Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Performance statements audit

Auditor-General Report No. 16 of 2023–24

Audits of the Annual Performance Statements of Australian Government Entities — 2022–23

Published

Monday 12 February 2024

Portfolio

Across entities

Entity

Across entities

Contact

Please direct enquiries through our contact page.

This report presents the 2022–23 performance statements audits findings and observations, assessments of auditees’ maturity in performance reporting, and the future direction of the ANAO’s performance statements program.

Executive summary

The context for performance reporting

1. Governments make investment decisions to support the achievement of their policy objectives and allocate funding to Commonwealth entities to deliver these objectives through the annual budget process.

2. Financial statements of Commonwealth entities provide useful information on expenditure and financial position, but do not contain all the information needed to measure and assess how well entities have used their allocated funding and public resources in the delivery of government policies and programs and the provision of goods and services. Consequently, Commonwealth entities need to supplement financial information with non-financial performance information1 to:

- enable the government to assess if it is achieving its policy objectives;

- be accountable for, and transparent about, how they use public resources;

- monitor and benchmark their performance over time and identify opportunities to improve the programs and services they deliver; and

- support government decision-making.

3. The Public Governance, Performance and Accountability Act 2013 (PGPA Act) establishes an entity’s corporate plan as its primary planning document2 and imposes specific obligations and requirements for entity performance reporting. Providing meaningful information to the Parliament and the public and meeting high standards of governance, performance and accountability are key objects of the PGPA Act.3

4. The development and use of performance information should be integral to an entity’s strategic planning, budgeting, monitoring and evaluation processes. The right amount of understandable performance information, on the right activities, can be used to promote the achievement of the entity’s purposes4, identify what is working and what areas need improvement and promote accountability to the Parliament, the government and the public for the effective delivery of government policies, programs and services.

5. Our audits indicate that entities are using their corporate plans and annual performance statements in different ways and giving them different levels of prominence within the entity. For example, where there is regular monitoring and reporting to senior leadership throughout the year it elevates the level of importance, improving the quality of performance information and reporting. Alternatively, if information is only reported as part of the annual performance statements preparation process it can be seen as a compliance exercise and not as an integral part of good management and stewardship of public resources.

Entities’ need for meaningful performance information

6. The measurement and reporting of performance is not something that is done for its own sake. It is a process undertaken to ensure that appropriate and trustworthy information is available, when required, to enable well-informed and evidence-based decisions to be made about how to improve performance and to promote accountability.

7. Annual performance statements should tell the story of whether the entity is doing its job well. For a Commonwealth entity to report high quality information that tells this story, there are fundamental questions to consider.

- Why does the entity exist, and what is it expected to deliver?

- What does good performance and success look like, and how will the entity know it is doing a good job?

- How can the entity’s performance be measured reliably over time?

- What performance information would provide a complete picture of an entity’s performance and enable the entity’s performance in achieving its purposes to be effectively measured and assessed?

- Will the entity’s annual performance statements provide a user, including the Parliament, meaningful information about how well the entity has performed?

8. The answers to these questions are key to an entity’s understanding of its business and whether it is using and managing public resources properly to deliver on what is expected. A focus on good governance practices and accountability is likely to produce annual performance statements that meet the needs of entities and users, including the Parliament, and the requirements of the Commonwealth Performance Framework (the framework).

The role of leadership in developing a performance culture

9. Effective performance reporting is more than an entity producing a set of annual performance statements that meet the minimum requirements of the PGPA Act and the Public Governance, Performance and Accountability Rule 2014 (PGPA Rule). Performance information should be integral to how an entity plans and operates to achieve its purposes. Strategic and concerted leadership is required to embrace meaningful performance reporting as essential to good management and the effective stewardship of public resources.

The 2022–23 performance statements audit program

10. In 2022–23, the ANAO conducted audits of 10 entities’ annual performance statements. This is an increase from the six entities in 2021–22.

11. There has been some improvement in entities’ processes and capability to develop high quality performance information, noting the requirement for entities to prepare annual performance statements under the PGPA Act took effect from 1 July 2015. The audit program has demonstrated that mandatory annual performance statements audits encourage entities to invest in the capabilities needed to plan, monitor and report high quality performance information on an ongoing basis.

12. Further improvement is required for performance statements to provide meaningful information on an entity’s performance in line with the spirit and intent of the framework. Ensuring annual performance statements comply with the minimum requirements of the PGPA Act and Rule is a necessary but not sufficient standard for Commonwealth entities to meet when reporting on their performance.

Audit conclusions and additional matters

13. Overall, the results from the auditor’s reports of the 2022–23 performance statements audits are mixed. Six of the 10 auditees received an audit conclusion without modification5: the Attorney-General’s Department (AGD), the Department of Education (Education), the Department of Industry, Science and Resources (DISR), the Department of Social Services (DSS), the Department of the Treasury (the Treasury) and Services Australia. Four entities received an auditor’s report with a qualified audit conclusion identifying areas where users could not rely on the performance statements: the Department of Agriculture, Fisheries and Forestry (DAFF), the Department of Infrastructure, Transport, Regional Development, Communications and the Arts (DITRDCA), the Department of Veterans’ Affairs (DVA) and the Department of Health and Aged Care (DoHAC).

14. The 2022–23 audits indicate improvement in entity performance reporting. Compared to the 2021–22 audits, in 2022–23 the proportion of audited entities that received a qualified audit conclusion decreased. The proportion of entities’ measures that were included in the basis for qualified conclusion also decreased from 2021–22 to 2022–23.

15. Where appropriate, an auditor’s report may separately include an ‘Emphasis of Matter’ paragraph. An emphasis of matter paragraph is a tool available to auditors to draw the reader’s attention to an important matter presented in the performance statements that, in the auditor’s judgement, is fundamental to the users’ understanding of the information in the performance statements.

16. Six of the 10 auditees received an auditor’s report containing an emphasis of matter paragraph: DAFF, Education, DoHAC, DSS, DVA and Services Australia. In 2021–22, one of the six auditor’s reports contained an emphasis of matter paragraph. An auditor’s report may also refer to ‘other matters’ to draw a reader’s attention to an issue without modifying the audit conclusion. DoHAC’s auditor’s report contained an other matter paragraph.

Audit findings

17. A total of 48 findings were reported to entities at the end of the final phase of the 2022–23 performance statements audits. These comprised 16 significant, 13 moderate and 19 minor findings. The resolution of 48 per cent of interim 2022–23 audit findings reflects that entities made effort to resolve findings during the final phase of the audit.

18. The significant (A) and moderate (B) 2022–23 audit findings fall under five themes:

- improved governance and accountability by implementing an enterprise-wide performance framework (issued to four entities);

- complete and meaningful performance information (issued to five entities);

- accuracy and reliability of reported information (issued to five entities);

- usefulness of performance information (issued to two entities); and

- preparation and record keeping processes (issued to three entities).

Observations of entities’ performance information

19. The main observations of the 10 entities’ performance information include the following:

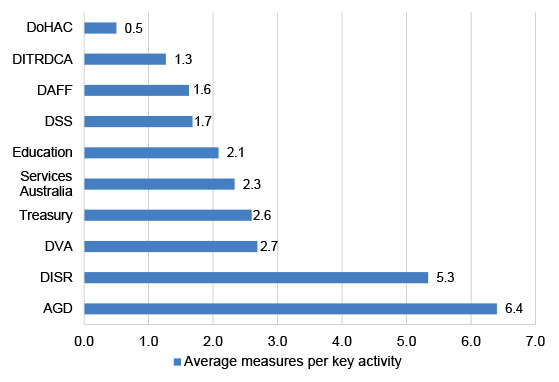

- on average, entities used 2.7 measures to assess a key activity;

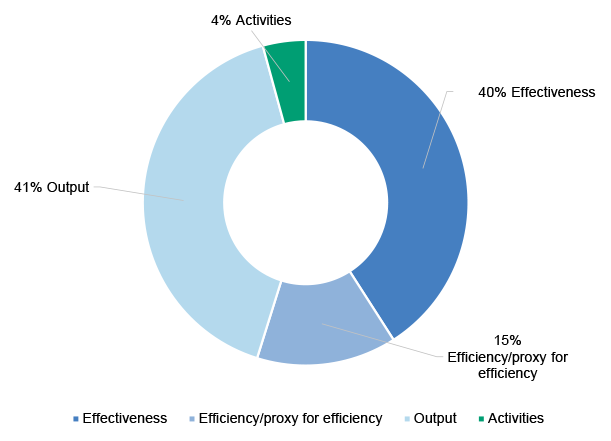

- entities predominantly used ‘output’ (41 per cent) and ‘effectiveness’ (40 per cent) measures to assess their performance;

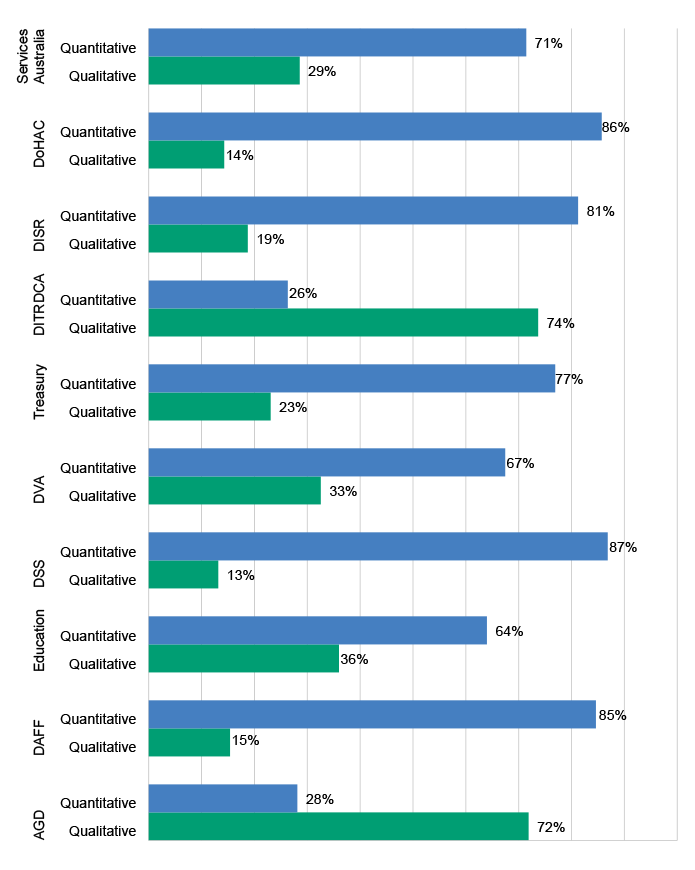

- a large majority of most entities’ performance measures are quantitative performance measures; and

- for six of the 10 entities, a majority of their 2022–23 performance measures were identical or comparable to the measures in their 2020–21 corporate plan.

The maturity of entities’ performance reporting processes

Leadership

20. An entity’s leadership is key to valuing performance information and setting expectations for its quality and use. The ANAO assessed that six of the 2022–23 auditees had either a mature or maturing performance culture with demonstrated buy-in from the accountable authority and senior executives. Ongoing leadership is essential to elevate the importance of performance monitoring and reporting to promote accountability and to demonstrate the performance of entities and the impact of government policies, programs and services.

Governance

21. Governance refers to the processes through which an entity’s performance information is planned, monitored, reported and used to guide decision-making. The Explanatory Memorandum to the PGPA Bill states that the third object of the Act is to require Commonwealth entities, among other things, to:

meet high standards of governance—good governance provides the foundation for high performance and community confidence in the public sector. Good governance is grounded in accountability, transparency, leadership, integrity and stewardship and in responsiveness to the needs and aspirations of citizens. The governance arrangements for entities should clearly spell out the roles, responsibilities and accountabilities of leaders and officials.6

22. The ANAO assessed that AGD, DISR, DVA and Treasury had mature governance processes to monitor and report performance. Entities’ governance can be improved through a properly implemented enterprise-wide performance framework. Most entities in the 2022–23 audit program have not fully implemented such a framework.

Data and systems

23. The ANAO did not assess any of the 2022–23 auditees as ‘mature’ in terms of their ability to use data and IT systems to produce complete and accurate performance results, including the use and validation of third-party data to generate and report performance information. There is also a need for better coordination and understanding between specialised data teams and those responsible for policy, service delivery and governance.

Capability

24. Capability relates to the knowledge and skills within an entity that contributes — both directly and indirectly — to designing, measuring and reporting high quality performance information on an ongoing basis. The 2022–23 audits indicate that the performance statements audit program is influencing change to improve entities’ capability for performance reporting. The ANAO assessed that AGD, DISR, DVA and Treasury have a ‘mature’ or ‘maturing’ capability.

Resourcing

25. Resourcing relates to an entity’s investment in, and coordination and management of, staff and other resources that are required to undertake performance reporting. Just like for financial management, entities should consider their resourcing profile for performance monitoring, evaluation and reporting, including the adequacy of resources to design and implement effective performance frameworks, undertake quality assurance and liaise with divisional areas in devolved structures.

The development and future direction of annual performance statements audits

26. Despite improvement in the quality of entity performance statements, performance information needs to be prepared and reported more robustly if it is to properly serve external user needs and be used by internal users, such as leaders and senior managers of Commonwealth entities, to improve public service effectiveness.

Areas of audit focus

27. The ANAO’s 2022–23 performance statements audits are designed to assess whether entity annual performance statements present fairly the entity’s performance in the reporting period and that the statements were prepared in accordance with the requirements of the PGPA Act and PGPA Rule.

28. The ANAO audits seek to incentivise entities to report appropriate and trustworthy information that will enable a user to assess if the entity has done a good job and not to merely report a minimum set of information to satisfy legal requirements.

Timeliness of reporting to Parliament

29. For the ANAO to provide timely assurance to the Parliament on entities’ annual performance statements, it is important that key audit and reporting milestones are met. Eight of the 10 auditor’s reports were signed before the end of September 2023. The ANAO’s aim is to align the timing of signing the auditor’s report with an entity’s financial statements and performance statements.

Ongoing engagement

30. The ANAO’s communication and engagement with the sector continues to be important to improving the sector’s capability to report meaningful performance information. In 2023, this has included the publication of an Audit Insights product — Reporting Meaningful Performance Information — and the ANAO’s Performance Statements Audit Manual, as well as the ongoing work of the Performance Statements Expert Advisory Panel.

Future direction

31. In 2023–24 and beyond, the ANAO will focus on:

- continuing to support sector capability including through provision of further guidance for the sector, noting that this can support Australian Public Service reform initiatives in evaluation, stewardship and Impact Analysis;

- consulting with the Department of Finance (Finance) on how the PGPA Rule is operating and the performance statements audit schedule;

- a response to the Joint Committee of Public Accounts and Audit on the sector’s feedback on the ANAO’s Audit Manual and Audit Strategy documents7;

- assessing Commonwealth entities with regulatory functions against the performance reporting expectations of Finance; and

- continuing to mature the performance statements audit methodology, including through feedback from the sector.

1. Introduction

Chapter coverage

This chapter explains why a Commonwealth entity needs high quality performance information. It then presents the context and progress of the Australian National Audit Office’s (ANAO’s) performance statements audit program.

The context for performance reporting

The Public Governance, Performance and Accountability Act 2013 (PGPA Act) establishes an entity’s corporate plan as its primary planning document and imposes specific obligations and requirements for entity performance reporting. An accountable authority of a Commonwealth entity must prepare annual performance statements that provide information about the entity’s performance in achieving its purposes. Providing meaningful information to the Parliament and the public and meeting high standards of governance, performance and accountability are key objects of the PGPA Act.

Entities’ need for meaningful performance information

Annual performance statements should tell the story of whether the entity is doing its job well. This story should provide entities with an understanding of their business and be meaningful to a reader of the statements. Whether the information presented in an entity’s performance statements is meaningful to users will depend on what users and readers of the statements find useful and valuable.

The role of leadership in developing a performance culture

Effective performance reporting is more than an entity producing a set of annual performance statements that meet the minimum requirements of the PGPA Act and the Public Governance, Performance and Accountability Rule 2014 (PGPA Rule). Performance information should be integral to how an entity plans and operates to achieve its purposes. Strategic and concerted leadership is required to embrace meaningful performance reporting as essential to good management and the effective stewardship of public resources.

The 2022–23 performance statements audit program

There has been some improvement in entities’ processes and capability to develop high quality performance information. The audit program has demonstrated that mandatory annual performance statements audits encourage a culture within entities of long-term investment in the capabilities needed to plan, monitor and report high quality performance information on an ongoing basis.

The context for performance reporting

1.1 Governments make investment decisions to support the achievement of their policy objectives and allocate funding to Commonwealth entities to deliver these objectives through the annual budget process.

1.2 Financial statements of Commonwealth entities report expenditure and financial position, but do not contain all the information needed to measure and assess how well entities have used their allocated funding and public resources in the delivery of government policies and programs and the provision of goods and services. Consequently, Commonwealth entities need to supplement financial information with non-financial performance information8 to:

- enable the government to assess if it is achieving its policy objectives;

- be accountable for, and transparent about, how they use public money;

- monitor and benchmark their performance over time and identify opportunities to improve the programs and services they deliver; and

- support government decision-making.

1.3 The Public Governance, Performance and Accountability Act 2013 (PGPA Act) establishes an entity’s corporate plan as its primary planning document9 and imposes specific obligations and requirements for entity performance reporting. Providing meaningful information to the Parliament and the public and meeting high standards of governance, performance and accountability are key objects of the PGPA Act.10

1.4 The development and use of performance information should be integral to an entity’s strategic planning, budgeting, monitoring and evaluation processes. The right amount of understandable performance information, on the right activities, can be used to promote the achievement of the entity’s purposes11, identify what is working and what areas need improvement and promote accountability to the Parliament, the government and the public for the effective delivery of government policies, programs and services.

1.5 Our audits indicate that entities are using their corporate plans and annual performance statements in different ways and giving them different levels of prominence within the entity. For example, where there is regular monitoring and reporting to senior leadership throughout the year it elevates the level of importance, improving the quality of performance information and reporting.

1.6 Alternatively, if information is only reported as part of the annual performance statements preparation process it can be seen as a compliance exercise and not as an integral part of good management and stewardship of public resources. By way of comparison, it is unlikely that there would be confidence in an entity that did not use its financial information for management and business improvement purposes.

Entities’ need for meaningful performance information

1.7 The measurement and reporting of performance is not something that is done for its own sake. It is a process undertaken to ensure that appropriate and trustworthy information is available, when required, to enable well-informed and evidence-based decisions to be made about how to improve performance and to promote accountability. Understanding gained through good performance information enables entities to continually improve the design and delivery of government policies, programs and services and allocate resources accordingly.

1.8 An Accountable Authority must measure and assess their entity’s performance in achieving its purposes and prepare and present annual performance statements within their annual reports.12 The Public Governance, Performance and Accountability Rule 2014 (PGPA Rule) requires the accountable authority of a Commonwealth entity to include in its corporate plan the entity’s purposes13, key activities and the measures, including targets where appropriate, it will use to assess whether its purposes have been achieved.14

1.9 The PGPA Act does not explicitly define what constitutes meaningful information.15 By design, the framework provides flexibility for each entity to determine its performance information and the structure and format of its annual performance statements. For performance statements to be useful and meaningful, they need to be nuanced for, and owned by, the entity preparing them.

1.10 Annual performance statements should tell the story of how well an entity is doing its job. For a Commonwealth entity to build and report a suite of high quality, relevant and meaningful performance information that tells this story, there are fundamental questions to consider.

- Why does the entity exist, and what is it expected to deliver?16

- What does good performance and success look like, and how will the entity know it is doing a good job?

- How can the entity’s performance be measured reliably over time?

- What performance information would provide a complete picture of an entity’s performance and enable the entity’s performance in achieving its purposes to be effectively measured and assessed?

- Will the entity’s performance statements provide a user, including the Parliament, meaningful information about how well the entity has performed?

1.11 The answers to these questions are key to an entity’s understanding of its business and whether it is using and managing public resources properly to deliver on what is expected.17

1.12 Whether the information presented in an entity’s performance statements is meaningful to users will depend on what users and readers of the statements find useful and valuable. Meaningful information in an entity’s performance statements will enable:

- the Parliament to fulfil its oversight function. The statements should allow members of Parliament to assess what has been achieved; how well it has been achieved; and factors that have impacted this achievement;

- executive government to understand whether its program and policy goals are being achieved and delivering value for money; who is benefitting from its programs and policies; and how it can best prioritise investment of limited public resources;

- the accountable authority to understand whether the entity is:

- operating efficiently and effectively in achieving its purposes and delivering what government and the Parliament expects;

- identifying opportunities to improve business capability and outcomes; and

- promoting accountability and the achievement of the entity’s purposes18; and

- the public to understand the entity’s performance overall and in areas of particular public and political interest.

1.13 This does not mean that the performance statements of an entity will be of equal relevance to all users. However, they can provide a starting point for users to explore and question for their own specific purposes — just as for financial statements where the bottom line is the starting point for analysis.

The role of leadership in developing a performance culture

1.14 Effective performance reporting involves more than an entity producing a set of performance statements that meets the minimum requirements of the framework. Entities require leadership that sponsors performance reporting as essential to good management and governance arrangements that ensure performance information is an integral part of the operation of the entity. In many respects, the success or failure of an entity’s use of performance information will depend on the maturity and sophistication with which the management of that information is handled by leaders and senior managers of an entity.

1.15 Accountable authorities have a duty to govern their entities in a way that promotes the proper use and management of public resources and the achievement of the purposes of the entity.19 One of the objects of the PGPA Act is to meet high standards of governance, performance and accountability and to achieve and demonstrate these standards through providing the Parliament with meaningful performance information.20 Good governance provides the foundation for high performance and is based on accountability, transparency, leadership, integrity and stewardship and in responsiveness to the needs and aspirations of citizens.21

1.16 As with financial reporting, non-financial performance information should be an integral part of the agency’s strategic and operational planning, budgeting, reporting and reviewing processes. Regular monitoring and evaluation of performance information should provide a basis for informed and evidence-based decision-making and accountability.

1.17 The Australian National Audit Office’s (ANAO) performance statements audits continue to indicate that, at least to some extent, Commonwealth entities view performance statements as a compliance exercise to be completed annually.22 There is information reported in entities’ performance statements that is not regularly monitored, reviewed and evaluated at the executive level. By extension, this suggests that this information is not important to the management of the entity and of limited use to an external user in assessing the performance of the entity in achieving its purposes.

1.18 Strategic and concerted leadership is required to embrace meaningful performance reporting as essential to good management and the effective stewardship of public resources. Developing a culture that values and produces high quality performance information and evaluation takes time and perseverance. Recent experience indicates that the strongest incentives for accountable authorities to drive high standards in performance reporting are transparency of performance information and external assurance through an ongoing audit program.23 This report observes some progress in entities’ development of a performance culture.

Performance statements auditing

1.19 The introduction of performance statements audits is the most significant change in Commonwealth public sector auditing since the implementation of performance auditing in the early 1980s. Performance statements audits are an important element of the enhancements to public management and accountability introduced by the PGPA Act and play an important role in building citizen trust in government. They provide the Parliament assurance on an annual basis over the reliability of reporting by entities on their performance.

1.20 The requirement for Australian Government entities to prepare annual performance statements under the PGPA Act commenced from 1 July 2015 with entities preparing annual performance statements for the first time in the 2015–16 reporting period.

1.21 The ANAO was funded as part of the 2021–22 Budget to implement the ongoing program of performance statements audits. This funding establishes assurance of non-financial reporting as a core component of assurance to the Parliament.

1.22 From the 10 audits in 2022–23, the performance statements audit program will expand to 14 audits in 2023–24, 19 audits in 2024–25 and 24 audits in 2025–26. This phased rollout will enable ‘repeat’ entities to improve the quality and reliability of their performance statements and enable the sector to learn from these audits and prepare accordingly.

1.23 Table 1.1 shows the expansion in the number of performance statements audits since the commencement of the ongoing program of audits in 2021–22. In each subsequent year of the rollout, new entities will be added to those already subject to audit. This approach enables the ANAO to continue to leverage the knowledge and expertise gained from auditing an entity to improve the efficiency and effectiveness of the audit process. This improves the sustainability of the audit program and value for money.

Table 1.1: Entities included in ANAO performance statements audit program 2021–24

|

2021–22 |

2022–23 |

2023–24 |

|

The six entities audited in 2021–22 and the following four entities:

|

The 10 entities audited in 2022–23 and the following four entities:

|

Note a: As a result of Machinery of Government changes that took effect from 1 July 2022, the Department of Agriculture, Water and the Environment became the Department of Agriculture, Fisheries and Forestry and the Department of Education, Skills and Employment became the Department of Education.

The 2022–23 performance statements audit program

1.24 The focus of this report is on the 2022–23 performance statements audits of 10 entities. The second year of implementation of the performance statements audit program demonstrated that entities continue to improve the quality of their performance reporting. There has been some improvement in entities’ processes and capability to develop high quality performance information, providing a basis for ongoing improvement in performance reporting.

1.25 Several entities in the 2022–23 performance statements audit program acknowledged the impact and the value of the performance statements audit process.24 The entities observed that the audits had contributed to improved internal governance processes and the quality of performance information.

1.26 The 2022–23 audit program has shown that:

- as intended, there is flexibility in the framework for entities to tailor how they measure, assess and present their performance information;

- entities are generally presenting accurate information in performance statements; and

- entities are using the iterative and educative design of the audit process to resolve prior year audit findings and respond to findings issued at the end of the interim audit phase.

1.27 The 2022–23 audits have also identified common areas of challenge for auditees. In particular, entities have not fully implemented enterprise-wide performance frameworks (see chapter 3).25 As a result, entities often lack clear internal processes to guide how, and what they identify as their purposes, key activities and performance measures, and performance information is not integrated into strategic planning, decision-making and accountability processes. This means that some entities are producing performance information that can be insufficient to provide a complete and meaningful picture of their performance or identify where improvements can be made to improve future performance.

1.28 The issue of whether an entity’s performance information is complete was raised in several 2022–23 performance statements audit findings. Six of the 10 auditees received a finding relating to the completeness of their performance information (see chapter 2).

1.29 Further improvement is required for performance statements to provide meaningful information on an entity’s performance in line with the spirit and intent of the Commonwealth Performance Framework, in addition to annual performance statements that comply with the minimum requirements of the PGPA Act and Rule.

Entities’ engagement with the 2022–23 audits

1.30 The ANAO issued an auditor’s report to most entities by the end of September 2023 (see Figure 4.4) indicating that entities have generally engaged with the performance statements audit process. Chapters 2 and 3 of this report discuss aspects of the timeliness and quality of entities’ engagement, noting those areas done well and where improvements could be made.

1.31 The terms of engagement for each performance statements audit state that the accountable authority is responsible for providing the ANAO with access to all information that is relevant to the preparation of the annual performance statements. The timely provision of this information is key to providing the Parliament with reasonable assurance over whether the entity’s annual performance statements are free from material misstatement in a timely manner. It is important, therefore, that the entity understands and complies with the terms of engagement.

1.32 Two entities in the 2022–23 performance statements audit program — the Department of Health and Aged Care (DoHAC)26 and the Department of Education (Education) — did not provide the ANAO with access on request to information relevant to the preparation of their statements. The entities advised the ANAO that there were legal restrictions to sharing the requested information.

1.33 In August 2023, the Auditor-General wrote (separately) to the accountable authorities of DoHAC and Education to issue formal notices under paragraphs 32(1)(a) and 32(1)(c) of the Auditor-General Act 1997. The notices directed each Secretary to produce to the Auditor-General the requisite information and documents in the department’s custody or under its control.

1.34 The ANAO is advising the Parliament through this report of the Auditor-General’s exercise of formal information gathering powers under section 32 of the Auditor-General Act 1997.

Entities’ resourcing

1.35 Entities’ evidence to the Joint Committee of Public Accounts and Audit (JCPAA) inquiry into the 2021–22 annual performance statements audits noted the resource cost associated with performance statements auditing. The Department of Veterans’ Affairs observed that the audit process is ‘resource intensive’ and that it is ‘constrained by the small pool of capable staff’ in performance reporting.27 Education put the following view:

[T]he volume of questions, requests for meetings and issues placed an unexpected resourcing pressure on DESE as it did not receive specific resourcing to support the audit. Education acknowledges that efficiencies should be realised in future audit processes as its performance information and the ANAO’s audit approach matures.28

1.36 The resource impact on entities, especially when being audited for the first time, reflects under-investment by entities in building their performance frameworks. This is despite legislative obligations requiring accountable authorities to prepare annual performance statements being in place for nearly a decade.29 Chapter 3 of this report comments further on entities’ resourcing for performance reporting.

2023–24 performance statements audit program

1.37 On 26 June 2023, the Auditor-General wrote to the Minister for Finance to propose expanding the performance statements audit program in 2023–24 to include 14 entities (Table 1.1).30 The Minister agreed with the proposal, requesting that the Auditor-General undertake assurance audits of 14 entities’ 2023–24 performance statements under section 40 of the PGPA Act.31

1.38 The Minister for Finance’s early request in July 2023 to conduct the 2023–24 performance statements audits is important to ensure that the selected entities prepare properly for the audit. It also enables the ANAO to commence formal engagement with auditees earlier than was the case for the 2022–23 audits.32

1.39 Early formal engagement with 2023–24 auditees will allow interim audit findings to be issued to each auditee in a timeframe that assists the entity to plan for the 2024–25 reporting period. The ANAO will continue to issue interim audit findings earlier in the performance statements audit cycle such that entities can consider these findings for both the current and upcoming reporting period.

Mandatory audits of annual performance statements

1.40 Conducting annual audits of performance statements ensures that the Parliament receives the same level of assurance on performance statements as it does for financial statements. Currently, the PGPA Act makes provision for annual performance statements to be examined by the Auditor-General at the request of the Minister for Finance or the responsible minister.33 This is a different process to the initiation of financial statements audits which are mandatory and do not require Minister for Finance approval.34

1.41 Annual performance statements must be included in entities’ annual reports. The process of tabling a performance statements audit report in the Parliament differs to the process of tabling a financial statements audit report. For performance statements audit reports, the PGPA Act requires that the requesting Minister table the Auditor-General’s report in the Parliament as soon as practicable after receipt, with a copy of the statements, but it is not included in the annual report (see paragraph 2.7).35 Financial statements and the Auditor-General’s report must be included in the entity’s annual report that is tabled in the Parliament.36

1.42 On three separate occasions, the JCPAA has recommended legislative change to enable the Auditor-General to initiate performance statements audits without the need for approval.37 The most recent recommendation was made in September 2023 as part of the JCPAA’s inquiry into the 2021–22 performance statements audits.

1.43 The ANAO strongly supports legislative change to enable mandatory annual audits of performance statements. Past experience has shown that intermittent, rather than annual, external review of performance information is unlikely to drive the desired level of improvement in performance measurement and reporting. Annual performance statements audits provide an incentive for entities to prepare annual performance statements to the standard necessary to meet the Parliament’s purposes.

1.44 The audit program has demonstrated that mandatory annual audits will promote a culture within entities of long-term investment in the processes and capabilities needed to plan, monitor and report high quality performance information on an ongoing basis.

Emerging context for performance reporting and evaluation

1.45 Consistent with international trends, there have been important recent developments in Australia aimed at enhancing the quality of information reported by public sector entities to explain how well they have used public money to deliver government policies, programs and services and achieve outcomes for the Australian community. This recognises the important role performance reporting can play in maintaining public trust and confidence in the public sector and the government.

Outcomes reporting through a Wellbeing Framework

1.46 For over a decade, there have been efforts internationally to measure wellbeing beyond conventional macroeconomic statistics. The Organisation for Economic Cooperation and Development’s (OECD) Framework for Measuring Wellbeing and Progress has been applied to produce five reports (2010–2020) on wellbeing outcomes in OECD countries. This research uses a range of indicators of wellbeing to gauge ‘whether life is getting better for people’ in these countries.38

1.47 In July 2023, the Australian Government released a statement titled ‘Measuring What Matters: Australia’s First Wellbeing Framework’. The Statement establishes a wellbeing Framework with five broad themes — healthy, secure, sustainable, cohesive, prosperous — and links to an online dashboard that uses 50 indicators of wellbeing.39 In terms of how the Framework is intended to be used, the Statement explains:

Consistent with our international counterparts, we will be looking for opportunities to embed the Framework into government decision making. This will involve guidance for agencies to inform policy development and evaluation. The Framework could also be used in areas of policy that require different levels of government to work together. 40

1.48 The intent of the MWM program is to ensure policies have a wellbeing focus, which it seeks to influence through the new policy formulation and decision-making process. This is distinct from the Commonwealth Performance Framework which focuses on the achievement of entities’ purposes. The Government is considering how to best embed the Wellbeing Framework into prioritisation and decision-making processes. At this stage, there is no alignment between the Wellbeing Framework and corporate reporting activities.

Australian Centre for Evaluation

1.49 The 2019 review of the Australian Public Service (APS) identified that in the future, the APS will require ‘a much stronger focus on research and evaluation in order to identify emerging issues and evaluate what works and why’. The review proposed that a central evaluation function be established to provide guidance and support to agencies on best practice approaches.41

1.50 On 1 July 2023, the Australian Centre for Evaluation was established within Treasury. The government has indicated that the Centre will promote and conduct evaluations, promote the Commonwealth Evaluation Policy42, work with entities to embed evaluation plans in New Policy Proposals and collaborate with governments and experts in Australia and internationally.43

1.51 High-quality performance information is a necessary condition for effective evaluation. Effectively designed performance measures enable an entity to continuously monitor the performance of key activities, obtain regular feedback and collect appropriate data to underpin evaluation activities. Performance statements audits can contribute to improved evaluation function by assisting entities to build a robust evidence base, monitor progress and strengthen data analytic capability to improve their capacity to evaluate their policies and programs.

Impact Analysis

1.52 Impact analysis provides decision-makers with information about the potential and the actual effect of policies and regulations on stakeholder groups.

1.53 The Government’s Impact Analysis Framework is designed to help policymakers identify the relevant policy problem, examine a range of viable options, assess the costs and benefits of the options, and develop the evidence base for well-informed decision making. The Office of Impact Analysis (OIA) within the Department of the Prime Minister and Cabinet aims to ensure that major policy decisions are supported by sound evidence and analysis. The OIA’s role is to ensure compliance with the IA framework and provide guidance and coaching across the sector to assist entities to produce high quality analysis.

1.54 From 1 March 2023, a new Australian Government Guide to Policy Impact Analysis came into effect. The Guide states that an impact analysis is required for:

any policy proposal or action of government, with an expectation of compliance, that would result in a more than minor change in behaviour or impact for people, businesses or community organisations.44

Climate-related disclosures

1.55 In June 2023, the International Sustainability Standards Board issued International Financial Reporting Standards (IFRS) S1 General Requirements for Disclosure of Sustainability Related Financial Information and S2 Climate-related Disclosures. The Standards will focus on the for-profit private sector and provide a common language for disclosing the effect of climate-related risks and opportunities on a company’s prospects.

1.56 As at September 2023, legislation was before the Parliament to give the Australian Accounting Standards Board (AASB) the ability to develop climate-related standards.45 The Australian Government envisages that these standards will align with the requirements in IFRS.46

1.57 The AASB issued an Exposure Draft, ED SR1 Sustainability Reporting Standards – Disclosure of Climate-related Financial Information, which is also based on consideration of the Treasury’s second consultation paper Climate related financial disclosure issued on 27 June 2023. The second Treasury paper proposes a three-phased approach to the application of mandatory disclosure requirements commencing with a limited group of very large entities expanding over three years to apply progressively to smaller entities.

Structure of the report

1.58 This report presents the 2022–23 audit findings and observations (chapter 2), assessments of auditees’ maturity in performance reporting (chapter 3), and the future direction of the ANAO’s performance statements program (chapter 4).

2. Audit results from the 2022–23 performance statements audits

Chapter coverage

This chapter discusses the results from the 2022–23 annual performance statements audits. It outlines the audit conclusions presented in the auditor’s report for each audit as well as key findings and observations on how entities are presenting their performance information.

Audit conclusions and additional matters

The 2022–23 audits indicate improvement from 2021–22 in terms of the reduced proportion of auditees that received a qualified conclusion in an auditor’s report, and the decreased number of measures that were included in the basis for qualified conclusion. Six of the ten 2022–23 auditees received an audit conclusion without modification, compared to three of the six auditees in 2021–22. In 2022–23, four per cent of all auditees’ measures were subject to a qualified conclusion, down from seven per cent in 2021–22.

Six of the 10 auditees received an auditor’s report containing an emphasis of matter paragraph, which draws the reader’s attention to an important matter in the performance statements that is fundamental to users’ understanding of the entity’s performance without modifying the audit conclusion. In 2021–22, one of the six auditor’s reports contained an emphasis of matter paragraph.

One of the 10 auditees received an auditor’s report containing an other matter paragraph to draw the reader’s attention to an issue without modifying the audit conclusion.

Audit findings

A total of 48 findings were reported to entities at the end of the final phase of the 2022–23 performance statements audits. These comprised 16 significant, 13 moderate and 19 minor findings. The resolution of 48 per cent of interim 2022–23 audit findings reflects that entities made effort to resolve findings during the final phase of the audit.

The significant (A) and moderate (B) 2022–23 audit findings fall under five themes:

- improved governance by implementing an enterprise-wide performance framework (issued to four entities);

- complete and meaningful performance information (issued to five entities);

- accuracy and reliability of reported information (issued to five entities);

- usefulness of performance information (issued to two entities); and

- preparation and record keeping processes (issued to three entities).

Observations of entities’ performance information

The main observations of the 10 entities’ performance information include the following:

- on average, an entity reported on a key activity using 2.7 performance measures;

- 41 per cent of all measures in entities’ 2022–23 performance statements were output measures and 40 per cent were effectiveness measures;

- a large majority of most entities’ performance measures are quantitative performance measures; and

- for six of the 10 entities, a majority of their 2022–23 performance measures were identical or comparable to the measures in their 2020–21 corporate plan.

2.1 Performance statements audits improve transparency and provide the Parliament with independent assurance over the quality and reliability of entities’ annual performance statements. They are also designed to identify areas where improvements can be made across the sector by presenting specific findings and recommendations to audited entities.

2.2 Findings and recommendations are communicated to entities at several stages during the audit to enable entities to address identified issues before finalising their performance statements for the reporting period. Where findings remain unresolved, these can be addressed by entities in the following year.

2.3 The audits demonstrate that entities can establish sound practices and improve the standard of their performance reporting processes and their performance information over the reporting period. Chapter 3 of this report assesses the maturity of entities’ processes to report their performance.

2022–23 performance statements audits

2.4 This chapter presents the findings from the 10 audits of entities’ 2022–23 performance statements. It provides detail on the significant and moderate audit findings and outlines the key matters that impacted the audit conclusion.

2.5 The analysis in this chapter refers to ‘repeat’ and ‘new’ entities in the 2022–23 audit program. These categories can be useful to show how the annual audit cycle of performance statements is improving entities’ performance information. The Department of Education, Skills and Employment (DESE) became the Department of Education and the Department of Agriculture, Water and the Environment (DAWE) became the Department of Agriculture, Fisheries and Forestry (DAFF) (rather than newly established) on 1 July 2022 following Machinery of Government changes. These entities are classified as ‘repeat’ entities given their involvement in the 2021–22 audit program.

2.6 The Auditor-General provided auditor’s reports to the Minister for Finance on 22 September, 12 October and 20 December 2023.47 The Auditor-General provided letters to responsible Ministers on the outcomes of the audits on 28 November 2023.48

2.7 The Public Governance Performance and Accountability Act 2013 (PGPA Act) requires that the Minister requesting an audit of an entity’s annual performance statements table a copy of the Auditor-General’s report in each House of Parliament as soon as practicable after receipt.49 The Minister for Finance tabled the reports in tranches, nine weeks and six weeks after the Auditor-General provided the reports to the Minister (see paragraph 2.6).50

Audit conclusions and additional matters

2.8 Overall, the results from the auditor’s reports of the ten 2022–23 performance statements audits are mixed.51 Six of the ten auditees received an auditor’s report without a modified conclusion52: the Attorney-General’s Department (AGD), the Department of Education (Education), the Department of Industry, Science and Resources (DISR), the Department of Social Services (DSS), the Department of the Treasury (the Treasury) and Services Australia. Four entities received an auditor’s report with a qualified conclusion: The Department of Agriculture, Fisheries and Forestry (DAFF), the Department of Infrastructure, Transport, Regional Development, Communications and the Arts (DITRDCA), the Department of Veterans’ Affairs (DVA) and the Department of Health and Aged Care (DoHAC).

2.9 The 2022–23 audits indicate improvement in terms of the number of auditees that received an audit report containing a qualified conclusion, and the number of measures included in the basis for qualified conclusion. Table 2.1 shows that based on the 2021–22 audits, in 2022–23 the proportion of audited entities that received a qualified audit conclusion decreased. The proportion of entities’ measures that were the subject of a modified conclusion also decreased from 2021–22 to 2022–23.

Table 2.1: Summary of audit conclusions

|

Reporting year |

Number of audited entities |

Number of modified audit conclusions |

Measures subject to modified conclusion as % of all entities’ measures |

Measures subject to modified conclusion as % of measures reported by relevant entities |

|

2022–23 |

10 |

4 |

4%a |

9% |

|

2021–22 |

6 |

3 |

7%b |

10% |

Note: This table represents performance measures that were the subject of a modified conclusion in 2022–23. In 2022–23 some modified conclusions relate to the omission of performance information.

Note a: Twelve of the 294 measures reported by the 10 auditees in 2022–23.

Note b: Thirteen of the 199 measures reported by the six auditees in 2021–22.

Source: ANAO analysis.

2.10 Six of the 10 auditees received an audit report containing an Emphasis of Matter paragraph (see paragraph 2.24 and Table 2.2).53 In 2021–22, only one of the six audit reports contained an Emphasis of Matter paragraph.

2.11 The following sections explain the bases for the ANAO’s qualified conclusions and Emphasis of Matter paragraphs.

Bases for qualified conclusion

Department of Agriculture, Forestry and Fisheries

2.12 DAFF’s 2022–23 performance statements reported on 13 performance measures underpinned by 13 targets. A qualified conclusion was issued on DAFF’s annual performance statements due to the omission of performance information for reporting against Objective 1: Industry Growth and Objective 3: Resilience and sustainability; and the biased construct of the measure relating to point-of-entry failures.54

2.13 The Australian National Audit Office (ANAO) identified that DAFF’s 2022–23 performance statements were not complete with respect to:

- Objective 1 (Industry growth), key activity 2 (maintaining and expanding exports and access to international markets) — DAFF reports against a single performance measure relating to point-of-entry failures. The performance statements did not report important information relating to DAFF’s work in expanding exports and access to international markets, which are key activities of the department. Failure to report on this area reduces the ability to assess DAFF’s performance in expanding export market access.

- Objective 3 (Resilience and sustainability), key activity 2 (increase the contribution that agriculture makes to a healthy, sustainable environment) — DAFF reports against a single performance measure relating to the sustainability of agriculture. There is no measure that assesses the resilience of agricultural, fisheries and forestry activities and the statements did not include narrative to explains the department’s rationale for not reporting on this aspect of its performance.

2.14 DAFF’s performance measure on the regulation of exported goods (IG-04) uses point-of-entry failures for meat exports as a proxy for all prescribed goods regulated under the Export Control Act 2020 (ECA) and the Export Control Rules.55 The ECA sets the overarching framework for the regulation of exported goods, including food and agricultural products. DAFF regulates the export of agricultural goods and issues Australian Government export certificates under the ECA and subordinate legislation.56

2.15 Given the definition of exported goods for the purposes of the ECA is broader than meat exports and also includes plants, eggs, dairy and live exports, the ANAO was unable to corroborate DAFF’s view that measuring point-of-entry failures for meat exports is a suitable proxy for DAFF’s overall performance in administering the ECA. The measure did not, therefore, provide an unbiased basis for measuring and assessing DAFF’s performance in regulating exports.

2.16 In addition, under IG-04 relating to the regulation of exported goods, only failures that are directly attributable to the department are reported as point-of-entry failures.57 DAFF’s export regulatory system is implemented and oversighted by establishments registered with DAFF under the ECA, through production and operational procedures that are agreed by DAFF and formalised as approved arrangements under the ECA. In this environment, the risk that point-of-entry failures would be directly attributable to DAFF is reduced, but only measuring failures that are directly attributable to the department, in an environment where the responsibilities are licenced to other parties, adds to the biased construct of the measure.

Department of Health and Aged Care

2.17 DoHAC’s 2022–23 performance statements reported on 35 performance measures underpinned by 70 targets. A qualified conclusion in auditor’s report was issued because the performance information reported against Outcome 3 ‘Ageing and Aged Care’ was not complete and did not enable a user to assess the department’s performance in achieving its purpose in relation to this outcome. In particular:

- The performance measures and analysis for Program 3.2, ‘Aged Care Services’, provides information on the use of Commonwealth Home Support Programme services and Home Care Packages as well as information on the number of residential aged care places available at 30 June 2023. Reporting on the use and availability of services does not provide sufficient information on the ability of older Australians to access appropriate services to assess the Department’s performance in achieving the objective of Program 3.2 to ‘provide choice through a range of flexible options to support older Australians who need assistance’. For example, the Final Report of the Royal Commission into Aged Care Quality and Safety58 contained discussion regarding wait times and the extent to which the support provided aligns with assessed need. The Australian Government Response to the Royal Commission accepted-in-principle recommendation 39: Meeting preferences to age in place, committing to provide immediate access to home care packages to senior Australians with highest needs.59 Health’s performance measures are not sufficient to provide information on these matters.

- The performance measure for Program 3.3, ‘Aged Care Quality’, relates to the quality of support from the Dementia Behaviour Management Advisory Service (DBMAS) and the Severe Behaviour Response Teams (SBRT). The supporting analysis for Program 3.3 also largely relates to the DBMAS and SBRT. The department has not explained how performance information on DBMAS and the SBRT is sufficient to assess the department’s performance in achieving the Program 3.3 objective, which is to ‘support the provision of safe and quality care for older Australians and their choice of care through regulatory activities and collaboration with the aged care sector and older Australians, as well as capacity building and awareness raising activities’. The department has not reported on the quality of other aged care services, including whether older Australians are receiving safe care.

Department of Infrastructure, Transport, Regional Development, Communications and the Arts

2.18 DITRDCA’s 2022–23 performance statements reported on 38 performance measures underpinned by 49 targets.60 A qualified conclusion was issued on DITRDCA’s performance statements because the performance information reported with respect to eight performance measures across three61 (of the department’s six) Outcomes was not complete.

2.19 The department reported that it was unable to assess its performance for either measure62 in Outcome 1, four63 of the five measures in Outcome 3 and the two measures64 in Outcome 4:

- the measures in Outcome 1 and Outcome 3 did not have reliable and verifiable data sources;

- for one65 of the measures in Outcome 3 and one of the Outcome 4 measures, DITRDCA did not implement a sound methodology for calculating the result, resulting in a high risk of bias in the reported result; and

- one66 of the measures in Outcome 3 and the other Outcome 4 measure67 were assessed as not valid indicators given these measures are not within the department’s control or influence.68

Department of Veterans’ Affairs

2.20 DVA’s 2022–23 performance statements reported on 43 performance measures underpinned by 43 targets. A qualified conclusion was issued on DVA’s 2022–23 performance statements because the performance information reported with respect to two measures in Program 3.1: Provide and maintain war graves was not sufficiently complete to allow assessment of the achievement of DVA’s purposes.

2.21 For these measures, the department reported that due to incomplete data, results are unable to be reported. Due to poor data and systems, DVA cannot demonstrate that war graves are being maintained, as expected by government. The measures are material to Outcome 3 and DVA’s purpose. Accordingly, the performance statements do not provide a complete basis to measure and assess DVA’s performance with respect to Outcome 3.

Emphasis of Matter

2.22 Where appropriate, an auditor’s report may include an ‘Emphasis of Matter’ paragraph. The inclusion of this paragraph does not modify the auditor’s conclusion. An ‘Emphasis of Matter’ paragraph is a tool available to auditors to draw the reader’s attention to an important matter presented in the performance statements that, in the auditor’s judgement, is fundamental to the users’ understanding of the information in the performance statements.

2.23 Six of the 10 2022–23 auditor’s reports contained an emphasis of matter paragraph.69 This is presented in Table 2.2.

Table 2.2: 2022–23 Emphasis of Matter paragraphs

|

Entity |

Matter and Implication |

Disclosure in Annual Performance Statements |

|

DAFF |

The ANAO drew attention to the disclosures within the annual performance statements in the Partnering to support fisheries and Sustainable forestry growth sections. DAFF’s performance statements do not include measures of performance relating to fisheries and forestry industries. These disclosures provide information in relation to DAFF’s responsibilities for fisheries and forestry and its assessment of the completeness of the reporting of these functions within the annual performance statements. Without measures on forestry and fisheries, the reader does not have a complete picture of the department’s performance against its purposes. |

Partnering to support fisheriesa Given our focus on longer-term strategic policy and the operational role of AFMA in managing fisheries, we do not have meaningful data to support annual performance measures directly relating to fisheries. This is why we removed performance measure RS-01 from the annual performance statements. Sustainable forestry growth Government programs and policy focus on longer-term outcomes to ensure the supply or manufacture of forestry products. We are developing performance measures focusing on how we administer funding to support sustainable growth of the forestry industry. Our Corporate Plan 2023–24 includes a performance measure relating to the Accelerate Adoption of Wood Processing Innovation program. |

|

Education |

The ANAO drew attention to the information provided by Education in the ‘Changes to our performance measures’ section of the annual performance statements regarding the department’s decision to no longer report on performance measure 023 (PM023), Proportion of researchers who report that access to NCRIS facilities and projects improved their research quality and outputs. The emphasis of matter paragraph draws readers’ attention to the PBS measure no longer reported. Funding for this initiative increased from around $286 million in 2022–23 to over $400 million in 2023–24 and $500 million in 2024–25. The decision not to report against this program means the reader does not have information on the outcomes of the government’s investment in this area. Information can be found in a NCRIS factsheet prepared by the Department (for example, NCRIS Factsheet – Department of Education, Australian Government)b. This information is not audited by the ANAO’s part of performance statements audits. |

After further analysis the department determined that there were significant difficulties in verifying the data used in the measure. Accordingly, the department considers that the measure does not meet the requirements of section 16EA of the Public Governance, Performance and Accountability Rule 2014 (Cth) (PGPA Rule), and will no longer report on PM023.c |

|

DoHAC Matter and Implication 1 |

The ANAO drew attention to the Department’s disclosure in the annual performance statements under the ‘Structure of the Annual Performance Statements’ section that states that the Department sought to undertake quality assurance for all performance measures. Where this was not able to be undertaken, the Department has included a ‘quality assurance’ caveat for the corresponding performance measure. For the following performance measures that include a ‘quality assurance’ caveat, the ANAO drew attention to the specific limitations outlined by the Department for not being able to validate the results presented, as the ANAO agreed with the department’s disclosure and assessment:

The ‘quality assurance’ caveats in DoHAC’s statements reflect there is a risk that there is insufficient evidence of any validation of referenced performance results. |

The department sought to undertake quality assurance for all performance measures. Where this was not able to be undertaken or completed, the relevant ‘quality assurance’ caveat has been included for the corresponding performance measure.d |

|

DoHAC Matter and Implication 2 |

The ANAO drew attention to a disclosure in the annual performance statements under the ‘Structure of the Annual Performance Statements’ section that states: that ‘additional activities that fall below the materiality threshold for having a published performance measure but were published in the Portfolio Budget Statements and Corporate Plan to ensure a fulsome account to Parliament of activities undertaken within appropriations’. The Department has disclosed 119 key activities that do not have accompanying performance measures at the end of the performance narrative for each program in the annual performance statements. DoHAC’s 2022–23 corporate plan identified 189 key activities and 35 performance measures. The department’s 2022–23 performance statements identify only 70 key activities related to performance measures, with the statements disclosing that the removed key activities are ‘under the materiality threshold’. The department does not disclose the specific rationale for not reporting performance for each of the individual removed key activities. It provides a generic statement that they are ‘under the materiality threshold’. |

For the purposes of the 2022–23 Annual Performance Statements, activities are presented as follows:

|

|

DSS Matter and Implication 1

|

The ANAO drew attention to a disclosure within the annual performance statements under the result for the 1800RESPECT component of the Women’s Safety measure. The caveats in DSS’ statements reflect there is an increased risk that the reported results for these measures are not reliable. Accordingly, there is also a risk that service standards specified in agreements are not being met and DSS may be paying for services it is not fully receiving. |

In 2022–23 the department initiated a process for a point in time review of data to validate overall data accuracy and completeness. However, it is acknowledged that the work is not yet completed and as a consequence the department has limited assurance over the accuracy of the reported result of 76.7 per cent of calls answered within 20 seconds. The department will continue to work with providers to improve data assurances moving forward.e |

|

The ANAO drew attention to a disclosure within the annual performance statements under the result for the Support for Carers measures. |

The ‘Carer Wellbeing’ DEX measures are being reported for the first time in 2022–23 and therefore were not part of the 2021–22 independent client survey. As such independent assurance of response bias has not yet been undertaken.f |

|

|

DVA Matter and Implication 1

|

The ANAO drew attention to DVA’s disclosure of changes to the targets for twelve timeliness performance measures related to Outcome 1 from the targets, that were originally set out in the 2022–23 corporate plan, under the heading Changes to DVA’s performance measures in the Introduction section of the performance statements. The timeliness of veterans’ claims processing is of high public importance. The interim report of the Royal Commission into Defence and Veteran Suicide recommended that the Australian Government ‘take urgent and immediate steps to fix problems with the processing of claims for veterans’.g |

A number of changes have been made since the publication of the Corporate Plan 2022–23 in order to:

Details of these changes are set out in Annexure 1: Performance measure changes.h |

|

The ANAO further drew attention to the disclosures in the Analysis of performance against Outcome 1 section of the performance statements that provides additional context for the change in the targets and analysis of DVA’s performance under the revised targets, including the historical trend information. For 5 of the 12 measures, the new targets are below the actual result achieved in the 2021–22. Targets should be realistic and achievable, and should be set with reference to requirements, agreements or requests for funding and reflect legislative requirements where they exist. |

For the full list of disclosures, refer to the DVA 2022–23 Annual Report.h |

|

|

Services Australia Matter and Implication 1 |

The ANAO drew attention to disclosures within the annual performance statements under the result for the measure ‘customers served within 15 minutes’. These disclosures provide information in relation to the limitations of Services Australia’s assurance over the result for the telephony component of this measure. Services Australia has not validated the data from the telephony providers system. Services Australia is not able to combine a single customer’s wait time if that customer is transferred to two or more queues. Issues relating to the timeliness of answering customers by phone and processing customers’ claims have gained parliamentary attention. Further to the information in its 2022–23 performance statements, Services Australia provided data to the Senate in October 2023 on recent trends in call answering and claims processing times. Accurate, reliable reporting on these issues is key to readers’ understanding of Services Australia’s performance. |

In 2022–23, 3.5 million calls were transferred between queues. Calls transferred internally between telephony queues are counted as separate telephone calls with separate wait times. Our systems are unable to combine call wait times once a call is transferred. This may have an impact on the results for this measure. The reported telephony results are based on data from our provider. The agency does not have a process in place to independently validate the data provided.i |

|

Services Australia Matter and Implication 2 |

The ANAO drew attention to disclosures within the annual performance statements under the result for the measure ‘work processed within timeliness standards’. These disclosures are fundamental to the reader’s understanding of the result for this measure. Without a clearly defined basis for including and omitting timeliness standards, there is a risk of bias (intentional or otherwise) in the methodology. |

Whilst all three programs are represented within the measure, not all processing work types within these programs are captured. This measure does not capture the full breadth of work processed by the agency. As new timeliness standards are agreed with partner agencies, the measure will be updated to incorporate these new work types. Start dates for new timeliness standards will be negotiated with partner agencies and included in the scope of this measure once agreed. We have been unable to identify the level of bias arising from the application of timeliness standards that are included or excluded from the measure.j |

Note a: Department of Agriculture, Fisheries and Forestry, 2022–23 Annual Report, p. 10–11, [Internet], available from https://www.agriculture.gov.au/sites/default/files/documents/Annual%20Report%202022-23%20final.pdf (accessed 13 November 2023).

Note b: Department of Education, ‘National Collaborative Research Infrastructure Strategy (NCRIS)’, Factsheet, 19 July 2022, [Internet], available from https://www.education.gov.au/national-research-infrastructure/resources/ncris-factsheet (accessed on 31 December 2023).

Note c: Department of Education, 2022–23 Annual Report, p. 31, [Internet], available from https://www.education.gov.au/about-department/resources/department-education-202223-annual-report (accessed 13 November 2023).

Note d: Department of Health and Aged Care, 2022–23 Annual Report, p. 25, [Internet], available from department-of-health-and-aged-care-annual-report-2022-23_0.pdf (accessed 15 December 2023).

Note e: Department of Social Services, 2022–23 Annual Report, p. 65, [Internet], available from https://www.dss.gov.au/sites/default/files/documents/10_2023/dss-annual-report-published-version_0.pdf (accessed 13 November 2023).

Note f: Department of Social Services, 2022–23 Annual Report, p. 85, [Internet], dss.gov.au/sites/default/files/documents/10_2023/dss-annual-report-published-version_0.pdf (accessed 13 November 2023).

Note g: Royal Commission into Defence and Veteran Suicide, Interim Report, 11 August 2022, Executive Summary, paragraph 18, [Internet], available from https://defenceveteransuicide.royalcommission.gov.au/publications/royal-commission-defence-and-veteran-suicide-interim-report, (accessed 5 December 2023).

Note h: Department of Veterans’ Affairs, 2022–23 Annual Report [Internet], available from https://www.transparency.gov.au/publications/veterans-s-affairs/department-of-veterans-affairs/department-of-veterans-affairs-annual-report-2022-23/04-annual-performance-statements/introduction (accessed 13 November 2023).

Note i: Services Australia, 2022–23 Annual Report, p. 33 [Internet], available from https://www.servicesaustralia.gov.au/sites/default/files/2023-10/annual-report-2022-23.pdf (accessed 13 November 2023).

Note j: Services Australia, 2022–23 Annual Report, p. 38 [Internet], available from https://www.servicesaustralia.gov.au/sites/default/files/2023-10/annual-report-2022-23.pdf (accessed 13 November 2023).

Source: ANAO analysis.

Other matter

2.24 An auditor’s report may also refer to ‘other matters’ to draw a reader’s attention to an issue without modifying the audit conclusion.70 DoHAC’s auditor’s report contained the following ‘other matter’:

Table 2.3: 2022–23 Other Matter

|

Entity |

Matter and Implication |

Annual Performance Statements Disclosure |

|

DoHAC |

The 2022–23 October Portfolio Budget Statements and the Department’s 2022–23 Corporate Plan included the ‘Closing the Gap’ performance measure relating to the healthy birthweight of First Nations babies in Program 1.3 ‘Aboriginal and Torres Strait Islander Health’ as follows: By 2031, increase the proportion of First Nations babies with a healthy birthweight to 91%. This performance measure was not reported on in Program 1.3 ‘Aboriginal and Torres Strait Islander Health’ in the annual performance statements. Instead, the Department developed an alternative measure that enabled it to report on the number of First Nations babies that have a healthy birthweight, being: Of First Nations babies who attend First Nations primary health care services, increase in the number of those that have a healthy birthweight. The Department obtained the data for the reported measure result from the Australian Institute of Health and Welfare (AIHW). The Department did not disclose in the annual performance statements that the AIHW had disclosed potential risks with data collection that may impact the accuracy of the reported results. The extent to which these risks occur is not known or adjusted for by the AIHW. |

As data would not have been available for the purposes of reporting on the measure that was published in the 2022–23 October Portfolio Budget Statement and Corporate Plan, an alternative measure has been developed which will enable the department to report on the number of First Nations babies that have healthy birthweight.a |

Note a: Department of Health and Aged Care, 2022–23 Annual Report, p. 41, [Internet], available from https://www.health.gov.au/sites/default/files/2023-10/department-of-health-and-aged-care-annual-report-2022-23_0.pdf (accessed 15 December 2023).

Source: ANAO analysis.

Audit findings

2.25 Audit findings are raised in response to the identification of risks to an entity’s performance statements preparation, including where performance measures do not adequately measure the entity’s performance and prior year findings have not been satisfactorily addressed. The rating scale for findings for the 2022–23 audit program is presented in Appendix 2.