Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 59 of 2003–04

Defence's Project Bushranger: Acquisition of Infantry Mobility Vehicles

Published

Wednesday 30 June 2004

Portfolio

Defence

Entity

Department of Defence

Sector

Defence

The objective of this audit was to provide an independent assurance on the effectiveness of Defence's management of the acqusition of armoured infantry mobility vehicles (IMV) for the Australian Defence Force (ADF). The audit sought to identify the initial capability requirements; analyse the tendering and evaluation process; and examine the management of the project by Defence. As such, this was not an audit of contractor performance, but of the formation and contract management of the aquisition project by Defence.

Summary

Background

In order to protect important civilian and military assets and infrastructure, Defence identified the need to mobilise the infantry through the procurement of both unprotected and protected vehicles. The initial phase of the project procured 268 unprotected Land Rover vehicles and 25 support vehicles, delivered in service by mid 2000 at a project cost of $57.69 million, in order to cover the interim period until protected vehicles could be procured.

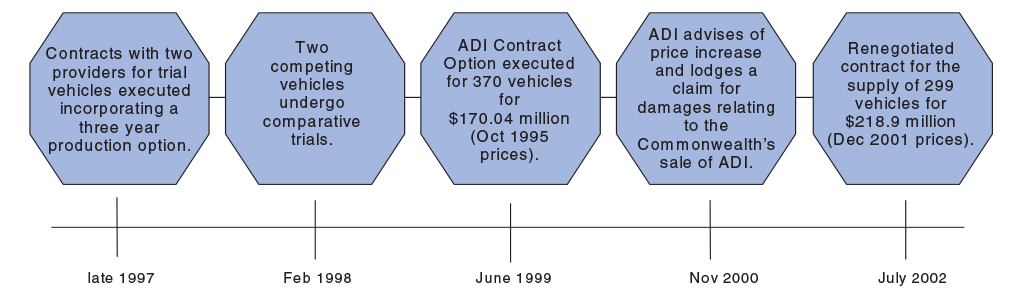

The second phase of Project Bushranger involved the trial and evaluation of protected vehicles by the then Defence Acquisition Organisation (DAO), for an approved cost of $11.6 million. Requests for Tender (RFT) were issued in September 1995, and trial vehicle contracts were signed with ADI Limited (ADI) for the Bushmaster vehicle, and Australian Specialised Vehicle Systems (ASVS) for the Taipan vehicle, in late 1997. The trial vehicle contracts included an option for full-scale production (see Figure 1).

In late 1998, Defence undertook comparative trials of the two tendering vehicles. Neither vehicle fully met all of the requirements of the specification, and performed with varying success over the course of the trials. The ADI Bushmaster vehicle was selected as the preferred vehicle in March 1999. The third phase of the project is the full rate production of the protected vehicles. The Production Contract Option was executed on 1 June 1999 with ADI, for the supply of 370 Bushmaster vehicles by December 2002. Shortly after the Production Option was exercised, a range of problems emerged with design enhancements, cost, and schedule slippage in the contract, leading to renegotiation of the Contract in July 2002 for 299 vehicles.

Figure 1: Contractual Acquisition of Bushmaster Vehicles

Source: ANAO analysis of Defence documentation.

The performance characteristics of Project Bushranger vehicles were to be optimised to, among other things, provide opportunities for Australian Industry Involvement (AII), including manufacture and through-life support (TLS). The approval documentation highlighted some of the risks associated with the design and development of an Australian vehicle. The target for AII in Project Bushranger was stipulated within the original 1999 Contract as around 70 per cent. Currently 68 per cent is being achieved. Defence advised ANAO that, at the time of audit, ADI was on track to meet the AII amount specified in the contract.

Defence advised ANAO in April 2004 that:

The Bushmaster Infantry Mobility Vehicle has been designed, developed and built in Australia by ADI Limited to meet a niche requirement of Australian forces. The vehicle is a world class design and has integral protection levels unparalleled by any comparable vehicle in operation anywhere in the world today; the Bushmaster protects against anti-vehicular and anti-personnel blast mines, mortar splinters and small arms ammunition. The Bushmaster has been designed to provide exceptional mobility to Australian forces and carries three days supplies for extended operations. The vehicles range is between 600-800 km dependent on terrain. There has been significant international interest in the capability, which has seen ADI and the Commonwealth work towards developing mutually supportive strategies to meet this demand.

The trial and initial production contract management for the project were undertaken by the DAO. In 2000, the DAO was merged to form the Defence Materiel Organisation (DMO). In mid 2002, Project Bushranger staff relocated from Canberra to Melbourne after the major changes to the contract were completed.

Audit Approach

The objective of the audit was to provide an independent assurance on the effectiveness of Defence's management of the acquisition of armoured infantry mobility vehicles (IMV) for the Australian Defence Force (ADF). The audit sought to identify the initial capability requirements; analyse the tendering and evaluation process; and examine the management of the project by Defence. As such, this was not an audit of contractor performance, but of the formation and contract management of the acquisition project by Defence.

Key findings

Formation of the Contract (Chapter 2)

Whilst initial Defence requirements provided for a number of infantry mobility solutions, it was generally considered by Defence that a modest lightly armoured vehicle with commercial truck components was to be procured. During the course of the project the number of battalions to be equipped has been reduced from eight to two. The vehicle ultimately procured by Defence was largely of an unproven design and capability, and was far more developmental than originally intended. However, Defence initially managed the project as though it was a Commercial Off the Shelf (COTS) procurement, rather than recognising the developmental nature of the project.

In September 1996, the company which originally tendered for the Defence contract novated its tender to ADI. Although ADI had been assessed in the initial Invitation to Register Interest (ITR), there is no evidence that it was assessed in the context of providing the unproven Bushmaster vehicle.

The ANAO found that Defence had generally complied with relevant pre-project approval and post-project approval phases required of major capability acquisition projects. In selecting a preferred tenderer, a comprehensive Tender Evaluation Plan (TEP) was developed and the probity risk arising from the pending sale of ADI was specifically addressed. The Australian Government Solicitor (AGS), in the role of independent monitor, advised Defence that no conflict had arisen during the tender process relating to the sale of ADI.

On the basis of the Source Evaluation Report (SER), the Bushmaster vehicle was assessed as superior in performance and cost criteria. The ADI tender to supply 341 vehicles was assessed by the Tender Evaluation Board to cost $183.8 million in October 1995 prices. The actual Production Contract Option that the Commonwealth executed was for an additional 29 vehicles (an eight per cent increase in capability), yet cost seven per cent less than that outlined in the SER for fewer vehicles.

During contract negotiation, a number of rectification and enhancement issues identified during the trials were discussed. Defence documentation indicates that agreement was reached on all of the issues with ADI. However, prior to signing the Production Contract Option in June 1999 for $170.04 million (October 1995 prices), Defence did not formally amend the contract to take into account these rectifications. The likelihood of cost overruns by the contractor was considerable and recognised by Defence prior to contract signature. The oversight of incorporating the rectifications before executing this option, exposed the Commonwealth to considerable risk, in efforts to enforce contractual terms and seek delivery in accordance with the contract schedule.

An advance payment of 20 per cent of the contracted price was initially agreed to by Defence. However, after selection of preferred tenderer, and before contract execution, Defence increased the advance payment to ADI by a further five per cent to an estimated $42.5 million. The reason given by Defence was to assist Defence spend their Budget allocation in 1998-99. In reality, because of exchange rate movements, and the rates applied in the contract, this resulted in an additional payment of $0.711 million which equated to a 26 per cent advance payment being made to ADI.

The advance payment of $43.2 million was made to ADI in June 1999 (an additional $1.3 million was paid in 2000 for price variations). At that time there was no requirement for the contractor to use the advance payment for the actual milestones for which it was advanced. In this instance, Defence paid a significant amount of money to a contractor, in order to lessen budgetary pressures, yet received no identifiable benefit in return for the advance payment. Some years after the payment was made, the contractor still had not delivered the product in accordance with the initial contract.

Contract Management (Chapter 3)

Defence exercised the Production Contract Option 18 months before it was due to expire. The Department indicated that the timing of selection of preferred tenderer was to achieve contract signature in 1998-99, and to account for the timing of the sale of ADI. 1

The contract stipulated that full rate production of the vehicles would commence almost directly after the prototype vehicles had passed testing. These vehicles were fundamentally different to those tested during the original trials. The Production Contract and the Statement of Work (SOW) did not adequately reflect the changed nature of the project.

ANAO considers that the development and testing of prototypes is a sound approach for projects with material developmental components. However, Defence moved to contract signature and full production before development work was finalised. Defence did not have a system in place to adequately ensure that the project was technologically ready to move through to high rate production. Also, even with significant changes in the contract in 2002, the project was still hovering around technology readiness level seven in early 20042. This is a less than satisfactory outcome for a project that was scheduled to start production in February 2001 under the initial Production Contract.

Defence advised ANAO that the failure to start production in 2001 had nothing to do with technology readiness. Rather, it related to delays being caused by the time required to establish contractual conditions that were acceptable to both parties. This is indicative of an inherent deficiency in the framing of contract deliverables, which needed to be addressed prior to the exercising of the Production Contract Option.

The Commonwealth had a significant forward commitment, having already paid out $44.5 million in advance payments. This was before having a proven product capable of meeting demonstration standards, let alone full rate production of 15 vehicles per month.

After contract signature and before renegotiation, Defence continued to make changes to the required capability. Internal contract management process allows for changes to the contract, through Engineering Change Proposals (ECPs) and Contract Change Proposals (CCPs). Throughout the course of the project a number of changes were required. However, in some instances, the formal process of CCPs was not followed. For example, in October 1999 a number of rectification and enhancement issues were discussed with the contractor, including reducing vehicle numbers. However, no CCPs or ECPs were developed at that stage.

ADI is contractually bound to provide a number of reports and plans to Defence as part of their management of the project. These project monitoring and reporting tools are deliverables in the contract. Some have already been delivered to Defence and subsequently paid for. Payments made for non-vehicle deliverables, by early 2004, amounted to $8 million.3 Excluding the advance payment these comprise one-third of all payments made for contract deliverables. A number of these contract deliverables, with regard to the early stages of the project, were not kept in a complete and consolidated form by the Program Office.

Review of the Contract by DMO (Chapter 4)

Before going to full rate production of the IMVs, ADI was required to supply prototype vehicles in January 2000 for testing. ADI were some four months late in providing the vehicles, which were fundamentally different to those tested during trials. In November 2000, ADI lodged a claim against the Commonwealth, stating that the vehicle unit price had escalated, which would result in a total cost increase of $38 million. In addition, ADI lodged a further claim for $38 million against the Commonwealth, for non-disclosure of contract problems relating to the sale of ADI in 1999.

In the early phase of the contract, when it became apparent that the project was incurring difficulties, the Program Office informed senior Defence management and the Minister through a series of internal minutes. Over the course of contract renegotiation, the Program Office and the Department fully informed the Minister of issues and options available to the Government in respect of the contract. In December 2001, the Defence Capability and Investment Committee (DCIC) recommended to the Minister that the contract be terminated. Following the Minister's consideration, Defence sought to resolve concerns through negotiation rather than termination. The CCP negotiations addressed: vehicle numbers and performance; cost; termination exit costs; schedule; ADI Sale Claim; ADI key staff; advance payment; and performance securities; reliability testing; test and evaluation; risk; ADI contingency; and warranty.

The Minister was informed of the DCIC consideration of the CCP, which considered that they had been able to resolve all significant issues. Subsequently, the Department undertook to provide to the Minister with a paper highlighting costs for contract renegotiation, termination, and alternative capability options. Defence advised the Minister that, whilst termination had been discussed with ADI, it would be a high risk option for Defence. They continued to explore contract renegotiation.

Revised DMO Production Contract (Chapter 5)

During contract renegotiation, the cost of the contract with ADI increased to $218.9 million (December 2001 prices). This increase was made up of a combination of price supplementation from automatic updates of $6.6 million, and exchange and real price variations totalling $42.2 million. The Government agreed to a transfer of funds between various elements of the project, to ensure that the project budget did not increase. The cost of the project has remained constant in real terms at $295 million (December 1998 prices). 4

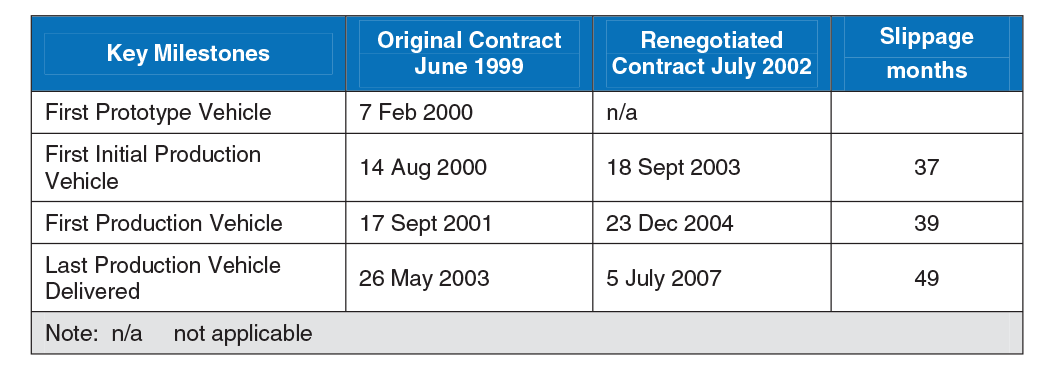

Timing of delivery of the last vehicle has been extended by 49 months compared with that of the original contract. The details of the slippage in the project schedule are outlined in Table 1.

Table 1: Revised Milestones for Original Contract and Renegotiated Contract

Source: Defence

Defence advised ANAO that, prior to signing the renegotiated contract, a number of improved management practices and procedures have been implemented, including: a selection of standard operating procedures; formalising the CCP and ECP process; weekly management discussion of contract deliverables; and engagement of legal specialists.

The renegotiated contract provides two exit points at which ADI must demonstrate that the IMVs meet required standards or face contract termination. These exit points are the Reliability Qualification Test (RQT) and the Production Reliability Acceptance Test (PRAT). The RQT is conducted to achieve a specified level of basic reliability and operational mission reliability. The PRAT assesses the reliability of three actual production vehicles delivered under the low rate initial production phase. The Minister for Defence announced, on 22 June 2004, that the vehicles had successfully passed the final stage of reliability tests. The contract provides that, in the event that ADI failed to pass either of the tests, the Commonwealth may have, at its sole discretion, terminated the contract. The Final Acceptance Test is due to be completed by the end of July 2004.

ANAO analysis of the advance payment, indicates that, by late July 2002 (just after the major contract amendment was finalised), only one per cent had been discharged from the advance payment in relation to contract deliverables. In effect, ADI has had the use of some $44 million of Commonwealth funds, interest free. ANAO has estimated the opportunity cost forgone by the Commonwealth, as at 30 June 2003, as a result of the advance payment made to ADI, and the delay in the contract being satisfied to amount to some $9 million. Defence has advised ANAO that, as at March 2004, some $2.37 million has been discharged from the advance payment. Further, the advance payment will not be fully consumed, and the advance payment security returned, until the last vehicle deliveries are made.

ADI advised ANAO in May 2004 that:

ADI has expended significantly more than it has recovered from its sales and would have a negative cashflow without advance funding.

As, to date, ADI has expended significantly more than it has recovered from its sales, the full amount of the advance payment is not available to ADI to recover interest from.

The report totally overlooks the point that ADI is not allowed to claim cost escalation on the proportion of the contract value covered by the advance funding. Cost escalation for the proportion of the contract value has to be provided for by interest received on the balance of any advance payments made.

Defence advised ANAO that offsetting the foregone interest of the advance payment has been a large cost saving to Defence, associated with a delayed introduction into service of the capability. The ANAO considers the quantum of the advance payment, resulted in a significant shifting in fiscal advantage to the contractor at the expense of the Commonwealth. The characterisation of delays in delivery as a cost saving to Defence budgeting position, merely increases the size of the cost to future Defence budgets, and delays the capability to the ADF.

When Defence is entitled to claim liquidated damages, the amount is considered a debt owed to the Commonwealth under section 47 of the Financial Management and Accountability Act (FMA Act) 1997. Under this section, an agency must pursue recovery of each debt for which it is responsible, unless: the debt has been written off; or the Chief Executive is satisfied that the debt is not legally recoverable; or he/she considers that it is not economical to pursue recovery of the debt.

The calculation of the potential liquidated damages, claimable by Defence for delay in receiving the identified items of supply, amounted to some $28 million by mid 2002. Due to the capping of damages within the contract, and complexities associated with whether they could be claimed, the maximum amount of damages that could have been claimed by Defence amounted to some $6.8 million. The ANAO found no documented evidence that Defence considered pursuing the debt arising from liquidated damages, when they became available.

Overall audit conclusion

This legacy procurement project incorporated minimal incentives for effective contractor performance. The large advance payment made by Defence, combined with systematic scope creep in the initial stages of the contract, resulted in a minor transference of contractual risk. Accordingly, the project was initially characterised by unwelcome surprises surrounding cost, time, schedule, performance and the risk of litigation.

The ANAO found that, despite the project having a lengthy demonstration phase, the requirement definition had not been fully developed at the time the Production Option was exercised. The outcome of this, combined with overly optimistic projections on deliverables, has been a nominal vehicle unit cost increase of 39 per cent, a forecast slippage of 49 months in delivery, and the need for Defence to commit significant management resources to turn around this project.

Significant under achievement in performance occurred in the initial contract on unit cost, delivery schedule and recoverability, which arose from a combination of Defence transference of capability and overly optimistic timeframes. Defence has managed the overall cost increase associated with the contract renegotiation within the approved project budget. This has been achieved by decreasing capability through the reduction of the number of vehicles by one-fifth, and reducing requirements, such as those relating to systems engineering funding, which has decreased by 93 per cent. Further, the ability of the vehicles to self-recover has been diminished, through the reduction of the number of vehicle winches.

The ANAO found that a large amount of administrative effort has been expended throughout this project, in order to fix problems which may not have occurred, with better management of the planning and implementation phases of the project. In 2002, Defence renegotiated the contract with ADI involving a reduction in contractual conditions, an increase in contract price, and a four year extension of delivery time. The renegotiation also saw the capability of the individual vehicles drop from that originally contracted of 370, down to 299. Defence maintains that the capability which they will receive is superior to that originally contracted and that, despite the problems in the past, Project Bushranger is now seen as a model project.

The ANAO considers that the renegotiated contract, signed in July 2002, has provided a generally improved framework for Defence to progress the project to completion. In the development of the renegotiated contract, Defence escalated issues as they arose, effectively, with Ministers, fully informing them of the various options, including recommending termination of the original production contract. The less than effective collaborative contract management approach, adopted with the contractor during the initial phase of the Production Contract, has now been replaced by one that is more commercially oriented. The Program Office's initial deficiency in contract management has now been addressed within the Office by:

- strengthening control over user requirements to prevent scope creep which contributes to slippage in time and cost schedules;

- elevating contractual problems effectively with the contractor and with senior Defence management;

- managing the contract in accordance with the terms of the contract;

- managing the contractual performance, using reports provided by the contractor; and

- providing and retaining appropriate records of dealings with the contractor that protects the Commonwealth's commercial interests.

Response to the report

The ANAO made seven recommendations directed towards the improvement of Defence's project and contract management. Defence agreed with all recommendations.

Footnotes

1 On 17 August 1999 Transfield Thomson – CSF Investments Pty Limited was selected as preferred buyer of the Commonwealth's shares in ADI. The Commonwealth announced in July 1997 that the Office of Asset Sales and IT Outsourcing was to commence the sale process of ADI. Final settlement occurred on 29 November 1999 and the gazetted price was $346.78 million.

2 Technology readiness level seven is described as: system technology prototype demonstration in an operational environment. Technology readiness level eight is described as: system technology qualified through test and demonstration.

3 ADI informed ANAO that these non-vehicle deliverables included: Joint Design Reviews; Reliability and First Article Testing; Maintenance and Support Analyses; Maintenance and Support Handbooks; Driver and Maintainer Training Packages; and Support and Test Equipment.

4 At December 2001 this represented a project cost of $323.18 million.