Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 44 of 2024–25

Conduct of Procurements Relating to Two New Child Sexual Abuse-related National Services

Published

Wednesday 18 June 2025

Portfolio

Attorney-General’s

Entity

Attorney-General’s Department

Contact

Please direct enquiries through our contact page.

Activity

Procurement

Audit snapshot

Why did we do this audit?

- The establishment of the new services is part of the response to the 2017 final report of the Royal Commission into Institutional Responses to Child Sexual Abuse.

- The timely conduct of the related procurements is intended to establish services that will provide support and advocacy for a cohort of victims of child sexual abuse and also to protect children by intervening before an individual offends.

Key facts

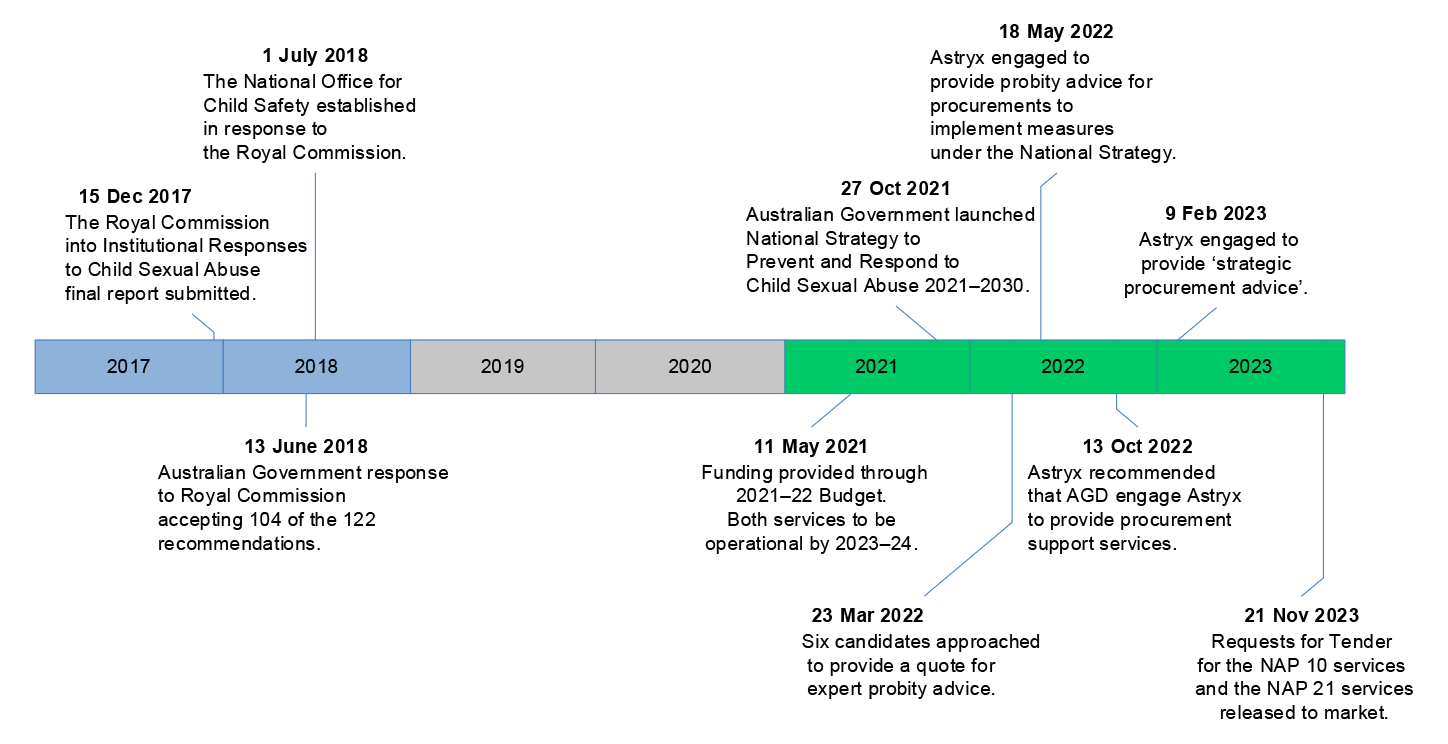

- Requests for Tender were issued in November 2023 to engage service providers to deliver a new national support service for non-offending family members of child sexual abuse perpetrators and a national child sexual abuse offending prevention service.

- Funding for the services was provided through the 2021–22 Budget with the expectation that services would begin to be provided by the start of 2023–24.

- Contracts have not been signed and services are yet to commence.

What did we find?

- The new child sexual abuse-related national services identified as needed by the Royal Commission are not being provided, with no contracts in place for the delivery of those services.

- The procurements did not involve open and effective competition and the selection of preferred tenderers did not demonstrate the achievement of value for money.

- The conduct of the request for tender processes was not timely, non-compliant tenders were accepted for evaluation and ethical requirements were not met.

- Tender evaluation to select preferred tenderers was not well planned, was not timely and did not demonstrably achieve value for money.

What did we recommend?

- The Auditor-General made six recommendations to the department to improve the conduct of procurements.

- The department agreed to the recommendations.

$19.8 m

budgeted for the provision of the new services.

June 2024

notification to preferred tenderer for a national child sexual abuse offending prevention service.

Sept 2024

notification to preferred tenderer for a new national support service for non-offending family members of perpetrators.

Summary and recommendations

Background

1. The National Office for Child Safety (NOCS) was established in July 2018 in response to the Royal Commission into Institutional Responses to Child Sexual Abuse (the Royal Commission). The Royal Commission had reported in December 2017. NOCS was initially located in the Department of the Prime Minister and Cabinet. It was moved in 2022 to the Attorney-General’s Department (AGD) as a result of the June 2022 Administrative Arrangements Order.

2. In October 2021, the Australian Government launched the National Strategy to Prevent and Respond to Child Sexual Abuse 2021–2030 (National Strategy).1 The first phase of the National Strategy includes two four-year action plans (from 2021 to 2024): the First National Action Plan (NAP), to be delivered by Commonwealth, state and territory governments; and the First Commonwealth Action Plan, to be delivered by Commonwealth agencies.

3. NOCS is responsible for launching three new national support services. The provision of the three national support services is to be contracted. The approach to procuring service providers for NAP Measures 7, 10 and 21 was considered in the same procurement strategy, in which the department stated, ‘the three services are in varying stages of development and would likely be ready to approach the market at different times throughout 2023’. A Request for Tender (RFT) process has been undertaken for NAP Measures 10 and 21. Procurements have also been undertaken for the advisers and consultants to assist with the NAP Measure procurement processes as well as an evaluation provider for the NAP 10 and NAP 21 services.

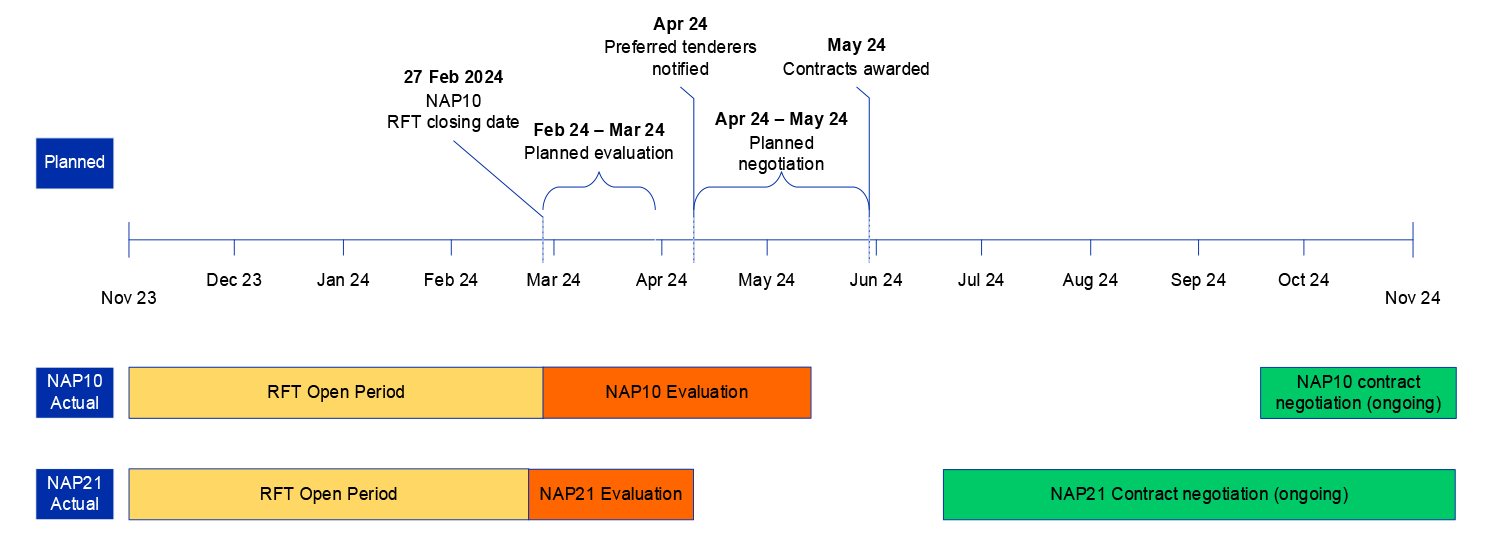

4. There will be a lag between contracts being signed and services being provided to non-offending family members of child sexual abuse perpetrators (NAP 10) and persons at risk of offending or re-offending (NAP 21). The contractual arrangements that were the subject of the RFTs set out that there would be four phases to service delivery. The first two phases are, on the basis of the tender responses from the two preferred tenderers, expected to take at least five to six months. Those phases involving planning, design and establishing the infrastructure to enable service delivery (including the operation of the helplines and provision of websites) to commence in the third phase. Service delivery to citizens commences in the third phase. The offer periods were extended in January 2025 from August 2024 to April 2025 and the department advised the ANAO in April 2025 that the preferred tenders had agreed to further extend their offer periods (to 31 July 2025).

Rationale for undertaking the audit

5. The establishment of the new services is part of the response to the 2017 final report of the Royal Commission into Institutional Responses to Child Sexual Abuse. The timely conduct of the related procurements is intended to establish services that will provide support and advocacy for a cohort of secondary victims of child sexual abuse perpetration and protect children by intervening before an individual offends. The audit was conducted to provide assurance to the Parliament about the establishment of the two new national services, as well as the department’s approach to procurement.

Audit objective and criteria

6. The audit objective was to assess whether the Attorney-General’s Department’s conduct of the procurements relating to two of the new child sexual abuse-related national services employed open and effective competition and achieved value for money, consistent with the Commonwealth Procurement Rules (CPRs).2

7. The new child sexual abuse-related national services identified as needed by the Royal Commission and agreed by government are not being provided, with no contracts in place for the delivery of those services as at May 2025. The audit examined the conduct of the procurements up to the point at which preferred tenderers were selected as representing the best value for money, and did not examine the conduct of contract negotiations given they had not been completed.

8. To form a conclusion against the objective, the following high-level criteria were adopted.

- Were the procurement processes open, competitive, fair and non-discriminatory?

- Was the selection of preferred tenderers consistent with achieving value for money?

Conclusion

9. The Attorney-General’s Department’s conduct of the procurements for two of the new national services (NAP 21 and NAP 10) did not involve open and effective competition and the selection of preferred tenderers was not consistent with achieving value for money. There have been significant delays with the conduct of both procurements and the preferred tenders were not capable of being accepted by the department without further clarification and negotiation. The offer validity periods expired with substantive matters continuing to be negotiated with each preferred tenderer.3 While the department selected preferred tenderers in June 2024 (for NAP 21) and September 2024 (for NAP 10) as offering the best value for money through a competitive procurement process, since then it has, in effect, conducted limited tenders with the two preferred tenderers, in circumstances that do not satisfy the conditions for a limited tender set out in the Commonwealth Procurement Rules (CPRS).4

10. The Attorney-General’s Department (AGD) conducted a single-stage, open approach to market for each of the NAP 10 and NAP 21 services. In most respects, the Request for Tender (RFT) documentation for the NAP 10 and NAP 21 procurements identified the information required by the Commonwealth Procurement Rules. The procurement processes were not conducted in accordance with the Commonwealth Procurement Rules. Of note:

- Seven of the 11 tenders received for the NAP 10 and NAP 21 procurements were not compliant with one or more of the requirements set out in the RFTs. This included six tenders that did not provide all of the pricing information that the RFT stated was required to be submitted to inform evaluation. The department’s approach did not include any marking down of the evaluation of those tenderers against the price criterion to reflect that information required by the RFT had not been provided. The two preferred tenderers were in the cohort of seven.

- The procurement processes were not consistently conducted in accordance with ethical requirements. The engagement of the probity adviser was through a process that lacked probity, and the later engagement (without any competition) of the probity adviser to also provide strategic procurement advice adversely impacted the independence and objectivity of the probity adviser.5 The declaration and management of conflicts of interest was also not to an appropriate standard. This included ineffective management of a conflict the chair of the Evaluation Committee for the NAP 21 procurement had with the tenderer that emerged as the preferred candidate.

11. In relation to advisers and consultants to support the conduct of the NAP 10 and NAP 21 service procurements, competition was not employed for five of the nine engagements and the department did not evaluate candidates against the specified criteria for each of the procurements.

12. The procurements were not timely with the result that selection of preferred tenderers occurred later than planned, no contracts are in place as of May 2025 and services are not being provided. The approach to evaluation was not designed and conducted in a way that enabled the Attorney-General’s Department (AGD) to demonstrate achievement of value for money in the selection of preferred tenderers for the National Action Plan Measure 10 (NAP 10) and National Action Plan Measure 21 (NAP 21) procurements.

- Departmental records do not document how the budgeted funding amounts for services were arrived at. Awarding the contracts to tenders that were less than the budgeted funding was an important element of procurement planning yet the price criterion was not one of the weighted evaluation criteria. The budgeted amounts played an important role in the outcome of the procurement process for the NAP 10 procurement.

- While tender evaluation plans were in place prior to the closing date for the NAP 10 and NAP 21 tenders, they did not adequately address how the department planned to evaluate the pricing information tenderers were required to include. The department also admitted into evaluation tenders that had not provided all of the required pricing information (including from the two preferred tenderers).

- The conduct of the tender evaluation for the NAP 10 and NAP 21 procurements was not timely. It was also not consistent with approach to market documents.

- The department’s evaluation records do not clearly demonstrate that the preferred tenderers for the NAP 10 and NAP 21 procurements provided the best value for money.

13. The processes to engage the consultants and advisers to support the NAP 10 and NAP 21 procurements also did not demonstrate value for money. This was due to an absence of competition and/or value for money not being assessed, or the successful candidate not being assessed as providing the best value for money.

Supporting findings

Open and competitive procurement

14. Open tender approaches to market were employed to engage the service providers for the NAP 10 and NAP 21 services. The procurement approach to engage the evaluation provider was a panel procurement, which involved approaching 12 candidates to respond to a RFQ. When procuring advisers and consultants to assist with the NAP 10 and NAP 21 procurements, the department’s processes involved some competition for less than half of the engagements and no competition for more than half of the engagements, which is inconsistent with the Commonwealth Procurement Rules. (See paragraphs 2.3 to 2.16)

15. In most respects, the RFT documentation for the NAP 10 and NAP 21 procurements issued by AGD identified the information required by the CPRs. This included the conditions for participation, minimum content and format requirements and evaluation criteria. AGD did not clearly identify the relative importance of each of the criteria to be applied in the evaluation processes. (See paragraphs 2.17 to 2.34)

16. With one exception, all tenders accepted for evaluation had been lodged by the specified closing date. ( See paragraphs 2.35 to 2.36)

17. Six of the tenders received for the NAP 10 and NAP 21 procurements were not compliant with the requirements of the RFT. The two preferred tenderers were not compliant with all of the requirements set out in the RFT, as neither had submitted all of the pricing information that the RFT had said was required. In addition, for the NAP 21 procurement, for the preferred tenderer the evaluation report identified 24 items related to service delivery, the solution/technical issues, legal/contract issues and pricing issues for which additional information was required by the department before a contract negotiation directive could be prepared. The department’s approach also did not satisfy the requirement of the CPRs that further consideration only be given to submissions that meet minimum content and format requirements. Three of the tenders for the NAP 10 and NAP 21 procurements that did not meet those requirements were progressed to evaluation before the department sought to address the situation. (See paragraphs 2.37 to 2.43)

18. Tenders for the NAP 10 and NAP 21 procurements were not fully and fairly evaluated against each of the criteria. In relation to the price criterion, tenderers were required to provide information under three scenarios (low, medium and high call volumes). The department did not evaluate tenders under each of the three scenarios because not all tenderers provided the required information. For the NAP 21 procurement, the department analysed the high volume call scenario whereas, for the NAP 10 procurement, the medium call volume scenario was used. The department’s approach reflects that it accepted for evaluation tenders that had not provided all the required price information and so it used the call volume scenario in each tender where it had a response from all tenderers. The approach to evaluation did not include any marking down of the evaluation against the price criterion for the tenderers that had not provided all of the required information.

19. In relation to the evaluation provider procurement, a second evaluation panel had to convene to re-evaluate responses after the department became aware it had not evaluated all four of those received.

20. For one of the procurements of advisers, the department’s evaluation did not address a mandatory requirement such that it had to retract its advice that the candidate assessed as offering value for money was preferred after it eventuated that the candidate did not meet the requirement. (See paragraphs 2.44 to 2.91)

21. The department did not conduct all tender clarification and collaboration activities in a fair and transparent manner as required by the Commonwealth Procurement Rules. (See paragraphs 2.92 to 2.105)

22. The department’s procurement processes did not demonstrate ethical conduct as required by the Commonwealth Procurement Rules.6 This included the approach employed to procuring the probity adviser. The department did not have an effective approach to the declaration, and management, of conflicts of interest. (See paragraphs 2.106 to 2.151)

Demonstrating achievement of value for money

23. Departmental records do not document how the budgeted funding amounts for services were arrived at. (See paragraphs 3.2 to 3.8)

24. There have been significant delays with the department’s conduct of the procurements with the result that the services aimed at protecting children from sexual abuse by intervening before an individual offends or re-offends, and at providing nationally available free support to non-offending family members of child sexual abuse perpetrators, are not yet available. The Requests for Tender (RFTs) were issued later than had been planned by the department. It also took longer than planned to evaluate the tender responses, select the preferred tenderers (who were notified in June 2024 and September 2024) and enter into contract negotiations. The offer validity periods expired with substantive matters continuing to be negotiated with each preferred tenderer. Should contract negotiations be successful, the department expects that services will not begin to be provided until mid-2025, which would be four years and eight months after the National Strategy was released. (See paragraphs 3.9 to 3.19)

25. Tender evaluation plans were in place prior to the closing date for the NAP 10 and NAP 21 tenders. The evaluation plans had not been signed off by the probity adviser. The evaluation plans did not adequately address how the department planned to evaluate the pricing information tenderers were required to submit. (See paragraphs 3.20 to 3.30)

26. The conduct of the tender evaluation for the NAP 10 and NAP 21 procurements was not timely and was not consistent with approach to market documents. (See paragraphs 3.31 to 3.44)

27. The department’s evaluation records do not clearly demonstrate that the preferred tenderers provided the best value for money.

- Each of the two preferred tenderers had not provided all of the information the RFT had identified as being required.

- For the NAP 21 procurement, after it was selected as the preferred tenderer, the department obtained significant additional information from the tenderer related to service delivery, the solution/technical issues and legal/contract issues. The need for this information was not identified in the tender evaluation report.

- For the NAP 10 procurement, the tenderer that scored highest against the weighted criteria was excluded from participating further in the tender process in favour of the second highest scoring tenderer. There were also departures from the RFT in terms of the evaluation criteria that were applied, and the approach taken to putting in place a performance guarantee with the successful tenderer. Further, the tender evaluation report did not identify that the department considered there were areas requiring clarification relating to pricing issues and solution/technical issues, including a concern that the tenderer’s pricing for the medium and high call volume scenarios exceeded the budgeted amount for each year of service delivery. (See paragraphs 3.45 to 3.60)

28. The roles and responsibilities of individuals involved in the NAP 10 and NAP 21 procurements set out in the evaluation plans provided for an appropriate separation of duties between the spending delegate and the Evaluation Committees. The probity adviser was not independent of the procurement processes as it also performed the role of strategic procurement adviser. (See paragraphs 3.61 to 3.65)

29. Appropriate procurement records were partly maintained. While available records addressed the requirement for the NAP 10 and NAP 21 procurements, evidence to support key decisions was not maintained. In addition, the tender evaluation report did not accurately reflect the evaluation process that was employed or satisfactorily demonstrate that value for money had been achieved. There are no records evidencing how the department arrived at the budgeted amounts for the two services. (See paragraphs 3.66 to 3.71)

30. Contracts for the two new services have not been signed, meaning the requirement to report on AusTender has not been triggered. The department met its obligation to report the evaluation provider contract accurately within the 42 day deadline. The department was also required to report on AusTender a number of the adviser and consultant contracts it entered into for the purpose of assisting with the main procurements. There were delays and inaccuracies in reporting of six of the eight contracts that required reporting on AusTender. (See paragraphs 3.72 to 3.74)

Recommendations

Recommendation no. 1

Paragraph 2.25

When conducting procurements, the Attorney-General’s Department clearly identify the relative importance of each of the criteria to be applied in the evaluation process. This should include appropriate weighting of the price criterion in circumstances where a budget has been established for the goods and/or services being procured.

Attorney-General’s Department response: Agreed.

Recommendation no. 2

Paragraph 2.65

When planning procurements, the Attorney-General’s Department:

- ensures that potential suppliers are required to provide all the information that is relevant for the purposes of evaluation, and not ask for any information that is not required;

- where data that is required for evaluation is not provided by a tenderer, this should be reflected in the tender either being excluded or a lower score against the relevant criterion (where the missing information relates to the evaluation criteria); and

- where data that is required for evaluation has been provided, the department should have a plan to evaluate this information and it should be evaluated in full by the department.

Attorney-General’s Department response: Agreed.

Recommendation no. 3

Paragraph 2.104

The Attorney-General’s Department improve its procurement framework to address the conduct of additional processes, including collaboration activities to ensure they are conducted in a fair and transparent manner.

Attorney-General’s Department response: Agreed.

Recommendation no. 4

Paragraph 2.151

The Attorney-General’s Department strengthen its adherence to recognised principles and processes for conducting procurements ethically, including the identification and effective management of conflicts of interest.

Attorney-General’s Department response: Agreed.

Recommendation no. 5

Paragraph 3.29

When developing evaluation plans, the Attorney-General’s Department ensure that the planned evaluation addresses all information tenderers are required to include in submissions.

Attorney-General’s Department response: Agreed.

Recommendation no. 6

Paragraph 3.70

The Attorney-General’s Department improve its procurement record keeping so that accurate and concise information exists on the process that was followed, how value for money was considered and achieved, and relevant decisions and basis of those decisions.

Attorney-General’s Department response: Agreed.

Summary of entity response

31. The proposed audit report was provided to the Attorney-General’s Department and an extract of the proposed report was provided to Astryx Pty Ltd. The Attorney-General’s Department’s summary response is reproduced below.

Attorney General’s Department

The department appreciates the opportunity afforded from the ANAO audit process to improve future procurement practices and accepts the ANAO’s key finding in the Section 19 Report. This includes all six of the ANAO’s recommendations, along with the opportunities for improvement identified throughout. The procurement processes being reviewed were complex in nature and the department made genuine efforts to ensure correct process was followed and ethical requirements were met throughout. The department has already taken steps to improve current procurements being run the by the National Office for Child Safety (NOCS) based on discussions with the ANAO, and is also committed to implementing departmental-wide improvements. The department thanks the ANAO for its audit of the conduct of procurements relating to two new child sexual abused-related national services, and is confident that procurement practices of NOCS, and across the whole of the department, will be improved as a result.

Key messages from this audit for all Australian Government entities

32. Below is a summary of key messages, including instances of good practice, which have been identified in this audit and may be relevant for the operations of other Australian Government entities.

Group title

Procurement

Key learning reference

Group title

Probity in procurement

Key learning reference

1. Background

Introduction

1.1 On 12 November 2012, the prime minister announced that she would recommend to the Governor-General that a Royal Commission be appointed to inquire into institutional responses to child abuse. The Royal Commission into Institutional Responses to Child Sexual Abuse (the Royal Commission) presented a final report on 15 December 2017. Of the 409 recommendations, 206 were directed wholly or partially to the Australian Government. On 13 June 2018, the Australian Government released its response to the Royal Commission.

1.2 The National Office for Child Safety (NOCS) was established in July 2018 in response to the Royal Commission. NOCS was initially located in the Department of the Prime Minister and Cabinet. It was moved in 2022 to the Attorney-General’s Department (AGD) as a result of the June 2022 Administrative Arrangements Order.

1.3 In October 2021, the Australian Government launched the National Strategy to Prevent and Respond to Child Sexual Abuse 2021–2030 (National Strategy).7 The National Strategy established a nationally coordinated framework intended to prevent and better respond to child sexual abuse in all settings. The National Strategy was a recommendation of the Royal Commission and responds to approximately 100 other Royal Commission recommendations to address child sexual abuse in all settings.8

1.4 NOCS led the development of the National Strategy and is leading its implementation. The first phase of the National Strategy includes two four-year action plans (from 2021 to 2024): the First National Action Plan (NAP), to be delivered by Commonwealth, state and territory governments; and the First Commonwealth Action Plan, to be delivered by Commonwealth agencies.

1.5 NOCS is also responsible for launching three new national support services, as summarised in Table 1.1. The provision of the three national support services is to be contracted. The approach to procuring service providers for NAP Measures 7, 10 and 21 was considered in the same procurement strategy, in which the department stated, ‘the three services are in varying stages of development and would likely be ready to approach the market at different times throughout 2023’. A Request for Tender (RFT) process has been undertaken for NAP Measures 10 and 21. Procurements have also been undertaken for the advisers and consultants to assist with the NAP Measure procurement processes as well as an evaluation provider for the NAP 10 and NAP 21 services.

Table 1.1: Procurements to establish new national services

|

Service |

Purpose |

RFT issued |

Tender closing date |

|

NAP 7: a website and helpline to assist victims and survivors to access help and information |

The objective of the NAP 7 service is to reduce the risk, extent and impact of child sexual abuse and related harms in Australia by providing a free nationally available information and referral service that provides advice about all forms of child sexual abuse, and connects people with existing national and jurisdictional child sexual abuse and related services and support. |

Not yeta |

Not known |

|

NAP 10: a new national support service for non-offending family members of child sexual abuse perpetrators |

Non-offending family members of child sexual abuse perpetrators are considered secondary victimsa of child sexual abuse perpetration, experiencing trauma associated with the discovery and aftermath of a family member’s perpetration. The objective of the NAP 10 service is to reduce child sexual abuse-related harms by providing nationally available and free support and advocacy for these secondary victims and also working with law enforcement agencies to support how officers engage with secondary victims. |

21 Nov 23 |

27 Feb 24 |

|

NAP 21: a national child sexual abuse offending prevention service |

The objective of the NAP 21 service is to protect children from sexual abuse by intervening before an individual offends or reoffends. It is expected that people will be able to contact the service if they are worried about their own sexual thoughts and behaviours towards children or young people, or when they are worried that an adult is at risk of or is already offending. Advice and guidance are to be provided on:

|

21 Nov 23 |

23 Feb 24 |

Note a: A Request for Expression of Interest (EOI) was published on AusTender on 14 October 2024 seeking responses by 22 November 2024 from parties interested in participating in a potential multi-stage procurement to secure a service provider to deliver the national information and referral service to assist victims and survivors of child sexual abuse and others seeking help and information. In January 2025, AGD advised the ANAO that it ‘anticipates releasing the RFT in or around March 2025 … this is indicative and subject to the outcomes of the EOI, which closed on 22 November 2024 and is currently in the process of evaluations.’ Further advice from AGD to the ANAO in April 2025 was that, due to delays, the department expected to be in a position to release the RFT in June 2025.

Source: ANAO analysis of AGD records.

1.6 There will be a lag between contracts being signed and services being provided to non-offending family members of child sexual abuse perpetrators (NAP 10) and persons at risk of offending or re-offending (NAP 21). The contractual arrangements that were the subject of the RFTs set out that there would be four phases to service delivery. The first two phases are, on the basis of the tender responses from the two preferred tenderers, expected to take at least five to six months. Those phases involving planning, design and establishing the infrastructure to enable service delivery (including the operation of the helplines and provision of websites) to commence in the third phase. Service delivery to citizens commences in the third phase.9 The offer periods were extended in January 2025 from August 2024 to April 2025 and the department advised the ANAO in April 2025 that each of the preferred tenders had agreed to further extend their offer periods (to 31 July 2025).

Rationale for undertaking the audit

1.7 The establishment of the new services is part of the response to the 2017 final report of the Royal Commission into institutional responses to child sexual abuse. The timely conduct of the related procurements is intended to establish services that will provide support and advocacy for a cohort of secondary victims of child sexual abuse perpetration and protect children by intervening before an individual offends. This audit was conducted to provide assurance to the Parliament about the establishment of the two new national services, as well as the department’s approach to procurement.

Audit approach

Audit objective, criteria and scope

1.8 The audit objective was to assess whether the Attorney-General’s Department’s conduct of the procurements relating to two of the new child sexual abuse-related national services employed open and effective competition and achieved value for money, consistent with the Commonwealth Procurement Rules (CPRs).10

1.9 The new child sexual abuse-related national services identified as needed by the Royal Commission are not being provided, with no contracts in place for the delivery of those services as at May 2025. The audit examined the conduct of the procurements up to the point at which preferred tenderers were selected as representing the best value for money, and did not examine the conduct of contract negotiations given they had not been completed.

1.10 To form a conclusion against the objective, the following high-level criteria were adopted.

- Were the procurement processes open, competitive, fair and non-discriminatory?

- Was the selection of preferred tenderers consistent with achieving value for money?

1.11 The audit focused on the design and conduct of the Attorney-General’s Department’s procurement processes in relation to the contracts summarised in Table 1.2. The procurement process for NAP 7 was not examined. As set out in Table 1.1, a Request for Tender for that service had not been released at the time this ANAO performance audit commenced.

Table 1.2: Procurements examined by the ANAO

|

Contract |

Counterparty |

Reported value ($) |

Contract term |

|

NAP 10 service |

NAP 10 Preferred Tenderer |

9,601,467a |

Not yet known |

|

NAP 21 service |

NAP 21 Preferred Tenderer |

7,200,000b |

Not yet known |

|

Evaluation of NAP 10 and NAP 21 services |

ARTD Consultants |

405, 859 |

24 Oct 2024 to 23 Oct 2026 |

|

Legal and commercial adviser |

Australian Government Solicitor |

88,483 |

n/ac |

|

Procurement adviser |

Astryx Pty Ltd |

345,000 |

10 Feb 2023 to 31 Jul 2024 |

|

Probity adviser |

Astryx Pty Ltdd |

298,000 |

18 May 2022 to 30 Jun 2025 |

|

Consultation provider — NAP 10 |

Lonergan Research Pty Ltd |

50,930 |

17 May 2022 to 26 Jul 2022 |

|

Consultation provider — NAP 21 |

Lonergan Research Pty Ltd |

79,420 |

22 Aug 2022 to 25 Nov 2022 |

|

Contact centre adviser — RFT advice |

MinterEllison Consulting |

25,000 |

10 Oct 2023 to 24 Nov 2023 |

|

Contact centre adviser — evaluation advice |

MinterEllison Consulting |

55,640 |

20 Feb 2024 to 31 Aug 2024 |

|

NAP 21 Evaluation Committee member |

Broomhall Consulting Psychology |

14,124 |

15 Jan 2024 to 30 Aug 2024 |

|

NAP 10 Evaluation Committee member |

Morag McArthur |

10,660e |

23 Jan 2024 to 27 Jul 2024 |

Note a: A contract with the preferred tenderer has not been signed. AGD’s estimated value of the procurement has been used. This estimate includes a reduction of $0.6 million of the $10.2 million that the department recorded as being provided through the 2021–22 Budget. The department allocated $0.6 million for staffing, travel, consultations, and evaluation.

Note b: A contract with the preferred tenderer has not been signed. AGD’s estimated value of the procurement has been used. This estimate includes a reduction of $2.4 million of the $9.6 million that the department recorded as being provided through the 2021–22 Budget. The department reduced the budgeted amount by $1.6 million it had allocated to other expenses and by a further 10 per cent ($0.8 million) at the suggestion of the department’s probity adviser.

Note c: In February 2025, AGD advised the ANAO that ‘a contact term does not exist between the department and AGS as AGS is part of the department. Arrangements for the provision of advice related to these procurements are covered in the email correspondence between the department and AGS… This differs to other Commonwealth agencies where a contract may exist. As of 1 July 2019, AGS uses an internal charging (cost recovery) model for all legal work’.

Note d: Astryx is engaged through a subcontracting arrangement with ServeGate Australia Pty Ltd.

Note e: The reported value does not reflect the amended value of $17,589. The department has not met its reporting obligation.

Source: ANAO analysis of AGD records.

1.12 The tender evaluation plans for the NAP 21 and NAP 10 procurements each identified that tender evaluation would be completed by the end of April 2024, with a recommendation then provided to the decision-maker within AGD. These were the same timeframes that had been set out in the respective RFTs, with tenderers informed that the NAP 10 contract would be awarded by the end of April 2024, and the NAP 21 contract in May 2024. AGD selected preferred tenderers in June 2024 (NAP 21) and September 2024 (NAP 10) as offering the best value for money following competitive procurement processes. As of May 2025, contract negotiations remained ongoing.

Audit methodology

1.13 The audit methodology involved:

- examination and analysis of Attorney-General’s Department records;

- meetings with departmental staff; and

- consideration of the citizens contributions to the audit that were received, including from some of the tenderers for the NAP 10 and NAP 21 procurements.

1.14 The audit was conducted in accordance with ANAO Auditing Standards at a cost to the ANAO of approximately $610,000.

1.15 The team members for this audit were Sean Neubeck, Lachlan Miles and Brian Boyd.

2. Open and competitive procurement

Areas examined

The ANAO examined whether the procurement process was open, competitive, fair and non-discriminatory.

Conclusion

The Attorney-General’s Department (AGD) conducted a single-stage, open approach to market for each of the NAP 10 and NAP 21 services. In most respects, the Request for Tender (RFT) documentation for the NAP 10 and NAP 21 procurements identified the information required by the Commonwealth Procurement Rules. The procurement processes were not conducted in accordance with the Commonwealth Procurement Rules. Of note:

- Seven of the 11 tenders received for the NAP 10 and NAP 21 procurements were not compliant with one or more of the requirements set out in the RFTs. This included six tenders that did not provide all of the pricing information that the RFT stated was required to be submitted to inform evaluation. The department’s approach did not include any marking down of the evaluation of those tenderers against the price criterion to reflect that information required by the RFT had not been provided. The two preferred tenderers were in the cohort of seven.

- The procurement processes were not consistently conducted in accordance with ethical requirements. The engagement of the probity adviser was through a process that lacked probity, and the later engagement (without any competition) of the probity adviser to also provide strategic procurement advice adversely impacted the independence and objectivity of the probity adviser. The declaration and management of conflicts of interest was also not to an appropriate standard. This included ineffective management of a conflict the chair of the Evaluation Committee for the NAP 21 procurement had with the tenderer that emerged as the preferred candidate.

In relation to advisers and consultants to support the conduct of the NAP 10 and NAP 21 service procurements, competition was not employed for five of the nine engagements and the department did not evaluate candidates against the specified criteria for each of the procurements.

Areas for improvement

The ANAO made four recommendations aimed at the department: clearly identifying the relative importance of each of the criteria to be applied in the evaluation process for procurements; an improved approach to obtaining and using relevant information to inform tender evaluations; improving its procurement framework to address the conduct of collaboration activities and similar processes to ensure they are conducted in a fair and transparent manner; and improved approaches to identifying and managing conflicts of interest.

The ANAO also identified opportunities for the department to improve its approach to ensuring all candidates in procurement processes receive addenda to the information provided to the market, and ensuring that the provision of advice within the department to senior officers is relevant and comprehensive, is not affected by fear of consequences, and does not withhold important facts or bad news.

2.1 Competition is a key element of the Australian Government’s procurement framework set out in the Commonwealth Procurement Rules (CPRs).11 Effective competition requires non-discrimination and the use of competitive procurement processes.

2.2 Generally, the more competitive the procurement process, the better placed an entity is to demonstrate that it has achieved value for money. Competition encourages respondents to submit more efficient, effective and economical proposals. It also ensures that the purchasing entity has access to comparative services and rates, placing it in an informed position when evaluating the responses. Openness in procurement involves giving suppliers fair and equitable access to opportunities to compete for work while maintaining transparency and integrity of process.

Were open approaches to market employed?

Open tender approaches to market were employed to engage the service providers for the NAP 10 and NAP 21 services. The procurement approach to engage the evaluation provider was a panel procurement, which involved approaching 12 candidates to respond to a RFQ. When procuring advisers and consultants to assist with the NAP 10 and NAP 21 procurements, the department’s processes involved some competition for less than half of the engagements and no competition for more than half of the engagements, which is inconsistent with the Commonwealth Procurement Rules.

2.3 The CPRs require ‘relevant entities’12 to use AusTender to publish open tenders and, to the extent practicable, make relevant request documentation available.13 An open tender involves publishing an open approach to market and inviting submissions.14 Potential suppliers must be given at least 25 days to lodge a submission from the date and time that a relevant entity publishes an approach to market.15

NAP 10 and NAP 21 procurements

2.4 The RFTs were developed by the department between June 2023 and November 2023. In developing the RFT, the department obtained a copy of the RFT developed by the Department of Social Services for its 2020 to 2022 procurement of counselling and support services provided through 1800RESPECT. The ANAO performance audit of that tender process concluded that it was effective and complied with the CPRs.16

2.5 On 21 November 2023, the department released RFTs on AusTender to engage service providers for NAP 10 and NAP 21.

2.6 A total of 11 addenda17 were issued by the department between 29 November 2023 and 19 February 2024 (eight days prior to the closing date for the NAP 10 procurement) to provide documents omitted during the original release, the link for an industry briefing, and to respond to or clarify potential tenderers’ enquiries.18

2.7 Tenders were required to be lodged by 23 February 2024 for the NAP 21 procurement and 27 February 2024 for the NAP 10 procurement. Potential suppliers had more than three months to respond to the RFTs. The RFT process resulted in six tenders being received for the NAP 10 procurement, and five tenders for the NAP 21 procurement.

Evaluation provider

2.8 The procurement approach to engage the evaluation provider was a panel procurement. The department recorded that it would approach organisations with significant experience and expertise in evaluating services and programs in relevant sectors, including social services, children and family services, family and domestic violence services, sexual abuse and child sexual abuse victim support services, and offending prevention and intervention programs. In September 2023, the department shortlisted 13 candidates of 89 organisations identified by the department on the Management Advisory Services (MAS) Panel19 listed under ‘program/project evaluation’ following its research on each organisation’s level of evaluation experience or expertise in social/criminology service (or project) evaluations in relevant sectors.

2.9 On 19 December 2023, RFQs were issued to 12 candidates of 89 program/project evaluation panellists to respond to a Request For Quote (RFQ) (see Table 2.1) on the MAS Panel.20 The department incorrectly attached the RFQ intended for a different supplier to the email to one candidate. That candidate did not provide a response to the RFQ. The closing date for responses was 16 February 2024.

2.10 Two addenda were issued by the department to respond to questions from candidates.21 The second addendum issued on 9 February 2024 to all 12 candidates included a revised RFQ and an extension of the RFQ closing date to 15 March 2024 (the original closing date was 16 February 2024).

2.11 Four responses to the RFQ were received.

Advisers and consultants

2.12 Table 2.1 outlines the extent of competition employed in the procurements of the advisers and consultants, as well as the evaluation provider.

Table 2.1: Extent of competition

|

Adviser/ consultant |

Services |

Expected value of the procurement ($) |

Reported procurement method |

Extent of competition |

|

Astryx Pty Ltd |

Probity adviser |

920,000 |

Open tender — panel |

RFQ to six candidates on 23 March 2022. Four responses from three candidates were received. |

|

Lonergan Research Pty Ltd |

Consultation provider (NAP 10) |

40,000 |

Limited tender |

RFQ to fifteen candidates on 21 April 2022 One response was received. |

|

Lonergan Research Pty Ltd |

Consultation provider (NAP 21) |

79,000 |

Limited tender |

RFQ to 19 candidates on 27 June 2022. Two responses were received that exceeded the $80,000 threshold that requires an Open Tender approach to be used or a Limited Tender exemption sought. The contracted price was negotiated down to below the threshold. |

|

Astryx Pty Ltd |

Strategic procurement adviser |

Not estimated |

Open tender — panel |

No competition. The reported procurement method does not reflect that this was a sole source procurement. |

|

Australian Government Solicitor |

Legal and commercial adviser |

88,483 |

Not reported (limited tender) |

No competition. |

|

MinterEllison Consulting |

Contact centre adviser — RFT advice |

Less than 20,000 |

Open tender — panel |

RFQ to ten candidates on 14 September 2024.Two compliant responses were received. MinterEllison Consulting was rated as providing ‘low value for money’. The candidate rated as providing the best value for money and notified that it had been successful was later notified that its proposal no longer met the requirements. |

|

MinterEllison Consulting |

Contact centre adviser — evaluation advice |

25,000 |

Open tender — panel |

No competition. The reported procurement method does not reflect that this was a sole source procurement. |

|

Broomhall Consulting Psychology |

Evaluation Committee member |

Less than 20,000 |

Limited tender |

No competition. Although AGD stated in the record of its spending approval that the candidate was identified following a ‘rigorous process’, only one candidate was approached ‘to avoid damaging existing relationships with the child safety sector’. |

|

Morag McArthur |

Evaluation Committee member |

Less than 20,000 |

Limited tender |

No competition. The department recorded that one candidate was approached ‘to avoid damaging existing relationships with the child safety sector’. |

|

ARTD Consultants |

Evaluation provider |

255,000 |

Open tender — panel |

RFQs were issued to 12 candidates of 89 program/project evaluation panellists on 19 December 2023. Four responses were received. |

Source: ANAO analysis of AGD records.

2.13 Of the nine procurement processes for advisers and consultants, five involved no competition. This included the engagement of Astryx Pty Ltd (Astryx) as the ‘strategic procurement adviser’ (also referred to as the ‘specialist procurement adviser’), which followed a recommendation from Astryx in its capacity as the probity adviser that it should be engaged to provide the additional services. While the procurement method was reported on AusTender as an open tender through a panel arrangement that was established by open tender, this does not reflect the process that occurred (see paragraphs 2.114 to 2.119).

2.14 In December 2024, the department advised the ANAO that it procured Astryx ‘without an open tender process as enabled through the SME [Small and Medium Enterprise] exemption to the CPRs’. The department was referring to the list of procurements in Appendix A of the CPRs that are exempt from the rules of Division 2 of the CPRs and from paragraphs 4.7, 4.8 and 7.26 of Division 1. As noted in paragraph 2.13, the procurement method was reported on AusTender as open tender. The department had not sought to rely on this exemption at the time it conducted the procurement.

2.15 There was some competition for four of the nine procurements, largely involving RFQs being issued to a number of the providers on a panel. This included the two processes for consultation providers, which resulted in the engagement of the same provider. The CPRs require entities to estimate the expected value of a procurement before a decision on the procurement method is made.22 This is to assess whether the procurement value is greater than the relevant threshold (in this case $80,000), and if it is, an open tender must be employed or a limited tender condition sought. The estimated value for both procurements was below $80,000 ($40,000 for the NAP 10 consultation, and $79,000 for the NAP 21 consultation). The planning for the procurements was that the department would approach candidates it had identified from an existing panel as well as through comparable procurements previously undertaken by NOCS. Limited tender was considered to be the ‘most appropriate procurement approach’ due to the procurement activities being under the relevant threshold and the ‘administrative burden’ related to the panel.

2.16 In advice23 on the department’s proposed response to a potential supplier’s enquiry regarding where the approach to market was advertised, the probity adviser described the department’s approach to the procurement as containing ‘ambiguity in how the suppliers were identified’ due to:

- the absence of criteria used to decide whether to include or exclude a panel supplier;

- the expected value calculated as $79,000 and the perception that it ‘conveniently’ falls under the $80,000 threshold24; and

- why the panel, managed by Services Australia, was an ‘administrative burden’ leading to it not being used.25

Did the request documentation clearly set out the requirements to participate and the approach to evaluation including the criteria that would be employed and any weightings to be applied?

In most respects, the RFT documentation for the NAP 10 and NAP 21 procurements issued by AGD identified the information required by the CPRs. This included the conditions for participation, minimum content and format requirements and evaluation criteria. AGD did not clearly identify the relative importance of each of the criteria to be applied in the evaluation processes.

2.17 The CPRs outline that request documentation must include a complete description of:

- any conditions for participation, including financial guarantees, information and documents that potential suppliers are required to submit;

- any minimum content and format requirements; and

- evaluation criteria to be considered in assessing submissions and, if applicable to the evaluation, the relative importance of those criteria.26

2.18 The CPRs also include a requirement that non-corporate Commonwealth entities, such as the Attorney-General’s Department, comply with procurement-connected policies where the policy indicates that it is applicable to the procurement process.27

Requirements to participate

2.19 The same three conditions for participation were included in the RFT Conditions of Tender for both procurements. While the request documentation for both procurements included the same four minimum content and format requirements, the NAP 10 RFT included an additional requirement. The additional requirement was that the tender complies with a clause requiring tender responses to be lodged electronically via AusTender before the RFT closing time and in accordance with the tender response lodgement procedures set out in the RFT documentation and on AusTender.28

2.20 Consistent with the Shadow Economy Procurement-Connected policy, the conditions for participation and minimum content and format requirements included the requirement for tenderers to provide a valid Statement of Tax record.

Evaluation approach and criteria

2.21 The request documentation set out, consistent with the CPRs, that tenders would be evaluated to identify the tender that represented the best value for money on the basis of evaluation criteria. It defined value for money as ‘a comprehensive assessment involving a comparative analysis of the relevant financial and non-financial costs and benefits of the Tenders, including risk’.

2.22 The request documents for both procurements set out that the criteria to be applied for the purposes of evaluation were ‘not in any order of importance’. In contradiction to this statement, tables containing the criteria included a list of four criteria with weightings of decreasing magnitude. The first of the four criteria (‘service delivery’ in each case) was weighted as the most important — 50 per cent for NAP 10, and 55 per cent for NAP 21. The weighted criteria were followed by a list of non-weighted criteria, including the criterion related to price.

2.23 This approach does not satisfy the requirement of the CPRs that request documentation set out the ‘evaluation criteria to be considered in assessing submissions and, if applicable to the evaluation, the relative importance of those criteria’. Further, the decision to not weight the price criterion did not have a rationale. This is important given the department’s procurement planning set out that the approach to market for the two tenders would include asking respondents to outline what level of service they could provide for the budgeted amounts.

2.24 The remaining non-weighted criteria were to ‘also be considered as part of the evaluation process’.29 The request documentation did not include information to demonstrate to potential respondents the relative importance of the non-weighted criteria, or the proposed approach to evaluating the extent to which tender responses met the criteria. This meant that the request documentation did not make clear the considerations that were of relative importance to the evaluation in terms of demonstrating value for money.

Recommendation no.1

2.25 When conducting procurements, the Attorney-General’s Department clearly identify the relative importance of each of the criteria to be applied in the evaluation process. This should include appropriate weighting of the price criterion in circumstances where a budget has been established for the goods and/or services being procured.

Attorney-General’s Department response: Agreed

2.26 The department will develop internal guidance to further support staff in weighting criteria to be applied during tender evaluation processes. This will include advice regarding the appropriate weighting of price criterion, including in circumstances where a budget has been established for the goods and/or service being procured.

Evaluation provider

2.27 The RFQ set out that responses would be evaluated against six evaluation criteria. The criteria were not weighted.

2.28 Important information included in the RFQ was that the service provider ‘may not’ nominate subcontractors to provide some or all of the services, and that ‘Travel will not be paid for by the Service Provider and the Service Provider will not be reimbursed for travel’. These two restrictions were the subject of enquiries from candidates.30

2.29 Two addenda were issued by the department.

- The first addendum, issued on 19 January 2024 to 11 of the 12 candidates31, stated that the successful candidate would not be able to sub-contract its responsibilities and deliverables to another organisation or individual but ‘would be able to work with, consult or collaborate with other organisations, academics, clinicians or experts as necessary’.

- The second addendum, issued on 9 February 2024 to all 12 candidates32 included a revised RFQ. The closing date was extended to 15 March 2024 (from 16 February 2024), and the proposed commencement date was amended to 3 May 2024 (from 29 March 2024). It also included changes to the subcontracting arrangements such that the candidates were allowed to nominate subcontractors to provide specific parts of the services.

2.30 The amendment to the subcontracting arrangements resulted from AGS advice that the RFQ and AGD’s draft second addendum were inconsistent with the terms of the MAS Panel. AGD had not sought AGS advice prior to issuing the RFQ or the first addendum.

Opportunity for improvement

2.31 To treat potential suppliers fairly, the department should issue any addenda to all candidates in a limited tender, and make the addenda available to all potential candidates when the procurement is by way of an open tender.

Procurements of advisers and consultants

2.32 Evaluation criteria were included in six of the nine procurement processes for advisers and consultants. The CPRs were not complied with in relation to the other three of these procurement processes (see paragraph 2.17).

2.33 For one of those six where evaluation criteria were available to potential suppliers, being the procurement of the NAP 10 consultation provider, the criteria that were used to evaluate the one response received by the department were not the same as the evaluation criteria included in the RFQ.

2.34 In addition, the RFQ that was issued to engage a service provider for contact centre advice on the NAP 10 and NAP 21 RFT packages was not well constructed. A requirement for the engagement was for key personnel to hold a baseline security clearance. The requirement was specified in one section — ‘Key personnel’ — but the section that was directly relevant — ‘Security clearance requirements’ — was blank (that is, it neither restated the requirement, nor cross-referenced to the other section). This impacted the evaluation of the responses and the selection of the successful candidate (see paragraphs 2.91 and 3.59).

Were only those tenders submitted by the specified closing date accepted for evaluation?

With one exception, all tenders accepted for evaluation had been lodged by the specified closing date.

2.35 The CPRs require all potential suppliers to lodge submissions in accordance with a common deadline.33 Late tenders must not be accepted unless the submission is late as a consequence of mishandling by the relevant entity.34 Consistent with this requirement, the RFTs for both procurements stated that tenders must be lodged before the closing time, as defined in the RFT.

2.36 A tenderer for the NAP 10 procurement submitted part of its tender response after the closing time of 4:00pm, 27 February 2024, as specified in the RFT (see Table 2.3). After submitting its response, the tenderer, NAP 10 Tenderer 6, emailed the department’s RFT contact officer at 6:10pm on 27 February 2024 a signed tenderer’s deed (required to satisfy the conditions for participation and minimum content and format requirements), which it had not submitted with its tender. Inconsistent with the CPRs, the department accepted the tender for evaluation (tenders were provided to the Evaluation Committee on 6 March 2024). The department did not seek to address this situation until the Initial Screening Report, which recommended the tender be accepted, was provided to and endorsed by the Evaluation Committee for the procurement between 12 March 2024 and 25 March 2024, after evaluations had commenced.

Was the approach to evaluation consistent with the request documents?

Six of the tenders received for the NAP 10 and NAP 21 procurements were not compliant with the requirements of the RFT. The two preferred tenderers were not compliant with all of the requirements set out in the RFT, as neither had submitted all of the pricing information that the RFT had said was required. In addition, for the NAP 21 procurement, for the preferred tenderer the evaluation report identified 24 items related to service delivery, the solution/technical issues, legal/contract issues and pricing issues for which additional information was required by the department before a contract negotiation directive could be prepared. The department’s approach also did not satisfy the requirement of the CPRs that further consideration only be given to submissions that meet minimum content and format requirements. Three of the tenders for the NAP 10 and NAP 21 procurements that did not meet those requirements were progressed to evaluation before the department sought to address the situation.

2.37 The RFTs for the NAP 10 and NAP 21 procurements identified:

- that tenders received after the closing date would be deemed to be a late tender and would not be admitted into evaluation unless the tender was late solely due to mishandling by the department;

- the conditions for participation35;

- the minimum content and format requirements; and

- certain information that was required to be provided as part of the tender. In particular, the RFT identified that tenderers ‘must’ address each of the evaluation criteria by completing various tender response forms. Of note given the nature of the services being procured, tenderers were ‘required’ to provide information on their service pricing for calls of 30 minutes duration under three scenarios (low, medium and high call volumes).36

2.38 In relation to the latter, tenderers were advised in the RFT that the department determined high, medium and low call volume scenarios by examining the call volumes of similar services.37 The RFTs did not permit tenderers to select their own preferred call duration. Rather, they should submit the required information and detail any cost implications if the 30 minute call duration assumption (or the assumption that the service would operate 8 hours a day, 5 days a week (for NAP 10) or 7 days a week (for NAP 21)) was materially different to the actual service operation.38

2.39 As illustrated by Table 2.2, four of the five tenderers for the NAP 21 procurement did not, on the basis of the department’s evaluation records, meet one or more of the above four requirements. The most common area of non-compliance related to the pricing information, specifically the requirement to provide service pricing for 30 minute calls under three call volume scenarios. This included the preferred tenderer which, rather than providing pricing on the basis of 30 minute calls as required by the RFT, outlined in its tender that it was pricing on the basis of 45 minute calls for the three call volume scenarios. The department, while identifying the issue, did not seek to address it until after it had been approved as the preferred tenderer by the spending delegate for the procurement. The assessment of tenders against the price criterion did not reflect that some tenders had not provided all the pricing information the RFT stated was required, or had provided pricing information based on a different call duration assumption. In February 2025, the NAP 21 preferred tenderer advised the ANAO that its perspective39 was that:

- it complied with all RFT requirements and, while a potential alternative was provided that it considered has the potential to enhance the services, it was also prepared to comply with the department’s preference; and

- its call duration assumption was based on experience and engagement with other offender prevention services and the assumption had very minor implications on estimated costs (and no impact on the 100 and 250 call scenarios).

Table 2.2: Compliance with RFT requirements by tenders received for NAP 21

|

Tenderer |

On time |

Minimum content and format |

Conditions for participation |

Required pricing information |

|

NAP 21 Preferred Tenderer |

◆ |

◆ |

◆ |

■ |

|

NAP 21 Tenderer 2 |

◆ |

◆ |

◆ |

■ |

|

NAP 21 Tenderer 3 |

◆ |

◆ |

◆ |

◆ |

|

NAP 21 Tenderer 4 |

◆ |

▲ |

▲ |

■ |

|

NAP 21 Tenderer 5 |

◆ |

◆ |

◆ |

■ |

Key: ◆ denotes that the requirement was met

▲ denotes that the requirement was not met and was addressed by AGD

■ denotes that the requirement was not met and was not addressed by AGD

Source: ANAO analysis of AGD records.

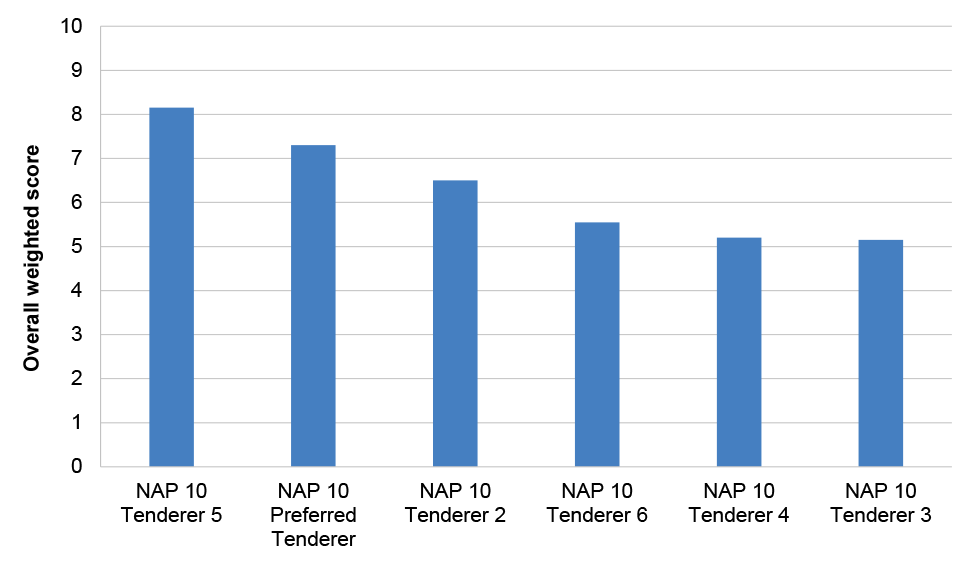

2.40 As illustrated by Table 2.3, three of the six tenders received for the NAP 10 procurement did not, on the basis of the department’s evaluation records, meet one or more of the RFT requirements. Similar to the NAP 21 procurement, the most common area of non-compliance related to the pricing information, specifically the requirement to provide service pricing for 30 minute calls under three call volume scenarios. This included the preferred tenderer which, rather than providing pricing on the basis of 30 minute calls as required by the RFT, outlined in its tender that it was pricing on the basis of 45 minute calls for the three call volume scenarios. The department, while identifying the issue, did not seek to address it at any stage including during collaboration activities. The highest ranked tenderer against the weighted evaluation criteria (NAP 10 Tenderer 5, with an aggregate score 12 per cent higher than the preferred tenderer) was in full compliance with the RFT requirements. Its evaluated price (under the medium call volume scenario) for the first three phases40 of the service was $8.4 million, which was closer to the $8.6 million available for service provision the department had outlined in the request documentation whereas the preferred tenderer’s evaluated price was lower at $7.1 million. The assessment of tenders against the price criterion did not reflect that some tenders had not provided all the pricing information the RFT stated was required, or had provided pricing information based on a different call duration assumption.

Table 2.3: Compliance with RFT requirements by tenders received for NAP 10

|

Tenderer |

On time |

Minimum content and format |

Conditions for participation |

Required pricing information |

|

NAP 10 Preferred Tenderer |

◆ |

◆ |

◆ |

■ |

|

NAP 10 Tenderer 2 |

◆ |

▲ |

▲ |

◆ |

|

NAP 10 Tenderer 3 |

◆ |

◆ |

◆ |

◆ |

|

NAP 10 Tenderer 4 |

◆ |

◆ |

◆ |

◆ |

|

NAP 10 Tenderer 5 |

◆ |

◆ |

◆ |

◆ |

|

NAP 10 Tenderer 6 |

▲ |

▲ |

▲ |

■ |

Key: ◆ denotes that the requirement was met

▲ denotes that the requirement was not met and was addressed by AGD

■ denotes that the requirement was not met and was not addressed by AGD

Source: ANAO analysis of AGD records

2.41 Also highlighted in Table 2.2 and Table 2.3 is that three tenders did not meet the minimum content and format requirements and the conditions of participation. The three tenders were progressed to evaluations before the department sought to address the non-compliances, an approach that does not satisfy the CPRs (see Appendix 3).

Advisers and consultants

2.42 There was one procurement process to engage an adviser in which a response was excluded from evaluation. The RFQ to engage a contact centre adviser for the NAP 10 and NAP 21 RFT packages was issued to 10 candidates on a panel. Three responses were received, all before the RFQ closing time. One of the respondents had not been issued the RFQ by the department. Following advice from AGD’s internal procurement section that this firm had not been approved to participate on the panel, AGD excluded its response from evaluation and advised the firm of its decision.

2.43 In relation to the NAP 10 consultation provider procurement, the department noted in its evaluation that the supplier response form was not used by the one respondent to the RFQ. This was not consistent with the requirements of the RFQ, which stated that the supplier response form must be used. Nevertheless, AGD accepted the response for evaluation.

Were all tenders accepted for evaluation assessed fully and fairly against each of the specified criteria?

Tenders for the NAP 10 and NAP 21 procurements were not fully and fairly evaluated against each of the criteria. In relation to the price criterion, tenderers were required to provide information under three scenarios (low, medium and high call volumes). The department did not evaluate tenders under each of the three scenarios because not all tenderers provided the required information. For the NAP 21 procurement, the department analysed the high volume call scenario whereas, for the NAP 10 procurement, the medium call volume scenario was used. The department’s approach reflects that it accepted for evaluation tenders that had not provided all the required price information and so it used the call volume scenario in each tender where it had a response from all tenderers. The approach to evaluation did not include any marking down of the evaluation against the price criterion for the tenderers that had not provided all of the required information.

In relation to the evaluation provider procurement, a second evaluation panel had to convene to re-evaluate responses after the department became aware it had not evaluated all four of those received.

For one of the procurements of advisers, the department’s evaluation did not address a mandatory requirement such that it had to retract its advice that the candidate assessed as offering value for money was successful after it eventuated that the candidate did not meet the requirement.

2.44 The CPRs set out that relevant evaluation criteria should be included in request documentation to enable the proper identification, assessment and comparison of submissions on a fair, common and appropriately transparent basis.41

2.45 The request documentation for both procurements outlined that tenders were to be evaluated to identify the tender that represents best value for money on the basis of:

- for the NAP 10 procurement, seven evaluation criteria, four of which were weighted and the remaining three (including the price criterion) were not weighted; and

- for the NAP 21 procurement, nine evaluation criteria, four of which were weighted and the remaining five (including the price criterion) were not weighted.

2.46 It further stated that value for money would be a comprehensive assessment involving a comparative analysis of the relevant financial and non-financial costs and benefits of the tenders, including risk.

2.47 All six of the tenders received in response to the NAP 10 RFT, and all five of the tenders received in response to the NAP 21 RFT, were progressed for evaluation.

Conduct of the tender evaluation

2.48 As set out in paragraph 2.22, the RFTs for the two procurements included four weighted criteria as well as various unweighted criteria, which included the criterion related to price. The tender evaluation plans for both procurements included a rating scale that Evaluation Committee members were required to use. Risk descriptions included in the rating scales were also to be used for considering the risk profile of each tender for the unweighted criteria.

2.49 The evaluation plans stated that the results of the price evaluation were not to be scored and weighted. Rather, price would be assessed as part of the overall value for money consideration by the Evaluation Committee. The evaluations plans did not reflect that the RFT package for both procurements required tenderers to prepare and submit five pricing tables (see paragraphs 2.60 and 2.61).

2.50 The conduct and results of the evaluation were recorded in individual evaluation sheets completed by each Evaluation Committee member (to varying degrees, see paragraph 2.54), consensus meeting notes recorded by a procurement support team member and the tender evaluation report (which included as an attachment an assessment sheet that recorded the results of the respective Evaluation Committees’ consensus meeting). The respective Evaluation Committee members signed and endorsed the tender evaluation reports between:

- 9 May 2024 and 22 May 2024, for the NAP 21 procurement; and

- 5 July 2024 and 29 August 2024, for the NAP 10 procurement.

2.51 External advisers engaged by the department for the evaluations were: a legal and commercial adviser (AGS), a probity adviser (Astryx), a procurement adviser (also Astryx) and a ‘contact centre’ adviser (MinterEllison Consulting). Also providing advice to the Evaluation Committee was the department’s Procurement and Framework Team (as the procurement adviser), and the department’s Financial Reporting Team (as the financial adviser).

Errors and flaws in the underlying evaluation records

2.52 There were a number of errors and flaws identified by the ANAO in the department’s records of the underlying evaluations (see Appendix 4). The errors and flaws adversely affected the department’s ability to demonstrate that all tenders were evaluated fully and fairly against the specified criteria.

Evaluation worksheets of Committee members

2.53 The tender evaluation plan for each procurement required that Evaluation Committee members use the ‘evaluation sheets’ provided to them. The tender evaluation plans outlined that those sheets ‘provide guidance on ensuring both compliance and risk are considered against each Evaluation Criteria [sic]’.

2.54 The evaluation sheets used to record the individual evaluations of Evaluation Committee members were generally incomplete and lacked sufficient detail to support the scoring against the weighted criteria, and the risk ratings against the unweighted criteria. This was reflected in the concerns raised by the department’s procurement support team with the department’s probity adviser about the level of detail provided in the evaluation sheets by some committee members, and the department’s request for advice as to whether it was permissible to have such limited detail. The probity advice to the department on 18 April 2024 in respect to the NAP 21 procurement was that:

this is a good lesson learnt to apply to future procurements. Best practice is for workbooks to be uploaded a few days before consensus to enable the secretariat or chair to check them for sufficient detail. Requesting more detail now does not add any value noting the consensus has been. Having sat on the consensus, I’m confident that the members came to an agreed and defendable outcome.

2.55 This lesson was not then applied to the NAP 10 procurement. On 11 June 2024, the department’s procurement support team raised similar concerns about the evaluation sheets as had been raised in relation to the NAP 21 procurement two months earlier. In seeking advice from the probity adviser, it was noted that the records ‘are significantly less completed than expected’. The probity adviser repeated its earlier advice. In February 2025, Astryx advised the ANAO that

the lack of detail in the individual evaluators worksheets was only brought to the attention of the probity advisor after the consensus meeting was held. It was the responsibility of AGD to ensure these were completed prior to closing of evaluations. To provide necessary clarity in the context of this matter, please refer to the detailed minutes that accurately provides a written recorded of the consensus meeting discussions. The probity advisor attended these consensus meetings and did not raise any probity concerns as the discussion was compliant with the process detailed in the approved evaluation plan. There was no probity need to retrospectively go back and update worksheets.

Opportunity for improvement

2.56 The key role of a probity adviser is to advise on whether the current procurement is being conducted in accordance with probity principles. This includes whether the issue on which advice is being sought is acceptable in terms of the approach to market documentation and evaluation plan for the particular procurement. While probity advice may add value by identifying lessons to be learned for future procurements, this should not be the main or sole focus of the advice.

Consensus meetings

2.57 Consensus meetings to agree a single score for each tender against the weighted criteria, and to agree whether the tender had satisfied each unweighted criterion and the associated risk rating, were held by the respective Evaluation Committees. For the NAP 21 procurement, the meetings were on 9 and 10 April 2024. For the NAP 10 procurement, meetings were held over three days from 22 to 24 April 2024.

2.58 The Evaluation Committee for the respective procurements agreed42 a single score for each weighted criterion for all tenders received, along with an associated risk rating. The evaluation records contained some inaccuracies in relation to those scores.

- There was an inconsistency in the score recorded for NAP 10 Preferred Tenderer’s submission against the second criterion for the NAP 10 procurement. The assessment sheet includes a score of ‘8’ (a rating of ‘Very Good’). The records of the consensus meeting are internally inconsistent, including scores of both ‘7’ (‘Good’) and ‘8’ (‘Very Good’) in different sections. The final score recorded in the tender evaluation report was ‘7’ with a rating of ‘Good’.