1. Background

1.1 Procurement of goods and services is an important and substantial activity for Australian Commonwealth entities to achieve their objectives. The Department of Finance's most recent publication on 'Statistics on Australian Government Procurement Contracts' reported in that in 2016–17, 64 092 contract notices were published on AusTender with a total value of $47.4 billion.

1.2 Each reporting entity is responsible for the accurate and timely reporting of contracts on AusTender.

1.3 Inaccurate contract reporting has been discussed in numerous ANAO audits. Most recently, the audit of Limited Tender Procurement found that only 41 of 155 contracts examined, correctly reported all details on AusTender. Common issues included inaccuracies in contract dates, contract values, procurement method, and categories of procurement.

1.4 This report covers a range of themes and analysis of the Australian Government's centralised publication of contract notices. The report aims to provide insight and information addressing the following areas:

- the volume and value of Government procurement contracts by entity, product/service categories, and other characteristics;

- entities' procurement contract behaviour in regards to the timing of procurements during each financial year, their use of procurement methods and confidentiality clauses, and amendments to contracts;

- accuracy and timeliness of entities' procurement contract reporting; and

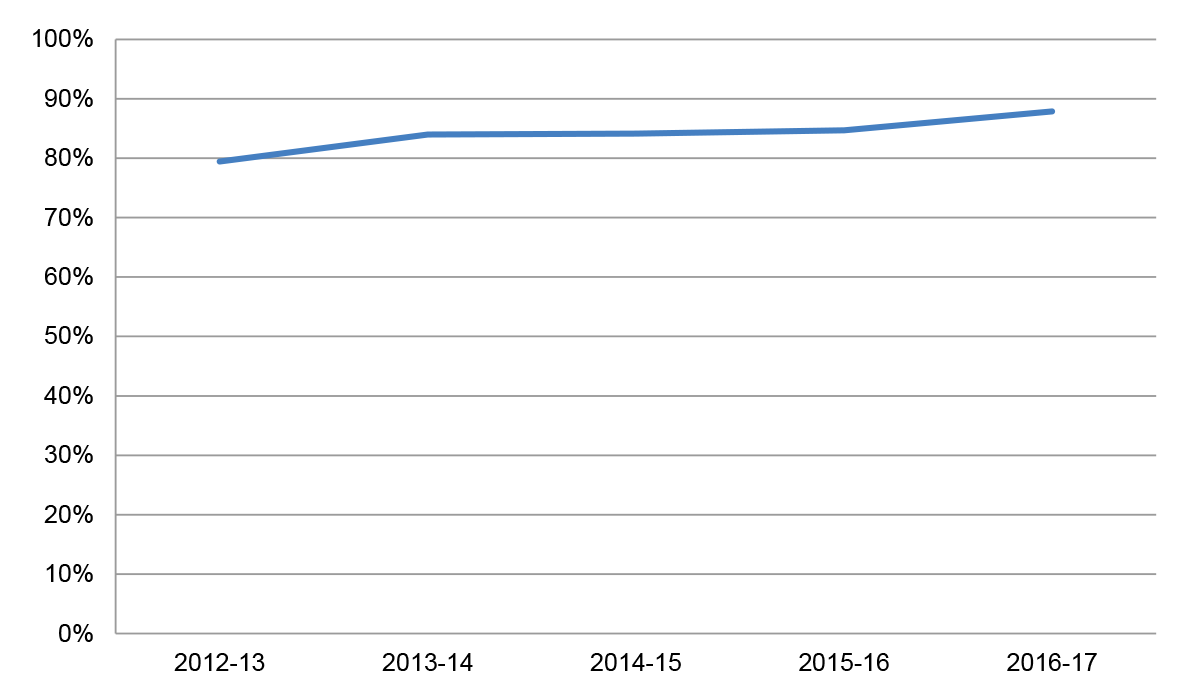

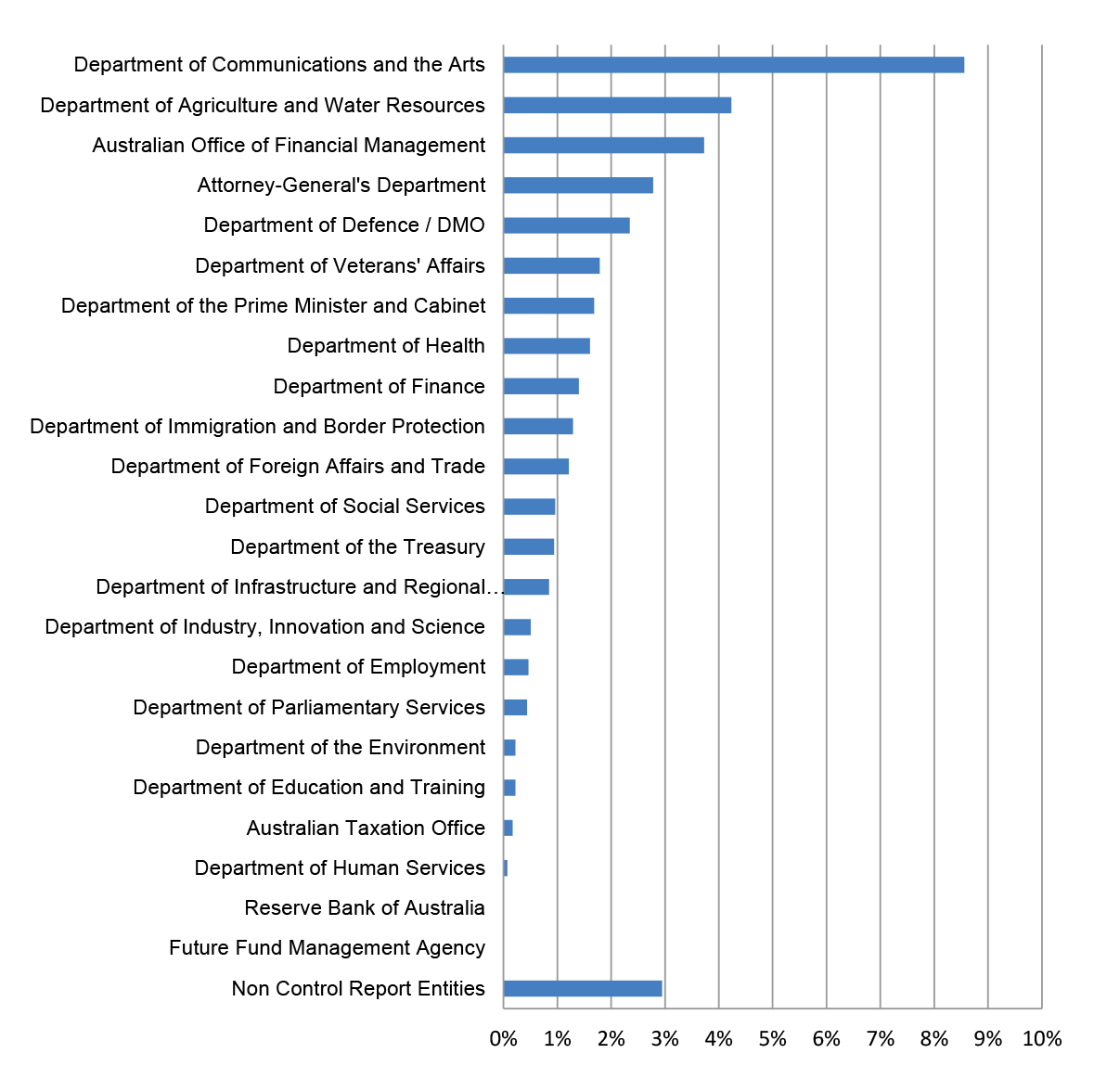

- reporting on the number and value of procurement contracts undertaken with Small to Medium Enterprises (SMEs).

2. Procurement contracts by entity

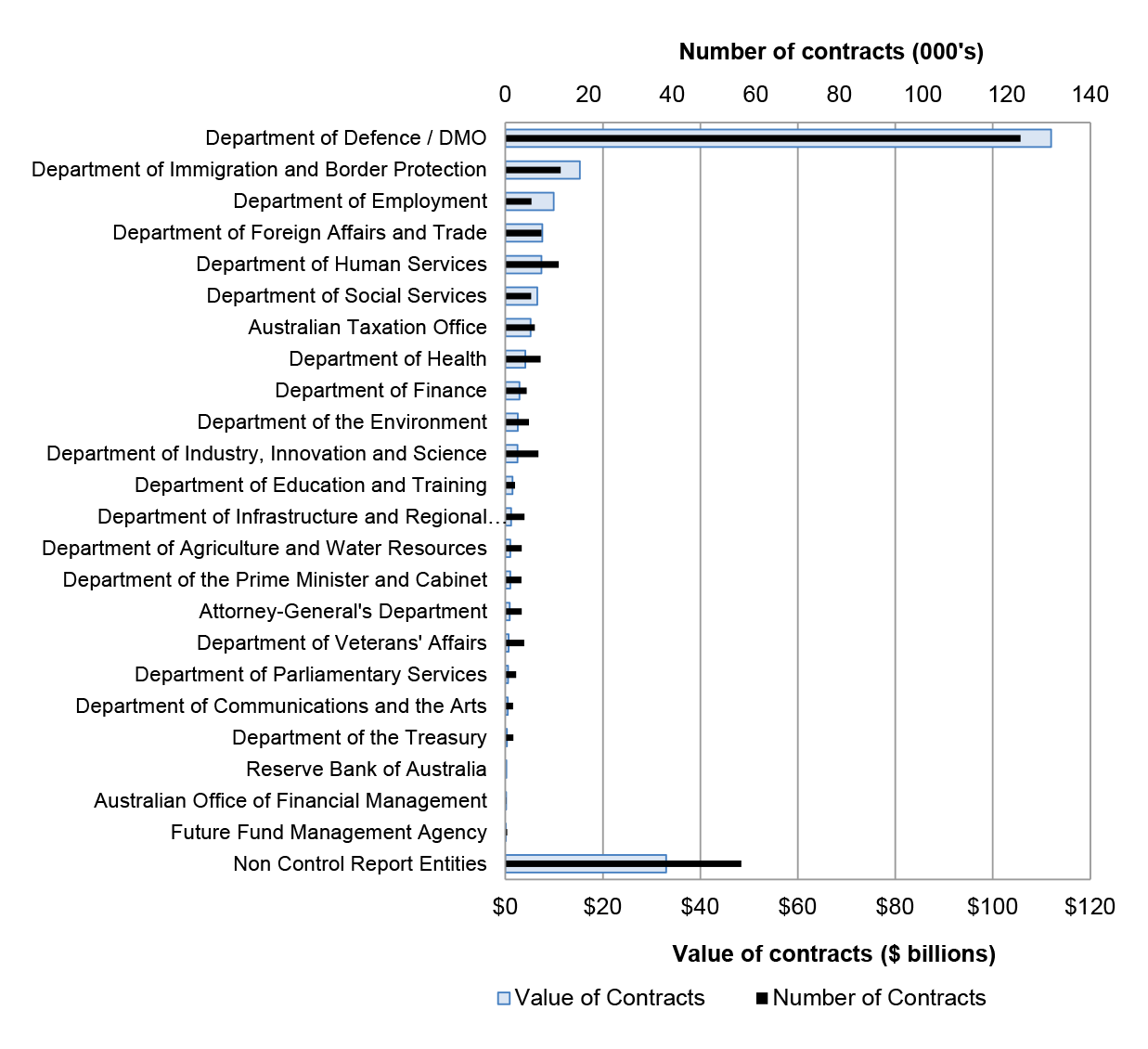

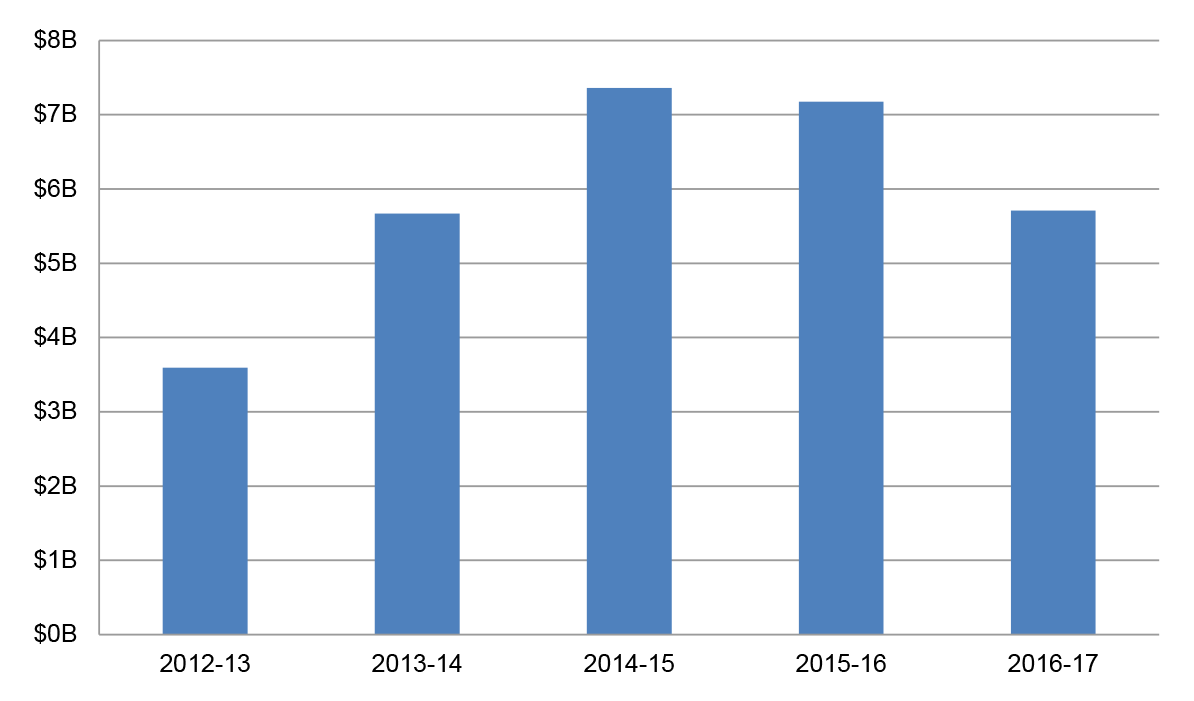

2.1 Figure 2.1 shows the total number and value of contracts with a listed start date in the period 2012–13 to 2016–17. The ANAO has aggregated contracts where entities have published multiple contract notices for purchases that relate to the same contract.

Figure 2.1: Number of contracts and value of contracts by entity (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

Table 2.1: Number of contracts and value of contracts by entity (2012–13 to 2016–17)

|

Attorney-General's Department

|

3,870

|

866,021

|

|

Australian Office of Financial Management

|

161

|

145,197

|

|

Australian Taxation Office

|

7,028

|

5,163,591

|

|

Department of Agriculture and Water Resources

|

3,906

|

1,013,731

|

|

Department of Communications and the Arts

|

1,849

|

463,406

|

|

Department of Defence / DMO

|

123,319

|

111,963,583

|

|

Department of Education and Training

|

2,279

|

1,466,787

|

|

Department of Employment

|

6,250

|

9,905,288

|

|

Department of Finance

|

5,105

|

2,905,746

|

|

Department of Foreign Affairs and Trade

|

8,601

|

7,561,204

|

|

Department of Health

|

8,418

|

4,093,154

|

|

Department of Human Services

|

12,789

|

7,397,857

|

|

Department of Immigration and Border Protection

|

13,198

|

15,266,862

|

|

Department of Industry, Innovation and Science

|

7,917

|

2,481,862

|

|

Department of Infrastructure and Regional Development

|

4,536

|

1,174,850

|

|

Department of Parliamentary Services

|

2,581

|

536,042

|

|

Department of Social Services

|

6,147

|

6,543,660

|

|

Department of the Environment

|

5,658

|

2,553,943

|

|

Department of the Prime Minister and Cabinet

|

3,853

|

976,467

|

|

Department of the Treasury

|

1,926

|

332,467

|

|

Department of Veterans' Affairs

|

4,520

|

674,600

|

|

Future Fund Management Agency

|

432

|

83,647

|

|

Non Control Report Entities

|

56,497

|

33,000,701

|

|

Reserve Bank of Australia

|

27

|

224,079

|

|

Total

|

290,867

|

216,794,744a

|

| |

|

|

Note a: Figures in table may not sum due to rounding.

Source: ANAO analysis of AusTender data.

3. Procurement contract categories (Products and Services)

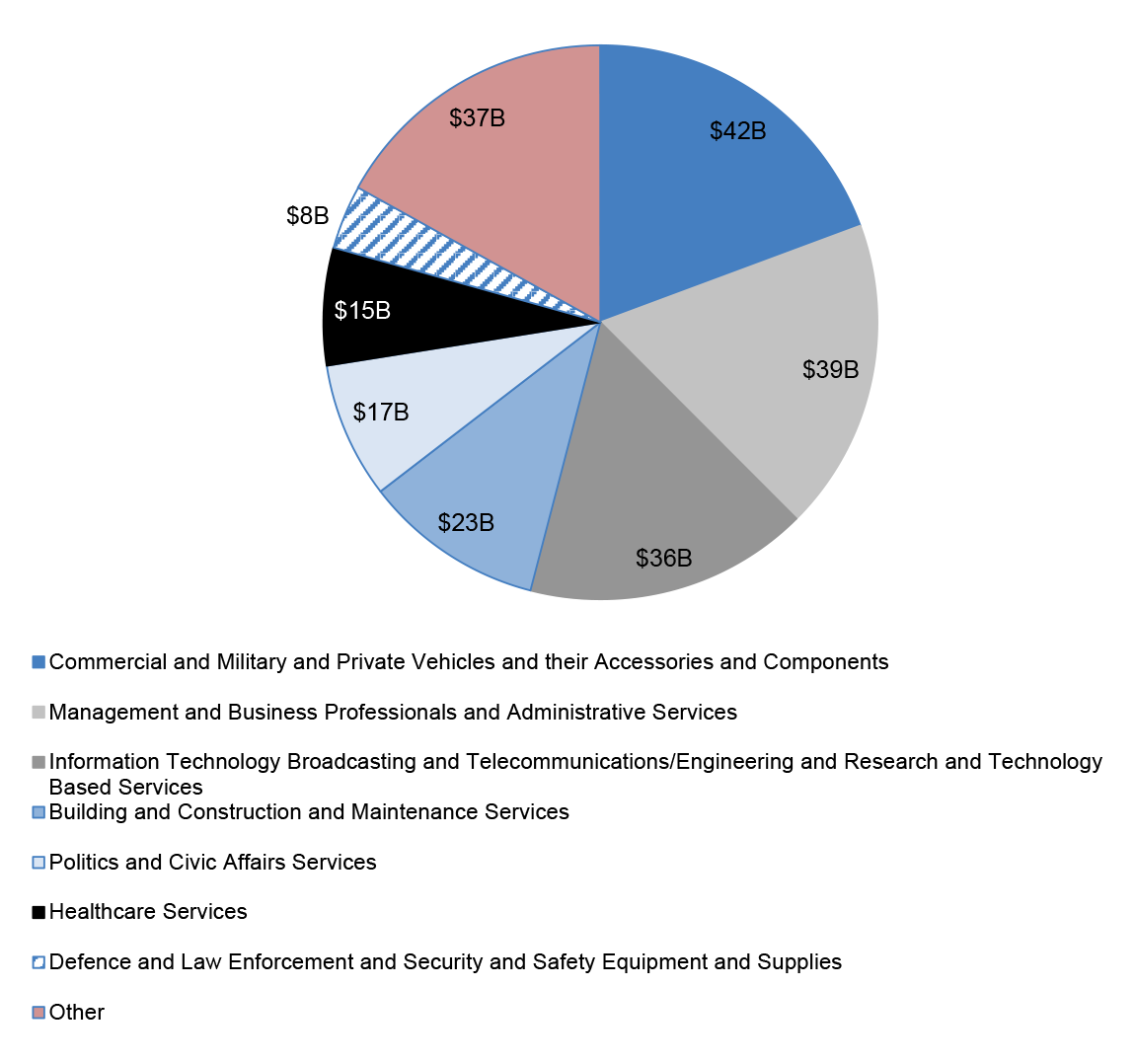

3.1 Figures and Tables below show the classification of contracts based on Department of Finance's customised United Nations Standard Products and Services Code.

Figure 3.1: Contract values by product and services category (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

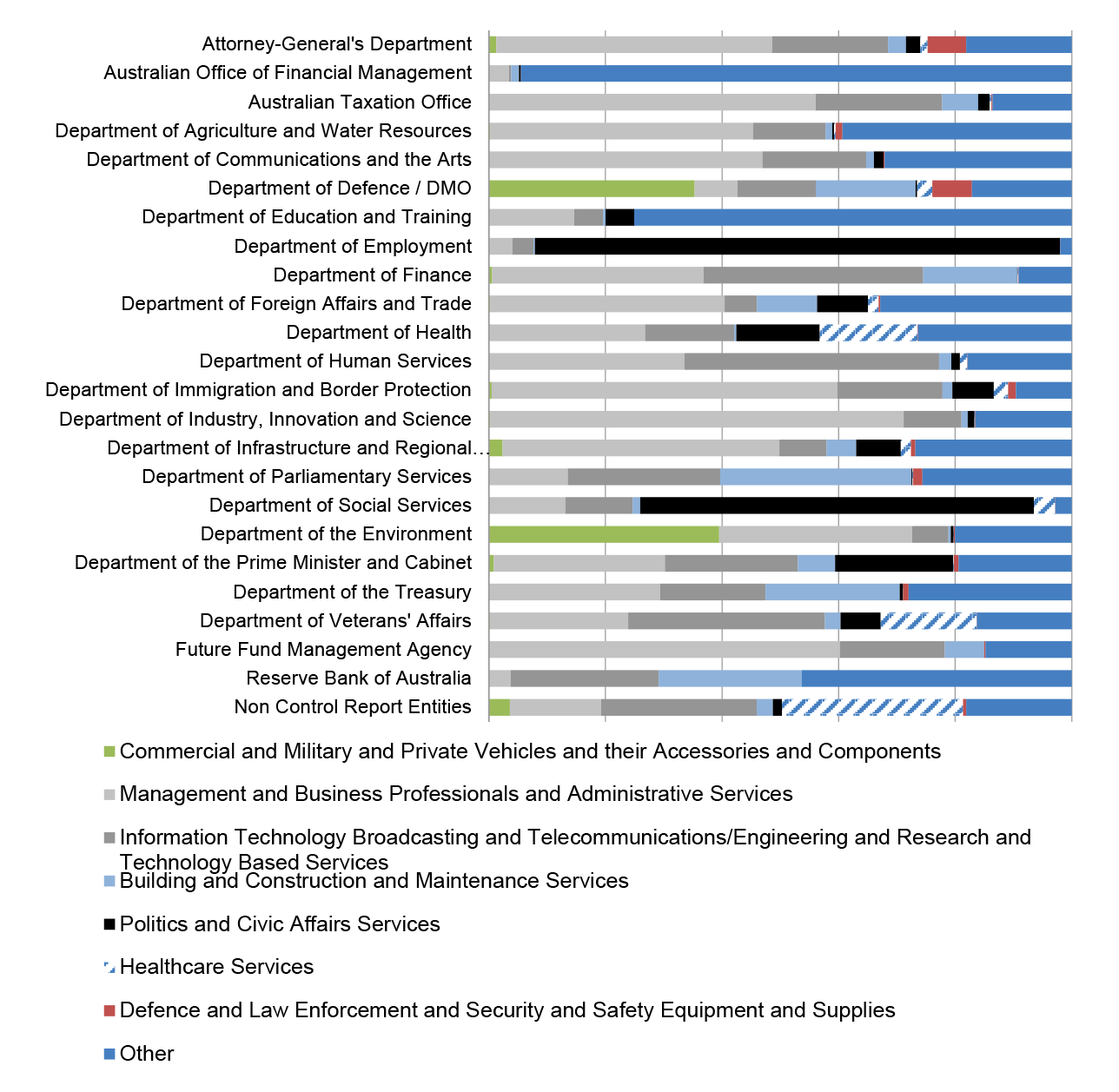

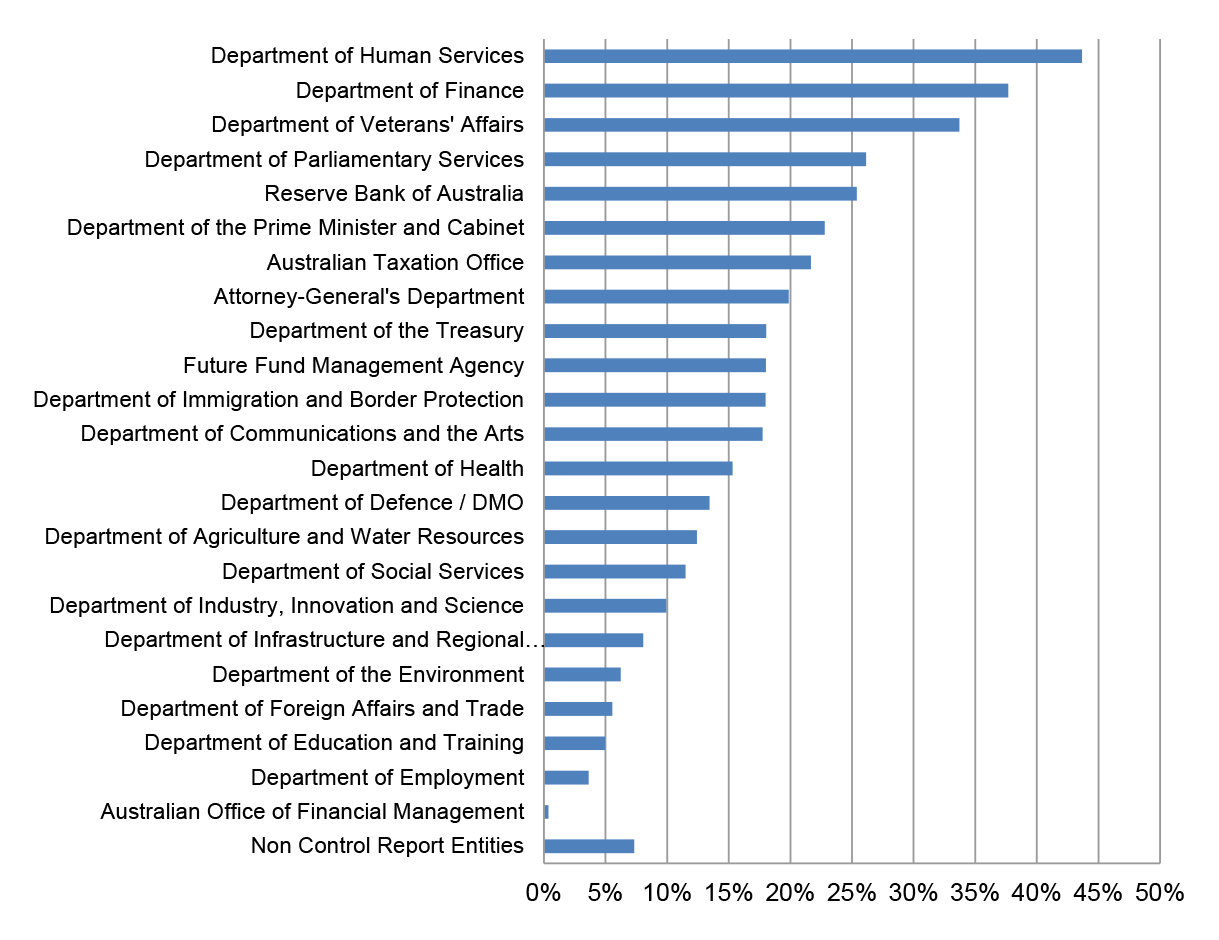

Figure 3.2: Proportion of contract value by entity (2012–2013 to 2016–17)

Source: ANAO analysis of AusTender data.

Table 3.1: Largest product and service categories of contract value by financial year (categories with five-year totals greater than $5 billion – 2012–13 to 2016–17) ($000's)

|

Commercial and Military and Private Vehicles and their Accessories and Components

|

9,695,489

|

8,136,624

|

9,364,908

|

10,421,762

|

4,289,032

|

41,907,815

|

|

Management and Business Professionals and Administrative Services

|

8,585,409

|

7,536,104

|

10,355,005

|

7,109,743

|

5,832,384

|

39,418,644

|

|

Information Technology Broadcasting and Telecommunications/Engineering and Research and Technology Based Servicesb

|

9,977,054

|

5,667,364

|

7,360,962

|

7,175,849

|

5,707,465

|

35,888,695

|

|

Building and Construction and Maintenance Services

|

2,684,062

|

2,288,719

|

9,578,568

|

3,963,237

|

4,233,700

|

22,748,285

|

|

Politics and Civic Affairs Services

|

1,552,581

|

4,847,937

|

798,106

|

9,441,672

|

562,084

|

17,202,381

|

|

Healthcare Services

|

3,459,557

|

243,929

|

1,552,659

|

325,369

|

9,255,727

|

14,837,241

|

|

Defence and Law Enforcement and Security and Safety Equipment and Supplies

|

795,670

|

1,084,897

|

1,876,394

|

2,213,538

|

2,147,554

|

8,118,054

|

|

Otherc

|

8,479,081

|

7,837,171

|

5,552,271

|

9,821,092

|

4,984,016

|

36,673,630

|

|

Totala

|

45,228,905

|

37,642,745

|

46,438,872

|

50,472,261

|

37,011,961

|

216,794,744

|

| |

|

|

|

|

|

|

Note a: Figures in table may not sum due to rounding.

Note b: ANAO has combined the categories of 'Information Technology Broadcasting and Telecommunications' and 'Engineering and Research and Technology Based Services'.

Note c: Other includes all other categories of contracts.

Source: ANAO analysis of AusTender data.

4. IT broadcasting, telecommunications, technology based services, engineering and research

4.1 This chapter shows contracts that entities have classified as either 'IT Broadcasting, Telecommunications' or 'Engineering and Research and Technology Based Services' using Department of Finance's customised United Nations Standard Products and Services Code.

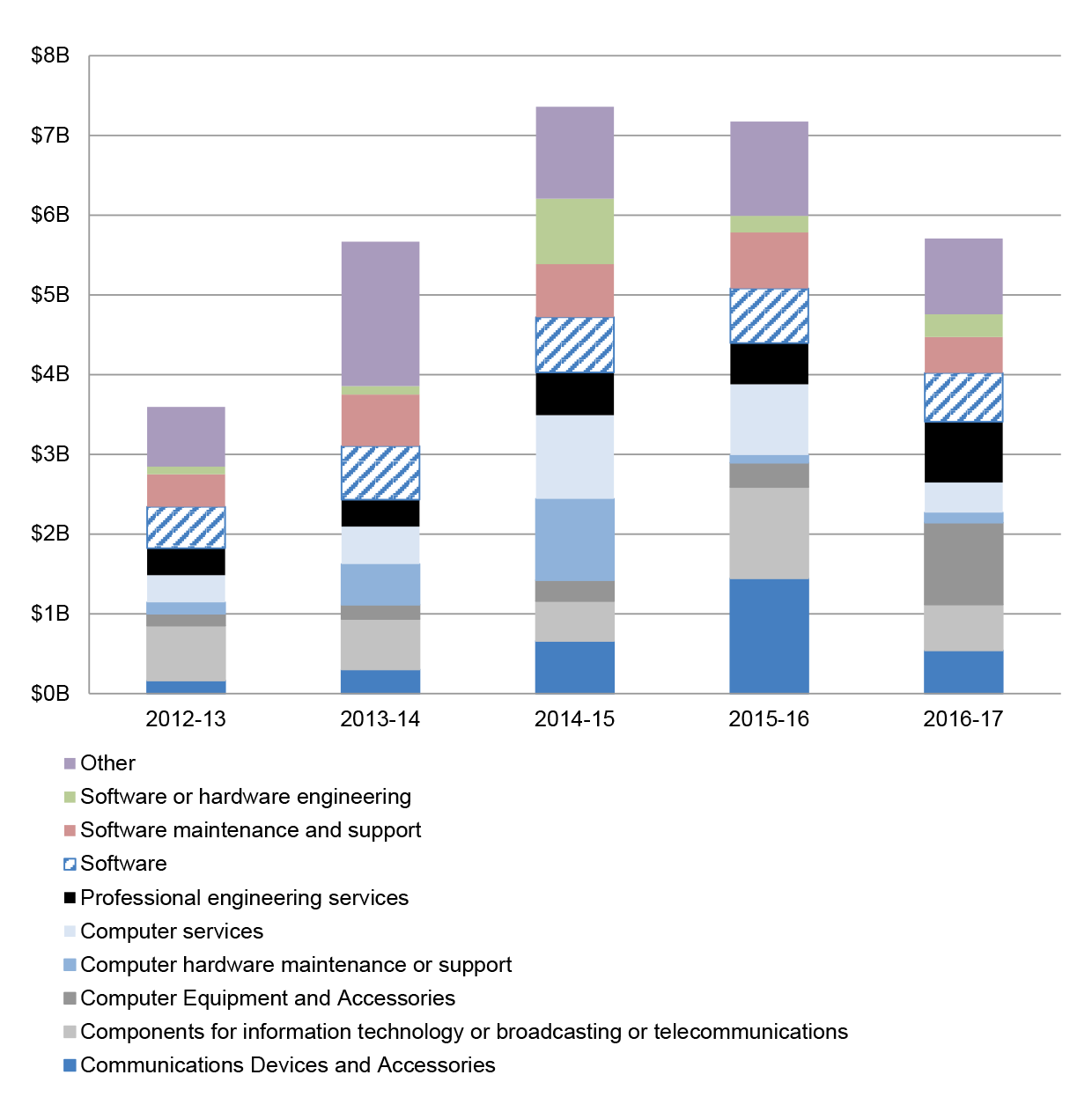

Figure 4.1: IT, telecommunications, tech and engineering contract value by financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

Figure 4.2: Contract value categorised as IT, broadcasting, telecommunications, or engineering and research and technology based services as a percentage of total entity contract value (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

Table 4.1: IT, broadcasting, telecommunications, or engineering and research and technology based services contract value 2012–13 to 2016–17

|

Department of Defence / DMO

|

15,058,177

|

|

Department of Human Services

|

3,230,632

|

|

Department of Immigration and Border Protection

|

2,747,713

|

|

Australian Taxation Office

|

1,119,242

|

|

Department of Finance

|

1,094,791

|

|

Department of Social Services

|

752,408

|

|

Department of Health

|

626,414

|

|

Department of Foreign Affairs and Trade

|

419,820

|

|

Department of Employment

|

358,717

|

|

Department of Industry, Innovation and Science

|

246,366

|

|

Department of Veterans' Affairs

|

227,468

|

|

Department of the Prime Minister and Cabinet

|

222,534

|

|

Attorney-General's Department

|

172,022

|

|

Department of the Environment

|

159,019

|

|

Department of Parliamentary Services

|

140,166

|

|

Department of Agriculture and Water Resources

|

125,763

|

|

Department of Infrastructure and Regional Development

|

94,613

|

|

Department of Communications and the Arts

|

82,270

|

|

Department of Education and Training

|

72,902

|

|

Department of the Treasury

|

60,005

|

|

Reserve Bank of Australia

|

56,902

|

|

Future Fund Management Agency

|

15,070

|

|

Australian Office of Financial Management

|

520

|

|

Non Control Report Entities

|

2,421,312

|

|

Total

|

29,504,845a

|

| |

|

Note a: Figures in table may not sum due to rounding.

Source: ANAO analysis of AusTender data.

4.2 Table 4.2 identifies the largest suppliers by contract value categorised as IT, Broadcasting, Telecommunications, or Engineering and Research and Technology Based Services in the last five financial years (those with greater than $300 million in contract value). The total contract value with government for each supplier, regardless of the product/service category is also provided.

4.3 Contracts for suppliers listed below have been identified and aggregated using both the Australian Business Number listed on the AusTender contract notice and a keyword match of the Supplier Name field.

Table 4.2: Largest IT, broadcasting, telecommunications, or engineering and research and technology based services suppliers to Government (2012–13 to 2016–17)

|

IBM

|

692

|

2,142,256

|

2,325,307

|

|

Boeing

|

165

|

1,601,297

|

4,209,267

|

|

Lockheed Martin Australia

|

260

|

1,132,692

|

1,457,564

|

|

Fujitsu

|

1092

|

961,386

|

1,041,298

|

|

Abacus Innovations

|

133

|

893,707

|

1,052,543

|

|

Data#3

|

1689

|

883,030

|

902,807

|

|

Telstra Corporation

|

1091

|

660,438

|

2,816,866

|

|

Hewlett Packard

|

1517

|

597,180

|

658,655

|

|

FMS Account (Foreign Military Sales)

|

50

|

585,944

|

10,350,755

|

|

Raytheon

|

238

|

543,641

|

2,044,325

|

|

Thales

|

783

|

535,597

|

6,411,119

|

|

Oracle Corporation

|

674

|

532,681

|

544,065

|

|

Accenture

|

127

|

485,423

|

1,190,205

|

|

Harris Corporation

|

186

|

457,575

|

500,629

|

|

Elbit Systems

|

39

|

443,450

|

454,976

|

|

Datacom Systems

|

336

|

425,959

|

583,322

|

|

BAE Systems

|

699

|

415,802

|

4,063,562

|

|

SAP Australia

|

284

|

387,410

|

394,814

|

|

Optus

|

281

|

344,821

|

567,897

|

|

Dell

|

1457

|

335,238

|

361,040

|

|

Unisys

|

61

|

318,332

|

352,844

|

|

CSC

|

171

|

306,429

|

388,472

|

|

Dimension Data

|

1225

|

306,361

|

461,873

|

| |

|

|

|

Source: ANAO analysis of AusTender data.

4.4 Figure 4.3 and Table 4.3 identify the largest product/service sub-categories within IT, Broadcasting, Telecommunications, or Engineering and Research and Technology Based Services by contract value in the last five financial years.

Figure 4.3: Largest product/service sub-categories within IT, broadcasting, telecommunications, or engineering and research and technology based services by financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

Table 4.3: Largest product/service sub-categories within IT, broadcasting, telecommunications, or engineering and research and technology based services by financial year (2012–13 to 2016–17)

|

Components for information technology or broadcasting or telecommunications

|

3,536,994

|

|

Software

|

3,181,791

|

|

Computer services

|

3,127,963

|

|

Communications Devices and Accessories

|

3,120,587

|

|

Software maintenance and support

|

2,873,133

|

|

Professional engineering services

|

2,488,495

|

|

Computer Equipment and Accessories

|

1,919,184

|

|

Computer hardware maintenance or support

|

1,896,175

|

|

Software or hardware engineering

|

1,515,304

|

|

Other

|

5,845,218

|

|

Total

|

29,504,845a

|

| |

|

Note a: Figures in table may not sum due to rounding.

Source: ANAO analysis of AusTender data.

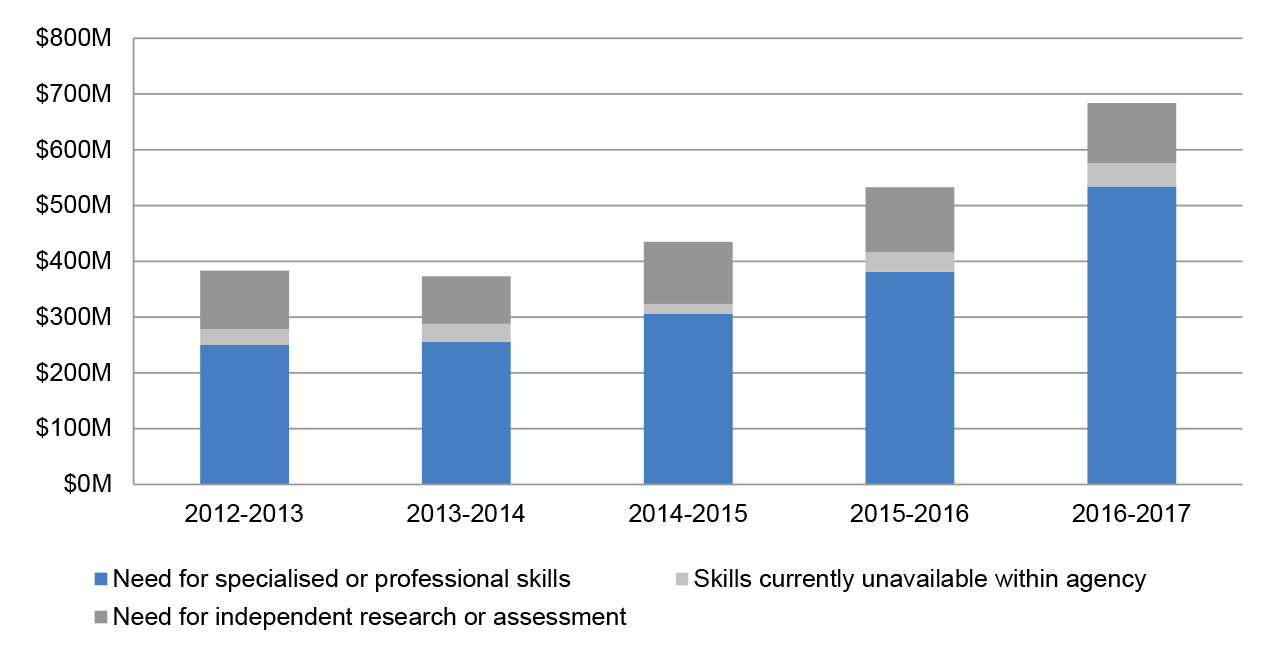

5. Consultancies and management advice

5.1 Contracts relating to consultancies are required to be identified on AusTender via the use of a 'Consultancy Flag' field, together with the supporting reason for the consultancy. Guidance released by the Department of Finance indicates contracts should be reported as consultancies when:

- the contract involves the development of an intellectual output that assists with decision making;

- the intellectual output represents the independent view of the service provider; and

- the output is the sole or majority element of the contract in terms of relative value or importance.

5.2 Entities are required identify the reason for the consultancy from the following list:

- need for specialised or professional skills;

- skills currently unavailable within agency; or

- need for independent research or assessment.

Figure 5.1: Consultancy contract value by consultancy reason and financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

5.3 Table 5.1 identifies the largest suppliers by value of contracts flagged as consultancy in the last five financial years. The table also shows the total value of contracts that each supplier has received from government, regardless of whether it was flagged as a consultancy.

Table 5.1: Largest suppliers by value of consultancy contracts (2012–13 to 2016–17)

|

PwC

|

411

|

174,439

|

523,532

|

|

Ernst & Young

|

350

|

129,187

|

422,422

|

|

KPMG

|

512

|

118,201

|

620,026

|

|

Deloitte

|

344

|

80,320

|

364,818

|

|

Accenture

|

22

|

39,014

|

1,190,205

|

|

URS Corporation

|

219

|

29,883

|

906,403

|

|

Australian Government Solicitor

|

588

|

29,499

|

480,454

|

|

Boston Consulting Group

|

21

|

29,224

|

77,745

|

|

Clayton UTZ

|

250

|

28,316

|

110,580

|

|

ASC (formerly the Australian Submarine Corporation)

|

2

|

27,718

|

3,492,285

|

|

GHD

|

91

|

25,593

|

190,056

|

|

Social Research Centre

|

25

|

24,634

|

47,332

|

|

Watpac Construction

|

1

|

23,975

|

406,662

|

|

St Hilliers Property

|

1

|

23,755

|

232,814

|

|

Microsoft

|

38

|

22,472

|

245,944

|

|

Partners In Performance

|

2

|

19,901

|

19,901

|

|

Griffith University

|

58

|

18,870

|

30,195

|

|

CSIRO

|

116

|

18,479

|

138,887

|

|

DMV Consulting

|

7

|

18,466

|

83,765

|

|

AECOM Services

|

52

|

18,136

|

172,637

|

| |

|

|

|

Source: ANAO analysis of AusTender data.

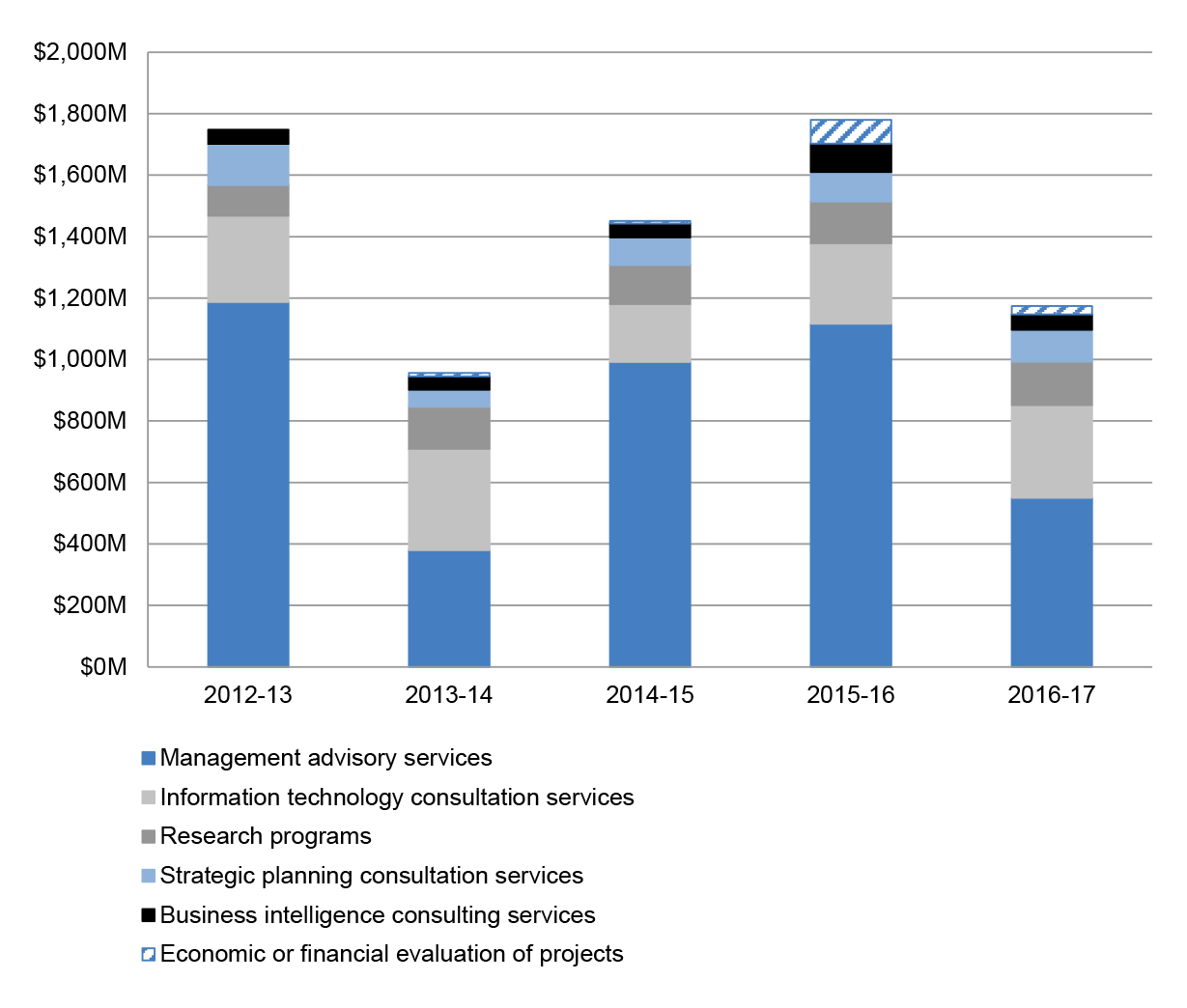

5.4 ANAO identified the largest six product and services sub-categories with contracts flagged as consultancies. These categories make up approximately 47 per cent of the value of contracts flagged as consultancies. However, almost 85 per cent of contract value in these categories belongs to contracts not flagged in AusTender as consultancy. The following analysis shows the contract value of these six service categories, regardless of the consultancy flag.

Figure 5.2: Largest six advisory and consultation categories by financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

5.5 Using the six categories identified above, Table 5.2 shows the largest suppliers by the value of contracts in these categories. The table also shows the total value of contracts for each supplier regardless of product/service category.

Table 5.2: Largest suppliers by value of contracts for the largest six advisory and consultation categories (2012–13 to 2016–17)

|

Cardno

|

42

|

466,973

|

867,688

|

|

Accenture

|

83

|

309,192

|

1,190,205

|

|

Colin Joss & Co

|

3

|

305,524

|

352,615

|

|

Abt JTA

|

20

|

302,403

|

761,901

|

|

Serco Global Services

|

1

|

246,646

|

246,646

|

|

KPMG

|

539

|

192,484

|

620,026

|

|

PwC

|

367

|

186,613

|

523,532

|

|

SMEC International

|

4

|

177,723

|

318,792

|

|

Ernst & Young

|

303

|

163,274

|

422,422

|

|

Baulderstone Hornibrook

|

2

|

162,946

|

425,137

|

|

Deloitte

|

364

|

149,427

|

364,818

|

|

Bechtel Management

|

2

|

107,132

|

107,132

|

|

Stellar Asia Pacific

|

1

|

96,263

|

96,263

|

|

Palladium International

|

13

|

87,463

|

491,544

|

|

GRM International

|

28

|

87,355

|

112,617

|

|

URS Corporation

|

44

|

63,312

|

906,403

|

|

DMV Consulting

|

28

|

59,371

|

83,765

|

|

Salmat

|

3

|

56,056

|

75,136

|

|

Microsoft

|

95

|

55,104

|

245,944

|

|

Nova

|

34

|

55,064

|

353,188

|

| |

|

|

|

Source: ANAO analysis of AusTender data.

5.6 For both suppliers and service categories with the largest value of contracts flagged as consultancies, analysis in this chapter shows a substantial difference in the value of contracts identified in AusTender using the 'consultancy' flag and the total value of contracts for the identified suppliers and categories.

5.7 Many of these suppliers publically report consultancy as a substantial component of their business. Contracts with these suppliers and contracts in service categories including 'management advisory services' and 'information technology consultation services' have the vast majority (by value) classified as not being consultancy. This may suggest entities have under-reported consultancy contracts.

5.8 Analysis of individual contracts with respective entities would be required to determine the extent to which consultancy contracts are being accurately reported in AusTender using the 'consultancy' flag.

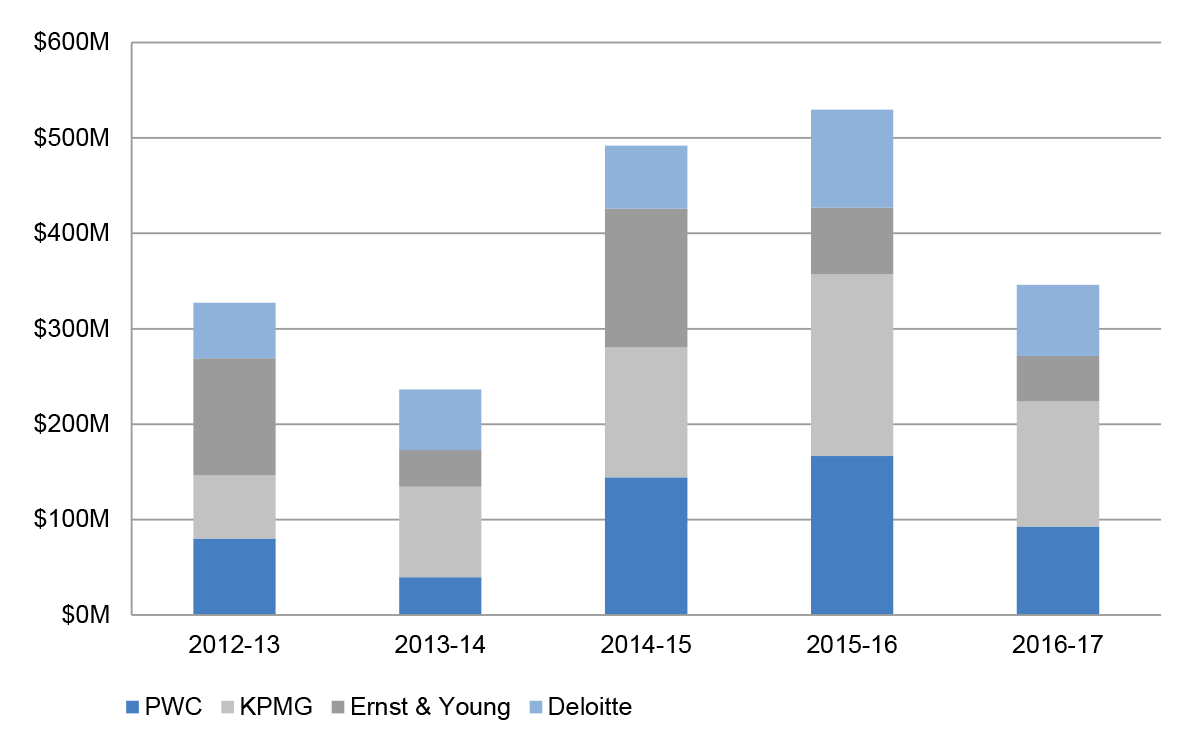

Procurement contracts with the 'big four' accounting firms

5.9 This section shows procurement contracts with the 'big four' Accounting firms as identified using a combination of ABNs and name matching.

Figure 5.3: Contract value with 'big four' accounting firms by financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

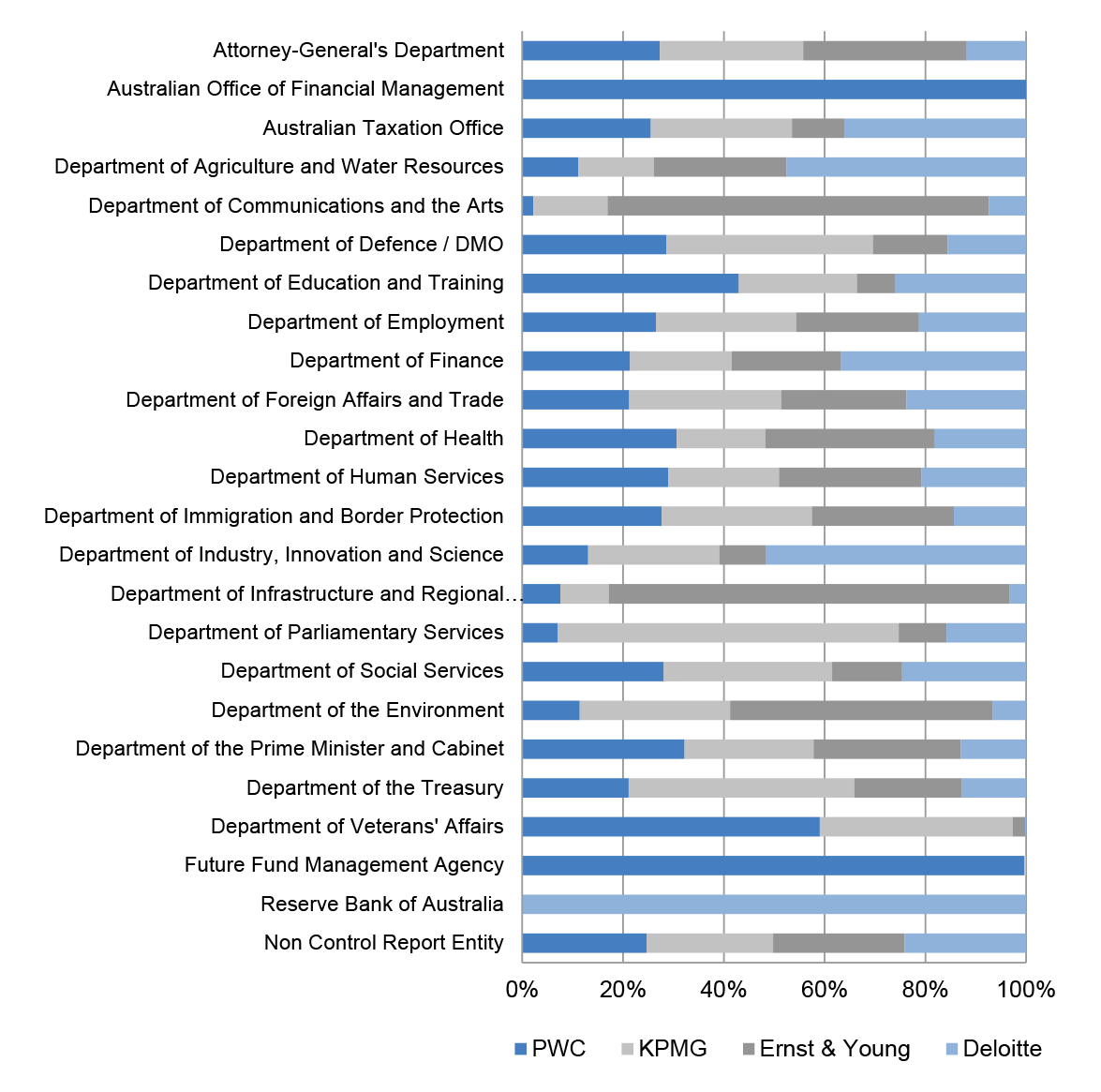

Figure 5.4: Proportion of 'big four' contract value by entity (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

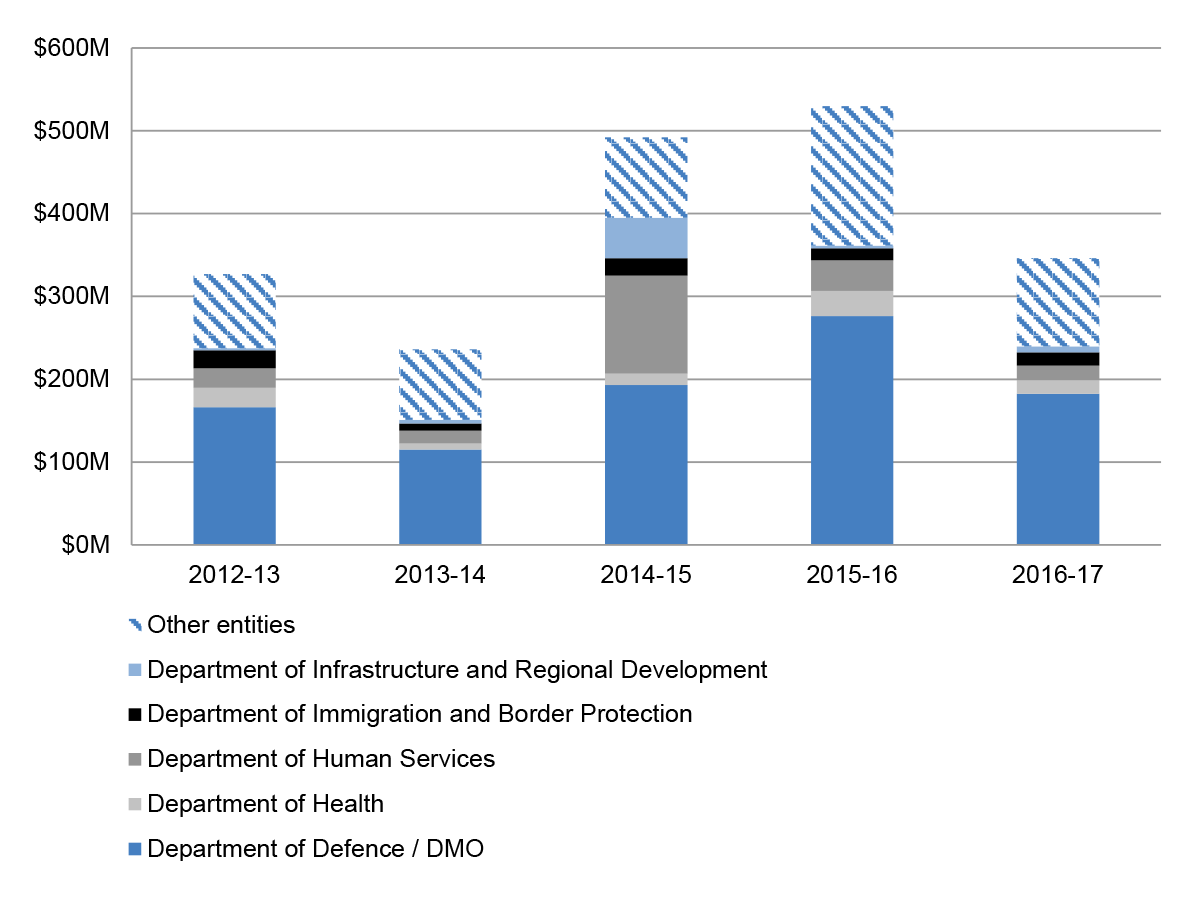

5.10 The following analysis shows the contract value with the 'big four' accounting firms by the largest five entities as determined by total contract value with the 'big four' in the period 2012–13 to 2016–17. All entities not in the largest five have been grouped as 'Other entities'.

Figure 5.5: Contract value with 'big four' by largest five entities by financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

6. Financial year procurement contract trends

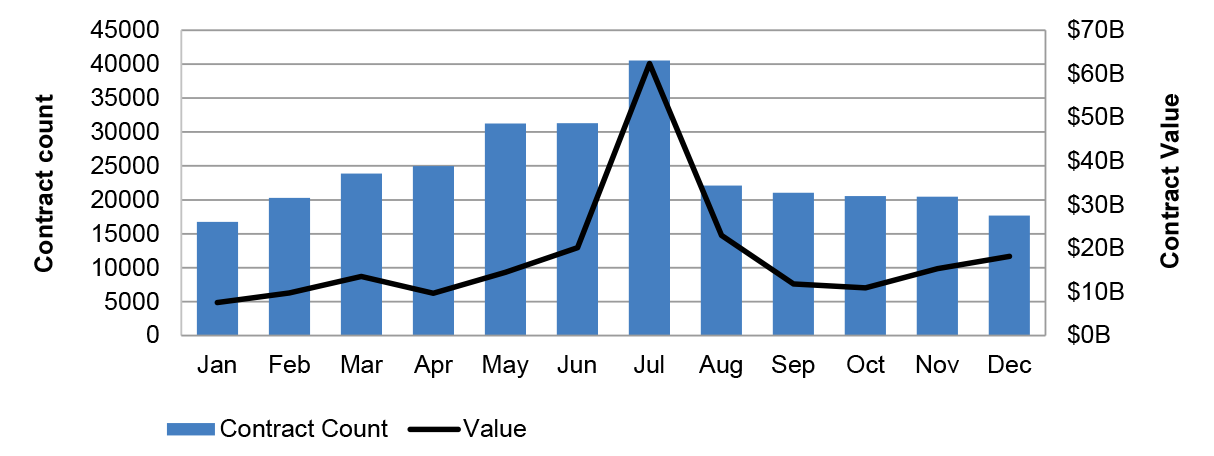

6.1 The ANAO analysed contracts in the period 2012–13 to 2016–17 to identify the number and value of contracts commencing by month. Figure 6.1 shows that for all contracts over the last five financial years, while there is an increase in the number of procurements towards the end of the financial year, more contracts commence in July than in any other month.

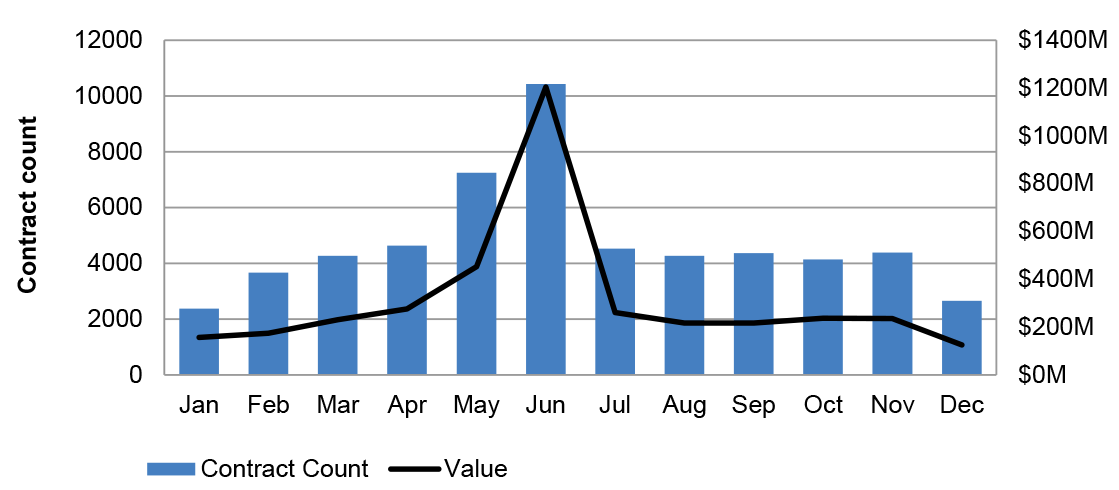

6.2 However, when looking only at short-term contracts, there is a significant increase in the number of contracts that commence in the final month of the financial year (Figure 6.2).

Figure 6.1: Contract commencement: All contracts by month start date (2012–13 to 2016–17)

Figure 6.2: Contract commencement: Short-term contracts by month start date 2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

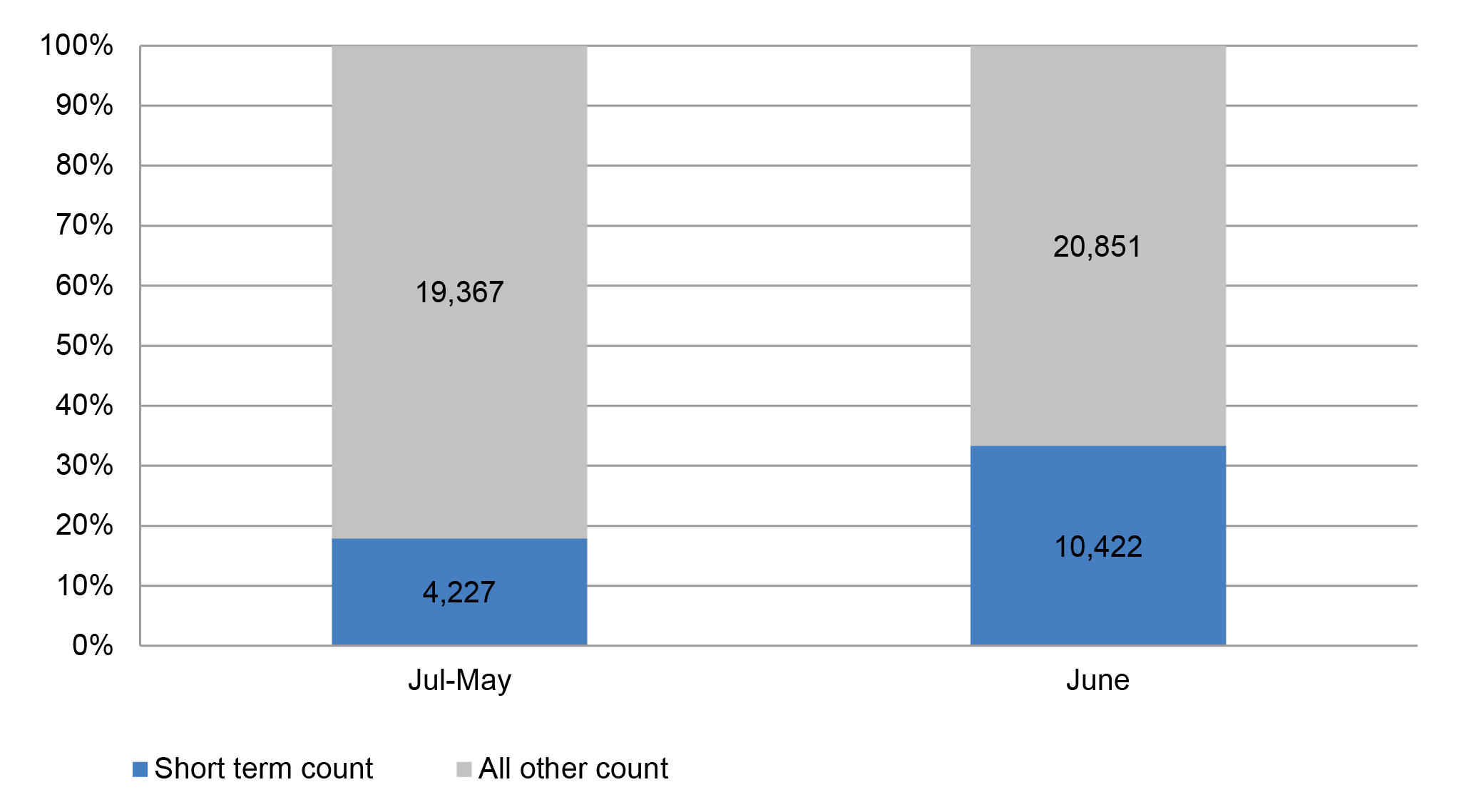

6.3 At the Whole-of-Government level, this represents an increase from an average of 845 short term contracts per month in July thru May to an average of 2084 in June (a 147 per cent increase). The value of short-term contracts entered into in June is also higher than the value of contracts entered into in each of the other months.

6.4 Figure 6.3 shows the relative proportion (by number) of short-term and all other contracts in June compared to the proportion of short term contracts in all other months.

Figure 6.3: Proportion of contracts (by number) commencing in June compared to the rest of the year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

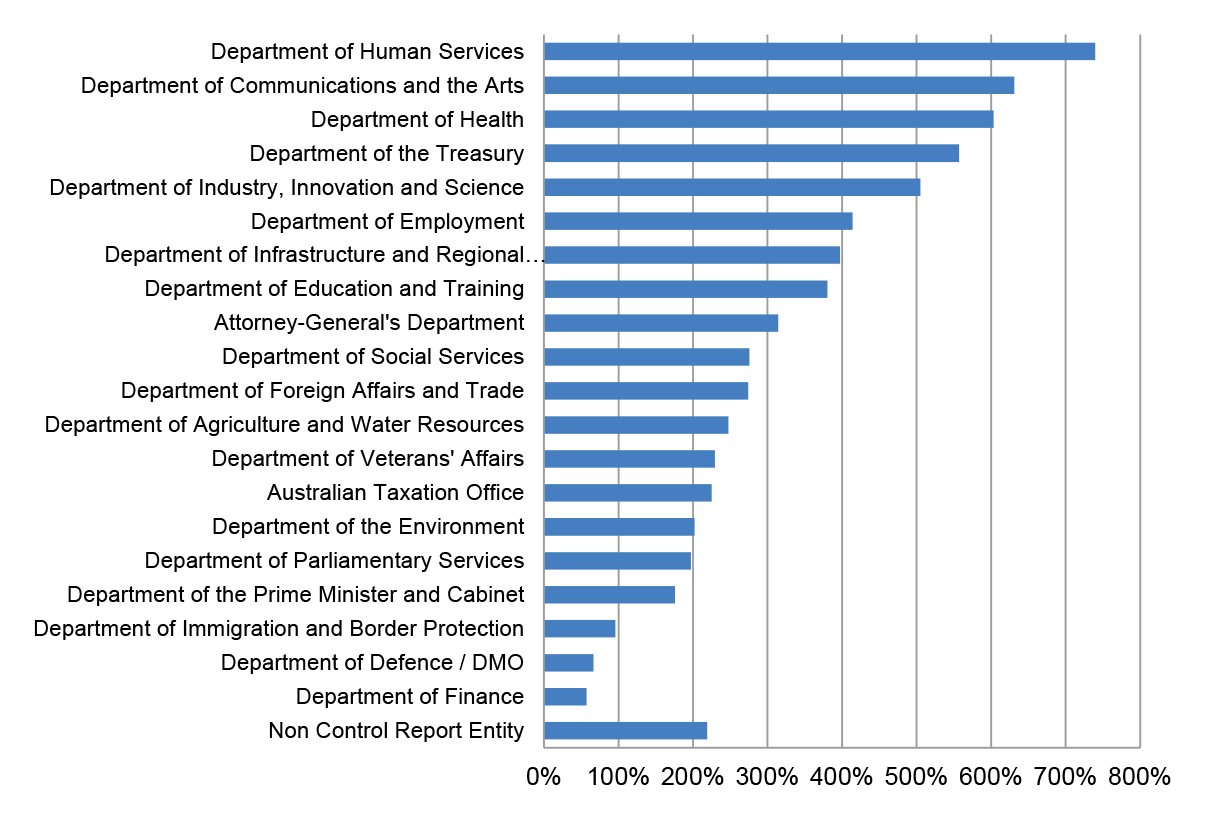

6.5 Figure 6.4 shows the percentage increase in short-term contracts between July–May and June by entity. While all 20 Control Report entities in the analysis had an increase in short term contracts in June, the extent varied considerably, ranging from 57 per cent to over 700 per cent increases.

Figure 6.4 Percentage increase in June short term contracts for selected control report entities (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

7. Procurement contract thresholds

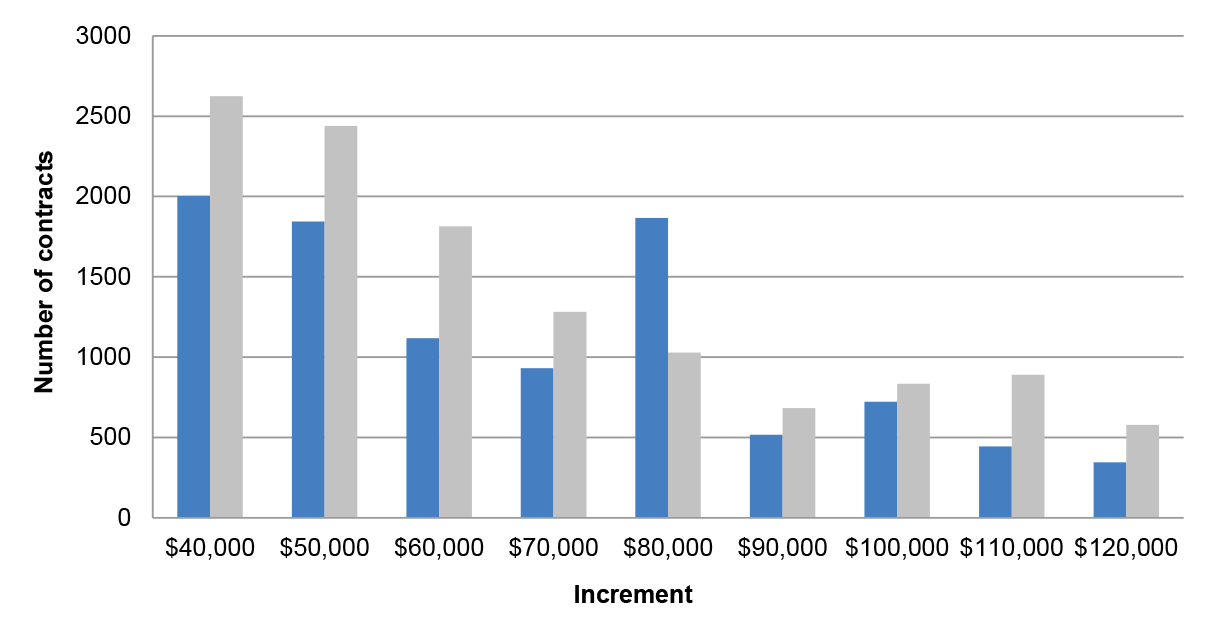

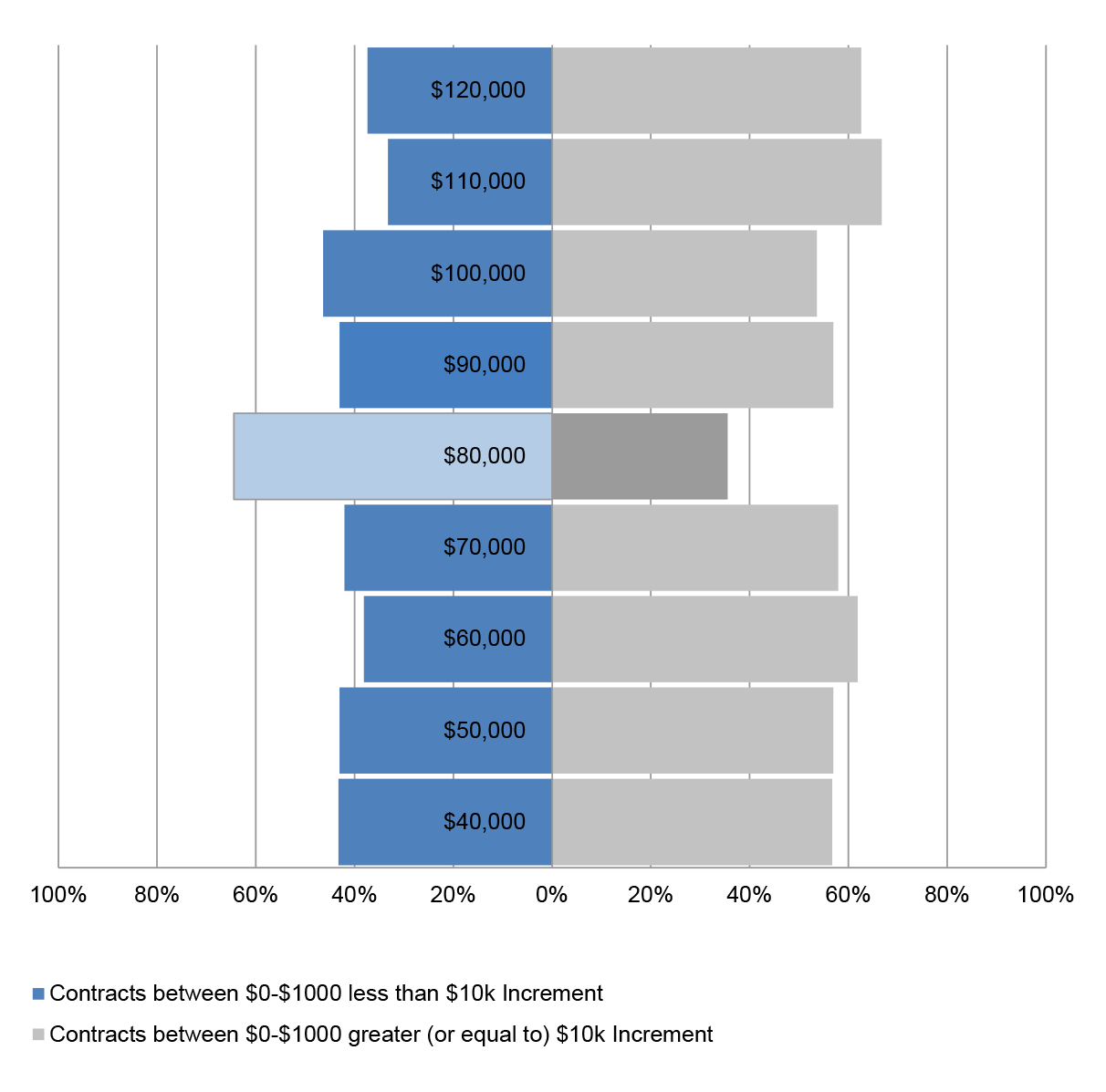

7.1 For non-corporate Commonwealth entities (other than for procurements of construction services), when the expected value of a procurement is at or above $80,000, additional rules in Division 2 of the CPRs must also be followed. Primarily, this requires that except under specified circumstances, procurements must be conducted by an open approach to the market.

7.2 The following analysis shows the distribution of reported contract values within $1000 of each $10,000 increment – that is, how many reported contracts are just below the $10,000 increment, and how many are just above. For all $10,000 increments, there are more contracts above the increment than below, except for the $80,000 threshold.

Figure 7.1: Number of contracts within $1000 of $10,000 Increments ($40,000 to $120,000 – FY 2012–13 to 2016–2017)

Source: ANAO analysis of AusTender data.

Figure 7.2: Percentage of contracts with values within $1000 of increments of $10,000 ($40,000 to $120,000 – 2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

7.3 The CPRs state that 'a procurement must not be divided into separate parts solely for the purpose of avoiding a relevant procurement threshold'. ANAO conducted analysis to identify sets of two contracts that had the following characteristics:

- both contracts were with the same entity;

- each of the contracts were entered into with the same supplier;

- the contracts had a start-date within the same quarter; and

- the combined value of the two contracts was above $80,000, but each of the reported contract values were below $80,000.

7.4 The ANAO identified 4914 individual contracts (or 2457 pairs of contracts) that met the above criteria.

Table 7.1: 'Potentially related' contracts (2012–13 to 2016–17)

|

2012–13

|

521

|

6111

|

|

2013–14

|

472

|

6022

|

|

2014–15

|

501

|

6766

|

|

2015–16

|

475

|

6969

|

|

2016–17

|

488

|

6656

|

|

Total

|

2457

|

32524

|

| |

|

|

Source: ANAO analysis of AusTender data.

7.5 The ANAO further analysed these 4914 contracts in order to categorise the pairs by whether one or both of the contracts identified as having an Open Tender process.

Table 7.2: 'Potentially related' contracts by procurement method (2012–13 to 2016–17)

|

At least one contract identified as Open Tender

|

950

|

1900

|

|

Neither contract identified as Open Tender

|

1507

|

3014

|

|

Total

|

2457

|

4914

|

| |

|

|

Source: ANAO analysis of AusTender data.

Figure 7.3: Potentially related contracts under $80,000 as a percentage of contracts between $80,000 and $160,000 by entity (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

7.6 Individual analysis of each contract would be required to determine whether these reflected:

- contracts for discrete procurements;

- data errors (such as duplicate entries); or

- if a single procurement had been split into smaller contracts in order to fall below the procurement threshold.

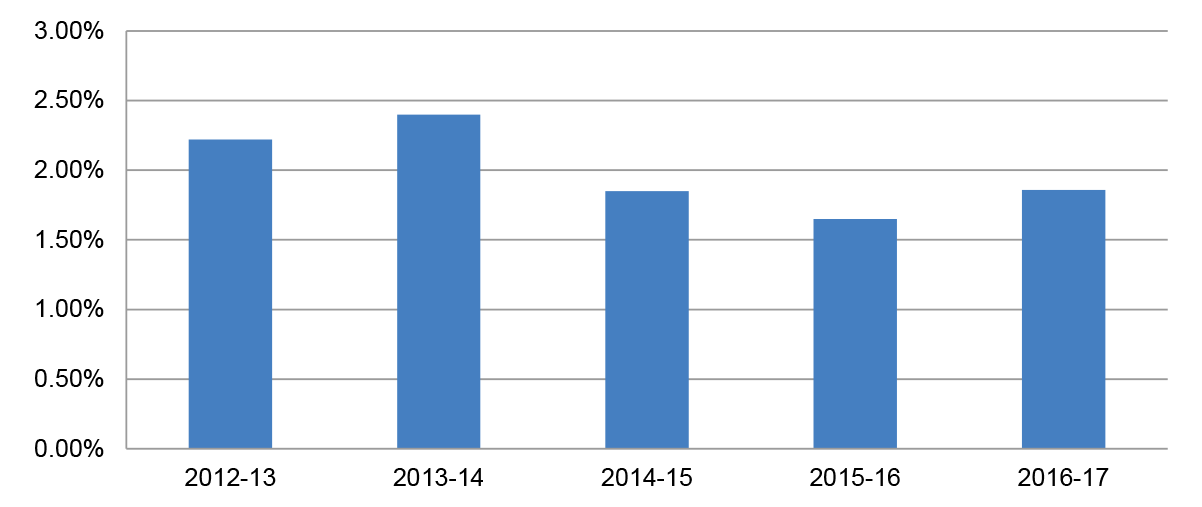

8. Accuracy and timeliness of procurement contract notice publication

Potential duplicate contract entries on AusTender

8.1 In addition to the analysis of potentially related contracts in Chapter 6, ANAO also identified a number of transactions with characteristics indicating the contract may have been mistakenly reported on AusTender multiple times. These contracts had the characteristics of:

- same entity;

- same supplier ABN (or supplier name where no ABN)

- same start date; and

- identical contract value.

8.2 In order to better identify potential duplicate entries on AusTender, unlike other sections of the report, this analysis has not aggregated related contracts where there were matching key fields in AusTender.

8.3 Results of this analysis indicate that almost two per cent of contracts reported on AusTender may be duplicate entries. This would have the effect of overstating reported AusTender procurement value, on average, more than $100 million per year (approximately 0.25 per cent).

8.4 This analysis would not identify instances where one of the contracts in a potential duplicate entry has been amended subsequent to its original publication.

8.5 Further analysis would be required to identify instances where entities contracts were validly reported reflecting goods or services being procured at the same price, on the same day, on multiple occasions from the same supplier.

Table 8.1: Estimated number and value of potential duplicate entries on AusTender

|

2012–13

|

1261

|

99,715

|

|

2013–14

|

1235

|

163,972

|

|

2014–15

|

1376

|

95,079

|

|

2015–16

|

1241

|

133,606

|

|

2016–17

|

1245

|

91,068

|

|

Total

|

6358

|

583,441a

|

| |

|

|

Note a: Figures in table may not sum due to rounding.

Source: ANAO analysis of AusTender data.

8.6 ANAO identified that two UNSPC categories make up a disproportional value of the potential duplicate entries. While contracts classified as 'Temporary Personnel Services' and 'Computer Services' account for only 2.35 per cent of total contract value, they account for 29.9 per cent of the total value of contracts identified as potential duplicate entries. ANAO's understanding is that these categories of contracts may be less likely to reflect duplicate entries as entities may enter into multiple contracts with supplier firms for staff contracted for the same period of time at the same rate.

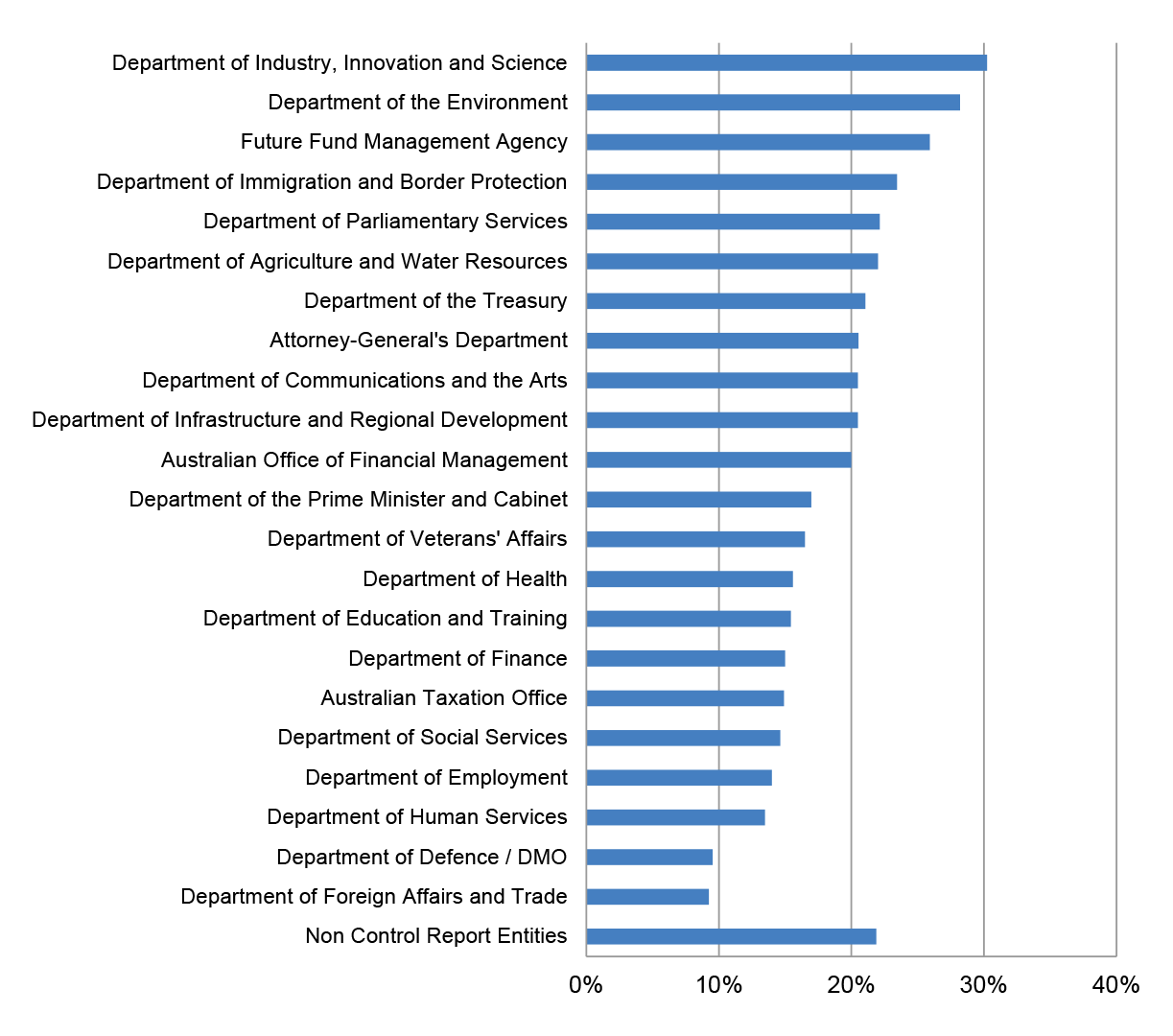

Figure 8.1: Estimated value of potential duplicate entry AusTender contracts as a percentage of total contract value by entity (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

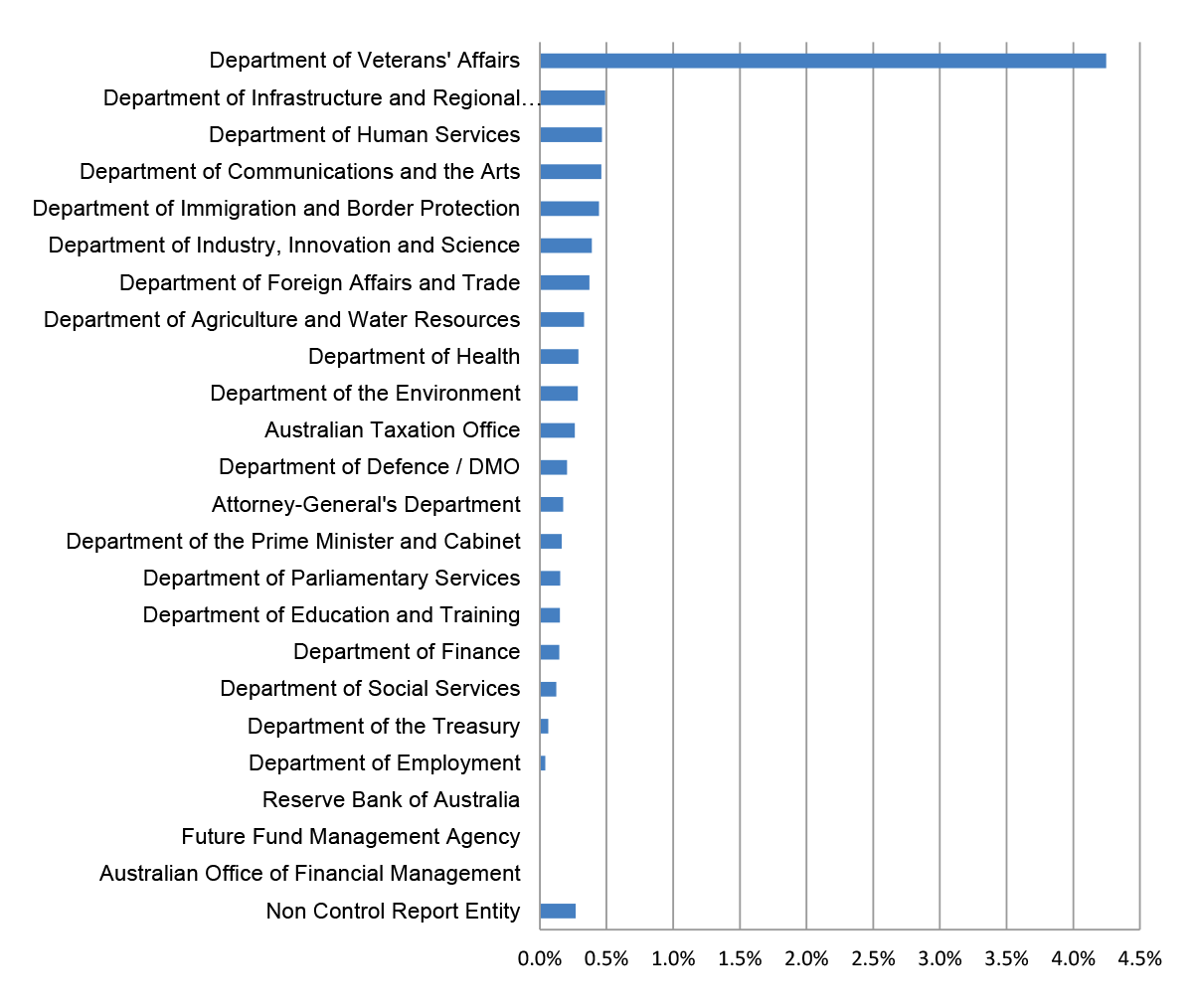

8.7 It should be noted that the Department of Veterans' Affairs had 29 per cent of its contract value in the categories 'Temporary Personnel Services' and 'Computer Services'. This is approximately 12 times higher than the Whole-of-Government average for these categories at 2.35 per cent.

8.8 As discussed previously, this may account for much of the reason why the Department of Veterans' Affairs has a 4.25 per cent value of potential duplicate entries compared with the 0.25 per cent Whole-of-Government average.

Timeliness of AusTender publication

8.9 The CPRs state that relevant entities must report contracts and amendments on AusTender within 42 days of entering into (or amending) a contract if they are valued at or above the reporting threshold.

8.10 Figures 8.2 and 8.3 show compliance with the 42 day publishing rule. AusTender does not capture the date on which contracts are entered into. It is possible for entities to notify a contract start date that is later than the date on which the contract is entered into (6.5 per cent of contracts list a start date after the publish date). Consequently, where:

- the contract was not published on AusTender within the 42 days of the contract having been entered into; but

- the publication nonetheless occurred within 42 days after the contract start date;

this analysis will treat the contract notice as having met the 42 day publishing rule.

8.11 The following analysis includes only transactions where the publish date is on or after the start date.

Figure 8.2: Percentage of contracts published within 42 days of the contract start date by financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

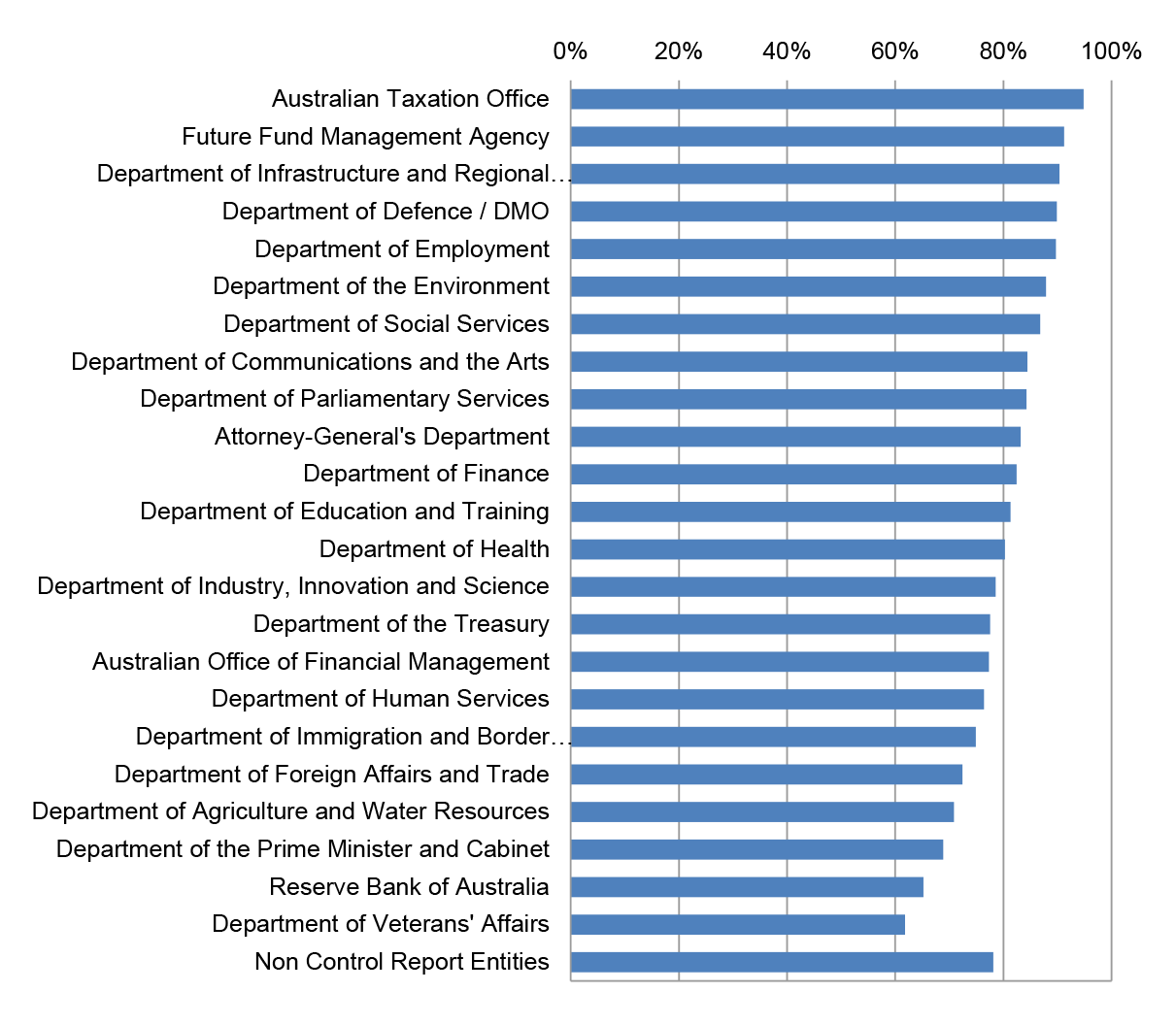

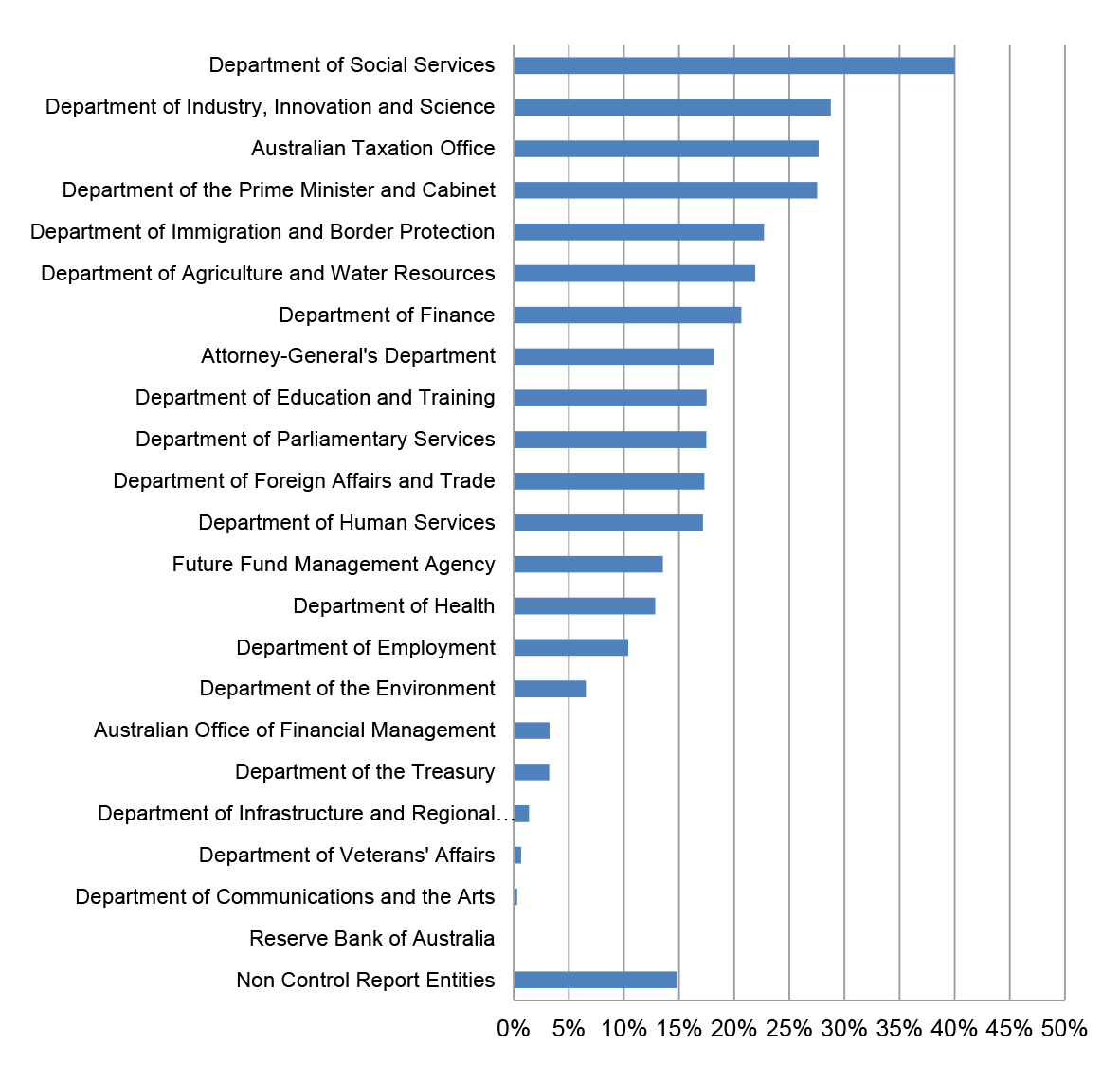

Figure 8.3: Percentage of contracts published to AusTender within 42 days of the contract start date by entity (2012–13 to 2016–17).

Source: ANAO analysis of AusTender data.

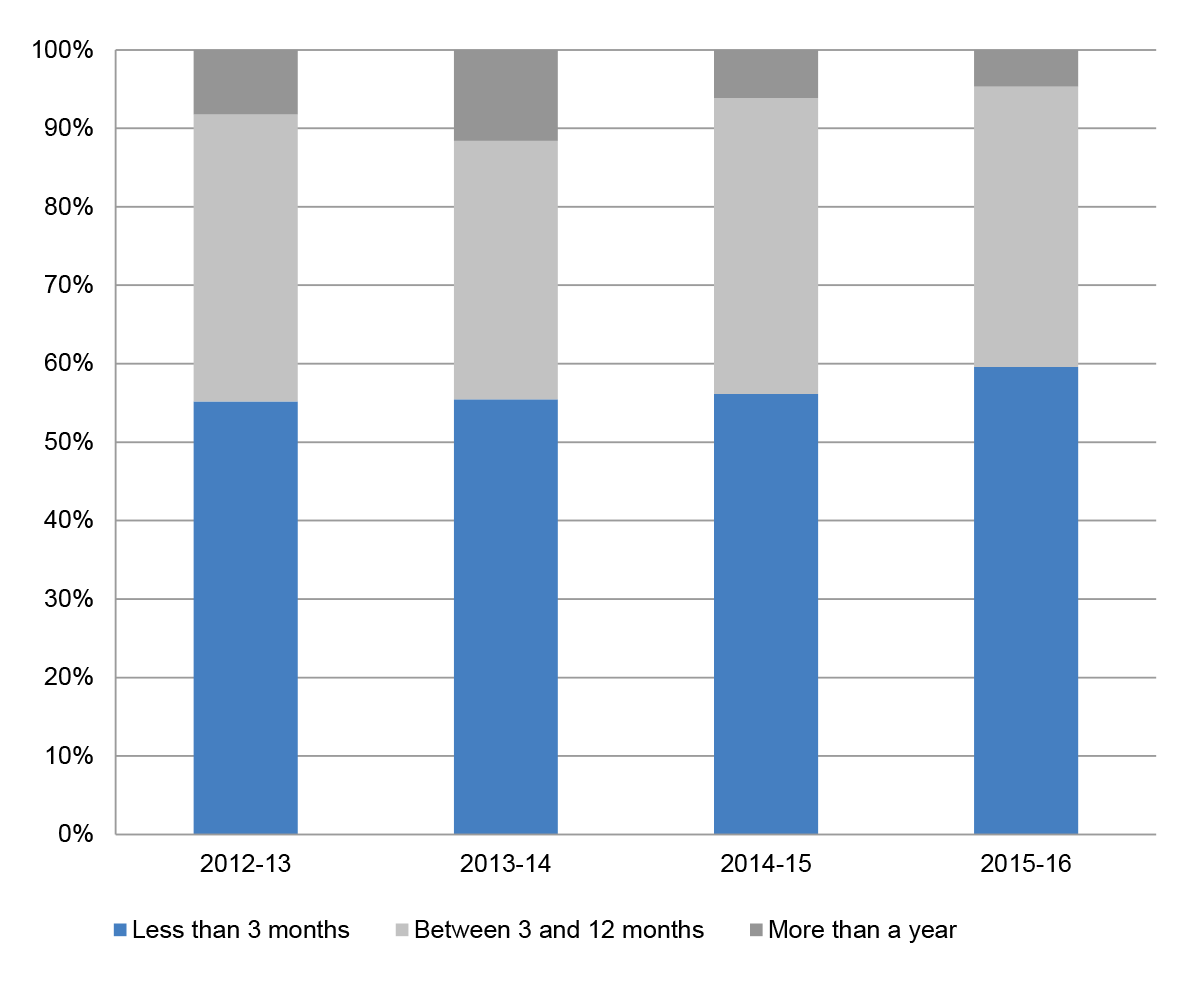

8.12 Figure 8.4 shows a stratification of the time taken to publish to AusTender, only those contracts that were not compliant with the 42 day publishing requirement (I.e. those where the publish date was more than 42 days after the contract start date).

Figure 8.4: Stratification of contracts published more than 42 days after start date by financial year (2012–13 to 2015–16)

Source: ANAO analysis of AusTender data.

9. Procurement contracts by location

9.1 ANAO matched the AusTender Contract Notice data with remoteness data published by the Australian Bureau of Statistics using the office and supplier postcodes. The following analysis classifies procurement by Major City, Regional, and Remote areas.

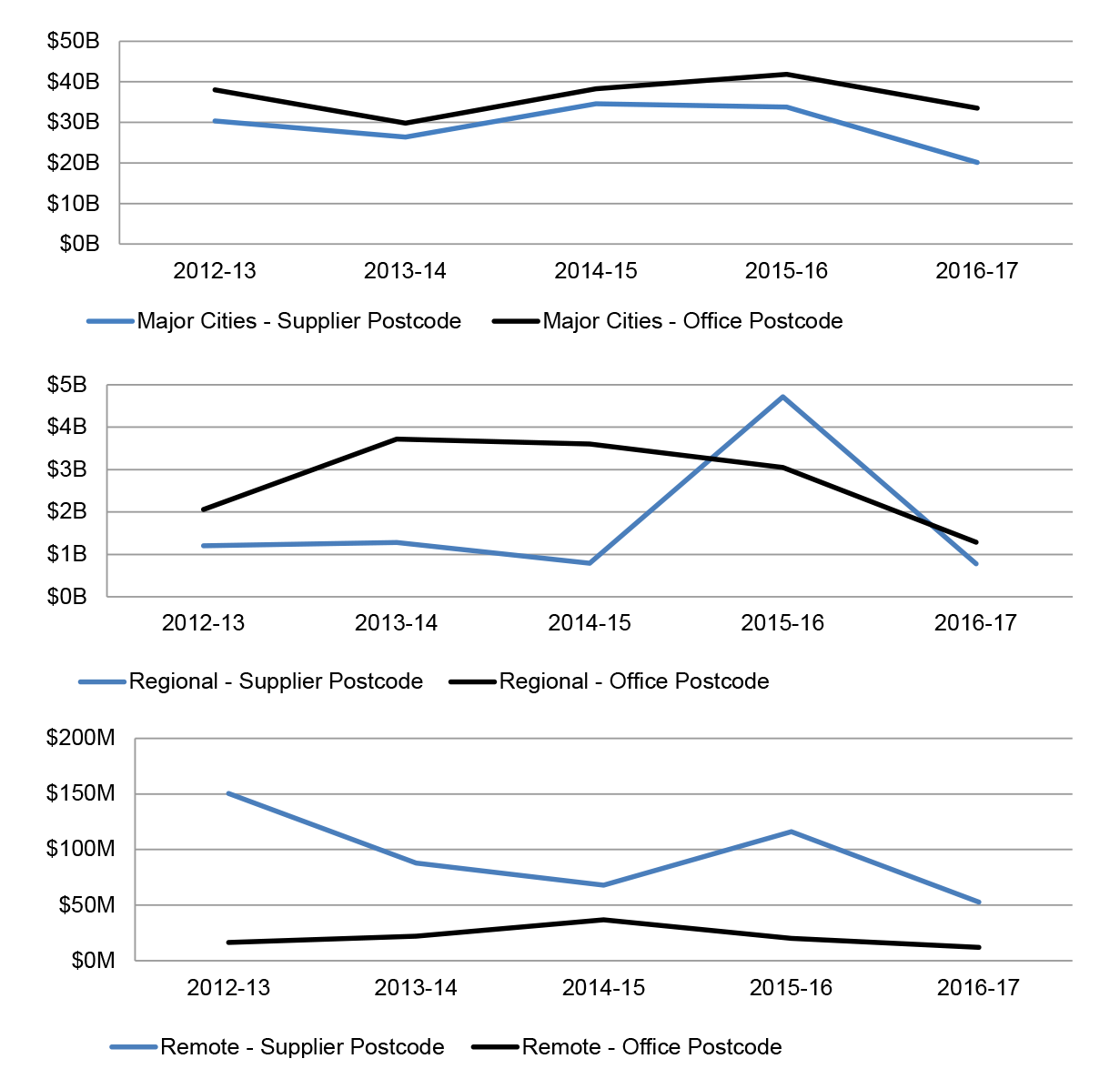

Figure 9.1: Contract value by supplier remoteness and office remoteness by financial year (2012–13 to 2015–16)

Source: ANAO analysis of AusTender data.

Figure 9.2: Contract value by supplier remoteness and financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

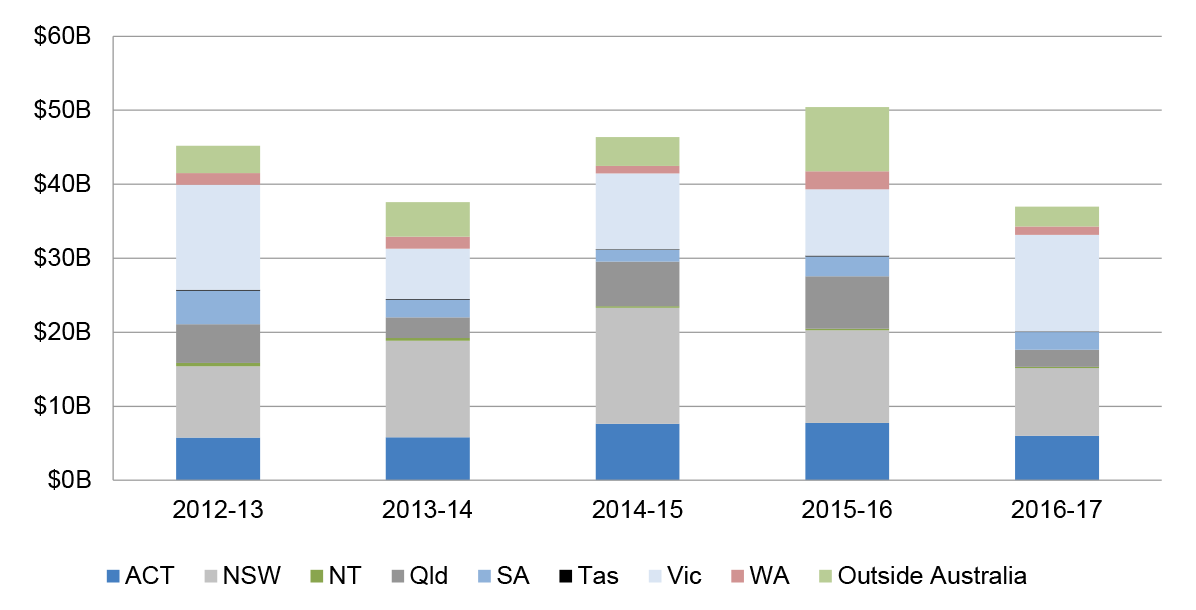

Figure 9.3: Contract value by supplier state and financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data,

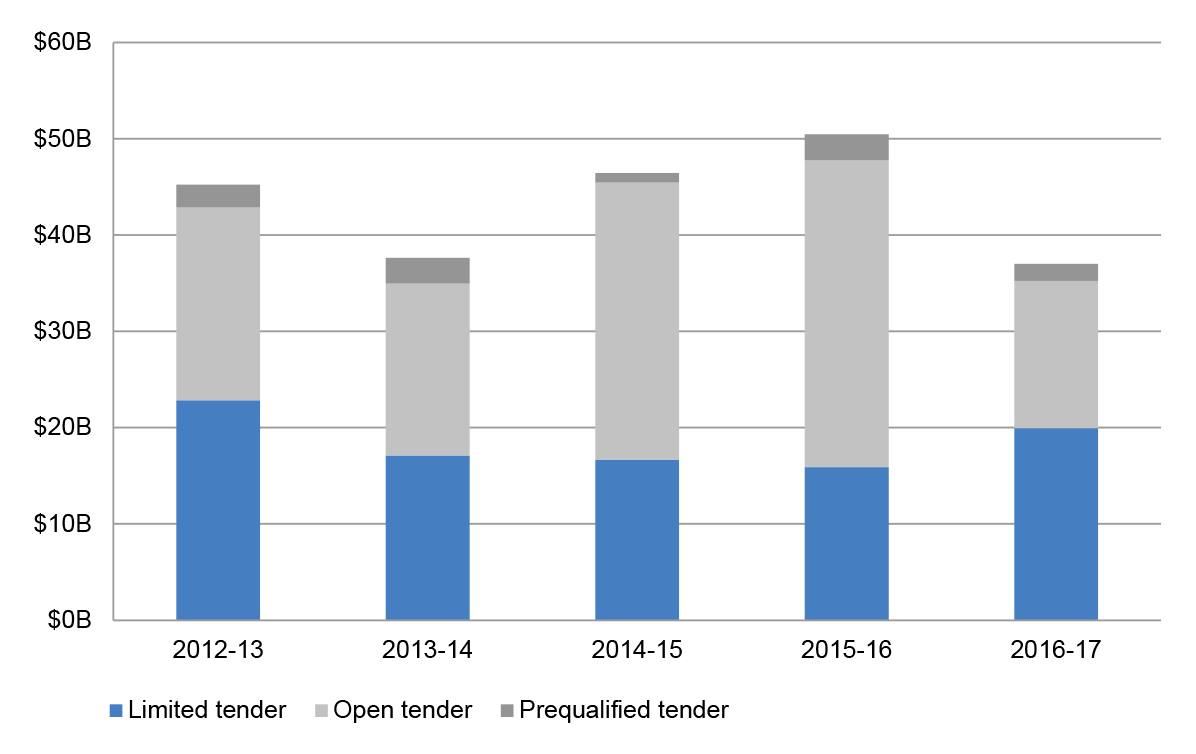

10. Procurement methods

10.1 Entities are required to report contracts against three methods of procurement; Limited Tender, Open Tender, or Prequalified tender. The analysis in this chapter shows use of procurement method across the Commonwealth and by entity.

Figure 10.1: Contract value by procurement method and financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

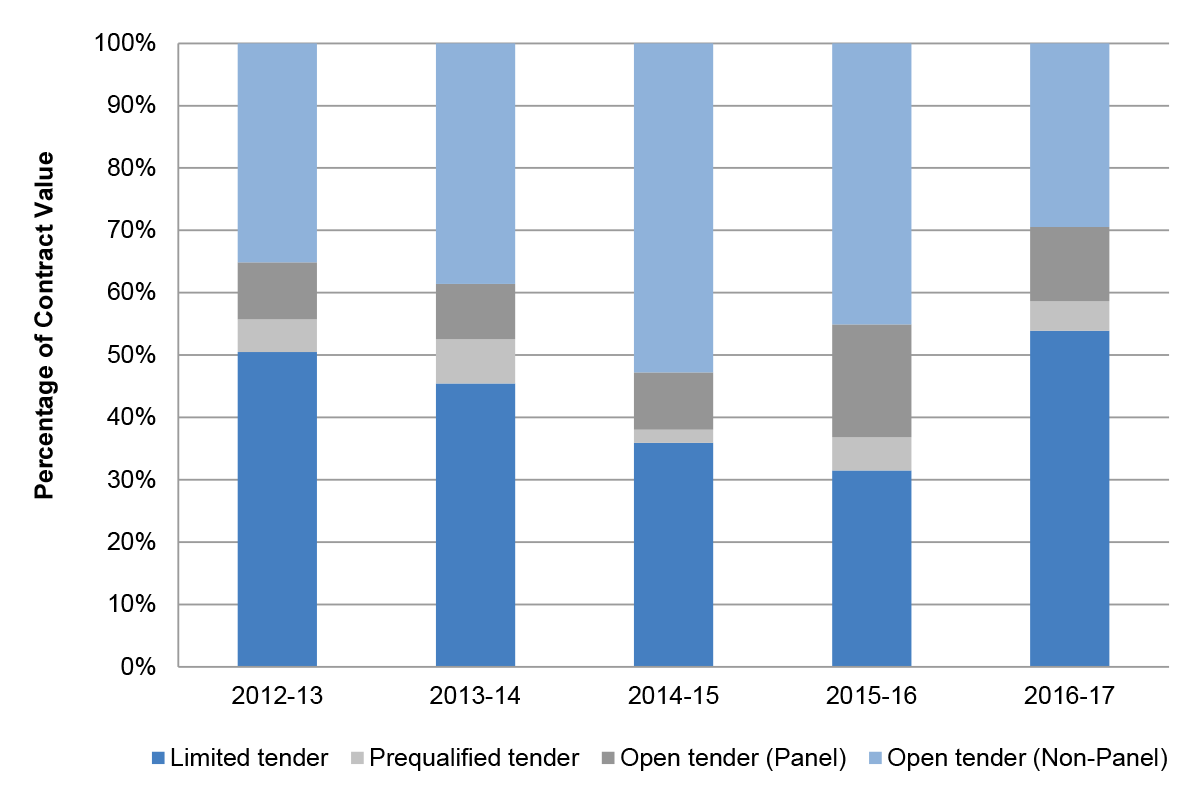

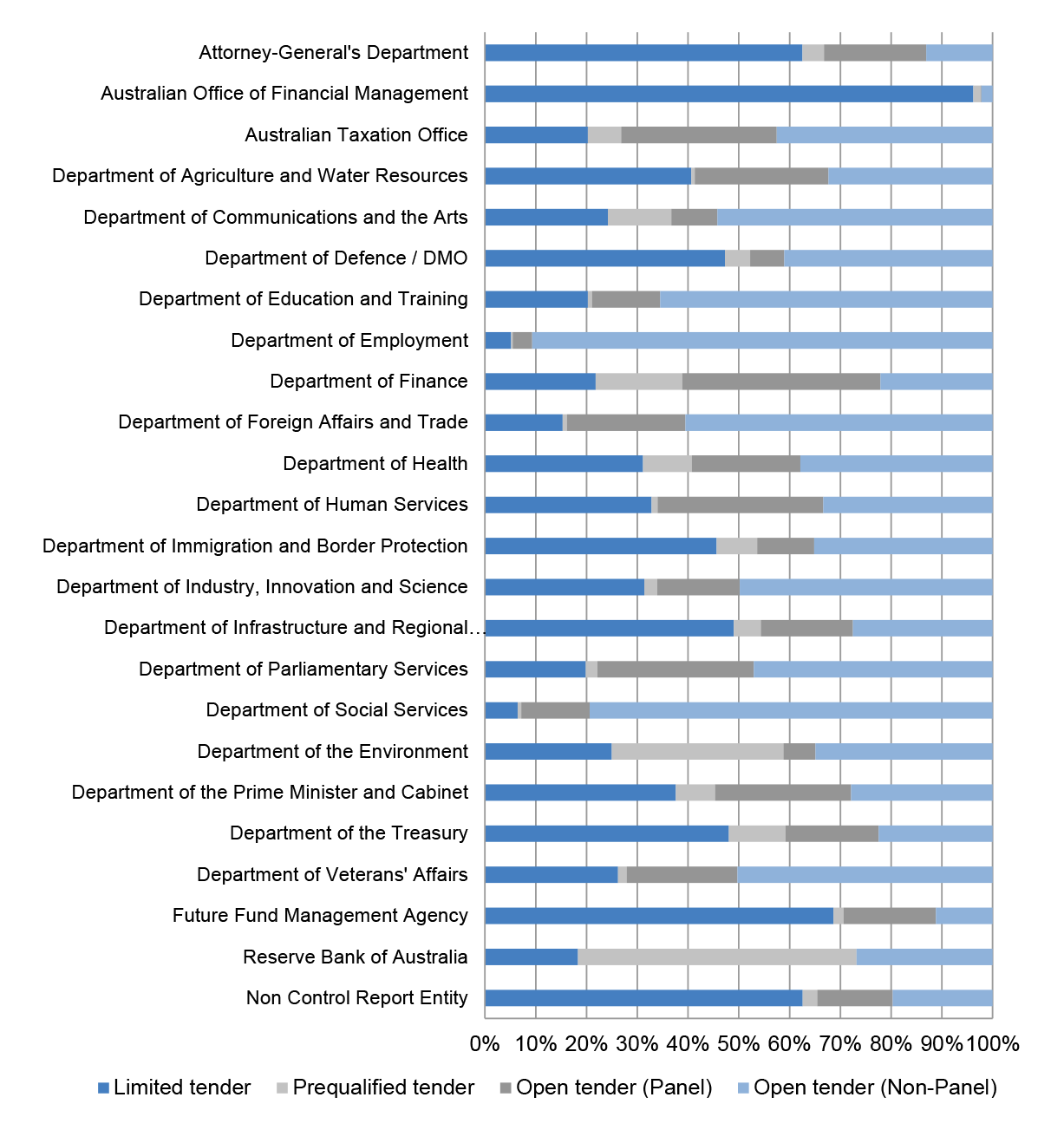

10.2 Entities are also required to identify when publishing contracts whether the procurement was conducted from a panel arrangement. Figure 10.2 shows the percentage of contract value by procurement method including for Open Tender contracts, whether the procurement was flagged as having a panel arrangement.

10.3 In addition to open approaches to market, contract notices may be categorised as 'open tender' where the supplier has been sourced from a panel arrangement that was established through a procurement process (either open tender or prequalified tender). Procurement can then be undertaken with any supplier on the panel.

10.4 Contracts with procurement methods other than Open Tender may also be flagged as using a panel arrangement however the percentages are small and have not been shown separately on this chart.

Figure 10.2: Percentage of contract value by procurement method (including panel arrangement status for open tender contracts) and financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

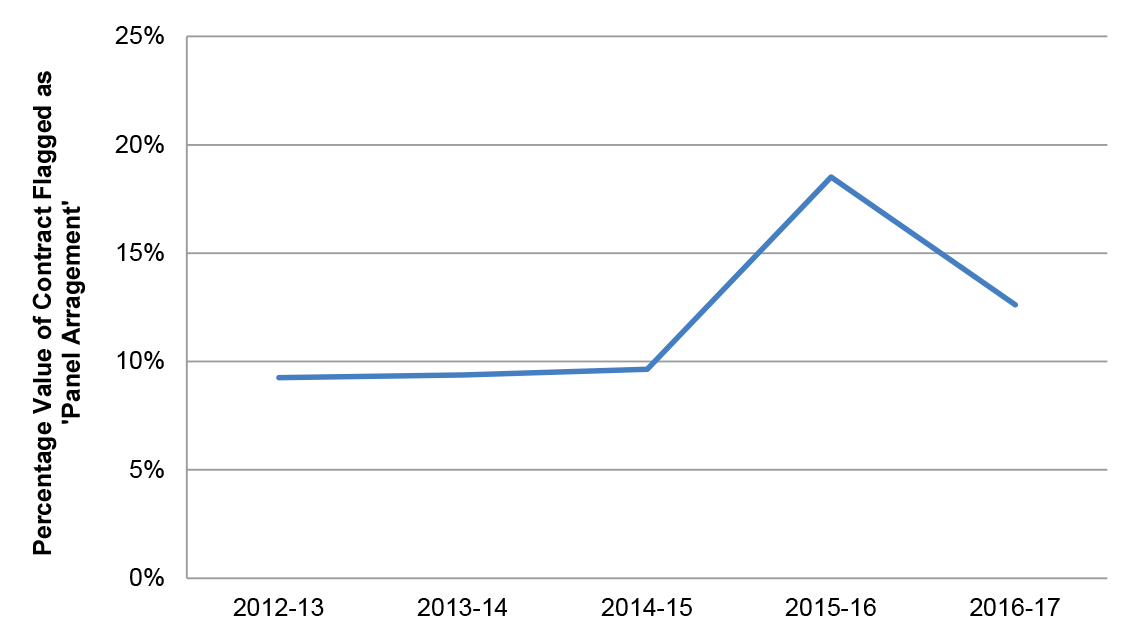

Figure 10.3: Value of contracts using panel arrangements as a percentage of all contracts by financial year (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

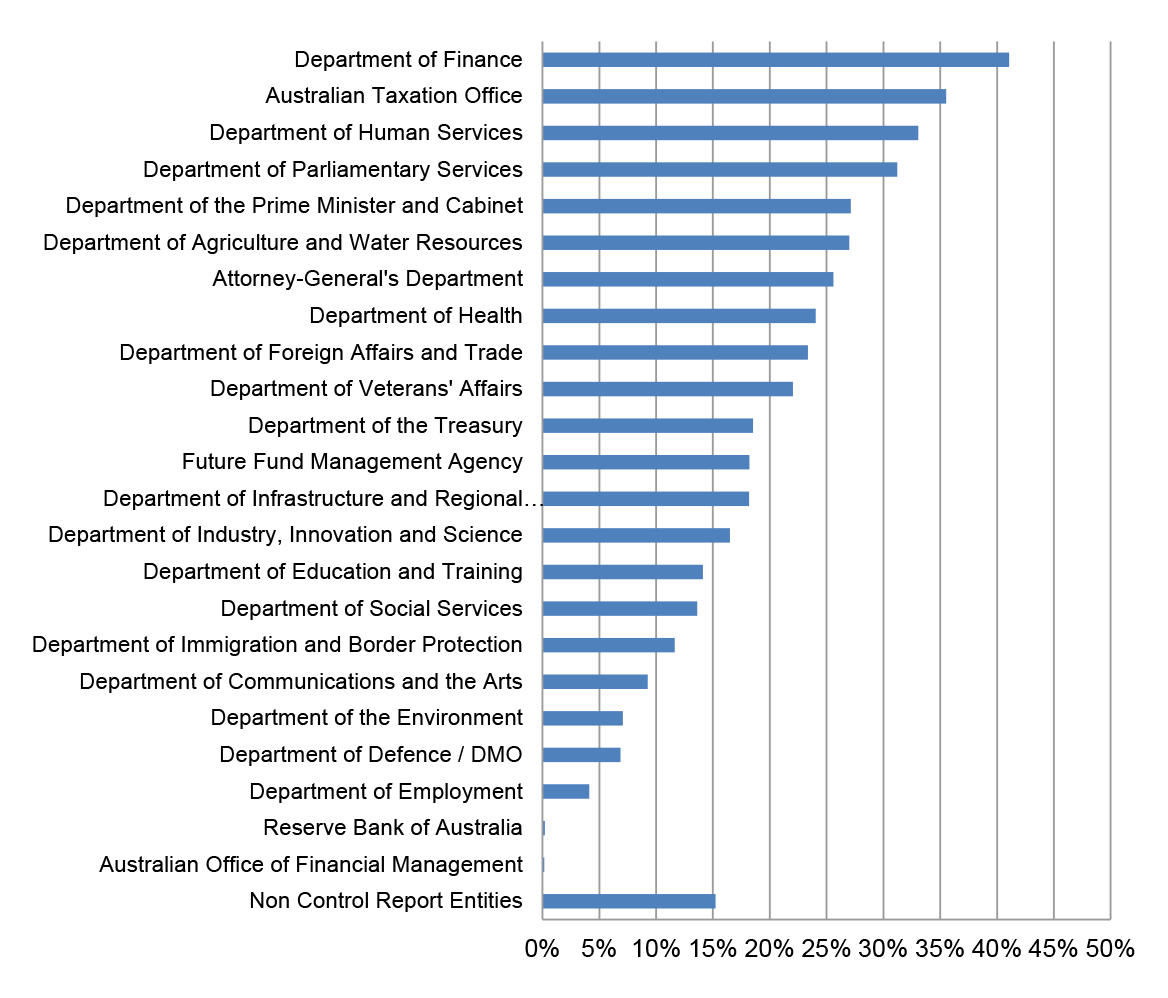

Figure 10.4: Percentage of contract value by procurement method by entity (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

Figure 10.5: Value of contracts using panel arrangements as a percentage of entities total contract value (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

11. Concentration of suppliers (use of panels)

11.1 Procurement panels are a tool for the procurement of goods or services regularly acquired by entities. Panels are established through procurement processes, where a number of suppliers are appointed through a contract or deed of standing offer. Panels are usually established at a point in time, and once established, the opportunity for other suppliers to join the panel will generally be limited.

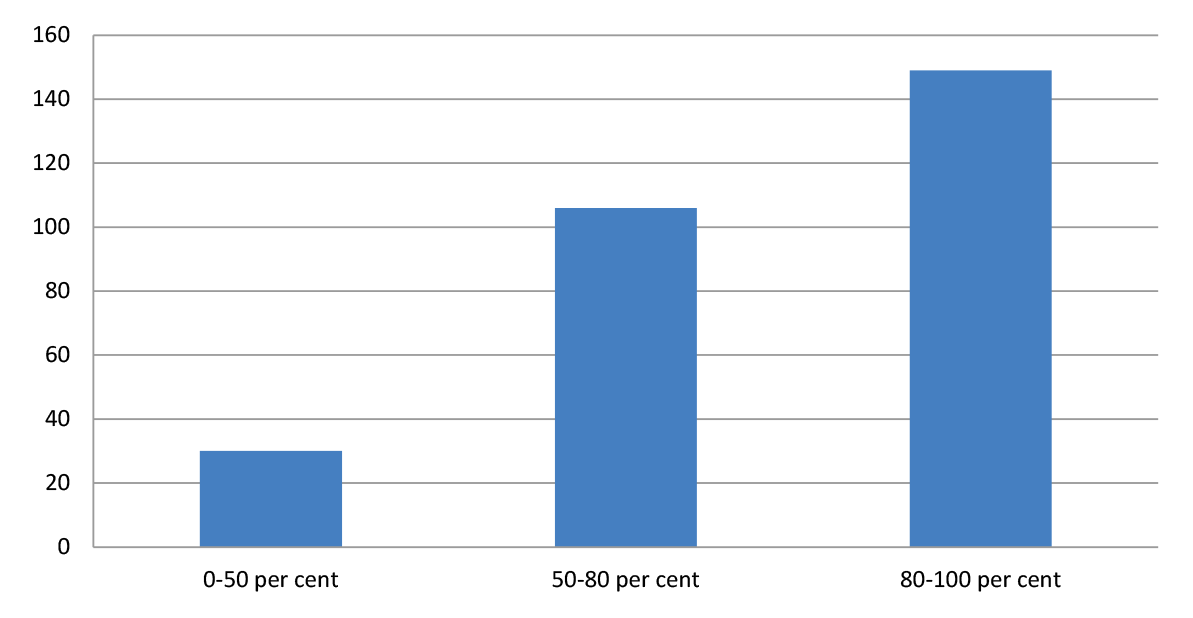

11.2 The ANAO analysed procurements from 285 procurement panels that contained contracts between and Financial Year 2012–13 and 2016–17. The ANAO examined panels with five or more suppliers, to identify a 'top 20 per cent'—the top 20 per cent of suppliers by value of contracts awarded. The ANAO then analysed the proportion of contracts (by value) that were awarded to these 'top 20 per cent' suppliers.

11.3 Table 11.1 and Figure 11.1 show the value of procurements undertaken by the 'top 20 per cent' of firms on each of the panels included in the analysis.

Table 11.1: Panels by the percentage of contract value awarded to the 'top 20 per cent' of suppliers

|

>80 per cent

|

149

|

11,281,891

|

12,427,074

|

The large majority of panels examined had a relatively small proportion of suppliers awarded the majority of contract value. There were a relatively small number of successful suppliers on these panels.

|

|

50–80 per cent

|

106

|

3,726,508

|

5,506,220

|

|

|

0–50 per cent

|

30

|

163,503

|

423,611

|

Generally, these panels saw more even distribution of procurements among successful suppliers

|

| |

|

|

|

|

Source: ANAO analysis of AusTender data.

Figure 11.1: Number of panels by the percentage of contract value awarded to the 'top 20 per cent' of suppliers (2012–13 to 2016–17)

Source: ANAO analysis of AusTender data.

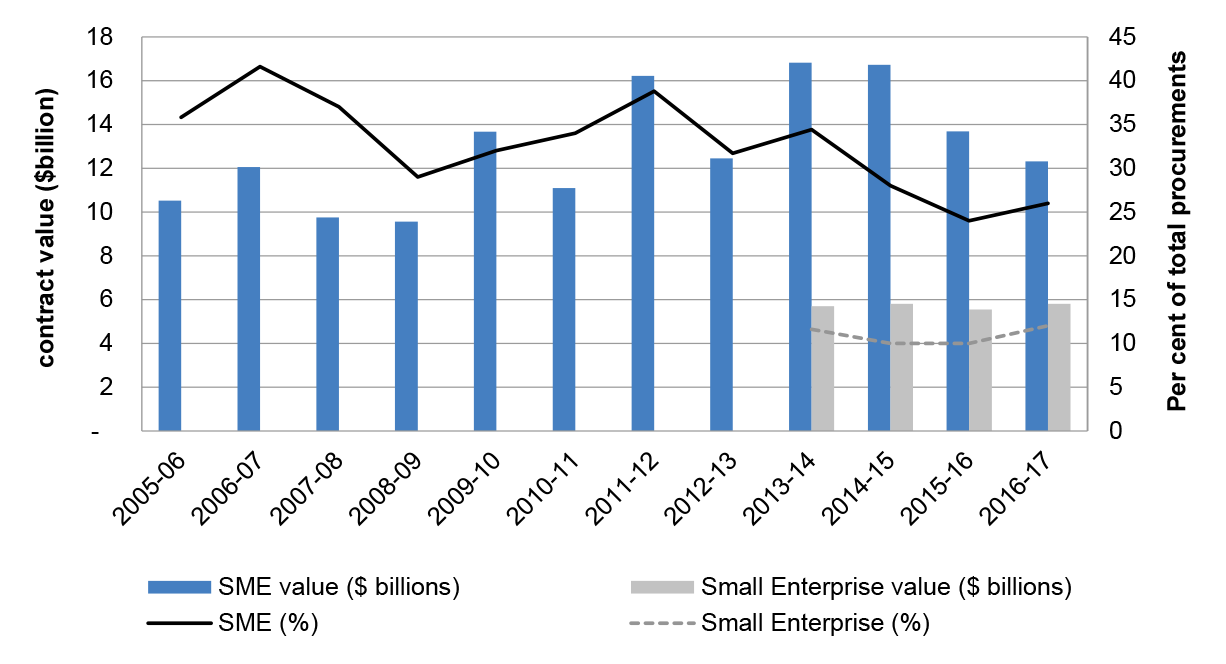

12. Small and medium enterprises

12.1 The CPRs set a target of at least 10 per cent (by value) of procurements from Small to Medium Enterprises (SMEs) by non-corporate Commonwealth entities. The Department of Finance (Finance) reports against this target, and the proportion of procurement contracts by number and value to small businesses. Figure 12.1 shows Finance's reporting of the value and percentage of procurements undertaken with SMEs since 2005–06; and from 2013–14, the value and percentage of procurements undertaken with small enterprises.

12.2 Since reporting began, Finance has published a result between 24 and 42 per cent, well above the Government target.

Figure 12.1: SME and Small Enterprises participation

Source: Department of Finance, reported Finance data, Statistics on Australian Government Procurement Contracts. available from <https://www.finance.gov.au/procurement/statistics-on-commonwealth-purchasing-contracts> [accessed 7 December 2016].

12.3 An SME is defined as a business which has fewer than 200 employees and operates independently of any parent organisation for taxation arrangements. A small business is defined as a business with fewer than 20 employees.

12.4 Finance contracts the analysis of Government procurement from SMEs to the Australian Bureau of Statistics (ABS). Aggregated results by entity and the number of businesses in each category (SME or Other) are published by Finance but the individual classification of suppliers as either SME or other is not released publically. The latest Finance publication of procurement statistics was released in November 2017 for the 2016–17 financial year.

Table 12.1: Entities with a reported percentage of contract value with SMEs greater than 85 per cent (2016–17)

|

Office of the Australian Information Commissioner

|

96

|

|

Royal Australian Mint

|

94

|

|

Administrative Appeals Tribunal

|

93

|

|

Clean Energy Regulator

|

92

|

|

National Capital Authority

|

92

|

|

Department of Foreign Affairs and Trade – Australian Aid Program

|

91

|

|

Australian National Audit Office (ANAO)

|

90

|

|

Old Parliament House

|

90

|

|

National Health Funding Body

|

87

|

|

National Mental Health Commission

|

86

|

| |

|

Source: Department of Finance, Subset of reported Finance data, Statistics on Australian Government Procurement Contracts, available from <https://www.finance.gov.au/procurement/statistics-on-commonwealth-purchasing-contracts>.

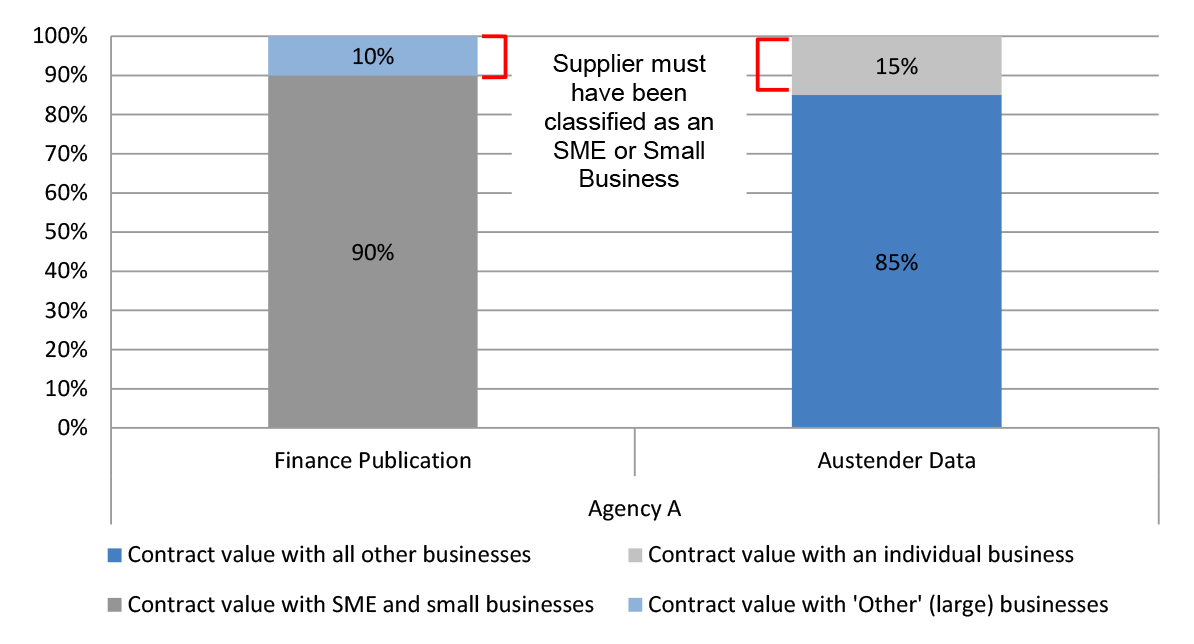

12.5 The absence of information regarding classification of suppliers as either SME or 'Other' (large) prevents an in-depth analysis of procurement with SMEs. However, the ANAO examined a selection of entities with a reported high proportion of SME contract value. In particular, the ANAO examined entities where:

- Finance reported a very high percentage (by value) of procurements awarded to SMEs; and

- the percentage of the value of contracts awarded to individual businesses by an entity was greater than the percentage of procurement Finance reported as belonging to 'Other' (large) businesses by that entity.

12.6 In the circumstance described above, that business would (by definition) have been classified as a small enterprise or SME.

- An entity is listed in Finance's annual statistics report has having undertaken 90 per cent of its procurements, by value, with small businesses or SMEs.

- The remaining 10 per cent, by value, of procurements were therefore by 'Other' (large) businesses.

- The entity reported contracts with a total value of $25 million.

- Therefore, if there is any business with a total value of contracts awarded by that entity greater than 10 per cent of the entity total (in this example, 2.5 million), that business must have been classified as an small business or SME for the purpose of reporting.

|

Figure 12.2: Illustration example—Identifying SMEs from entity level results

12.7 Using this methodology, ANAO identified a number of businesses with large numbers and values of contracts in 2016–17 that appeared to have been classified as SMEs. These included major consultancy/accountancy firms and other Australian arms of large global business with thousands of employees.

12.8 Table 12.2 lists these suppliers with the entity that was used to identify them as a likely SME and the value of contracts for that supplier with that entity in 2016–17.

Table 12.2: Selection of suppliers classified as small or SME and contract value (2016–17)

|

Abt JTA

|

Department of Foreign Affairs and Trade – Australian Aid Program

|

194,199

|

|

Charter Hall Real Estate Management Services

|

Australian Prudential Regulation Authority (APRA)

|

105,402

|

|

Cardno

|

Department of Foreign Affairs and Trade – Australian Aid Program

|

81,207

|

|

Coffee international Development

|

Department of Foreign Affairs and Trade – Australian Aid Program

|

57,193

|

|

Baxalta Australia

|

National Blood Authority

|

47,219

|

|

Seco Tools Australia

|

Royal Australian Mint

|

23,179

|

|

Sliced Tech

|

National Capital Authority

|

3,426

|

|

Dixon Appointments

|

Tertiary Education Quality and Standards Agency

|

3,239

|

|

ActewAGL

|

National Capital Authority

|

3,229

|

|

Design Craft Furniture

|

Department of the Senate

|

2,828

|

|

Connetica Consulting

|

National Mental Health Commission

|

847

|

|

PwC

|

National Health Funding Body

|

636

|

|

Holding Redlich

|

Office of the Australian Information Commissioner

|

401

|

|

Ernst & Young

|

National Health Funding Body

|

399

|

|

Nous Group

|

National Mental Health Commission

|

380

|

| |

|

|

Source: ANAO Analysis of AusTender data.

12.9 The ANAO provided ABS with the results of this analysis. The ABS advised it has revised its methodology relating to 'the classification of large businesses operating under multiple ABNs and the potential for these businesses to be incorrectly classified as Small to Medium Enterprises'.

13. Procurement contract confidentiality provisions

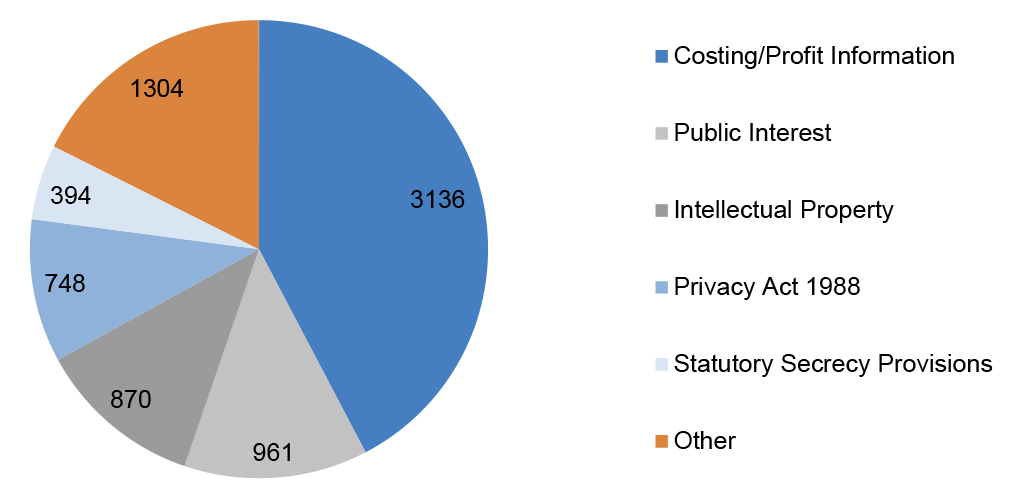

13.1 Contracts published on AusTender are required to identify if the contract includes a confidentially provision. The reasons for confidentially should also be recorded.

Figure 13.1: Proportion of contracts with confidentiality provisions by financial year (2012–13 to 2016–17)

Source: ANAO Analysis of AusTender data.

Figure 13.2: Reasons for contract confidentially 2012–13 to 2016–17

Source: ANAO Analysis of AusTender data.

Figure 13.3: Percentage of contracts with confidentialy provisions by entity (2012–13 to 2016–17)

Source: ANAO Analysis of AusTender data.

14. Contract amendments

14.1 The publically available contract notice data lists the latest information relevant to each contract, but does not provide historical data on contract amendments. In order to conduct a more detailed analysis of contract amendments, the ANAO has used data from weekly export files that Finance publish on AusTender. These files are only provided for the most recent 18 months and include fields showing the 'Parent' (or previous) Contract Notice ID and the 'Amendment Publish Date'.

14.2 At the time of publishing this report, ANAO had access to two years of these weekly export files containing contracts published or amended between 8 November 2015 and 6 November 2017.

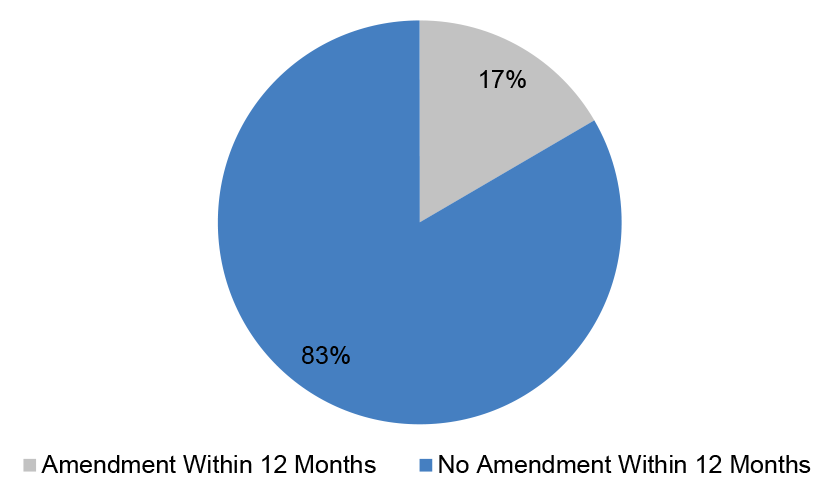

14.3 Figure 14.1 and Figure 14.2 show the percentage of contracts originally published in the first year of the data range (8 November 2015 to 7 November 2016) that were amended within 12 months of the contracts original publication date.

14.4 For the purposes of this analysis, ANAO only considered contracts to be amended if the contract value or end date had been changed after the contract was originally published.

14.5 The Department of Defence / Defence Materiel Organisation have been excluded from this analysis as they do not record contract amendments using the 'Parent CN ID' or 'Amendment Publish Date' fields provided in AusTender.

Figure 14.1: Percentage of contracts amended within 12 months of contracts original publish date by entity – Contracts with an original publish date from 8 November 2015 to 7 November 2016

Source: ANAO Analysis of AusTender data.

Figure 14.2: Percentage of contracts amended within 12 months of contracts original publish date – Contracts with an original publish date from 8 November 2015 to 7 November 2016 – excluding Department of Defence / DMO

Source: ANAO Analysis of AusTender data.

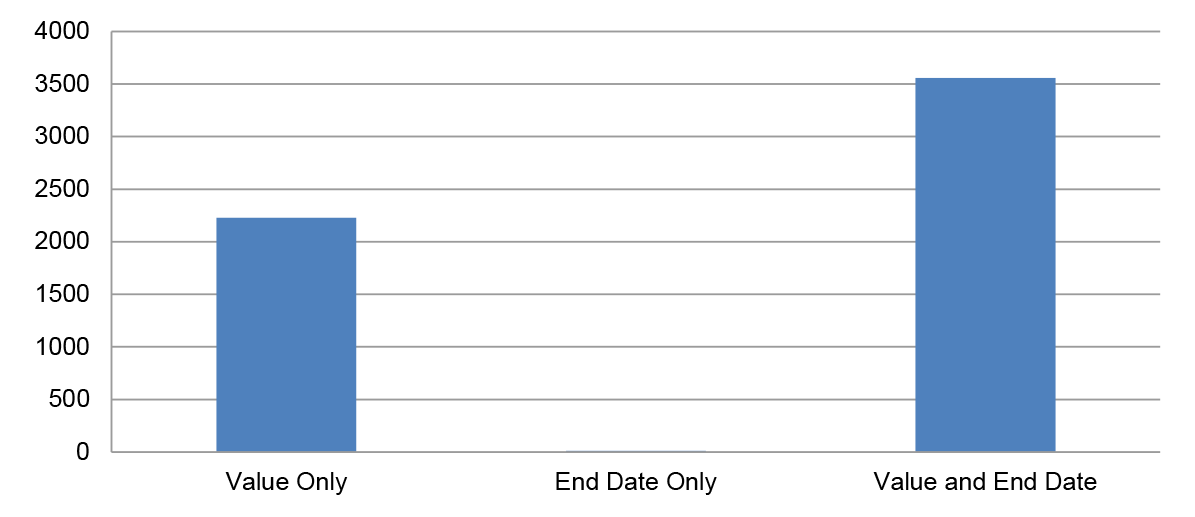

14.6 The following analysis looks at only those contracts that were amended within 12 months of the contracts original publish date.

Figure 14.3: Number of contracts amended within 12 months of contracts original publish date – field/s amended

Source: ANAO Analysis of AusTender data.

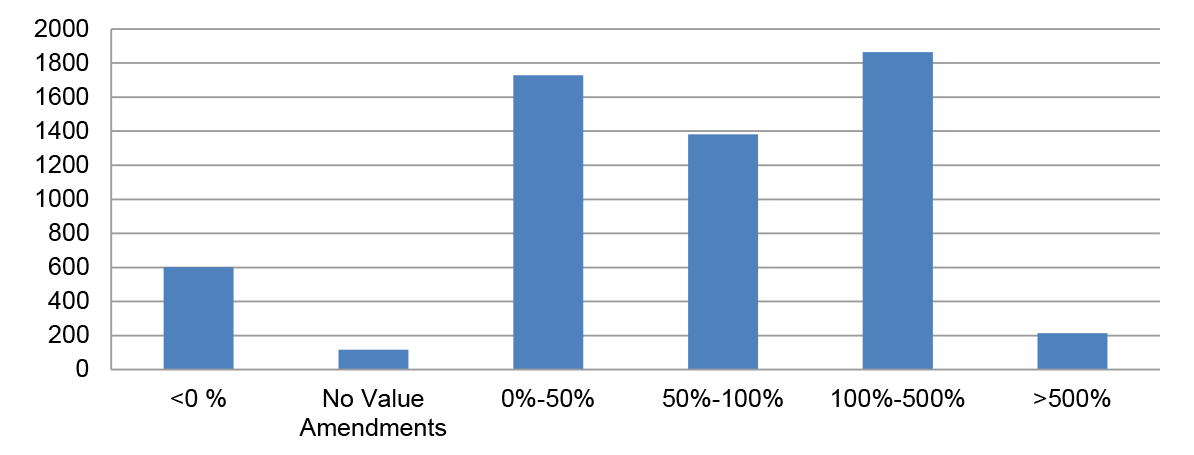

Figure 14.4: Contracts amended within 12 months of original publish date – percentage change in contract value

Source: ANAO Analysis of AusTender data.

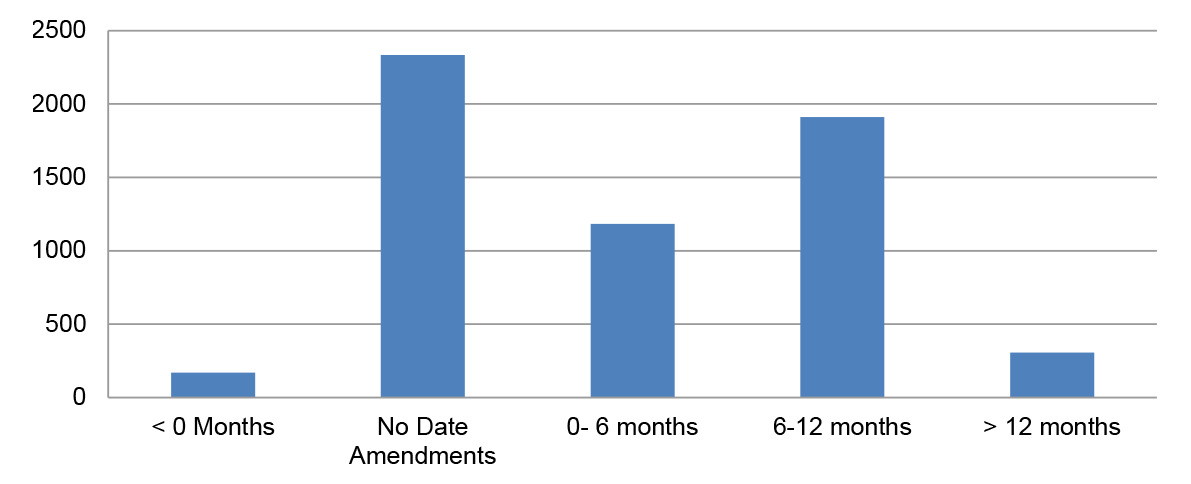

Figure 14.5: Contracts amended within 12 months of original publish date – changes to contract end dates

Source: ANAO Analysis of AusTender data.