Background

1. The conversion of broadcasting from analogue to digital transmission marks a significant shift in Australia's communications technology. The advantages of digital television broadcasting include improved sound and picture quality and more efficient use of the spectrum, which allows multiple channels to be broadcast simultaneously (multi-channelling).

2. In 1997 and again in 1999, the Government decided to provide financial assistance to the national broadcasters—the Australian Broadcasting Corporation (ABC) and Special Broadcasting Service Corporation (SBS)—to assist in their conversion to digital broadcasting. The Phase 1 and 2 Strategies separately developed by each broadcaster provided the basis for the government's funding for capital equipment and transmission and distribution services.

3. The conversion to digital broadcasting projects began in late 1997 and have been, arguably, the largest and most complex capital equipment projects ever undertaken by the national broadcasters. It required them to replace analogue equipment with digital equipment and procure digital transmission and distribution services to meet fixed legislative digital broadcasting timeframes. This had to occur at a time when digital broadcasting technology was embryonic but evolving rapidly. The project involved many key staff of the broadcasters undertaking digital conversion on top of their normal duties.

4. The overall objective of the Australian National Audit Office (ANAO) audit was to determine the efficiency and effectiveness of the conversion to digital broadcasting by the national broadcasters. This encompasses, among other things, addressing the request from the former Minister for Communications, Information Technology and the Arts (the Minister) for an audit of the actual cost of digital conversion, the sources of funds applied and the efficiency of funds utilisation. It also involved an examination of the broadcasters' management processes to deliver their Strategies and to ‘minimise the call on the Budget'.

Overall audit conclusion

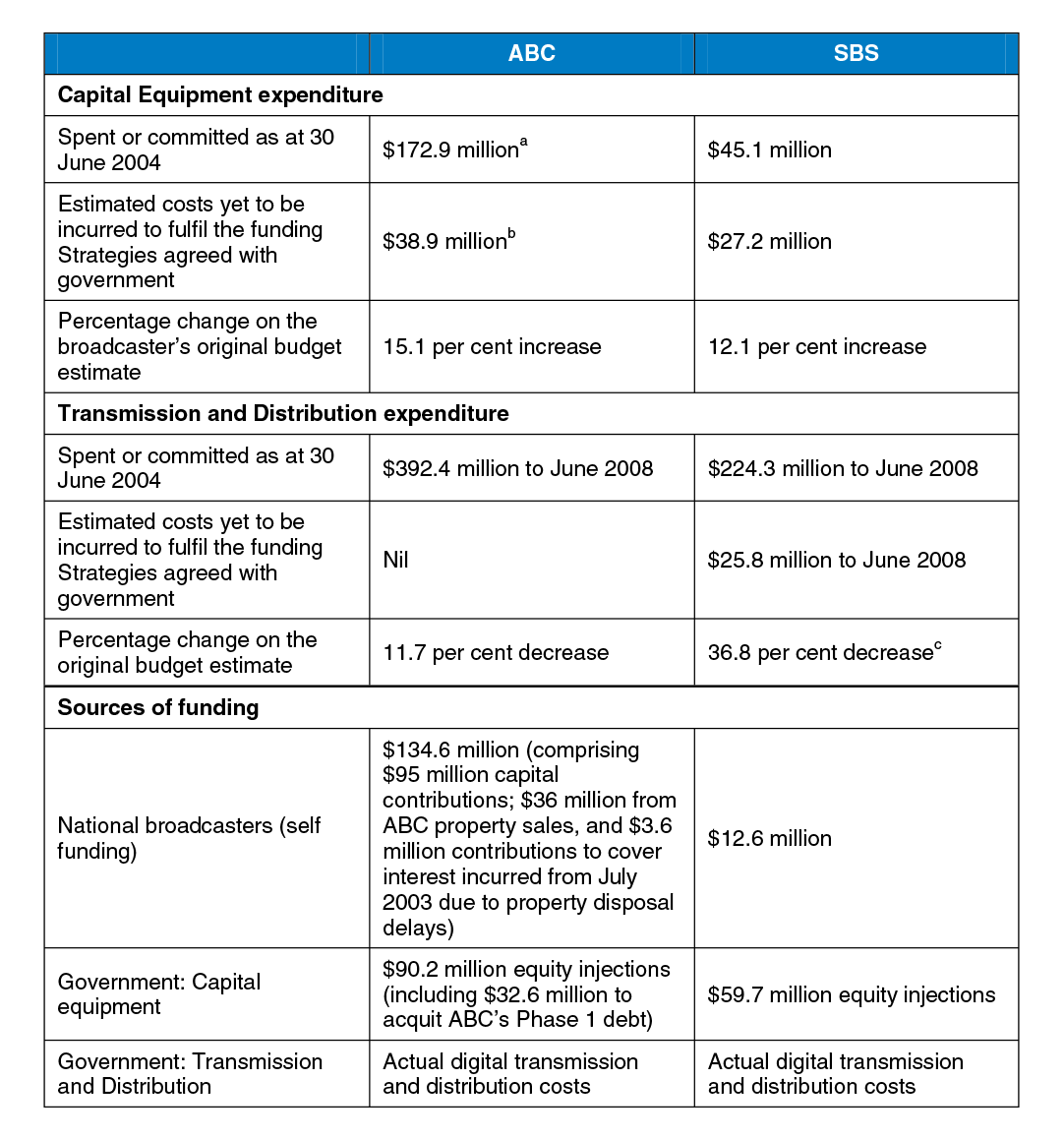

5. The ANAO concludes that the national broadcasters' staff did a commendable job to determine related needs; procure, install and commission the equipment; and successfully negotiate the transmission and distribution contracts. The ANAO notes that the national broadcasters met the legislative deadlines for starting digital broadcasting, without on-air interruptions to analogue broadcasting. Both national broadcasters consider that the new technology has notably increased the quality and timeliness of their broadcast material. It has also led to some work practice changes that have increased the efficiency of content production.

6. In addressing the request for an audit from the former Minister, the ANAO found that digital conversion expenditure to June 2004 and the sources of funding applied are as outlined in Table 1. In addition, both national broadcasters are undertaking digital conversion efficiently in implementing the Strategies, primarily due to the value for money obtained on individual pieces of equipment and the thorough processes followed to procure digital transmission and distribution services.

7. Although, the national broadcasters are achieving the objectives of their digital conversion Strategies, the ANAO noted improvements that could be made to their project management approaches and the maintenance of appropriate documentation, particularly for SBS. More often than not, a sound project management process is likely to lead to good results. A well-documented process demonstrates adequate consideration and management of project risks and improves the transparency of decision-making. In addition, it enhances management's accountability to internal stakeholders (the Board) and external stakeholders (including the Minister and the Parliament). The process also provides a sound basis for evaluating the project's success or otherwise, and for learning lessons for future projects.

8. The ANAO found that both national broadcaster's digital conversion projects at times were affected by:

- a lack of the applied formal project management methodologies; and

- shortcomings in, or the lack of adequate documentation evidencing, budgetary management and the monitoring of the achievement of the objectives of the various Strategies.

The ANAO acknowledges the steps taken by the ABC and SBS to implement better practice project management methodologies in the latter stages of their projects. The areas for improvement and other related issues are discussed in the Key Findings below.

9. Digital conversion, as outlined in the Phase 1 and 2 Strategies, was not intended to convert all of the national broadcasters' old analogue equipment to their digital counterparts—only a significant proportion. Both the ABC and SBS have indicated that long-term strategic capital planning is currently underway. The ANAO endorses this action, noting that the national broadcasters have recently reassessed their digital equipment needs to fully implement the Strategies. Strategic capital planning will assist them to determine their capacity to fund and manage their total equipment needs for the future.

Table 1: Digital conversion expenditure and sources of funding as at June 2004

Source: ANAO analysis 2004.

a Does not include $11.9 million in interest expense incurred to June 2004 from the agreement with Government to fund the ABC's Phase 1 debt.

b Does not include $1.1 million in interest expense estimated to be incurred from July 2004 until property rationalisations are completed. Includes scope increases of approximately $8 million

c The ANAO considers that the majority of the saving reflects the scaling back of the number of digital services SBS planned to roll-out.

Key Findings

Procurement of digital equipment (Chapter 2)

Project management

10. The progress of the national broadcasters' digital conversion has meant that both the ABC and SBS have successfully met legislated timeframes for digital broadcasting. However, the ANAO found little documentary evidence to suggest that the national broadcasters applied any formal, comprehensive ‘whole-of-project' management to digital conversion in the early stages of their projects.

11. Until the ABC's formal project management began to improve from mid-2002, the ABC's departure from project management better practice had the potential to adversely impact the smooth implementation of its project. The departures included the areas of high-level needs assessment, budget management, risk management and monitoring the achievement of the Strategies. However, the ANAO considers that the competency of the many ABC sub-project managers involved in the digital equipment solutions mitigated many of the impacts of the ABC's departure from project management better practice (see Procurement).

12. At SBS, the ANAO noted a general lack of project management documentation that would normally be expected for a project of the size and complexity of digital conversion. This is most notably in the same areas listed in the preceding paragraph that apply to the ABC, with the additional area of SBS changing/refining the original scope of the digital conversion project without the Minister's or DCITA's knowledge (see Needs Assessment). SBS considers that its project management has been thorough, but concedes that it was not documented as well as it could have been. The ANAO considers that the competency of the key members of SBS's small project management team mitigated, for the most part, the risk of misunderstandings within the project team arising from little or no documentation.

13. The ANAO observes that the ABC began implementing formal project management methodologies that are consistent with better practice from April 2002, and SBS from early–mid 2004. This should allow the national broadcasters to better manage future projects of the size and complexity of digital conversion and to better address any external accountability requirements.

Risk management

14. The national broadcasters have adequately managed most of the risks evident at the component/sub-project level because of their normal, thorough, procurement guidelines; staff expertise; and general financial controls.

15. However, the national broadcasters did not undertake or integrate formal whole-of-project risk assessments with their digital conversion projects from the outset. This would have greatly assisted in the early identification of project management risks that subsequently emerged. SBS contends that formal risk management was not as well developed in 1999 as it is today, and that its small project team informally managed the project's risks for capital procurement without documenting them. SBS also considers that there were no adverse consequences for the project arising out of its approach to risk management.

16. In the absence of whole-of-project risk assessments, the ANAO considered the relevance of the national broadcasters' corporate-wide risk management planning to their digital conversion projects. The ANAO found that digital conversion and project management were not identified as stand-alone corporate risks for the ABC.

17. In SBS, its corporate Risk Management Plan rated the ‘concentration of specialised knowledge' risk as being among SBS's greatest corporate risks. This ‘key man' risk is also a significant risk for the digital conversion project, particularly given the largely undocumented knowledge base held within its small project management team. SBS has assessed the existing controls for this risk as ‘poor'. From 2003–04 SBS has taken, and intends to take, further action to address the risk. However, the lack of documentation supporting SBS's earlier management of risks means that it was not obvious to the ANAO how SBS mitigated this perceived risk before 2003–04. SBS indicated that its digital conversion project had at least one, and in some cases, two back-up staff with enough detailed knowledge to step in and undertake the role without disrupting the project. Nevertheless, the ANAO notes the findings of a consultant engaged by SBS in mid-late 2003 who found that there was a ‘huge knowledge void' between one particular manager and his subordinate. This manager was a key member of SBS's digital conversion project management team.

Financial management

18. Both national broadcasters' general financial management information system (FMIS) controls are considered to be adequate.

19. However, the ANAO found that between early-2000 and mid-2002, there were deficiencies in the ABC project's budgetary management, which flowed through to expenditure forecasts in reports to the ABC Board. This led to the Board not being informed, in a timely manner, of a budgetary shortfall of $27.8 million (represented approximately by $8 million in scope changes and $20 million in cost increases) to complete its digital conversion project. Although acknowledging shortcomings with its project budgetary management, the ABC considers that its general FMIS controls ensured that the project never expended or committed more than that approved by the Board. In addition, the ABC considers that the Board's options for progressing the digital conversion project in light of the budgetary shortfall were not impeded by the late notice of the shortfall. However, the ANAO considers that the ABC's budget management deficiencies for the project exposed the ABC to an unnecessary risk that may have limited the Board's alternatives in responding to the options available to it.

20. The ANAO notes that the ABC has, since mid-2002, made improvements to its digital conversion budgetary management that address the related shortcomings identified earlier in the project.

21. For SBS, the ANAO considers that there were gaps in the financial monitoring and reporting documentation that would be expected for such a large and complex project as digital conversion. The ANAO noted, in particular, a lack of documentation underpinning routine, strategic multi-year budgetary management. SBS's own internal strategic reviews of the project, undertaken in mid-2000 and early 2004, provide the only documented evidence of SBS comprehensively considering the project's ongoing financial status. The ANAO considers that more regular reporting of final forecast cost-to-complete for the project would have provided greater assurance of robust project monitoring to the SBS Board and external stakeholders. SBS indicated that it adequately monitored key risks such as budget over-commitment and overruns, although it agrees the documentation could have been improved. SBS also indicated that there was no necessity to prepare formal multi-year or cost-to-complete analyses because of the year-by-year underspending on the project and the confidence SBS had in its tight, annual fiscal management. Nevertheless, the ANAO has recommended that SBS improve its internal financial reporting of significant SBS projects.

Needs assessment

22. At a whole-of-project level, the ANAO noted that the national broadcasters have adequately integrated digital conversion with their other business planning. However, project implementation planning documentation appears to have been insufficient at the whole-of-project level to demonstrate the national broadcasters' interpretation of the broad strategic outcomes sought into measurable, adequately scoped functions. The ANAO acknowledges that, given the evolution of technology occurring rapidly at the time, the plan would have had to be continually refined as conversion progressed. However, the lack of scope definition has implications for measuring whether, and when, the original Strategies have ultimately been achieved.

23. For the ABC, internal audit reports forewarned on three occasions between October 1999 and early 2002 of the need to properly plan, or otherwise make recommended improvements to digital conversion project planning. However, suggestions/improvements appear to have gone largely unaddressed until budgetary problems were identified in mid-2002. The ANAO acknowledges the ABC's efforts to address matters brought to its attention during the audit by documenting the link between the Strategies' objectives and its procurement actions. However, it would have been better to have maintained a consolidated and contemporaneous record of key scoping decisions. This would have provided greater assurance to external stakeholders of the rationale for the boundaries for the ABC's digital conversion at minimum cost. Project implementation plans would have assisted in this regard.

24. At the individual component/sub-project level, the ABC adequately assessed and documented its needs. ABC managers (i) considered the context in which their sub-projects resided; (ii) developed comprehensive technical and operational specifications for the required equipment; and (iii) undertook some formal and informal quantitative studies to determine quantities of equipment required at each ABC location.

25. In respect of the whole-of-project level, SBS has indicated that, having a small project management team, meant operational changes could be agreed within the team without the need for formal documentation. In this regard, the ANAO considers that SBS made significant scope changes/refinements early in the project's life that the Minister and DCITA were unaware of until the changes/refinements were brought to DCITA's attention by the ANAO. Specifically, the ANAO noted two instances that resulted in SBS benefiting by $14.8 million through reallocations of digital conversion funding within the project. They were:

- SBS reallocating $4.8 million in transmission and distribution funding to its costs of operating the digital equipment. Although the latter is related to the digital conversion project, the ANAO considers the reallocation to be contrary to the specific purpose for which this funding was approved. On the other hand, SBS considers that the reallocation funded actual costs of digital conversion that were part of the original plan, and that digital services would not have been provided unless these costs were met; and

- SBS effectively reallocating $10 million of funding planned for distribution capital costs to the ongoing distribution service annual charges, separately funded by Government, without reducing SBS's capital budget for digital conversion by a similar amount. This meant that the $10 million formerly allocated to distribution capital costs could fund other capital components on the project. SBS has indicated that this represents an operational change rather than a change in scope and that SBS was not required to report to DCITA on capital outlays. (For DCITA's response to both SBS scope changes/refinements, see Oversight by DCITA).

26. At the individual component/sub-project level, SBS also considered the context in which their sub-projects resided; and developed comprehensive technical and operational specifications for its radio equipment purchases. However, SBS purchased a large proportion of its television playout and encoding equipment without comprehensively documenting the technical and operational specifications of the required equipment in advance of procurement. This was because SBS relied on the results of tenders for similar digital equipment purchased for SBS's analogue and/or digital networks. There is also little documentation to support how SBS determined its equipment needs for the peripheral television equipment such as camcorders, video tape recorders and picture monitors. SBS indicated the peripheral television equipment needs were determined by discussion. SBS further indicated that although documentation of the discussions would have been ideal, it is questionable as to whether this would have led to different, or better, outcomes for these relatively low-value purchases.

Procurement

27. Digital conversion equipment has been procured according to the established procurement processes of each national broadcaster.

28. The ANAO considers that the ABC's procurement met better practice through the extensive and appropriate use of competitive tendering. The ABC obtained value for money during the purchasing of individual pieces of digital equipment.

29. SBS used differing methods to purchase digital equipment, although all accorded with its Procurement Guidelines. SBS obtained value for money by using comprehensive competitive tendering processes to procure its radio equipment. However, a large proportion of the television playout and encoding equipment purchases were based on the results of previous tenders of similar digital equipment purchased for SBS's analogue and/or digital networks. SBS advised the ANAO that, for compatibility reasons, it chose not to seek alternative solutions after these initial selections were made. SBS considers that it received value for money as their key staff were aware of price movements in the digital equipment marketplace. As well, SBS attracted significant discounts on the list price for the equipment.

30. The ANAO found that SBS purchased most of its peripheral television equipment on an ‘as-needed' basis using predetermined brands selected by competitive tender in prior years. The ANAO notes that the SBS's video tape recorder brand of choice, which comprises the bulk of the value of peripheral television equipment, was chosen by tender nearly seven years ago. The ANAO considers that it would be prudent for SBS to retest the market at regular intervals to obtain assurance that it is still receiving value for money. SBS indicated that expanded use of tendering would have introduced considerable delay into an already tight timeframe to get on-air by the legislative deadline. The ANAO notes, however, that the ABC was able to conduct thorough competitive tendering exercises for all of its digital equipment even though its requirements were more complex than those of SBS.

31. Users and managers are, essentially, pleased with the new digital equipment. The equipment is delivering on the functionality that they expected. There were some ‘teething' problems at the start, but these have generally been addressed in a timely manner. In many respects, digital equipment has reduced the time taken by staff to perform the equivalent functions using analogue equipment. Generally, the national broadcasters have used this time saving to increase the quality and quantity of output, which was envisaged under the Strategies.

Achievement of the Strategies

32. For the first few years of the digital conversion projects, the ANAO saw little recorded evidence that the national broadcasters formally monitored the extent to which the planned and completed equipment components/sub-projects fulfilled the desired functionalities in the original Strategies. The ANAO therefore considers that there may have been gaps between Strategy achievement and the national broadcasters' original expectations for digital conversion.

33. The ANAO observed shortcomings in ABC's monitoring of the link between the Strategies and the equipment sub-projects that purport to implement the Strategies. However, the ABC's recent efforts to document the link between the Strategies' objectives and its procurement actions provide assurance that significant gaps in Strategy achievement are unlikely to exist.

34. For SBS, documentation of the annual and quarterly reviews of the digital conversion project does not evidence a thorough and consolidated consideration of the project's overall status. SBS indicated that the project's status was considered during these reviews, but was not documented. SBS considers that its Phase 1 Strategy has been substantially implemented. However, a review of the Phase 1 Strategy dated August 2000 was the only documentation the ANAO sighted that evidences SBS monitoring the relationship between this Strategy and its procurement actions. In respect of SBS's Phase 2 strategy, the only relevant documentation sighted by the ANAO was project progress reviews dated August 2000 and early-mid 2004. In the latter review, SBS reassessed the meaning of its 16 sub-strategies in light of a maturing digital technology market and decided to self-fund the increase in project costs arising from the new project scope changes/refinements identified in the review.

35. The national broadcasters contend that, after completing certain outstanding components, their Phase 1 and 2 digital conversion Strategies will have been achieved. The ANAO acknowledges that the levels of digital conversion being achieved accord with the general intent of both broadcasters' Strategies. The ANAO further acknowledges that the digital conversions are being achieved efficiently. The national broadcasters have undertaken digital conversion efficiently, primarily due to the value for money obtained from individual pieces of equipment procured. In addition, the national broadcasters' decisions to self-fund the increases in their project budgets boosted value for money on the projects. In the ABC, the agreement to use any windfall gains on property rationalisations to partly offset the Government's financial contributions to the project also contributed to the value for money of the project. SBS considers that value for money has been bolstered by the use of its full digital spectrum through multi-channelling—the only free-to-air broadcaster to do so—with self-funded content.

36. Digital conversion, as defined by the Strategies, forms only a part of a broader acquisition of digital technology to provide adequate new platforms for the ABC's and SBS's broadcasting services. The digital technology acquisitions, which will be an ongoing cost over the coming years, are integral to the core business of the broadcasters. The broadcasters have thus far obtained value for money from purchasing equipment that is relevant to their digital technology acquisitions. Therefore, it is suggested that the broadcasters' focus should be on continuing to obtain value for money from purchasing appropriate equipment throughout their digital technology acquisitions. Strategic capital planning can assist in this regard.

ABC property rationalisations (Chapter 3)

37. The ABC is complying with its agreement with the Government to source $36 million in digital conversion funding from the disposal of some of its properties (Gore Hill-Sydney and Adelaide Terrace-Perth). However, as a matter of improved public administration, at the beginning of the project, the ABC and DCITA should have itemised which costs, and the related timeframes, that would be used to offset against the gross proceeds of sale to arrive at the net proceeds that the ABC agreed to contribute towards digital conversion. This potentially has significant implications for the ABC as the sale costs that it wishes to offset from the gross proceeds may run to millions of dollars and be ongoing for quite some time. The ABC has advised that it will discuss with DCITA the costs that should form part of the offset, once the ABC has itemised these sale costs.

38. Both property disposals have been significantly delayed. The Gore Hill tender process exhibited better practice. However, the ABC terminated the tender when tender bids were all significantly below price expectations. In the end, an unsolicited bid received after the ABC terminated the tender is expected to lead to a satisfactory result. The 1999 ‘tied' construction and sale agreement involving construction at East Perth and sale of the Adelaide Terrace property has now been terminated. The ABC is now considering its options for separately disposing of its Adelaide Terrace property, which is adding to the costs for the ABC and the delay in completing this aspect of the digital conversion project.

Procurement and management of transmission and distribution services (Chapter 4)

Procurement

39. As well as funding the conversion to digital equipment, the Government agreed to fund the actual costs of the national broadcasters' digital transmission and distribution services. The Ministers for Communication, Information Technology and the Arts, and Finance and Administration (the Ministers) were charged with overseeing the broadcasters' procurement of transmission and distribution services with a view to minimising the call on the Budget.

40. The ABC procured these services through competitive tendering processes covering its entire digital transmission and distribution network. SBS decided to procure transmission and distribution services in stages. SBS has procured distribution services and, until recently, transmission services, through competitive tendering processes. Of late, the Ministers approved a change to SBS's procurement approach for transmission services that has SBS now directly negotiating with the dominant transmission service provider using a comprehensive pricing model.

41. The ANAO notes that the contracting of transmission and distribution services, and the progressive rollout of new services by providers, is being undertaken at a pace that has met, and is likely to continue to meet, legislative requirements for digital broadcasting.

42. The ANAO considers that the robust nature of the procurement processes for digital transmission and distribution services oversighted by DCITA, provides assurance that the national broadcasters have procured effectively to meet the requirements of the Strategies and have thus far minimised the call on the Budget.

Reconciliation of appropriated amounts to actual cost

43. The Government's agreement to fund the actual costs of digital transmission and distribution services requires DCITA, with assistance from the Department of Finance and Administration (Finance), to reconcile appropriated funds to actual costs for the national broadcasters. Although digital transmission services have been provided since January 2000, the first reconciliations have only been completed recently. DCITA and Finance indicated that the ABC and SBS have been overpaid about $5.7 million and $9.1 million, respectively.1 The ABC and SBS have agreed with the reconciliation amounts, which they will be required to repay shortly (although SBS has sought approval from the Minister to retain $4.8 million that SBS reallocated to its costs of operating the digital equipment – see Needs Assessment).

44. Finance indicated that delays in completing the first reconciliations were caused by delays in constructing a detailed forward estimates model to match appropriations to ABC and SBS contracted payments. Finance further indicated that Finance and DCITA will undertake future reconciliations on a yearly basis.

Contract monitoring

45. The ANAO considers that there are appropriate mechanisms operating within the auspices of the contracts to monitor the performance of digital transmission and distribution services. The national broadcasters are generally satisfied with these services and have taken action when performance deviated from agreed requirements. The national broadcasters and the service providers have reserve broadcasting equipment, which results in audience reception being unaffected by most transmission and distribution problems.

Oversight by DCITA (Chapter 5)

46. DCITA's role in the ABC's property rationalisations and the national broadcasters' procurement of digital transmission and distribution services are covered in the preceding chapters.

Capital procurement

47. In approving the national broadcasters' Phase 2 Strategies in March 2000, the Government agreed that the proposed contracts for the purchase of digital equipment, transmission and distribution services by the ABC and SBS be assessed by the Ministers with a view to minimising the call on the Budget. In April 2000, the Ministers agreed that no further scrutiny of the national broadcasters' digital capital costs was necessary for a number of reasons. The reasons included that independent consultants confirmed the reasonableness of the cost estimates for the broadcasters' Strategies and that the Auditor-General would be asked to review digital conversion costs in 2003. DCITA considers that this approach reflected the view that digitisation was an activity of the broadcasters themselves. DCITA, nevertheless, expected to be informed of any significant impediments to the national broadcasters' achievement of the Strategies and any significant scope changes.

48. However, the ANAO considers that some risks to the Government's objective of minimising the call on the Budget still remained. In the ANAO's view, the existence of such risks obliged DCITA to take steps to address them. These risks included that the national broadcasters would not:

- institute and document project management processes of sufficient rigor and with sufficient transparency to demonstrate to Government (and satisfy DCITA) that the call on the Budget would, in fact, be minimised; and

- provide comprehensive and timely information to DCITA on significant changes and/or refinements to project scope.

49. A greater proactive monitoring or management of these risks may have enabled the Minister and DCITA to be better informed of the significant SBS scope changes/refinements. As noted in Needs Assessment, SBS benefited by $14.8 million from two reallocations of digital conversion funding within the project. DCITA has suggested that SBS approach the Minister to seek government approval to retain the first reallocation of $4.8 million. In relation to the second reallocation of $10 million, DCITA indicated to the ANAO its belief that Cabinet's decision did not require SBS to demonstrate that digital capital funding was applied to the specific equipment identified in the Strategies.

50. The ANAO considers that DCITA's latter comment means that SBS had the ability to transfer the $10 million in distribution capital costs to the operating expenditure stream, without having to reduce the capital budget by a similar amount. The ANAO further considers that this undermines the Ministers' rationale for not scrutinising the broadcasters' digital capital costs, because SBS's reallocation had the potential to alter the independent consultant's opinion on the reasonableness of the projects ‘after the event', could not have replaced the value of DCITA monitoring the risks to minimise the call on the Budget as the national broadcasters' projects progressed. DCITA remains of the view that its level of oversight of the digitisation Strategies has been appropriate and commensurate with its formal current relationship with the national broadcasters.

Generic performance information

51. With no established specific reporting or monitoring protocols, it can be argued that appropriate performance information on significant funding initiatives should appear in agencies' annual reports. The ANAO notes that SBS annual reports, and to a lesser extent ABC annual reports, over the past few years only make general mentions of digital conversion progress and activities, including key purchases. Nevertheless, the ANAO suggests that agencies and their portfolio department should consider negotiating appropriate performance indicators consistent with better practice for all significant funding initiatives. Agencies should then report regularly on their performance against such indicators while the initiatives remain active. Ideally, this would include reporting through annual reports to promote greater accountability for the expenditure of public funds.

Recommendations

52. The ANAO has directed one recommendation to SBS to aid its management of future capital projects.

Agency response

53. The audited agencies provided the following summary comments in response to the audit. The full text of the ABC's and SBS's responses is located at Appendix 1.

Australian Broadcasting Corporation

The ABC welcomes the ANAO's finding that the Corporation has efficiently undertaken one of the largest and most complex capital equipment projects in its history. The audit report acknowledges that the ABC has: integrated digital conversion with other business planning; met legislated timeframes without any interruptions to service; increased the quality and timeliness of its broadcast material; improved the efficiency of content production; delivered to technology users the functionality they expected; avoided ‘equipment excesses'; and applied ‘better practice' procurement disciplines.

In return for the Government's capital contribution of about $90 million, the ABC has delivered a digital conversion program throughout Australia to a total value of about $225 million. It did so at a time of considerable fluidity in the digital technology environment, purchasing necessary equipment from overseas suppliers when the Australian currency experienced a depreciation of around 30% in relation to the US dollar.

Special Broadcasting Service Corporation

SBS agrees with the ANAO's overall conclusions that SBS has undertaken digital conversion efficiently, that SBS staff did a commendable job, and that the digital conversion has met all of the legislative deadlines set by Government. In respect of digital outcomes, SBS has achieved excellent results, as evidenced by:

- SBS is the only free-to-air television network in Australia running a digital multi-channel service (24 hours a day), which was fully operational as at 1 January 2001.

- SBS was also the first free-to-air network in Australia to concurrently simulcast the entire output of its main channel in high definition.

- SBS maximised its available spectrum and is broadcasting more digital services than any free-to-air broadcaster in Australia.

These outcomes were delivered significantly within the appropriation provided, thereby minimising the call on the Commonwealth Budget.

Department of Communications, Information Technology and the Arts

The Department of Communications, Information Technology and the Arts (the Department) welcomes the ANAO's conclusion that the Department's oversight of the procurement and management of transmission and distribution services was robust. (Paragraph 42).

The Department notes the concerns raised about SBS digital conversion funding at paragraph 25 of the report and that SBS has written to the Department in relation to the $10m reallocation and to the Minister for Communications, Information Technology and the Arts in relation to the $4.8m reallocation referred to in that paragraph.

In relation to oversight more generally, the Department will take into account the ANAO's suggestion at paragraph 5.10 for improving the management of residual risk in major new technology funding initiatives for the national broadcasters.

Department of Finance and Administration

The Department of Finance and Administration notes that it has been agreed between the Minister for Finance and Administration and the Minister for Communications, Information Technology and the Arts that the reconciliation of actual digital transmission and distribution costs to the amounts appropriated to the ABC and SBS will occur annually by November each year.

Footnotes

1 The national broadcasters cannot use the overpayments for purposes other than to satisfy the costs of digital transmission and distribution services.