Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 35 of 2013–14

Managing Compliance of High Wealth Individuals

Published

Wednesday 4 June 2014

Portfolio

Treasury

Entity

Australian Taxation Office

Contact

Please direct enquiries relating to reports through our contact page.

Sector

Taxation

The objective of the audit was to assess the effectiveness of the ATO’s activities to promote tax compliance by high wealth individuals.

Summary

Introduction

1. The Australian Taxation Office (ATO) is responsible for administering Australia’s taxation system. Based on self‑assessment, the system relies on high levels of voluntary participation by taxpayers. The ATO’s goal is to support people to understand their rights and responsibilities, and protect the community by deterring, detecting and dealing with those taxpayers who do not meet their obligations. For these taxpayers, including some high wealth individuals (HWIs), the ATO implements a range of compliance strategies that increase in intensity as taxpayers’ willingness to comply decreases.

2. The ATO defines HWIs as Australian resident individuals who, together with their associates, effectively control an estimated net wealth of $30 million or more.1 In total, HWIs control significant wealth, estimated by the ATO to be in excess of $500 billion in 2012–13. Despite HWIs’ contribution to taxation revenue ($1.4 billion in 2011–12) there is a perception among the wider population that the rich may not always pay their fair share of tax.

3. HWIs tend to have complex business arrangements, with their wealth spread across a group of closely‑held companies and trusts, each of which is generally a separate taxpayer entity. They may maintain expensive lifestyles without relying on income in a conventional taxable form. Wealth can be accessed in a variety of ways such as through the sale of pre‑capital gains tax assets, loans and the use of lifestyle assets owned by the group. Publicly‑available information on HWIs is often limited, as private companies and trusts are not subject to the stock exchange disclosure requirements on public companies and not overly affected by Australian Securities and Investments Commission requirements.

4. To encourage HWIs to meet their taxation obligations and to minimise potential revenue losses, the ATO has had a particular focus on HWIs since 1996. By 2013, the ATO had identified approximately 2600 HWIs and 3700 potential HWIs2, and reported that it had collected over $3 billion in additional revenue as a result of the compliance activities conducted since 1996. Accordingly, while representing a relatively small number of individuals, HWIs are a key population group for the ATO in terms of revenue collected through active compliance activities.

5. The ATO uses two broad categories of compliance activities: voluntary compliance activities that encourage taxpayers and their representatives to understand and comply with their obligations3; and active compliance activities that seek to verify information or enforce taxation law. Active compliance includes three main types of activities:

- preliminary risk reviews, which do not generally involve contact with the taxpayer and seek to gain a better understanding of an individual’s tax affairs to determine if a more in‑depth review is needed;

- comprehensive risk reviews, which involve taxpayer contact and are a more detailed examination of the individual’s tax affairs; and

- audits, which can be specific or wide‑ranging examinations of an individual’s tax affairs and can involve visits to the taxpayer’s premises. Audits are generally more intensive and take longer to complete than a comprehensive risk review.

6. The ATO responds to HWI compliance risks through the Private Groups and High Wealth Individuals business line, which also has similar responsibility for not‑for‑profit organisations, medium businesses and wealthy Australians.4 This business line has conducted many active compliance activities involving HWIs, and has a target of conducting 500 audits and risk reviews in 2013–14. Approximately 300 staff will be involved in these active compliance activities.

7. The HWI compliance strategy is based on a risk‑management approach that determines compliance activities according to the risks HWIs pose to the taxation system. The ATO uses a range of wealth and risk assessment tools, collectively referred to as the Risk Differentiation Framework (RDF)5, to help in the selection of those HWIs that will be subject to compliance activity. The RDF has also become an important medium for communicating the ATO’s risk management approach to the HWI taxpayers, and was used to source almost all HWI compliance cases (94 per cent for the period December 2010 to September 2013).

8. In the 2012–13 Mid‑Year Economic and Fiscal Outlook, the Government allocated $390 million in additional funding to the ATO for further compliance activities. Approximately $37 million of this funding was for the implementation of a new strategy Engaging newly identified HWIs, which aims to confirm that these newly identified HWIs meet their tax obligations.

Audit objective and criteria

9. The objective of the audit was to assess the effectiveness of the ATO’s activities to promote tax compliance by high wealth individuals. To form a conclusion against this objective, the ANAO adopted the following high‑level criteria:

- compliance activities were supported by effective business and administrative arrangements;

- compliance risks were identified effectively;

- compliance activities, and associated objections and reviews, were conducted effectively; and

- outcomes and objectives were achieved.

Overall conclusion

10. High Wealth Individuals pose considerable challenges to tax administrations around the world because of the complexity of their affairs and opportunity for aggressive tax planning6, their contribution to revenue, and the potential for their behaviour to influence perceptions of the integrity of the tax system. In Australia, the tax compliance of HWIs is considered by the ATO to represent a significant revenue risk. Providing assurance that HWIs meet their tax obligations is essential to protect Australia’s revenue base and maintain community confidence in the equitable administration of the taxation system.

11. The ATO has effectively carried out a range of activities and engaged with HWI taxpayers and their representatives to reinforce their understanding of, and promote compliance with, tax obligations. The ATO’s engagement approach has been one of transparency about its key areas of focus, and it has disseminated extensive guidance material and information in relation to tax requirements. The ATO has also had a particularly extensive HWI active compliance focus, conducting audits and risk reviews7 of over 90 per cent of the population between 2009–10 and 2012–13 and collecting almost $852 million as a result of these compliance activities ($671 million from audits and $181 million from risk reviews).

12. However, the results of these activities have not always been commensurate with the level of effort deployed by the ATO. Over the four‑year period, 90 per cent of the cash collected was from 12 per cent of the audits and five per cent of the comprehensive risk reviews undertaken by the ATO.8 The majority of these audits (70 per cent) and comprehensive risk reviews (84 per cent) did not have a financial outcome.9 Going forward and in anticipation of a focus on a larger pool of HWIs (from 2600 to around 6300), there is scope for the ATO to improve its risk assessments to better target active compliance activities and reduce compliance costs for both HWI taxpayers and the ATO.

13. The ATO has recognised the need for improved risk identification and differentiation, and since 2004 has been developing and refining the HWI risk assessment tools, most recently the Risk Differentiation Framework (RDF). Despite acknowledged shortcomings, the RDF has been central to the implementation of the HWI compliance strategy. Between 2009 and 2013, 94 per cent of all cases selected for compliance intervention were identified using the RDF. The ANAO’s analysis of the outcomes of HWI compliance activities has however indicated that the RDF has not always been effective in identifying higher risk cases. The analysis also indicated that there was little or no link between wealth and non‑compliance within the HWI population. The ATO has advised that it is further refining the RDF, including by modifying the weighting of wealth, and will continue to assess its reliability in effectively differentiating risk within the HWI population. In this regard, it is important that the ATO analyses the outcomes of the compliance activities in order to assess the effectiveness of the RDF in identifying the highest risk HWIs as well as to test the validity of the risks that have led to the selection of compliance cases.

14. HWI compliance work is complex, dealing with intricate business structures and contentious tax issues, with little available public information. This often makes it difficult for the ATO officers undertaking HWI compliance work to reach readily agreed positions in a timely way. Almost 40 per cent of reviews and audits completed between 2009–10 and 2012–13 were not delivered within the scheduled cycle time.10 Audits in particular exceeded cycle times by 352 days on average, against an already long initial cycle time (of 730 days for the majority of cases).11 Despite these timeframes to resolve cases, HWI taxpayers objected to the outcome of their reviews or audits in approximately 65 per cent of cases completed in 2011–12 and 2012–13. Half of these objections resulted in a positive outcome for HWIs; being allowed either in full or in part. In more than 50 per cent of the cases where an objection had been allowed or settled, ATO objections staff recorded that the original compliance decisions were at least partially incorrect, or the ATO had changed its interpretation of the law.

15. These high rates of successful objections, together with the large proportion of compliance cases without a financial outcome and frequent completion of cases well beyond target cycle times, highlight opportunities for improving the conduct of HWI compliance activities. The ATO acknowledges these opportunities and has initiatives underway to strengthen compliance practices through improving staff capability, better using technical support, promoting staff communication with taxpayers and reducing the number of aged cases. To more efficiently allocate compliance resources, it is also important that the Private Groups and High Wealth Individuals (PGH) business line better assesses the costs of HWI compliance activities and more accurately calculates the actual return on investment12 from these activities.

16. The ANAO has made two recommendations aimed at improving the reliability of the RDF through analysis of active compliance outcomes; and improving resource allocation by having greater regard to compliance risk and financial return.

Key findings by chapter

Assessing compliance risks (Chapter 2)

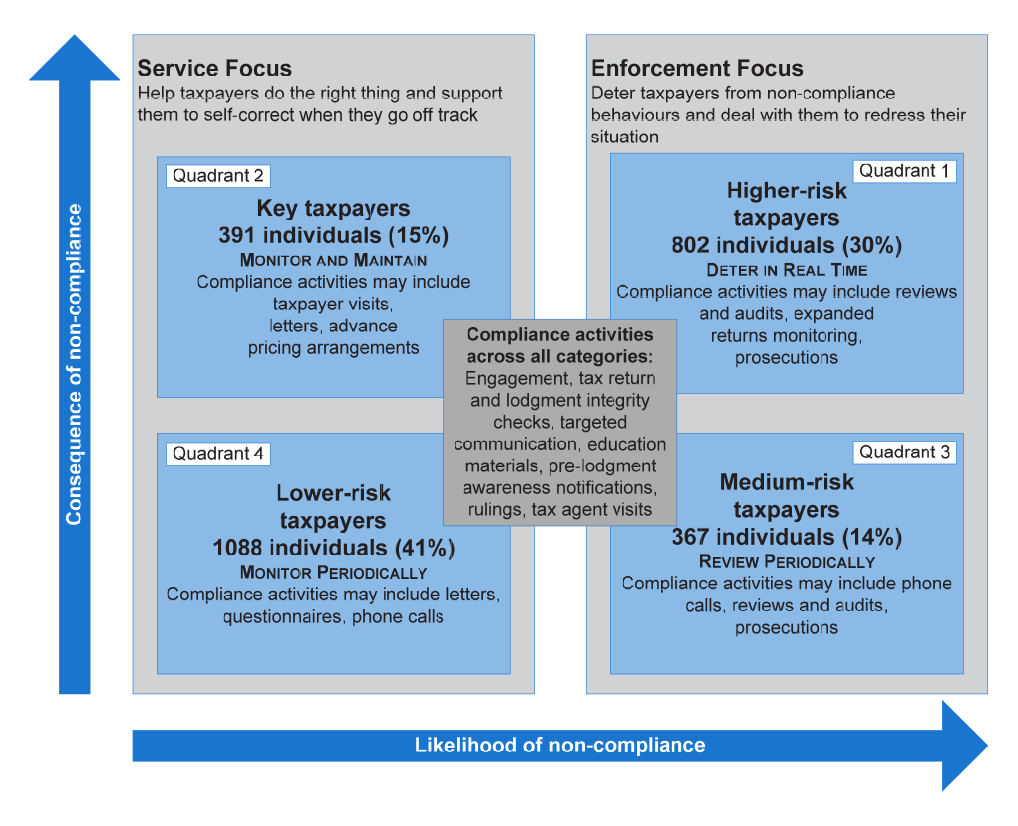

17. The ATO has used assessment tools (including risk engines, data mining and analytical models) to automate the identification and risk assessment of the HWI population since 2004. Three main tools contribute to the current HWI risk assessment process: the Group Wealth System, which calculates the net wealth of the entire taxpayer population; the Integrated Scoring Model, which extracts HWIs from the taxpayer population, assesses them against known risks, and applies a likelihood and consequences score to those risks; and the RDF, which provides a visualisation of the level of risk represented by each HWI taxpayer (Figure S1). The RDF was applied for the first time in the PGH business line in 2012 and is used by the ATO to guide the nature and intensity of its interaction with taxpayers.13

Figure S.1: ATO’s Risk Differentiation Framework for HWIs, 2013

Source: ANAO, based on ATO, Tax Compliance for Small‑to‑Medium Enterprises and Wealthy Individuals and ATO, Minute to the PGH Risk Management Committee, 18 October 2013.

18. The ATO has developed a formal process to review existing risk rules and identify new rules. Three committees, each with separate responsibilities, oversee the identification of the population and development of risk rules underpinning the risk ratings assigned to HWI taxpayers.

19. Compliance teams, through their case work, are well positioned to validate existing risks and identify new risks, and their observations represent an important source of intelligence, including identifying areas of the law that may require clarification. The ATO released, in July 2013, a new intelligence framework, ATOintelligence Discover, which should enable more effective collection of intelligence from compliance teams. While there are review processes, there is no systematic quantitative analysis of the outcomes of the compliance activities, to assess if the compliance cases selected through the RDF process are the highest risk cases.

20. The information technology processes supporting the development of the RDF are relatively complex. These processes are characterised by a succession of steps, some manual and some automated, which necessitate repeated access to a range of internal and third party databases. While the control environment is not as mature as in other ATO systems, it is suitable for the context in which it operates, as the information produced is intended to be further analysed and filtered by downstream business processes. However, documenting the end‑to‑end process is likely assist in efforts to improve control over the quality of the information produced, as well as provide guidance to staff.

21. The RDF process is used by the ATO to determine the level of risk each HWI represents by assessing the relative likelihood of the individual being non‑compliant and the consequences of that potential non‑compliance. The ATO determined the boundaries between higher and lower risk HWIs on the basis of its available compliance resources and commitments, rather than in relation to an analysis of risk tolerance. Also, the algorithm used by the ATO to determine a HWI’s position on the consequence axis of the RDF meant that wealth and business income contributed to 80 per cent of the HWI’s consequence score, subsequently impacting the overall HWI risk rating. Analysis undertaken by the ANAO of the outcomes from compliance activities conducted between 2009–10 and 2012–13 indicated that there is little or no link between wealth and non‑compliance within the HWI population.

22. There would be merit in the ATO testing the relationship between the other risk factors of the Integrated Scoring Model (including business income) and non‑compliance, to assess whether the weightings attributed to these factors are sound. The ATO advised that work is being undertaken to determine fixed boundaries for the RDF, based on the level of risk that the ATO considers tolerable or intolerable. As part of this work, the ATO is also reviewing the weightings attributed to the different factors in the Integrated Scoring Model.

Compliance case selection (Chapter 3)

23. The aim of the case selection process is to provide compliance teams with a pool of the highest risk compliance cases, reflecting the ATO’s HWI compliance strategy. Since January 2011, the selection of HWI compliance cases is coordinated by a single team, the National Case Selection team. This team coordinates the selection of compliance cases, initially using the RDF process, and then manually assessing the RDF‑identified cases to determine their priority for compliance activity. The establishment of a centralised case selection process supports a more systematic and robust process for selecting cases, and better alignment between the compliance strategy and active compliance resources and commitments.

24. Evaluating the effectiveness of the RDF process in selecting the highest risk compliance cases is essential to confirm that compliance resources are being used effectively, and to support continuous improvement processes. Accordingly, the ANAO examined 1445 cases assessed by the National Case Selection team between December 2010 and September 2013. The RDF was the primary source of cases selected for active compliance, representing 94 per cent of all cases assessed.14 In most years to September 2013, almost all cases were drawn from Quadrant 1, the highest risk quadrant. In 2011–12, the ATO drew 61 per cent of compliance cases from the lowest risk quadrant of the RDF (Quadrant 4). The ATO advised in May 2014 that these lower risk cases were selected because they had likelihood and consequence profiles that were similar to the higher risk cases in Quadrant 1. The ATO missed this opportunity to compare compliance outcomes from cases selected from different quadrants to assess the effectiveness of the RDF.

25. The ANAO used two key indicators to assess the effectiveness of the RDF process in selecting cases that present the higher risk (likelihood and consequences) of non‑compliance:

- cases drawn from the RDF are either not actioned or directed to compliance by the National Case Selection team15: the proportion of cases not actioned can be expected to reduce over time, reflecting the continuous improvement to the RDF process, and be smaller for cases categorised as higher risk cases. Conversely, the proportion of cases accepted for compliance activity should increase over time and be larger for cases categorised as higher risk cases. However, the proportion of cases not actioned and cases accepted for compliance has remained constant since 2011–12 and remained similar for higher and lower risk cases; and

- active compliance escalation rate16: escalation can indicate that the initial selection of the case was successful, as the compliance risks were confirmed. The escalation rate can be expected to be higher for higher risk cases than for lower risk cases. However, the categorisation of a case as higher or lower risk through the RDF did not impact on the decision by active compliance teams to escalate the case for more intensive examination.

26. These results raise issues about the effectiveness of the RDF process in selecting the highest risk cases and emphasise the importance of the ATO regularly assessing the RDF risk factors.

27. In response to a recommendation from the Inspector‑General of Taxation17, the ATO initiated a review of its risk assessment processes. Five measures were developed.18 One of these measures, the risk rule confirmation rate, which compares the risks identified through the RDF process to the risks confirmed, not actioned or newly identified by the compliance officer, yielded particularly useful information on the effectiveness of some of the risks. The ATO advised that this information was used to improve the RDF. There would be benefit in the ATO continuing to collect and analyse this performance data.

Conducting compliance activities (Chapter 4)

28. The ATO effectively engaged with HWI taxpayers and their representatives to gain assurance that they are aware of their tax rights and obligations. The ATO website makes available HWI‑specific information and resources, including information on the ATO’s compliance strategy, and legal and policy information (through the ATO Legal Database also accessible from the ATO website). Senior ATO executives have also engaged directly with HWI taxpayers and their representatives in numerous forums; and general and specialised publications have relayed the ATO’s message.

29. As previously discussed, the ATO has conducted a large number of audits and reviews that generated $852 million in cash collections between 2009–10 and 2012–13. In conducting these activities, the ATO has covered a large proportion of the HWI population (over 90 per cent). However, for the majority of cases (70 per cent of audits and 84 per cent of comprehensive risk reviews), there was no financial outcomes.

30. Between 2009–10 and 2012–13, almost 40 per cent of audits and reviews were not completed within the allocated cycle time. Audits that did not meet the cycle time standard exceeded it by an average of 352 days; comprehensive risk reviews by an average of 152 days; and preliminary risk reviews by an average of 65 days. Exceeding cycle times, especially for compliance activities that already have a long completion time such as audits, generates management challenges for the ATO, and extends the compliance burden for the taxpayer.

31. In a context of reduced ATO resourcing, it becomes even more important for the ATO to determine where the most effective compliance effort should be directed. Currently, the ATO determines its return on investment by dividing the total amount of liability raised through HWI compliance work by the average salary of the compliance staff involved. A more accurate measure would be to use the amount of cash collected, in addition to the liabilities raised. In 2012–13, the return on investment for HWI compliance activities was $27 for each dollar spent based on liabilities raised, but only $7 when based on cash collected. Further, the ATO does not currently calculate the cost of HWI compliance activities, and does not compare these with other populations in the business line. Assessing the cost of compliance activities for the HWI population could enable the ATO to more efficiently allocate compliance resources across the PGH business line.

32. The ANAO reviewed the management of HWI compliance cases by examining a sample of 244 comprehensive risk reviews and audits finalised between 2009–10 and 2012–13. There were some weaknesses in the recording of key documents and approvals in the ATO’s electronic case management system. While active compliance staff indicated that they considered the case management system to be inflexible, slow, and generating duplication, it is important that key case documentation and approvals are recorded. Direct engagement and communication with HWI taxpayers and their representatives is encouraged by the ATO and greatly appreciated by the HWIs’ representatives. However, it did not take place as systematically as prescribed in ATO processes, or as desired by HWI representatives, in the cases reviewed by the ANAO.

Objections and appeals (Chapter 5)

33. The law gives taxpayers the right to object to ATO decisions when a taxpayer has been issued with an amended assessment following a compliance activity. When this occurs, the ATO conducts an independent internal review. The ATO aims to complete its review of the objection within 56 calendar days. If taxpayers disagree with the result, they are able to apply to the Administrative Appeals Tribunal or the Federal Court of Australia for an independent external review.

34. Approximately 65 per cent of compliance decisions (123) resulted in an objection in 2011–12 to 2012–13, of which almost half (49 per cent) gained a positive outcome for HWI taxpayers. For a large proportion of cases allowed in full or in part (45 per cent), new facts and evidence were introduced after completion of the compliance activities. However, for the remainder (55 per cent), the ATO recorded that the compliance decisions were at least partially incorrect, or that the ATO had changed its application of the law.

35. More than one in three HWI objections finalised between 2011–12 and 2012–13 required more than a year to complete. For those HWI taxpayers who object to their amended assessment, the time taken to determine an objection adds to the time taken to finalise the audit or review. Typically this will mean that taxpayers will be uncertain about their tax liability for over one thousand days for audits and over 600 days for reviews.19

36. Delivering soundly‑based compliance decisions is both a priority and a desired outcome for the ATO, especially given the considerable time and resources expended on HWI compliance activities. Objection data suggests that, despite the time taken to complete compliance work, a substantial proportion of objections were allowed because the initial compliance decision was at least partially incorrect. The ATO advised that tax adjustments for HWIs often relate to complex, contentious and grey areas of the law. In this light, the work being undertaken by the ATO to improve the capability of compliance staff, and the increased use of alternative dispute resolution processes, may have a positive effect on active compliance timeframes and outcomes.

Measuring compliance effectiveness (Chapter 6)

37. Since 2008, the ATO has used a compliance effectiveness methodology (CEM) to measure the impact of its compliance strategies on treating specific compliance risks. The methodology is an iterative, workshop‑centred approach based on two key elements: the identification of measurable compliance objectives; and the articulation and treatment of the risks to achieving these objectives.

38. The ATO has undertaken a CEM evaluation of HWI compliance activities on three occasions (2007, 2009 and 2012), and is planning for another evaluation in 2014. The 2012 iteration of the CEM was largely a refresh of the previous approaches, with some refinements to the success goals and effectiveness indicators. None of the three completed evaluations reached a firm conclusion as to the overall effectiveness of compliance activities in addressing HWI compliance risks, although the Chair of the Risk Management Committee observed that the compliance strategies were ‘heading in the right direction’.

39. The indicators used for the 2012 CEM implementations addressed key elements of the effectiveness of the ATO’s strategies to address HWI compliance risks, covering trends in voluntary compliance, outcomes from active compliance activities and community confidence levels. However, there were no indicators relating to interpreting the legislation to reduce potential lack of clarity in the application of the law by taxpayers and minimising aggressive tax planning. Further, the indicators did not adequately use information that could be obtained from the extensive programs of HWI audits and risk reviews, or from the risk assessment tools. In this regard, the evaluations could have analysed the results from active compliance activities, including the number of compliance cases resulting in an amended assessment and the relative scale of those returns. Such analysis could have facilitated the identification of more substantial opportunities to improve risk assessments, case selection and active compliance strategies and treatments.

40. There is limited external reporting of the results of HWI compliance activities. The ATO does monitor performance and report internally, particularly against deliverables such as revenue and other active compliance targets (including the number of compliance cases, liabilities raised and cash collected). Internal monitoring and reporting of HWI performance was examined in an ATO review of internal reporting arrangements within the PGH business line that was completed in February 2014. The ATO advised that as a result of the review, the reporting was more consistent, streamlined and reliable. The review also identified opportunities for consolidating the business line’s reporting capabilities, which were still being considered for implementation at the time of this audit.

Summary of agency response

41. The ATO provided the following response to the audit report, with the formal response at Appendix 1.

The ATO welcomes this report. In finding the ATO’s compliance approach to be generally effective, the review recognises the challenges that the ATO has in managing tax compliance of HWIs. Such challenges include complex business arrangements, opportunities for aggressive tax planning, intricate structures, contentious tax issues, grey areas of the law and limited public disclosure of financial information.

While the review focused on the four years to 30 June 2013, the ATO has made a number of significant improvements to its work in this area over the last 12 months.

We acknowledge there are further improvements to be made and the two recommendations will further assist with our improvements in this area.

Recommendations

|

Recommendation No. 1 Paragraph 3.29 |

To improve the reliability of the Risk Differentiation Framework (RDF), the ANAO recommends that the ATO analyses the outcomes of active compliance cases to assess the effectiveness of the RDF process in identifying those HWI taxpayers at higher risk of non‑compliance. ATO response: Agreed.

|

|

Recommendation No.2 Paragraph 4.43 |

To enable the ATO to more efficiently allocate compliance resources across the Private Groups and High Wealth Individuals business line, and to more accurately demonstrate return on investment, the ANAO recommends that the ATO: (a) better assesses the cost of compliance activities for the HWI population; and (b) calculates the return on investment for HWI compliance activities on the basis of cash collected, in addition to liabilities raised. ATO response: Agreed.

|

Footnotes

[1] ATO, Tax Compliance for Small‑to‑Medium Enterprises and Wealthy Individuals. The ATO uses the market value of assets to estimate the net wealth controlled by HWIs.

[2] Potential HWIs are wealthy individuals who meet the ATO definition of a HWI but whose wealth estimate has yet to be confirmed ATO, Highly Wealthy Individuals: 2013–18 overarching strategy.

[3] The ATO’s strategy to improve voluntary compliance is to be transparent about its key areas of focus, to provide information and to engage with HWIs and their representatives. Key messages are disseminated through the ATO’s compliance program, annual reports, speeches delivered by the Commissioner of Taxation and senior ATO executives, and the media.

[4] Wealthy Australians are Australian residents controlling a net wealth of $5 million to $30 million.

[5] The RDF is also used to identify the HWI population and determine differentiated levels of tax compliance risk.

[6] Aggressive tax planning takes advantage of the technicalities of a tax system or of mismatches between the tax systems of two or more countries for the purpose of reducing tax liability.

[7] As previously noted, there are two main types of risk reviews: preliminary risk reviews, which do not generally involve contact with taxpayers; and comprehensive risk reviews, which involve contact with taxpayers and a more detailed examination of their tax affairs.

[8] A relatively small amount of cash was also collected from preliminary risk reviews—$3.6 million from five of 1812 completed preliminary risk reviews.

[9] The ATO advised that the main purpose for undertaking a comprehensive risk review is to consider if an audit is warranted, rather than seeking to obtain a financial outcome. It is also important to note that additional cash may be collected in later years in respect of the liabilities raised from both audits and risk reviews, and that adjustments to losses may have a positive effect on future revenue collections.

[10] Cycle times refer to the elapsed timeframe for completion of a review or audit determined by the compliance team at the start of the case examination. They vary depending on the type of activity and the complexity of the case.

[11] For the period examined by the ANAO, preliminary risk reviews should have taken between 40 and 60 days; comprehensive risk reviews between 30 and 365 days, and audits between 180 and 1095 days. The current cycle times are: 60 days for preliminary risk reviews; 180 days for comprehensive risk reviews; and 730 days for audits.

[12] The ATO calculates the return on investment by dividing the total amount of liability raised (but not necessarily collected) through HWI compliance work by the average salary of the compliance staff involved in HWI compliance work, as further discussed in paragraph 31.

[13] This report refers to the RDF to collectively describe the processes leading to the identification, risk assessment and scoring of the HWI population, rather than referring to the specific tools used in the process.

[14] Other sources include referrals from internal and external intelligence.

[15] Two outcomes are possible for cases considered in the selection process: not actioned, if the case selection teams consider that the compliance risks presented by the case were not sufficiently high or if the case was selected by the RDF in error; or sent to active compliance to be submitted to a risk review.

[16] A case is escalated when it is moved from a lower intensity compliance activity, such as a comprehensive risk review, to a higher intensity activity, such as an audit.

[17] Inspector‑General of Taxation, Review into the ATO’s compliance approaches to small to medium enterprises with annual turnovers between $100 million and $250 million and high wealth individuals, December 2011, p. 72.

[18] The five measures were: strike rate (ratio of audits which reached a financial outcome to total audits completed); escalation rate; analysis of ‘no further action’ cases (cases that were not deemed to warrant further investigation and did not reach a financial outcome); National Case Selection panel validation rate (ratio of cases drawn from the RDF and subsequently validated by the case selection panels as worthy of further investigation by the compliance area); and risk rule confirmation rate (ratio of risks identified through the RDF and subsequently confirmed by the compliance area, to risks identified through the RDF).

[19] Audits required on average 716 days to complete; and comprehensive risk reviews on average 250 days to complete, added to the average 352 days to determine an objection.