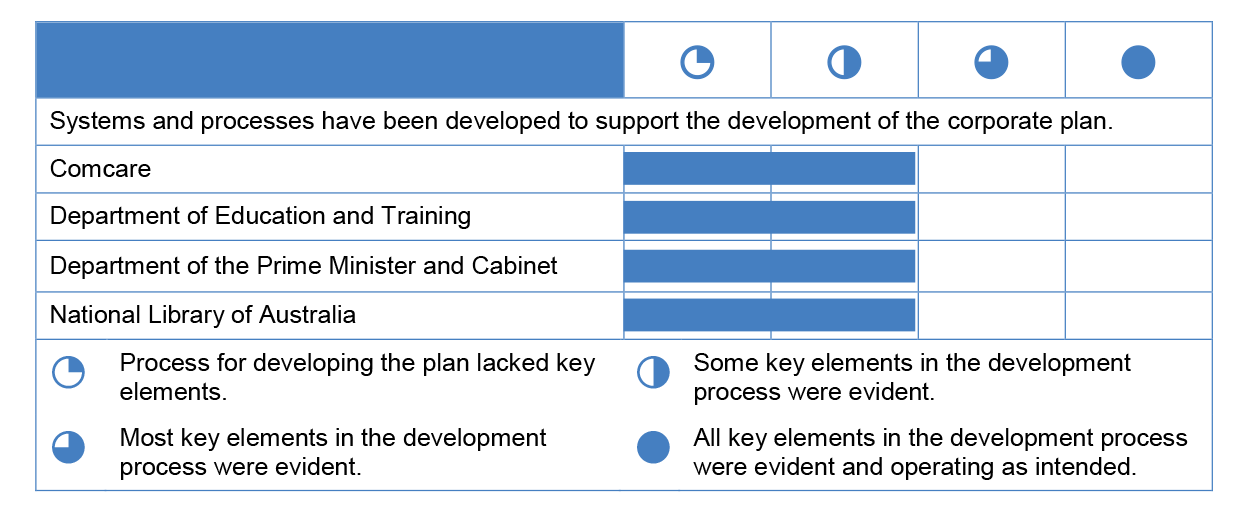

2.10 The ANAO’s overall assessment of the maturity of the systems and processes adopted by the selected entities to develop their corporate plan (prepared for the 2016—17 planning cycle) is presented in Figure 2.2.

Figure 2.2: Assessment of the maturity of entities’ systems and processes to support the development of corporate plans (2016–17 planning cycle)

Source: ANAO analysis.

2.11 There was no clearly documented process supporting the development of the corporate plan in Comcare, NLA and PM&C. Where a documented process and schedule were in place at Education it was, for a number of reasons, not followed.

2.12 The corporate plan requirement was driving changes to entity planning arrangements and processes in each entity but more so in Comcare and the NLA. In all four entities there was scope to further integrate the development of the corporate plan into the entities’ planning framework. In addition, not all roles, responsibilities and accountabilities were documented or were fully operating as intended in the four entities.

2.13 Across the four entities there was either no or limited consultation with external stakeholders to assist in shaping the content of the corporate plans, and no formal arrangements in place for this to occur. In Education and PM&C there was scope to engage senior management earlier and more systematically to better direct the development process.

Opportunities for improvement in relation to developing corporate plans

2.14 There remains scope for the selected entities to strengthen the systems and processes used for developing their corporate plans. A more structured approach would involve:

- implementation of a documented process and schedule for development of the corporate plan;

- better integration within the entity’s broader planning framework;

- clearer definition of roles, responsibilities and accountabilities and the operation, as intended, of defined roles, responsibilities and accountabilities; and

- development of strategies for more systematic engagement of stakeholders and executive management in the corporate planning process.

Did entities’ corporate plans meet the requirements of the PGPA Rule?

Each of the selected entities met the minimum requirements for the publication of their corporate plans prepared for the 2016–17 planning cycle. Entity plans were provided to responsible Ministers and the Finance Minister as required, and placed on entity websites by 31 August 2016.

The selected entities included the six specific matters required by the PGPA Rule. These are an introduction and matters relating to the entity’s purposes, environment, performance, capability, and risk oversight and management. There is scope for entities (Comcare, Education and PM&C) to add additional value to the corporate planning process by providing a summary of the risk oversight and management systems of the entity which also addresses the interaction of key system elements.

The content, interpretation and application of one mandatory process requirement—that four of the six minimum content requirements are required to cover the four reporting periods of the corporate plan—remains an issue for entities, notwithstanding the release of revised Finance guidance in July 2016. The clarity of current requirements should be considered as part of the review of the operations of the PGPA Act and the PGPA Rule to be conducted after 1 July 2017.

2.15 The PGPA Act (section 35) requires the Accountable Authority of a Commonwealth entity to prepare and publish a corporate plan each year in accordance with any requirements prescribed by the PGPA Rule. There is a similar requirement (section 95) for the directors of a Commonwealth company. The PGPA Rule (section 16E) outlines the minimum content and publishing requirements for all corporate plans (see Appendix 2).

2.16 All of the selected entities met the minimum requirements for the publication of their corporate plans for the 2016–17 planning cycle. These requirements are to provide their corporate plan to the relevant Minister and the Minister for Finance prior to publishing the plan on the entity’s website by 31 August 2016.

2.17 The PGPA Rule also requires that six specific matters be included in entity corporate plans. These matters are: an introduction, and matters relating to the entity’s purposes, environment, performance, capability, and risk oversight and management. All entities included the six matters in their corporate plans. Two specific issues identified in the course of the audit are discussed below.

Risk oversight and management

2.18 The PGPA Rule requires entities to include in their corporate plan a summary of the risk oversight and management systems of the entity for each reporting period covered by the plan, including any measures that will be implemented to ensure compliance with finance law.

2.19 While each of the selected entities included some descriptive information about their risk management processes, the NLA also addressed the interaction of key system elements. This approach adds additional value to the corporate planning process by providing the Parliament and stakeholders with specific information and enhanced assurance about the way an entity is managing its risks.

2.20 Example 2.1 illustrates how the NLA’s summary addressed the interaction of key system elements.

|

The relevant section of the corporate plan identifies that:

- The NLA’s Corporate Management Group is responsible for identifying and managing risks associated with collecting, storing and making available the NLA’s collections; and reports regularly to the NLA Council through the Audit Committee.

- The Audit Committee considers the appropriateness, adequacy, efficiency and effectiveness of the NLA’s internal control system and procedures for risk oversight and management, and oversees compliance with those systems and processes.

- The principal risk and mitigation strategies are managed through the NLA’s Emergency Planning Committee, which is guided by the NLA’s Risk Management Framework.

- The Emergency Planning Committee and Corporate Management Group are responsible for: determining the NLA’s appetite for risk; and developing and reviewing annually the NLA’s Risk Management Register and the procedures and plans for significant business risks.a

|

Note a: These include the Collection Disaster Plan, the Information Technology Disaster Recovery Plan, the Business Contingency Plan for Critical Building Systems, the Business Continuity Framework and the Work Health and Safety Framework.

Source: ANAO summary of NLA corporate plan risk oversight and management.

Four year time horizon

2.21 The PGPA Rule also requires that information relating to four of the six matters is to be provided for each reporting period covered by the plan. Finance’s review of the first cycle of corporate plans (2015–16 planning cycle) identified this area as one in which entities consistently did not meet the mandatory requirements. The ANAO’s previous performance audit of the corporate planning requirements commented that Finance should clarify, in future guidance, the requirements relating to reporting on each period covered by the corporate plan. Finance released revised guidance in July 2016 which stated that:

All six of the minimum requirements under subsection 16E (2) of the PGPA Rule are required to cover the four reporting periods of the corporate plan.

2.22 However, Finance’s guidance went on to advise that entities could adjust their approach somewhat, depending on the requirement:

It is expected that issues under the Environment, Capability, and Risk Oversight and Management requirements are discussed for the whole period covered by the corporate plan (four years).

For the Performance requirement, an entity must specifically cover the four reporting periods of its corporate plan.

2.23 In addition to issuing guidance, Finance raised this matter in its Community of Practice sessions with entities and in its January 2017 lessons learned paper on 2016–17 corporate plans.

2.24 The content, interpretation and application of the requirement and revised guidance (discussed at paragraphs 2.21 to 2.22) remains an issue for the entities examined in this audit and should be considered as part of the review of the operations of the PGPA Act and the PGPA Rule to be conducted after 1 July 2017 (in accordance with section 112 of the PGPA Act). The entities selected for this audit did not report, in a manner that specifically addressed the four reporting periods, for each of the four mandatory sections of the plan.

- Comcare, Education, and PM&C did not clearly address each of the four reporting periods covered by their corporate plan in the environment, capability and risk sections of their plans. The NLA did not clearly address each of the four reporting periods covered by its corporate plan in the capability and risk sections of its plan.

Opportunities for improvement in relation to meeting the requirements of the PGPA Rule

2.25 Subsection 35(2) of the PGPA Act provides that the corporate plan must comply with any requirements prescribed by the PGPA Rule. There is scope for entities to improve compliance with the mandatory requirements relating to the content of corporate plans by providing a summary of the risk oversight and management systems of the entity which captures the interaction of key system elements (Comcare, Education and PM&C).

2.26 As noted in paragraphs 2.21 to 2.24, one mandatory process requirement—that four of the six of the minimum requirements under subsection 16E(2) of the PGPA Rule are required to cover the four reporting periods of the corporate plan—remains an issue for the entities. The clarity of current requirements should be considered as part of the review of the operations of the PGPA Act and the PGPA Rule to be conducted after 1 July 2017.

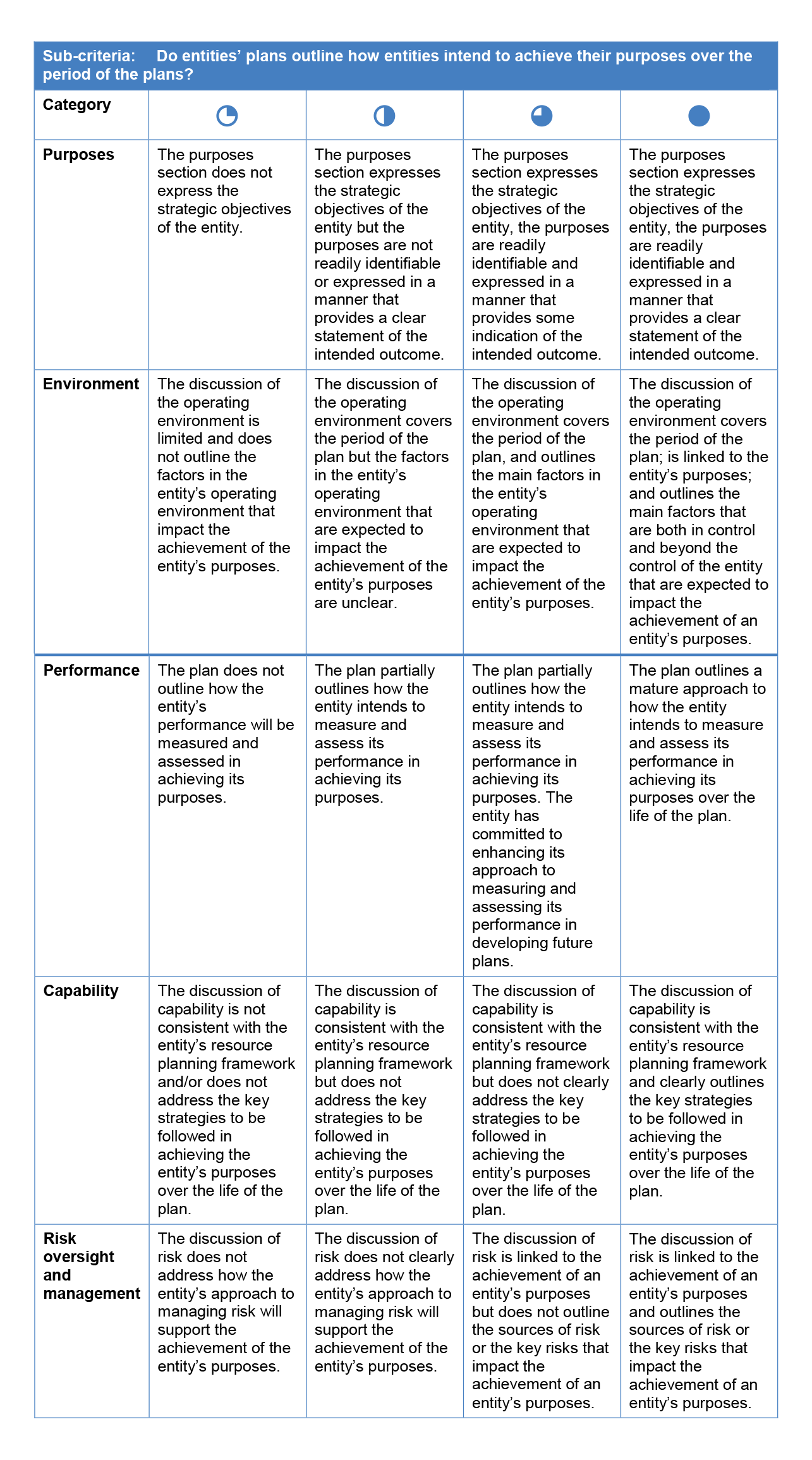

Did the corporate plans outline how entities intended to achieve their purposes over the period of the plan?

The ANAO’s assessment of the maturity of each key mandatory section of the selected entities’ corporate plans—relating to purposes, environment, performance, capability, and risk oversight and management—indicates that there is scope for improvement in respect to:

- Purposes—by making purposes more readily identifiable (Education), and by providing a clearer statement of the intended outcome (NLA and PM&C).

- Environment—by better outlining the main factors that are both in control and beyond the control of the entity that are expected to impact the achievement of an entity’s purposes (all entities except NLA).

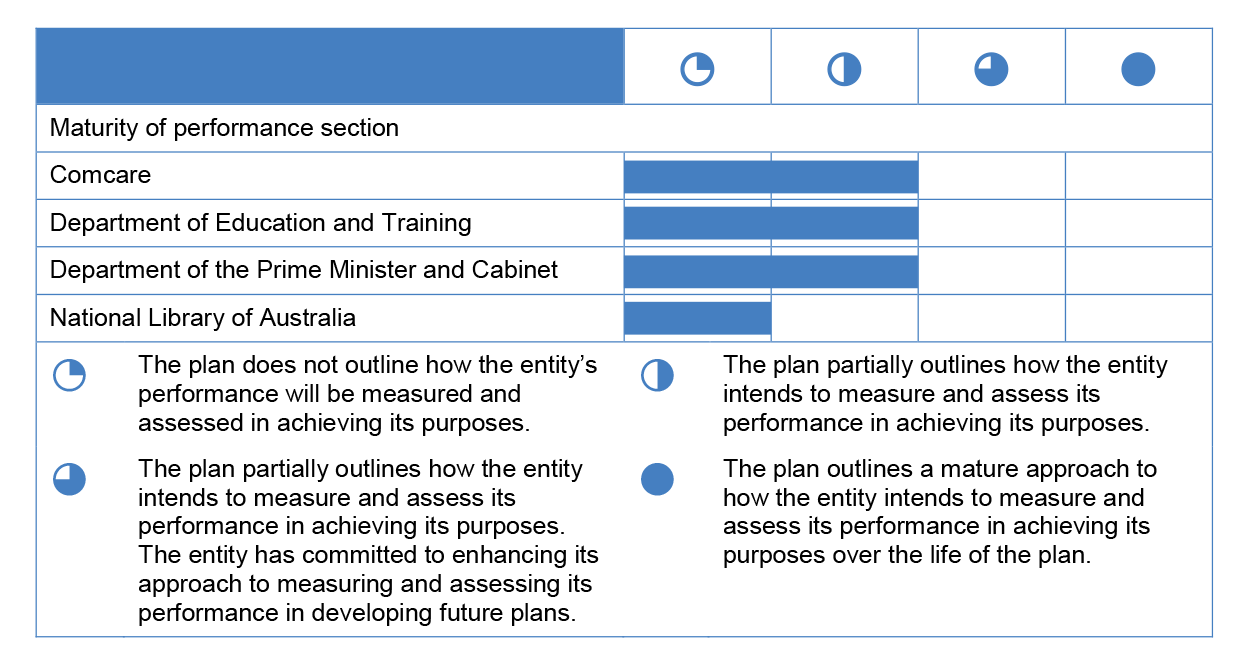

- Performance—by more clearly outlining how the entity intends to measure and assess its performance in achieving its purposes over the life of the plan (all entities except Comcare).

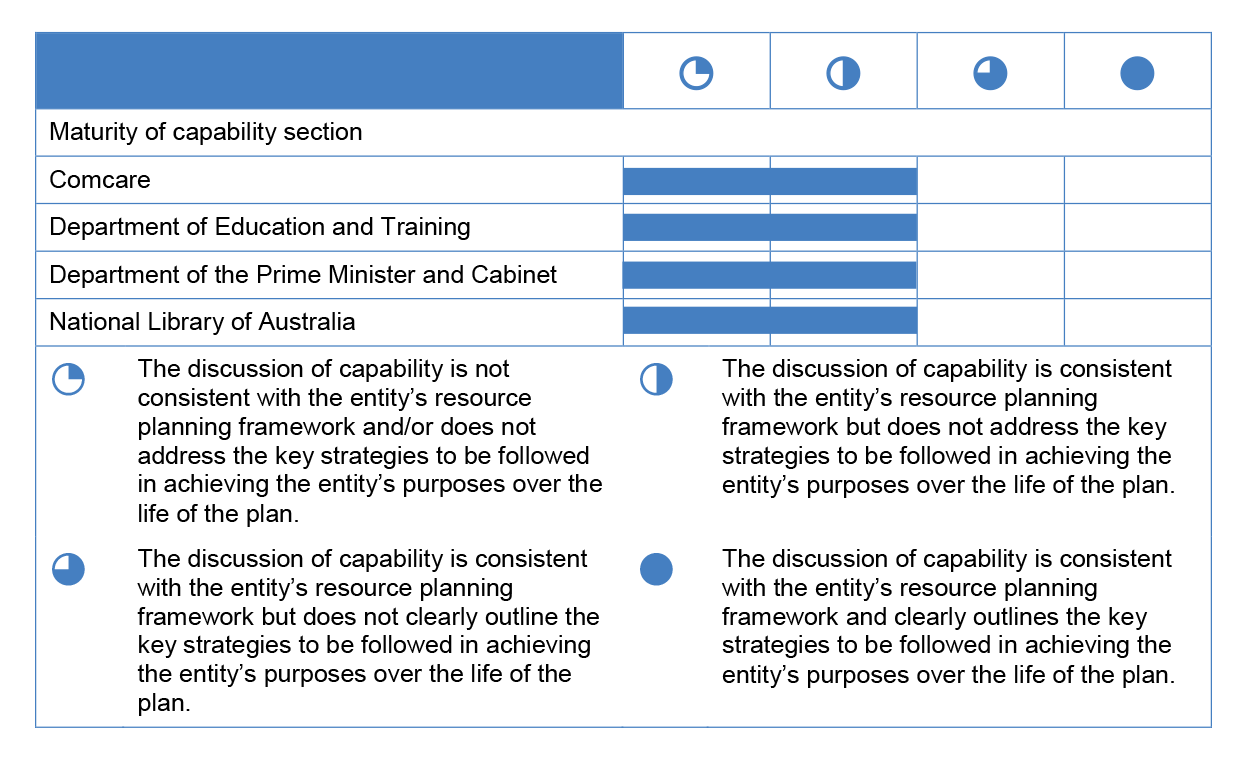

- Capability—by more clearly outlining the strategies to be followed in achieving the entity’s purposes over the life of the plan (all entities).

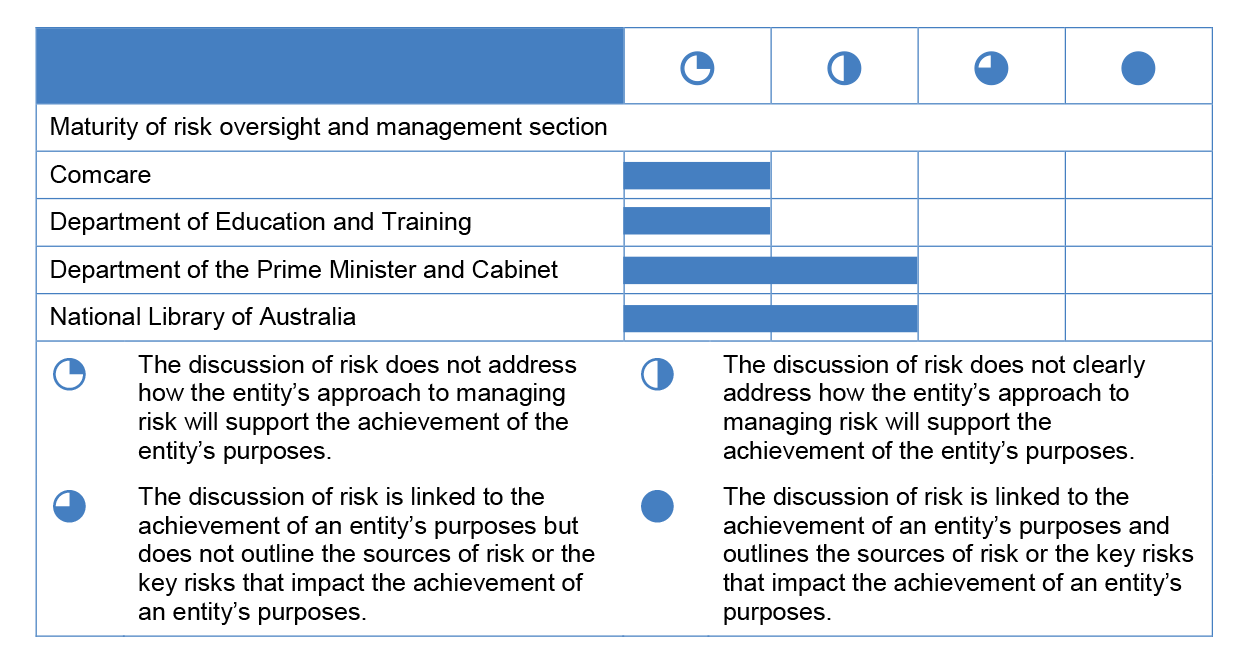

- Risk management and oversight—by outlining the key risks that impact the achievement of an entity’s purposes and explaining how its approach to managing risk will support the achievement of entity purposes (all entities).

2.27 Good performance is likely to result when the purposes of an entity are clear and senior leaders are able to organise resources and activities to deliver on these purposes. Finance guidance recognises that an entity’s Accountable Authority is responsible for developing and tailoring the corporate plan to suit the entity’s particular circumstances.

2.28 In addition to assessing compliance with the PGPA Rule, the ANAO assessed the maturity of each key mandatory section of the selected entities’ corporate plans, relating to: purposes, environment, performance, capability, and risk oversight and management. The material in these sections of the corporate plan should enable a reader to assess how an entity intends to achieve its purposes over the period of the plan.

Purposes

2.29 The PGPA Rule requires that the corporate plan include the purposes of the entity. The purposes of a Commonwealth entity are the strategic objectives that the entity intends to pursue over the reporting period. The aim of the purposes is to give context to the significant activities that the entity will pursue over the period covered by the plan. Clearly and concisely presenting purposes in entity corporate plans better allows a clear read through to results reported at the end of the reporting period through annual performance statements. The description of purposes and activities in the corporate plan forms the foundation on which to develop performance information and tell a meaningful performance story. Meaningful performance information depends on having a clear understanding of the purpose to be fulfilled, and expressing that understanding in a way that is measurable. A well-expressed purpose states the outcome that an entity seeks to achieve for clients, stakeholders and the public.

2.30 Finance provides guidance to entities on the wording of purposes and also provides tips for developing a common understanding of purpose as outlined in Table 2.1 and Example 2.2 respectively.

Table 2.1: Example of entity purpose in Finance guidance

|

Provide support to regional industry

|

Encourage further investment in regional areas that leads to generation of new jobs

|

|

Defending Australia

|

Develop and sustain military capability that meets the government’s strategic and operational needs

|

|

Improve health services for people with serious and life-threatening illnesses

|

Reduce mortality rates for people with serious and life-threatening illnesses

|

| |

|

Source: Department of Finance, Resource Management Guide No. 131 Developing good performance information, April 2015, p. 15.

|

Discussing the following questions extensively internally as well as with delivery partners and key external stakeholders, will assist in establishing a clear and coherent understanding of the purpose (or purposes) to be fulfilled:

- What need is being met? What is the government’s role in meeting that need?

- How will things be different when the need is met, and for whom?

- Who should be involved in making this difference? How long will it take?

- How can this difference be achieved effectively at the lowest cost?

- When will stakeholders know a significant difference has been made? What will be observed to have changed?

|

Source: Department of Finance, Resource Management Guide No. 131, Developing good performance information April 2015, p. 16.

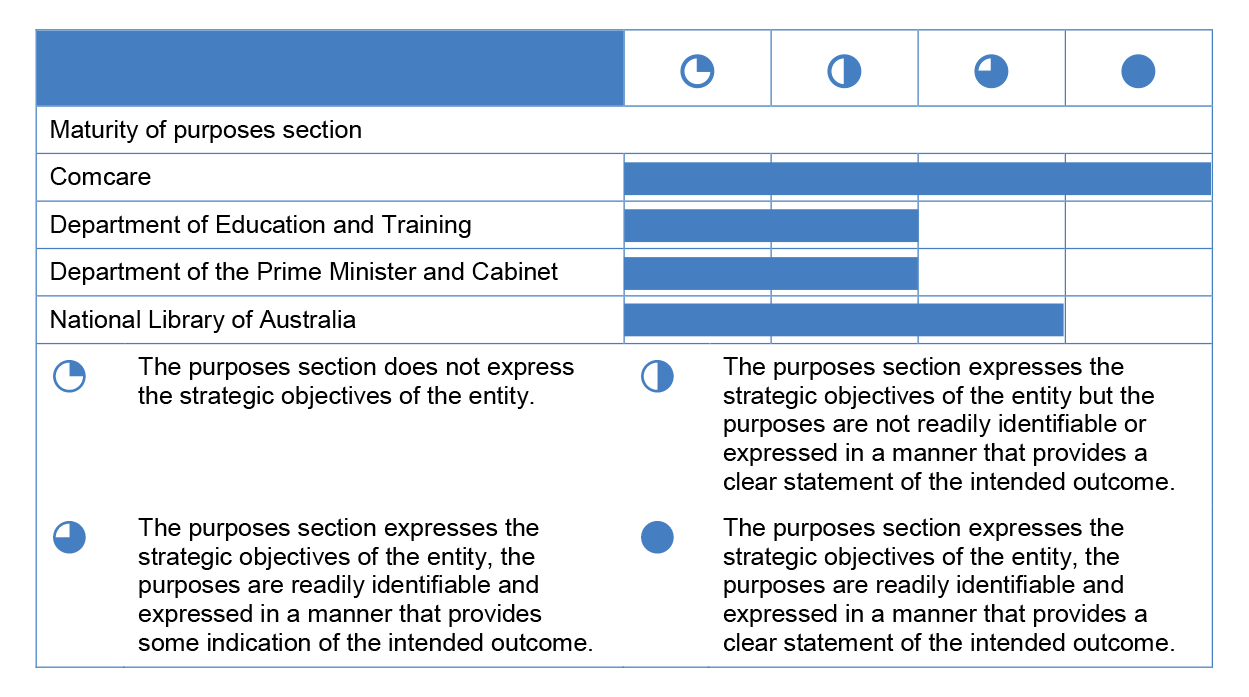

2.31 The ANAO’s assessment of the maturity of the purposes section of the selected entities’ corporate plans (2016–17 planning cycle) is presented in Figure 2.3.

Figure 2.3: Assessment of the maturity of the purposes section of corporate plans (2016–17 planning cycle)

Source: ANAO analysis.

2.32 Each of the selected entities expressed their strategic objectives in the purposes section of their 2016–17 corporate plan and provided context for the entity’s activities.

2.33 Comcare clearly and concisely identified its four purposes in its corporate plan and the outcome to be achieved when the purposes are fulfilled.

2.34 In Education’s corporate plan the section headed ‘Purpose’ presents the department’s vision, mission, outcomes, goals, values and culture, discusses that Indigenous business is everyone’s business, and includes a diagram titled ‘why are we here?’ Collectively this information provides readers with information regarding the strategic objectives of the department. Education’s purpose is not readily identifiable leaving it to the reader to interpret what the purposes are. The absence of a readily identifiable purpose makes it more difficult for Education to develop performance criteria that will demonstrate that it has made progress towards fulfilling its purpose.

2.35 The NLA’s purpose is readily identifiable and gives some indication of the intended outcome. The purpose could be expressed in a manner that more clearly states the outcome to be achieved when the purposes are fulfilled.

2.36 PM&C’s corporate plan identifies three key purposes: supporting the Prime Minister as the head of the Australian Government and the Chair of Cabinet; providing advice on major domestic policy and national security matters; and improving the lives of Indigenous Australians. The first two purposes are expressed as actions or activities rather than as an outcome or result to be achieved. It is also not clear what change will occur as a result of activities undertaken by the department. PM&C’s third purpose gives some indication of the desired outcome (improvement in the lives of Indigenous Australians). The reader’s understanding of the link between PM&C’s purposes and intended outcomes is improved by reading the purposes together with the Secretary’s covering statement.

Environment

2.37 The PGPA Rule (section 16E) requires the corporate plan to describe the environment in which the entity will operate for each reporting period covered by the plan. The environment section may provide an explanation of the nature and intricacies of the environment in which the entity operates. This could include demographic, geographic or temporal factors that affect the entity and its work, and the regulatory or competitive environment in which it operates.

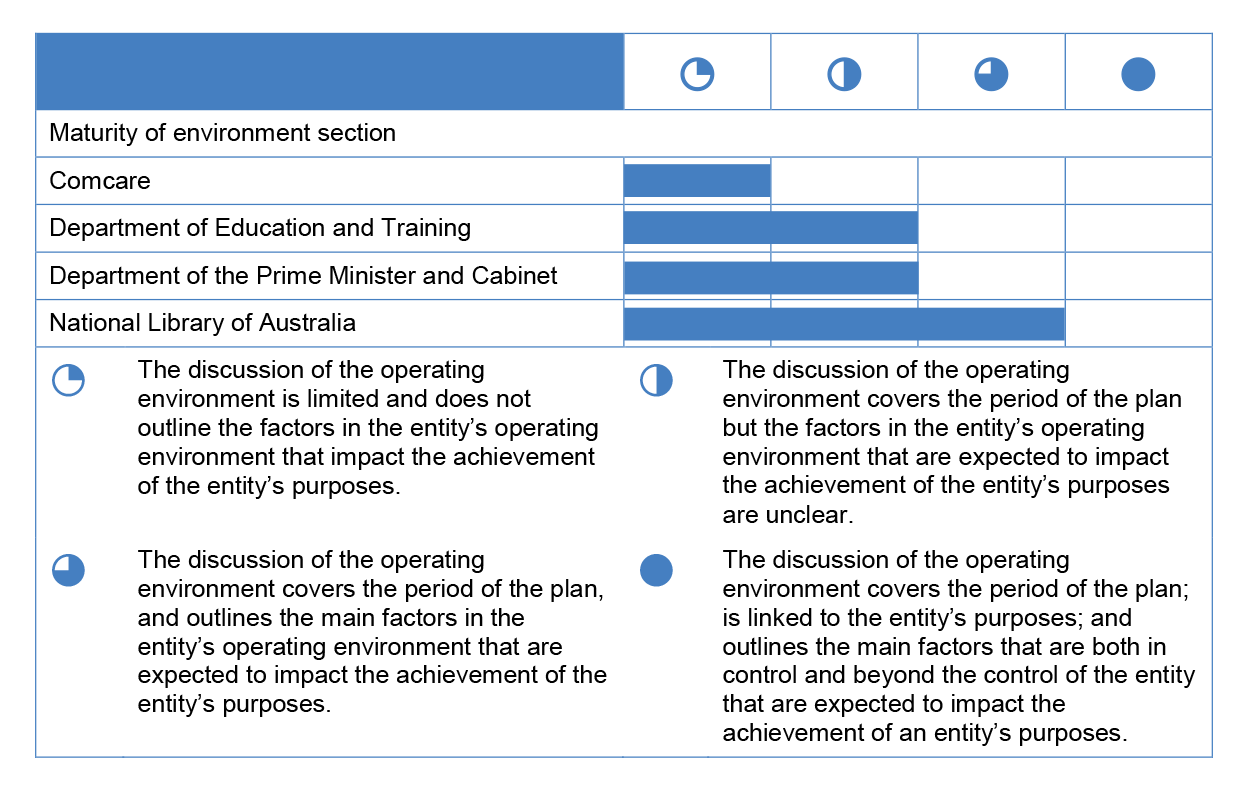

2.38 The ANAO’s assessment of the maturity of the environment section of the selected entities’ corporate plans (2016–17 planning cycle) is presented in Figure 2.4.

Figure 2.4: Assessment of the maturity of the environment section of corporate plans (2016–17 planning cycle)

Source: ANAO analysis.

2.39 In most cases, entities’ description of the environment in which they will operate for each reporting period covered by the plan lacked specificity. Entities referred to factors such as global, national, social and economic factors, changes in technology or other challenges, many of which are common to the operating environment of most entities in the Australian public sector. The breadth of these environmental factors limited entities’ capacity to describe how specific changes in their operating environment may impact the entity’s achievement of its purposes.

2.40 Specifying how environmental factors, both within and outside the control of the entity, are likely to impact on an entity’s capacity to achieve its purposes would strengthen this section of entities’ corporate plans. Finance guidance also suggests where environmental factors relate to the risks faced by entities, identification of these factors makes for a ‘clear read’ between the environment, capability and the risk oversight and management sections of entity corporate plans and is encouraged.

2.41 The NLA’s environment section provides an explanation of the nature and intricacies of the entity’s operating environment and outlines the main factors in the entity’s operating environment that are expected to impact the achievement of the entity’s purposes.

|

The environment section of the NLA’s 2016–20 corporate plan provides a description of the environment in which it operates, how the environment is changing, and how the environment impacts the Library’s capacity to achieve its purposes.

In particular, the corporate plan discusses the changing needs and demands of the NLA’s client base, including the growing demand for digital access to the collection, the decline in hard copy publishing and increase in digital publishing, and systems and processes put in place to meet this emerging and growing demand.

Resourcing is discussed and the plan provides an example of where resourcing will require the NLA to focus on critical, very high impact projects only.

The ‘Our Partners’ subsection provides an understanding of how and why the NLA collaborates with its equivalents in the states and territories, and other cultural, community and philanthropic partners.

The ‘Government Framework’ subsection discusses opportunities and challenges inherent in the broader government framework and how the NLA will engage with, contribute to, and become embedded in this framework.

|

Source: ANAO summary of NLA corporate plan environment section.

Performance

2.42 The PGPA Rule (section 16E) requires that for each reporting period covered by the corporate plan, the entity must provide a summary of how the entity will achieve its purposes, and how the entity’s performance will be measured and assessed. The summary must include any measures, targets and assessments that will subsequently be used to measure and assess the entity’s performance in the entity’s annual performance statements prepared under section 16F of the PGPA Rule. Finance has advised entities that performance information should convey a coherent message and tell a rich and meaningful story about what will be achieved over the periods of the plan.

A good performance story answers the following questions:

2.43 Finance has further advised that a small set of relevant and high-quality performance measures that generate information, and tell a coherent story about the achievements of activities directed at satisfying a specific purpose, will always be preferred over larger amounts of poorly focused and messaged performance information.

2.44 The ANAO’s assessment of the maturity of the performance section of the selected entities’ corporate plans (2016–17 planning cycle) is presented in Figure 2.5.

Figure 2.5: Assessment of the maturity of the performance section of corporate plans (2016–17 planning cycle)

Note: The audit did not include a detailed assessment of the appropriateness of the performance measures included in entity plans.

Source: ANAO analysis.

2.45 Three of the selected entities included performance measures in their corporate plans. The measures were predominantly quantitative, output based, and simple in nature. Outcome measures and targets were infrequently specified.

2.46 The NLA’s corporate plan did not indicate how the entity intended to measure and assess its performance in achieving its purposes. During 2015–16, the NLA completed a major review of its performance indicators and commenced work on developing a new reporting framework to better position itself to meet the requirements of the PGPA Act. The NLA has now endorsed ten entity level performance measures and the NLA advised the ANAO that these will be incorporated in the next corporate plan (2017–18 planning cycle).

2.47 Each of the selected entities recognised that there is scope for improvement in relation to the presentation of performance information, and all have taken steps to improve performance measurement since the publication of their last corporate plan in August 2016. Key areas of focus should include:

- Progressively implementing more sophisticated performance measures to assess performance in achieving entity purposes. This includes transitioning from the measures currently in place, that largely tell a performance story of what was delivered, to measures that also provide information on effectiveness in achieving purposes.

- The inclusion of material that enhances the overall performance story, such as qualitative measures, case studies and other narrative material.

- The inclusion of information on how performance will be assessed, including how often performance information is collected.

Capability

2.48 The PGPA Rule states that the corporate plan must include the key strategies and plans that the entity will implement in each reporting period covered by the plan to achieve the purposes of the entity. Entities may describe their current capability and assess how their capability needs may change over the term of the corporate plan. They may also outline the strategies they will put in place to build the capability they need in areas such as (but not limited to) staffing, capital investment or ICT.

2.49 The ANAO’s assessment of the maturity of the capability section of the selected entities’ corporate plans (2016–17 planning cycle) is presented in Figure 2.6.

Figure 2.6: Assessment of the maturity of the capability section of corporate plans (2016–17 planning cycle)

Source: ANAO analysis.

2.50 None of the selected entities addressed the key strategies and plans to be implemented to achieve the entity’s purposes. Much of the discussion on capability in entities’ corporate plans was expressed in generic terms that could apply to most entities in the Australian public sector. For example, entities outlined the need for relevant skills (such as leadership and policy analysis) and/or ICT capability (such as data analytics and the management of digital transformation). The plans did not clearly identify the specific capabilities required by entities to achieve their purposes and the key strategies the entity will implement to obtain those capabilities.

2.51 The capability sections of corporate plans would be enhanced if entities included:

- details of existing and future capability requirements;

- how capability requirements might change over time; and

- how entities plan to obtain or build the necessary capabilities to enable them to achieve their purposes.

Risk oversight and management

2.52 The PGPA Rule requires corporate plans to include a summary of the risk oversight and management systems of the entity for each reporting period covered by the plan (including any measures that will be implemented to ensure compliance with the finance law). The applicable Finance guidance noted that:

As a strategic planning document, the corporate plan needs to demonstrate that effective systems of risk oversight and management have been implemented. Entities should explain how their approach to managing risk will support the achievement of their purposes.

2.53 The ANAO’s assessment of the maturity of the risk oversight and management section of the selected entities’ corporate plans (2016–17 planning cycle) is presented in Figure 2.7.

Figure 2.7: Assessment of the maturity of the risk oversight and management section of corporate plans (2016–17 planning cycle)

Note: The audit did not include a detailed assessment of entities’ approach to managing risk.

Source: ANAO analysis.

2.54 The risk oversight and management section of the selected entities’ corporate plans did not identify risks specific to the delivery of the entities’ purposes. The risk discussion was generic and at a high level. Two of the selected entities (Comcare and Education) did not address how the entity’s approach to managing risk supported the achievement of the entity’s purposes.

2.55 Finance’s July 2016 guidance indicated that a mature approach to addressing risk in the corporate plan may include a discussion of:

… how the key sources of risk to an entity’s purposes are being managed in the context in which the entity operates, the activities undertaken and the purposes the entity seeks to achieve.

… the capability and environment components of the corporate plan, and how those components impact the risk profile of the entity.

… key sources of emerging risks that may impact its ability to achieve its purposes in the future.

… the risks an entity faces into the context in which the entity operates, the activities undertaken and the purposes it seeks to achieve.

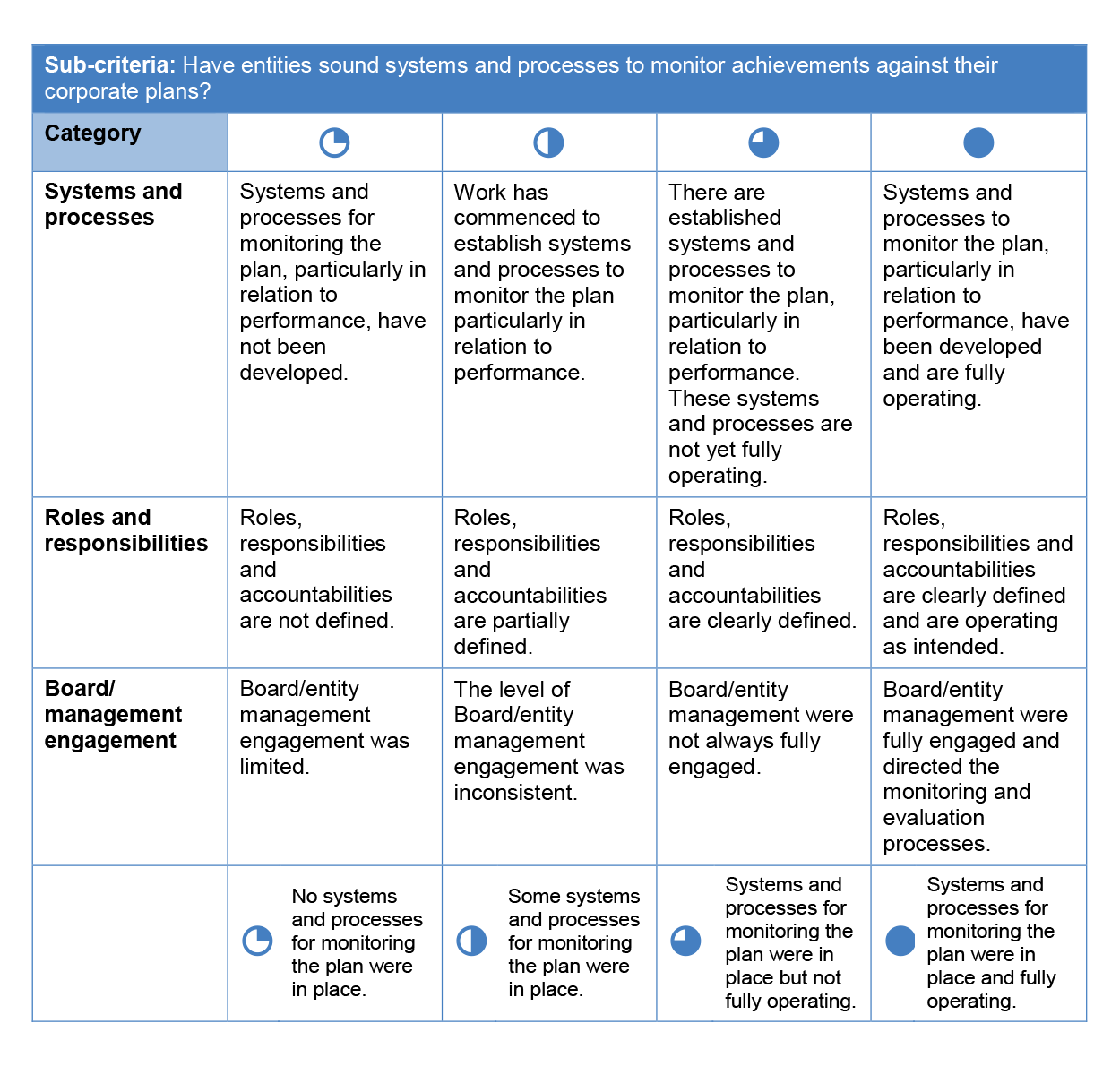

Did entities develop sound systems and processes for monitoring achievements against their corporate plan?

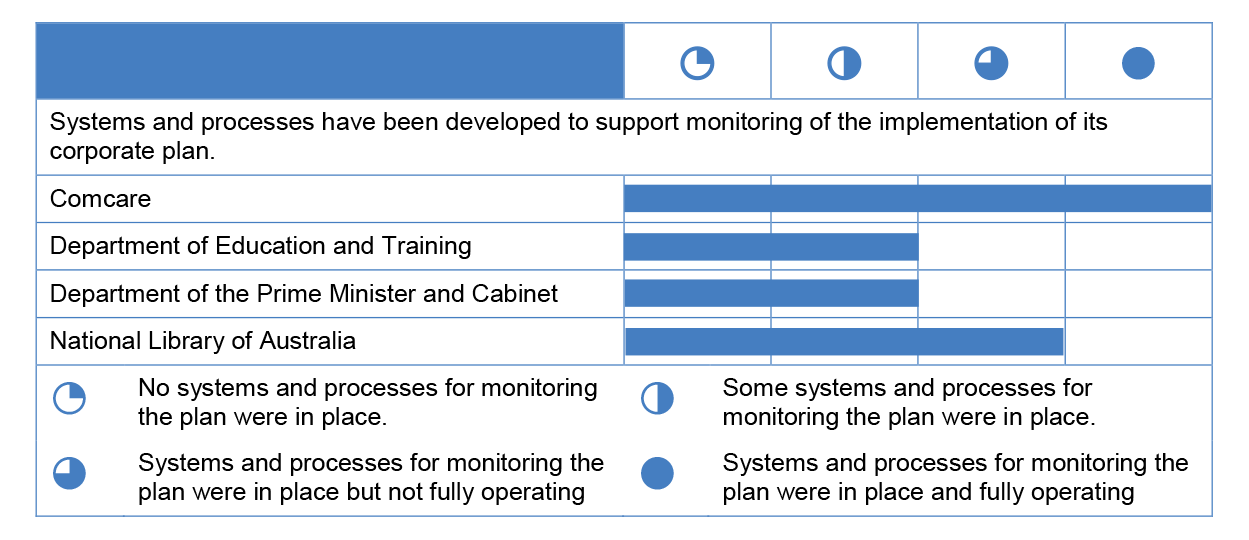

The systems and processes established by entities for monitoring and reporting on achievements against corporate plans were at different levels of maturity. Comcare and the NLA had developed systems and processes to monitor the plan and report periodically to their senior management and Accountable Authority. In Education and PM&C work has commenced to enhance the systems and processes used to monitor implementation of the plan and report on progress to the executive.

Roles, responsibilities and accountabilities for monitoring and reporting on the corporate plan were not clearly defined by the selected entities.

There is scope for improvement in respect to:

- the frequency of monitoring and reporting against the corporate plan, to establish it as the primary planning document and more effectively support senior management (Education and PM&C); and

- clarity of roles, responsibilities and accountabilities for monitoring and reporting (all entities).

2.56 The corporate plan is intended to be the primary planning document of an entity and represents the beginning of the annual performance cycle. An annual performance statement closes the performance cycle and is intended to provide an assessment of the extent to which an entity has succeeded in achieving its purposes, as outlined in its corporate plan. It is therefore important that entities establish arrangements for monitoring and reporting on progress in achieving the measures and other commitments included in the corporate plan.

2.57 In reviewing the arrangements adopted by entities to monitor the implementation of their corporate plans, the ANAO considered whether entities:

- developed systems and processes to monitor their plans, particularly in relation to performance;

- established clearly defined roles, responsibilities and accountabilities; and

- had fully engaged their senior management and/or Board.

2.58 The ANAO’s overall assessment of the maturity of the systems and processes adopted by the selected entities to monitor achievements against their corporate plans (2016–17 planning cycle) is presented in Figure 2.8.

Figure 2.8: Assessment of the maturity of entity systems and processes to support the monitoring of corporate plans (2016–17 planning cycle)

Source: ANAO analysis.

2.59 The ANAO’s assessment indicates that the systems and processes established by entities for monitoring and reporting on achievements against corporate plans were at different levels of maturity.

2.60 Comcare and the NLA had developed systems and processes to monitor the plan, particularly in relation to performance. Comcare’s arrangements were fully operating for the duration of the plan, while NLA’s were fully operating from January 2017.

2.61 Roles, responsibilities and accountabilities for monitoring and reporting on the corporate plan were not clearly defined by each of the selected entities.

2.62 Periodic reporting to senior management and the board, where relevant, of progress in achieving the measures and other commitments outlined in the entity’s corporate plan is a demonstration of an entity’s commitment to positioning the corporate plan as the entity’s primary planning document.

2.63 Comcare reports to its senior executive, while the NLA reports to its Director-General and Council on progress against indicators outlined in the corporate plan.

2.64 In Education and PM&C work has commenced to enhance the systems and processes used to monitor implementation of the plan and report on progress to the executive.

Example of good practice

2.65 The following example of good practice was observed during the ANAO’s review of entity processes for monitoring achievements against the corporate plan.

Reporting to the senior executive

|

Comcare provides a quarterly non-financial performance report to its senior executive that lists each of the performance indicators in the corporate plan and reports results against them by quarter.a The report also identifies the target that was included in the corporate plan and indicates whether operational plan delivery strategiesb are on track, at risk (minor issues), have major issues, are on hold or complete.

|

Note a: In some cases no results are provided as the results are not yet available or data was not collected every quarter.

Note b: Comcare’s Operational Plan is a subsidiary document closely aligned to the corporate plan.

Source: Comcare documentation.

Opportunities for improvement in relation to monitoring achievements against the plan

2.66 There remains scope for entities to strengthen the systems and processes used to monitor achievements against the plan. This includes:

- developing systems and processes to monitor the plan particularly in relation to performance, and ensure these systems and processes are operating as intended;

- clearly defining roles, responsibilities and accountabilities for monitoring the implementation of the plan; and

- fully engaging senior management in directing the monitoring and evaluation process.