Areas examined

This chapter examines the Department of Immigration and Border Protection’s (DIBP) procurement processes and decisions relating to the consolidation of contracts for the procurement of garrison support and welfare services in Nauru and on Manus Island in 2013–14. It also examines whether the processes adopted were sound and met the requirements of the Commonwealth Procurement Rules (CPRs).

Conclusion

The department decided to consolidate contracts for the provision of garrison support and welfare services and conducted a limited tender relying on paragraph 10.3(b) of the CPRs– relating to urgent and unforeseen circumstances. The available record does not indicate such circumstances existed. The department first selected the provider and then commenced a process to determine the exact nature, scope and price of the services to be delivered.

The reasons for not continuing with the existing provider (G4S) were not clearly documented. Advice prepared by the department’s Central Procurement Unit was not consistent with the CPRs and the Department of Finance (Finance) guidance on key issues. In seeking advice from Finance, the Unit made written statements implying underperformance by service providers which was not supported by the evidence. The department subsequently referenced Finance’s support in briefings for its Minister.

Engaging Transfield through limited tender procurement placed the department in a position where it removed competition from the process at the outset. When a price was put forward by Transfield it was higher than anticipated and far exceeded that charged by G4S.

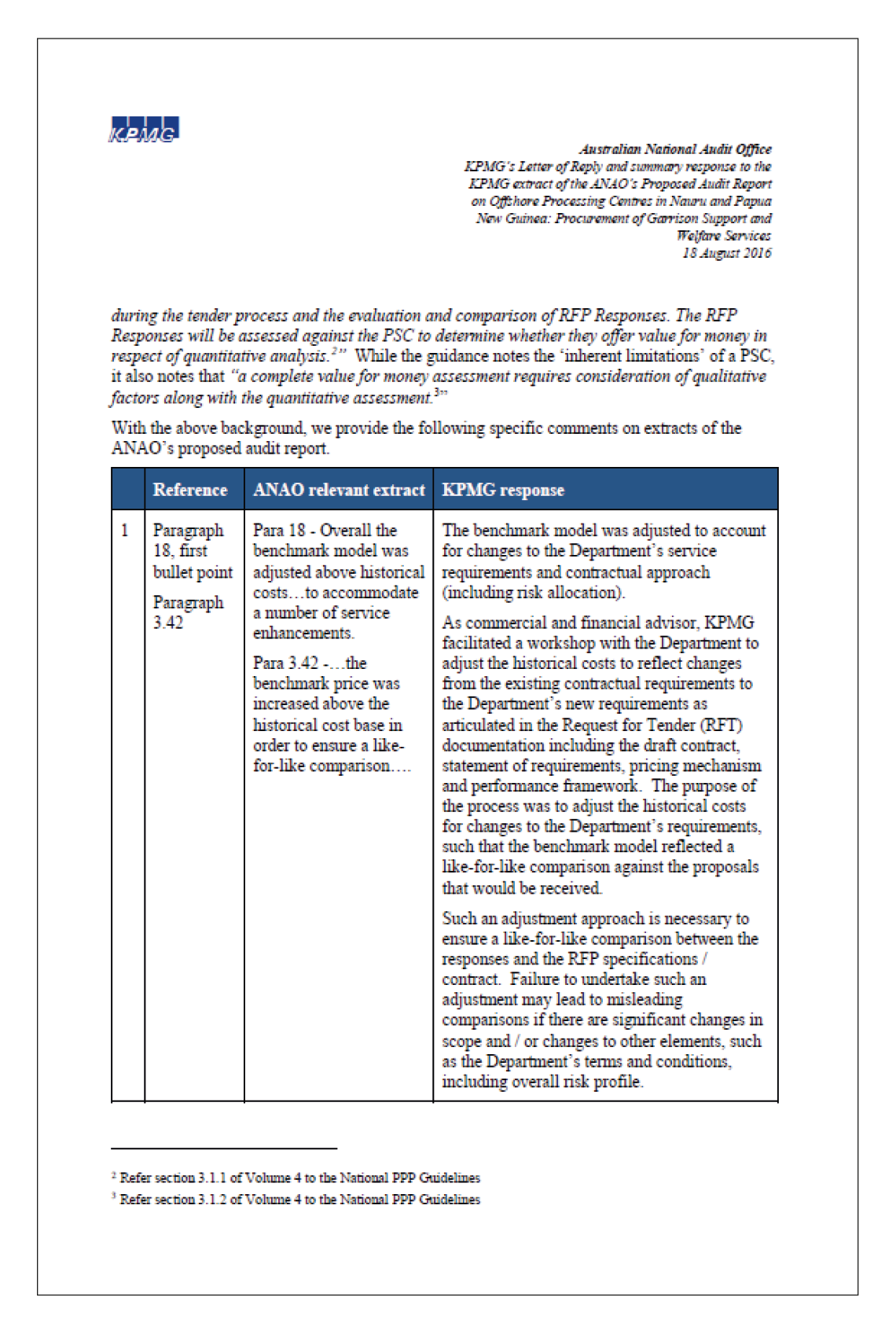

The department applied a benchmark model to demonstrate the achievement of value for money. Overall the benchmark was adjusted above historical costs, upwards to $372 million, to accommodate a number of service enhancements. The Government had directed the department to reduce per-head costs. The department had no authority to increase the funding value of the contract above historic costs.

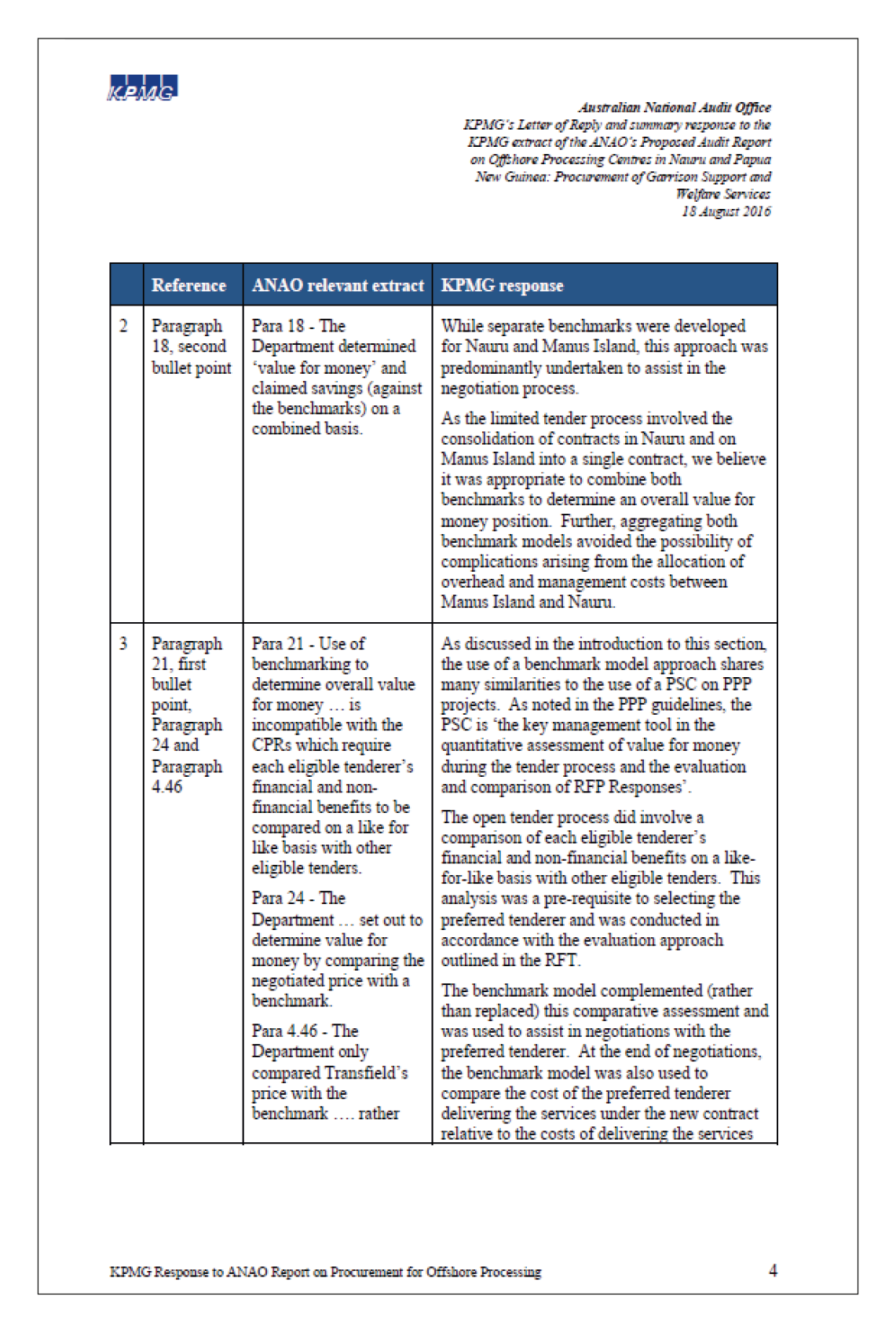

Separate benchmarks were developed for Nauru and Manus Island, but the department determined ‘value for money’ and claimed savings (against the benchmarks) on a combined basis. While Transfield’s bid for Nauru was lower than historical costs, the bid for Manus Island exceeded historical costs by between $200 million and $300 million.

The intent of the consolidation was to achieve innovation and savings. In estimating savings the department based its calculations on higher capacity levels which were never achieved. The department was aware of the fall in the number of new boat arrivals in early 2014, but continued to use higher than actual levels to determine expected costs. This approach resulted in a risk of the Commonwealth locking-in a premium for service delivery under the contract.

The Prime Minister had requested that per head costs be lower as a result of retendering the contracts, but the department did not calculate a per person cost. Finance advised the ANAO that under the consolidated contract, the per person per annum cost of holding a person in the offshore processing centres in Nauru and on Manus Island at the Mid-Year Economic and Fiscal Outlook 2015–16 in December 2015, was $573 111. Prior to consolidation Finance estimated the cost at $201 000.

3.1 The Australian Government commenced Operation Sovereign Borders on 18 September 2013. Operation Sovereign Borders continued the offshore processing of asylum seekers in Nauru and Papua New Guinea (Manus Island). The Government also sought to achieve innovation and savings through consolidating the garrison support and welfare services contracts. At the time, consolidation was considered an interim measure pending an open tender process in 2014.

3.2 Transfield and Save the Children were selected by the department to perform the services. The selection of Transfield (to deliver a consolidated contract) attracted considerable media and parliamentary attention, focusing on:

- the use of limited tender procurement and the exclusion of G4S from the tender process;

- the value of the contract ($2.1 billion) as reported on AusTender;

- reported contract savings of $77 million; and

- recommendations made in the National Commission of Audit (see paragraphs 3.13 to 3.18) including that:

by renegotiating contracts and better targeting of services, the per person cost of operating the onshore immigration network be reduced to 2011–12 levels and similar efficiencies be sought for the offshore network.

3.3 In respect to the consolidation of contracts for garrison support and welfare services in Nauru and on Manus Island, the then departmental Secretary, Mr Martin Bowles PSM advised members of the Legal and Constitutional Affairs Legislation Committee in February 2014, that:

The reason for changing the arrangements on Manus had nothing to do with the performance of the contract. It was to do with trying to get synergies from having one provider working across both islands. The work we have done in the department, trying to understand how we manage those two islands, led us to believe that the best way to do that was with a single contractor. It will drive logistical improvements and further efficiencies when we can actually put them together. The decision, which was ultimately made by me, was that we would transition out of G4S on Manus to Transfield.

3.4 The ANAO reviewed whether the procurement process for the consolidated contract was conducted in accordance with the Commonwealth Procurement Rules (CPRs) and if the contract achieved the innovations and savings required by Government. In particular, the ANAO examined:

- the planning for consolidation and use of limited tender;

- procurement advice;

- contract negotiations and value for money; and

- probity and conflict of interest.

Was the adoption of a limited tender process on the grounds of urgent and unforeseen circumstances appropriately documented and defensible?

The department again relied on paragraph 10.3(b) of the CPRs to conduct a limited tender, on the basis of urgent and unforeseen circumstances, to engage Transfield in Nauru and on Manus Island as part of a contract consolidation process. At the time, consolidation was considered an interim measure pending an open tender process in 2014. The available record does not indicate that urgent or unforeseen circumstances existed but suggests that the department first selected the provider and then commenced a process to determine the exact nature, scope and price of the services to be delivered.

- The department decided not to continue with the existing provider (G4S), but did not clearly document its reasons.

- Advice prepared by the department’s Central Procurement Unit was not consistent with the CPRs and the Department of Finance (Finance) guidance on key issues. In seeking advice from Finance, the Unit made written statements implying underperformance by service providers which was not supported by the evidence. The department subsequently referenced Finance’s support in briefings for its Minister.

Planning for consolidation and the use of limited tender

3.5 The CPRs require that all procurements over the threshold (see Box 1) be undertaken using open tender, unless the conditions for limited tender under paragraph 10.3 can be met, or the procurement is exempt under Appendix A of the CPRs.

3.6 The department began a procurement process which resulted in consolidation of the garrison support and welfare contracts in early November 2013 when the then Minister requested advice on options for service delivery on Manus. Available departmental records indicate that the options canvassed with the Minister’s Office involved the use of limited tender processes which would result in G4S’s contracts being taken over by: Serco as an extension to Serco’s existing onshore contract; or by Transfield as an extension to its contract in Nauru. The option of Save the Children undertaking the Salvation Army’s contract for welfare services was also canvassed.

3.7 Serco advised the ANAO that it was not approached in 2013 to provide services on Manus Island. The department’s records indicate that the option of engaging Serco through limited tender was not pursued on the basis that:

it would be bringing a new provider into offshore services and we would have no basis to do a limited tender to just Serco when Transfield has a proven capability in offshore garrison support services.

3.8 A number of firms had approached the department in mid-October 2013 with proposals regarding service provision. Transfield approached the Secretary by email (on 14 October 2013) stating that they had reviewed their operations on Nauru and could offer suggested changes to the contracting model to make it more effective and efficient in delivering stable and successful operations. It was proposed that these changes would result in an overall reduction in cost per transferee. Transfield also stated that it was taking a de facto leadership role on Nauru and could lead the ongoing operations on the Island using an integrated management approach:

The original concept was for the Salvation Army to act as the lead agency however evidence indicates that they are not comfortable with this role. Our assessment is that logistics (to ensure maximum capacity at all times) and intelligence (to ensure voluntary returns and more rapid processing) are the key factors for ongoing success on Nauru. We believe Transfield Services could lead the ongoing operations on the Island using an integrated management approach.

3.9 The then Secretary was also approached by G4S (on 14 October 2013) with a proposal to deliver services in Nauru and on Manus Island. There is no available record of the department having considered that proposal or having responded to G4S.

3.10 The department met with Transfield in mid-November 2013 with a view to having a close-to-agreed proposal ready for execution if approved later that month, and arrangements in place by February 2014. From this point preparations were made for a contract to be entered into with Transfield. The preparations included commercial advice from an external adviser (KPMG) on how a process could be run to determine the price and scope of the services Transfield would provide in Nauru and on Manus Island. Available DIBP email records also indicate that by 17 November 2013, the department had ‘the Minister’s clearance’ to the consolidation proposal. At this time the department considered seeking the Minister’s approval for a short contract extension for G4S and The Salvation Army through to the commencement of the new arrangement.

3.11 Other key meetings with service providers which occurred at the time, and related correspondence, included:

- 16 November 2013—The Salvation Army approached the department for advice on the expiry of its contract. The Salvation Army advised that it was experiencing difficulties in engaging and retaining staff as a result of not yet having a decision on whether its contract would be extended.

- 26 November 2013—the Minister met with Transfield, at the Minister’s request.

- 3 December 2013—Transfield presented the department with a preliminary concept of operations paper for service delivery in Nauru and on Manus Island identifying annual estimated savings of $14.76 million. In providing this paper to the department, Transfield noted:

- ‘Further to Transfield Services’ meeting with Minister Morrison last week and a subsequent discussion with Martin Bowles [the then Secretary] yesterday, please find attached Transfield Services’ Concept of Operations for the integration of Nauru and Manus Island into a single service delivery model.’

- 4 December 2013—G4S met with the Minister’s Chief of Staff advising that its contract was due to expire and expressing concern at not knowing if the contract would be extended. In email correspondence with the department, the Chief of Staff observed that G4S had assumed that its existing contract would be extended for an unspecified period and there had been no request for tender. The Chief of Staff also recorded that she had made no comment in this regard (due to probity concerns) except to say that contract management was a matter for the department.

- 12 December 2013—G4S and The Salvation Army were advised of the contract consolidation and a short term extension to their contracts pending their departure from service delivery in Nauru and on Manus Island. Save the Children was not advised of the consolidation proposal, rather the department wrote to them requesting a variation to the extension clause in the contract. The department’s letter also indicated that a longer term extension to 31 October 2015 may be possible, which would include various other amendments to the contract, if appropriate cost reductions could be achieved.

3.12 A timeline commencing with the decision to consolidate contracts on 4 November 2013 through to DIBP signing contracts with Transfield (on 24 March 2014) and Save the Children (on 29 August 2014) is set out in Figure 3.1.

Figure 3.1: Timeline of key events and decisions for contract consolidation

Note a: Save the Children was not advised of the consolidation.

Note b: Request for quote (RFQ).

Source: ANAO analysis of documentation from DIBP and service providers.

Recommendations by the National Commission of Audit

3.13 The National Commission of Audit was announced by the Treasurer, the Hon Joe Hockey MP, and the Minister for Finance, Senator the Hon Mathias Cormann, on 22 October 2013. The Commission was established by the Australian Government as an independent body to review and report on the performance, functions and roles of the Commonwealth government.

3.14 Commission Chair Mr Tony Shepherd AO had been Chairman of Transfield for a decade until his resignation on 23 October 2013. The ANAO sighted evidence which demonstrated that at the time of his resignation, Mr Shepherd divested himself of all interests in Transfield and shortly thereafter (14 and 15 November 2013) sold his shareholdings.

3.15 The then Secretary of the department (Mr Bowles) met with the National Commission of Audit including the Commission Chair and Secretariat on 28 November 2013, as part of the Commission’s consultative processes with Commonwealth entities. DIBP also made a submission to the Commission and there was a subsequent request from the Commission for additional information. There were no DIBP or Commission of Audit records that indicated the department’s contracts with Transfield were discussed. Mr Bowles and Mr Shepherd advised the ANAO that the department’s contract with Transfield was not discussed.

3.16 In its February 2014 report the National Commission of Audit observed that the detention and processing of illegal maritime arrivals:

has been the fastest growing Government programme over recent years.

3.17 The Commission recommended that:

- (a) by renegotiating contracts and better targeting of services, the per person cost of operating the Onshore immigration network be reduced to 2011–12 levels and similar efficiencies be sought for the offshore network; and

- (b) this process also be supported by an audit of the scope and cost of services currently being provided and how these have changed over time.

3.18 In reflecting on the Commission’s work, Mr Shepherd advised the ANAO that:

The NCOA was charged with reviewing some $408 billion in Commonwealth expenditure over three months and concentrated on the main offenders. However, as the ANAO draft [performance audit] report says we were concerned about the growing cost of onshore and offshore processing and recommended steps to contain and reduce these costs. Like many of the Recommendations in the NCOA Report I am not aware of whether there was any follow through by the Commonwealth.

Procurement advice

3.19 DIBP officials responsible for the consolidation process sought procurement advice from the department’s Central Procurement Unit (CPU) on the possibility of extending the contracts and/or conducting a limited tender process. The CPU considered that under the CPRs:

a variation to extend a contract beyond the terms of the original contract where the contract has no further options to extend, and where the services are within scope/the same, is possible, so long as a new checklist for procurement is completed in accordance with the CPRs, amongst other things, to confirm that the Department has a continuing need for the Services, has considered and addressed the relevant risks and has ensured that the extension will continue to represent value for money. Subject to the new procurement checklist being adequately completed, it is open to the department to extend a contract to cover service provision during an approach to market.

3.20 That advice was not consistent with Finance guidance, which stated that a:

variation to extend a contract or deed of standing offer beyond the terms of the original contract (rather than exercising an extension option within the terms of a contract), is a new procurement that must be conducted in accordance with the CPRs. Variations to include new extension options generally increase the scope of the contract or panel arrangement and are therefore not allowed.

3.21 The CPU also proposed as one option, that the procurement could be conducted overseas so the CPRs would not apply. The CPU advised that:

it was open to the department to undertake a limited approach to the market, so long as the procurement process occurred outside of Australia. To facilitate this, the CPU suggested that the department ask staff on Manus or Nauru to undertake this work, or engage Transfield or another process manager to do this, noting that it was unlikely that Transfield would be permitted to tender for the same services that it is managing.

3.22 The advice did not address the risks to achieving value for money in the absence of competition.

3.23 On 28 November 2013, the CPU sought Finance advice on conducting a limited tender relying on paragraph 10.3(b) of the CPRs—relating to urgent and unforeseen circumstances. The department advised Finance that:

DIBP has contracts operating in the offshore space, these contracts involve issues with the contract providers and the level of services we are receiving, there is areas of underperformance amongst other issues. We have had a scrutiny and recommendation report recommending that we not take up the extension option available to us due to the underperformance by the service providers and the risk to us knowing this and not ending the contracted services.

Due to Government commitments and the political and sensitive nature of services offshore and at detention facilities we cannot simply end the services whilst we approach the market through an open approach. We therefore seek to engage another service provider who is already providing similar services at another Immigration site and has been previously assessed as representing value for money.

We wish to complete this under CPR exemption 10.3(b) as an interim arrangement until 2015, by which time we expect to have an ATM [approach to market] for existing services and any new or changed services, depending on the nature of Government decisions and policies.

Based on our conversation/s today, I believe that DoF [Finance] is in agreement that this exemption could be used appropriately as a bridging mechanism whilst further market approaches are undertaken.

3.24 The ANAO was advised by DIBP that the ‘report’ referred to by the CPU was a November 2013 decision brief for the Commander of the Joint Agency Taskforce, prepared by the Joint Advisory Taskforce following a security risk assessment of the Manus offshore processing centre. The department provided a summary of the risk assessment to a Parliamentary Committee in June 2014. The summary included the risk assessments recommendations which related to improvements to infrastructure at the Manus offshore processing centre including fencing, lighting, installation of close circuit television, relocation of the logistics hub and establishment of a potable water supply.

3.25 The ANAO reviewed the full decision brief and found that the briefing did not recommend that DIBP not take up the extension option available with G4S and the Salvation Army due to underperformance, as had been stated by the CPU in its advice to Finance. Mr Bowles advised the ANAO that:

Whilst the report did not specifically highlight ‘performance issues’ relating to the contract, it did highlight areas for improvement and potential areas of change to the nature of the services provided.

3.26 There was no available record that the department provided any advice or feedback on the recommendations of the assessment to service providers. G4S advised the ANAO that they were not provided with any advice or feedback in relation to the Joint Agency Taskforce assessment. Both G4S and The Salvation Army were advised that the decision with respect to consolidating service providers was not based on their performance.

3.27 The department also advised Finance that the supplier it wished to engage (Transfield) had previously been assessed as representing value for money. As noted in chapter 2 of this audit report, the ANAO’s review indicated that in procuring services from Transfield in 2012, the department did not conduct a robust value for money assessment.

3.28 In response to the information provided by the department’s CPU, Finance advised DIBP on 28 November 2013 that:

limited tender could apply on the basis of poor performance of the existing provider, a new supplier is required immediately, and that the department’s decision is not made following a review to decide whether to exercise the extension option, with the intention of finding a new supplier.

3.29 The department used Finance’s advice to seek approval from the departmental delegate to conduct the procurement as a limited tender under paragraph 10.3(b) of the CPRs. The advice was also used in departmental advice for the Minister’s use in discussions with his colleagues on the consolidation proposal in December 2013. The advice indicated that it was DIBP’s view that Transfield was the best option for service delivery at the offshore processing centres and offered the lowest risk in regards to implementing a consolidated approach to service delivery. The advice outlined the proposed strategy for consolidation, including that:

- the preferred procurement method to achieve innovation and savings would be to approach Transfield directly with a limited tender;

- any public comment should reflect the Government’s desire to achieve innovations and savings through the consolidation processes and there was no need to discuss performance issues; and

- in relation to handling and timeframes, following the Government’s decision, a request for quote would be sent to Transfield for the provision of garrison and welfare services at both offshore processing centres.

3.30 The department’s use of limited tender under paragraph 10.3(b) of the CPRs would have been more defensible if: any G4S performance shortcomings had been documented; G4S had been advised of the department’s concerns; and had G4S not taken steps to remedy any documented performance issues after receiving such advice. The ANAO’s review indicates that the department did not advise G4S of performance issues during the life of the contract, and payments were never abated. There is no evidence of a loss of confidence in G4S’s ability to deliver services. In his December 2013 comments on communications prepared for G4S and The Salvation Army, a DIBP Deputy Secretary noted gaps in the advice:

…In communicating and dealing with G4S and TSA [The Salvation Army], we do not have [a] line on “why is Transfield continuing, and not us”. This is another way for the issue of performance to be raised. What do we say about that.

3.31 In reply, the Assistant Secretary responsible for Offshore Detention Services advised that:

…have worked up the lines below. Re the elephant in the room performance issue, not sure what else we can say short of the ‘their performance has been better than yours’ discussion which we don’t want to get into.

3.32 In its correspondence to the department over the decision to end the contract, G4S stated that there had been no indication that such a decision was imminent or was being contemplated:

It was confirmed in our meetings that the decision had nothing at all to do with the operational performance of G4S on Manus and there were no concerns in this respect. Based on this we are at a loss to understand how this decision can have been arrived at without G4S at least being given an opportunity to provide a submission outlining our own capabilities and potential cost efficiencies. Our strong preference is that the Department would reconsider its decision and give us an opportunity to explain how we are best placed to address any desire to achieve cost and operational efficiencies.

3.33 G4S’s confidence in relation to its performance was separately demonstrated by its earlier submission to the then Secretary of a proposal (14 October 2013) to deliver services in Nauru and on Manus Island (paragraph 3.9 refers).

Did the process applied to contract consolidation support the achievement of planned savings, innovations and efficiency in service delivery?

DIBP’s approach to engaging Transfield through limited tender procurement removed competition from the outset. The services to be provided and related costs were not agreed with Transfield prior to G4S and The Salvation Army being advised that they would exit from service delivery on Manus Island. The proposed costs submitted by Transfield were higher than the department had anticipated and exceeded those charged by G4S and The Salvation Army for service provision on Manus Island.

Ministers expected the consolidation of contracts to achieve innovation and savings. Savings were not realised and the basis which the department relied upon to demonstrate savings was unreliable. In particular:

- The department applied a benchmark model to demonstrate the achievement of value for money. Overall the benchmark was adjusted above historical costs to account for changes to the department’s service requirements and contractual approach, upwards to $372 million, to accommodate a number of service enhancements. The Government had directed the department to reduce per-head costs. The department had no authority to increase the funding value of the contract above historic costs.

- Separate benchmarks were developed for Nauru and Manus Island, but the department determined ‘value for money’ and claimed savings (against the benchmarks) on a combined basis. This allowed the department to demonstrate ‘savings’ by offsetting higher costs for Manus Island against lower costs for Nauru. While Transfield’s bid for Nauru was lower than historical costs, the bid for Manus Island exceeded historical costs by between $200 million and $300 million.

While the department based the negotiated contract price on a high capacity scenario, there was a steady drop off in new asylum seeker arrivals from a high of 1 647 in August 2013 to zero in March 2014. On this basis it was increasingly unlikely that the high capacity levels would eventuate. The resulting contract was volume driven, with significant economies of scale expected at high capacity levels. This contract exposed the Commonwealth to the risk of locking-in a high price for services delivered at lower capacity levels.

There is no available record of specific conflict of interest declarations having been made by departmental officers who were responsible for the procurement. There is also no available documentation to indicate whether the department performed due diligence checks on the successful tenderer (Transfield) or its subcontractors as part of the contract consolidation.

The Prime Minister had requested that per head costs be lower as a result of retendering the contracts, but the department did not calculate a per person cost. Finance advised the ANAO that under the consolidated contract, the per person per annum cost of holding a person in the offshore processing centres in Nauru and on Manus Island, was estimated at $573 111, at the time of the Mid-Year Economic and Fiscal Outlook 2015-16. Prior to consolidation Finance estimated the cost at $201 000.

3.34 The Minister sought Government approval for the consolidated contract arrangement in December 2013. In his submission to colleagues, the Minister proposed to explore options to consolidate existing services to enhance consistency, security and efficiency and incorporate innovation and savings into the extension provisions, noting that this was an interim measure pending an open tender process that would be conducted in 2014. In its comments and briefing on the submission, Finance highlighted that the cost of providing services under the consolidated contract was expected to rise by $93 000 per asylum seeker, taking costs from $201 000 to $294 000 per asylum seeker per annum. Finance also noted that the increase in unit costs appeared to be attributable in part to the department entering contracts with higher service provider costs than those factored into the forward estimates. For example, the Transfield monthly costs per asylum seeker had increased from $13 206 to $21 742 and the Salvation Army monthly cost per asylum seeker increased from $1 556 to $2 490.

3.35 The Government sought a reduction in costs with savings to be delivered through the contract consolidation. On 3 December 2013 the Minister sought and gained the Prime Minister’s agreement to proceed with the consolidation at an indicative cost of $2.6 billion. In responding the Prime Minister made it clear that he expected per head costs to be lower as a result of retendering the contracts. The Prime Minister’s agreement to proceed with consolidation did not provide DIBP with authority to increase the value of the contract to accommodate service enhancements or adjustments.

3.36 The department’s documentation on the Request for Quote (RFQ) process and subsequent negotiations with Transfield indicates that DIBP officials found it difficult to achieve the savings required by Ministers.

Contract negotiations and value for money

3.37 The department entered into contract negotiations with Transfield and Save the Children in early 2014. The approach taken in these negotiations is outlined below.

Transfield

3.38 On 3 December 2013 in response to the department’s briefing on its proposed approach to the consolidation of services at the Offshore Processing Centres, the Minister noted that this outcome [consolidation]:

…must be managed. Also pls advise on the employment of an external contract negotiation advisor to ensure there is rigorous negotiation to deliver savings from Transfield.

3.39 KPMG was engaged for this role. In advising the department, KPMG proposed benchmarking Transfield’s tendered price against existing contractor payments (the combined cost of G4S and Salvation Army service delivery on Manus Island). KPMG noted that in the context of sole source procurement it was important that the tenderer was aware that the Commonwealth would test value for money against a price benchmark.

3.40 KPMG’s evaluation report on pricing (3 February 2014) raises a number of issues in relation to Transfield’s costs against the benchmark for the number of detainees serviced.

3.41 Transfield’s initial submission introduced four pricing Capacity Bands for each location. During negotiations the number of pricing bands was increased to 14. The change in banding structure is outlined in Table 3.1 below.

Table 3.1: Initial and final capacity bands in Transfield’s submissions

|

0–600

|

0–800

|

1

|

1–2

|

|

601–1200

|

801–1600

|

2

|

3–6

|

|

1201–1800

|

1601–2400

|

3

|

7–10

|

|

1801–2400

|

2401–3200

|

4

|

11–4

|

Source: KPMG pricing evaluation report.

3.42 Transfield’s prices represented a price reduction in Nauru. For services on Manus Island the prices represented a significant price increase (KPMG referred to this increase as a premium) when compared to the price benchmark. Overall, KPMG concluded that:

when compared to the benchmark costs, the Respondent’s risk adjusted pricing yields inconsistent results. The Respondent’s pricing for Capacity Band 4 represents a 4.5% saving in comparison to benchmark costs, however the Respondent’s pricing represents a premium of approximately 50.8%, 12.8%, and 2.2% for Capacity Bands 1, 2 and 3 respectively.

3.43 Figure 3.2 shows the risk adjusted total bid costs for Transfield’s initial price against the benchmark for each of the four Capacity Bands for Nauru and Manus Island.

Figure 3.2: KPMG’s risk adjusted total bid cost in $ millions vs benchmark—by band and facility

Source: KPMG pricing evaluation report.

3.44 The risk adjusted pricing for the centre in Nauru represented savings of 17 per cent, 25 per cent and 28 per cent for Capacity Bands 2, 3 and 4 respectively, compared to the benchmark costs at Nauru. Capacity Band 1 for Nauru represented a 5 per cent pricing premium above the benchmark costs. Pricing at Manus Island represented a significant pricing premium when compared to benchmark costs (as extrapolated from incumbent pricing) of 38 to 128 per cent. Table 3.2 shows the difference between risk adjusted prices and the benchmark on a percentage basis.

Table 3.2: Difference between Transfield’s risk adjusted price and the benchmark

|

|

Manus Island

|

Nauru

|

Manus Island

|

Nauru

|

Manus Island

|

Nauru

|

Manus Island

|

Nauru

|

|

Percentage difference above or below the benchmark

|

123.2%

Above

|

4.9%

Above

|

64.3%

Above

|

(17.0%)

Below

|

48.4%

Above

|

(25.1%)

Below

|

38.1%

Above

|

(28.0%)

Below

|

Source: KPMG pricing evaluation report 2014.

3.45 After considering the KPMG report, the department’s evaluation committee recommended that: the department enter into negotiations with Transfield; and that a contract be executed only if the department could be satisfied that value for money could be obtained. Key matters for negotiation included the performance framework and performance measures, savings measures and clarification that key service delivery elements were adequately covered in the statement of work.

3.46 Transfield provided DIBP with responses to clarification questions and revised pricing information on the issues to be negotiated on 11 February 2014. In a minute to the delegate (the First Assistant Secretary Offshore Detention and Returns Task Group) dated 21 February 2014, the Assistant Secretary for Offshore Detention Services advised that the final negotiated position represented value for money and also resulted in a number of changes considered to be significant improvements. The delegate was also advised that:

The negotiation process has resulted in a number of significant improvements between the initial bid, and the final negotiated position… Further understanding and clarification of the cost differences between Transfield’s Nauru and Manus costs during negotiations allowed the department to have confidence that the additional investment in Manus was justified and required…

3.47 The department also considered that the negotiated performance management framework would contribute to innovation and provide an incentive for cost savings, as Transfield was eligible to share in 50 per cent of demonstrated savings to fixed costs and 15 per cent of savings to pass through costs.

3.48 In respect to value for money the delegate was advised that the negotiated position represented a movement of $150 million in the Commonwealth’s favour. The delegate approved the proposal on the basis that it represented value for money and signed a letter of intent to Transfield (21 February 2014) to cover service delivery until a contract could be drafted.

3.49 The advice to the delegate indicated that the $150 million movement in the bid price demonstrated a ‘saving’ against the benchmark, whereas the KPMG report reflected that these were price adjustments agreed to during the negotiation:

The Transfield bid now represents a risk adjusted saving of 5.9% over the benchmark for band 3. This is made up of a saving of 26% on the benchmarked Nauru costs and an increase of 29% on the benchmarked Manus costs (down from 48%), noting the value of the Nauru benchmark is $1.25bn and Manus $0.797bn. The benchmark has been calculated based on contract payments for the 12 months to November 2013, uplifted for increased numbers of Transferees, inflation and other assumptions and reflects a conservative estimate of current costs that may not accurately reflect current operational tempo.

3.50 The advice to the delegate also noted that the benchmark for Manus Island did not take into account a number of enhancements offered by Transfield relating to enhanced security, improved catering, reduction in international travel costs and agreement to a performance management framework. Collectively these enhancements were considered to be worth $60 million, and it proposed that the benchmark be adjusted accordingly. Table 3.3 shows the advice to the delegate included adjustments and negotiated outcomes. This advice was based on Transfield’s Capacity Band 3 (refer paragraph 3.41 and Table 3.1).

Table 3.3: Adjustments to the benchmark and other negotiated outcomes ($ millions)

|

Initial difference between risk adjusted price and benchmark

|

32.4 (1.6% over)

|

|

Negotiations–efficiency dividend/security/accommodation security

|

Savinga 61.3

|

|

Removal of working hours risk

|

Saving 31.9

|

|

Increases to the benchmark for enhanced service

|

Saving 60.0

|

|

Final difference between risk adjusted price and benchmark

|

120.8 (5.9% under)

|

Note a: This is a notional saving against the benchmark as opposed to an actual savings against historic costs.

Source: Minute to Offshore Detention and Returns Task Group 21 February 2014.

3.51 In addition to the minute of advice, the delegate received the final report on the negotiations prepared by KPMG, presenting analysis of the proposal and a comparison against the benchmark constructed by KPMG. This report stated that the benchmark price was increased above the historical cost base in order to ensure a like for like comparison of pricing. The report noted that the benchmark was compared against the bid price for each facility, and ‘savings’ were presented as an aggregate (combined Nauru and Manus Island).

3.52 The ANAO compared the benchmark and bid with a projection of the historic cost for each capacity band and found that the benchmark was pitched at above the historical costs at all capacity band levels. Overall the benchmark was adjusted above historical costs by some $372 million. For Nauru the difference between the benchmark and historical costs was valued at its highest point at $166 million, while for Manus Island it was $206 million. The Government had directed the department to reduce per-head costs. The department had no authority to increase the value of the contract above historic costs to cover service enhancements, and was aware of this. In seeking internal financial approval for the proposed contract the delegate was advised of the potential need for further policy approvals:

Whilst this is within our garrison and welfare service delivery funding allocation in the demand driven model, it is likely that further policy approval will be required to update the demand driven model for the new contract.

3.53 The ANAO also compared the bid for Nauru and Manus Island separately and against the benchmark and historic costs. The bid price for services in Nauru was lower than the benchmark and historic costs for most capacity levels. For Manus Island the bid was above both the benchmark and historic costs for all capacity levels. Figure 3.3 and 3.4 summarise the ANAO’s analysis.

Figure 3.3: Nauru bid, benchmark and historic costs

Source: ANAO analysis of the spreadsheet used to prepare the KPMG Price Evaluation Report.

Figure 3.4: Manus Island bid, benchmark and historic costs

Source: ANAO analysis of the spreadsheet used to prepare the KPMG Price Evaluation Report.

3.54 The ANAO’s analysis indicates that the combined value of Transfield’s Nauru and Manus Island bids was over the historical costs at capacity band one through to nine and was only below the historic costs above capacity band ten. The consolidated (KMPG) benchmark (Nauru and Manus Island combined) was above the historic costs by $372 million at its highest point (the red line in Figure 3.5 shows that the highest point was $2 646 million for capacity band 13, while the historic cost was $2 274 million).

Figure 3.5: Combined bid values, benchmarks and historic costs—Nauru and Manus Island

Source: ANAO analysis of the spreadsheet used to prepare the KPMG Price Evaluation report.

3.55 In its final pricing evaluation report, KPMG assessed that post-negotiation Transfield’s bid represented both actual value for money and improved value for money relative to the opening position. In particular, KPMG advised that the increase in the number of pricing bands, from four to 14, had provided an improved value for money outcome due to the more efficient incremental pricing structure, with greater potential price benefits over the benchmark potentially achieved at the higher capacity band levels.

3.56 The available records do not indicate whether in assessing value for money, the department considered the relationship between price and the actual capacity levels of the centres. Advice to the delegate stated that:

Capacity band 3 activity has been used as a baseline based on predicted occupancy levels going forward. Band 4 results are significantly better than band 3 and bands 3 and 4 have been considered to be appropriate levels of activity for the analysis of value for money.

3.57 As outlined in Table 3.1 capacity bands three and four equated to capacity bands 7–10 and 11–14, which ranged from 1201–1800 and 1801–2400 detainees respectively for Manus Island and 1601–2400 and 2401–3200 detainees respectively for Nauru.

3.58 Since opening in 2012, there had been large variations in the number of asylum seekers housed in the centres. Figure 3.6 shows the total number of asylum seekers in Nauru and on Manus Island and Finance forecast numbers commencing from late 2013.

Figure 3.6: Total number of asylum seekers in offshore processing centres by month—actuals and Finance forecast numbers commencing late 2013

Source: Finance briefing and DIBP published monthly statistics.

Note: Actual Total Detainees in Regional Processing Centres represents individuals who were held in the offshore processing centres at a point in time. The variation in actual total asylum seekers over time represents the movement in asylum seekers arriving and leaving the centres. The increase from August 2013 represents individuals who arrived in Australian waters by boat after the July 2013 announcement and who were required to be transferred to an offshore processing centre and could never be settled in Australia. The Forecast Increase in Total Detainees anticipated that the number held across the two centres would be maintained by a flow of around 390 new arrivals a month through to June 2015, beyond which inflow would drop to 50 a month.

3.59 The centres in Nauru and on Manus Island had never reached their full combined capacity of 5600 persons, and there were few new arrivals after December 2013. While the department based costings on a high capacity scenario, there was a steady drop off in new boat arrivals during the contract negotiation period. On this basis it became increasingly unlikely that the high capacity levels would be achieved. The department did not consider the price impact of a volume driven contract with significant built-in economies of scale. Advice to the departmental delegate did not consider whether constructing a price based on these capacity levels, to achieve economies of scale, might lock the Commonwealth into paying a premium for services delivered at lower capacity levels.

3.60 In April 2014 the Minister for Finance was advised by his department that since December 2013 there had been 373 arrivals in total compared to the MYEFO projection of 541 per month. In addition, reports suggested that the policy of turning back boats, in combination with offshore resettlement arrangements, had generated the fall in the arrival rate. A breakdown of arrival numbers as at 11 April 2014 is provided at Table 3.4.

Table 3.4: Asylum seeker arrival numbers since August 2013 (as at 11 April 2014)

|

Asylum seeker arrivals (less crew)

|

1 647

|

853

|

347

|

221

|

369

|

3

|

1

|

0

|

0

|

Source: ANAO presentation of advice to the Finance Minister, April 2014.

Note: The period of the contract negotiations was January to late March 2014.

3.61 The ANAO’s analysis of the final Transfield bid against the benchmark and actual capacity levels indicates that the higher capacity levels have never been required. Figure 3.7 shows the final tender bid and capacity bands, including the amount over and under the benchmark for each band in the Transfield bid for the centres in Nauru and on Manus Island. The columns show the actual capacity bands used during the contract. In summary, the premium paid (shown in green) outweighs the discount achieved (shown in purple).

3.62 The then Secretary, Mr Bowles, advised the ANAO that:

From the vantage point of 2015–16 the drop off in UMA arrival numbers in Feb 2014 looks clear and distinct. At the time however, there was never certainty that this drop-off of numbers would continue. The flow of UMAs had always had peaks and troughs, and was especially susceptible to the weather cycle and monsoon seasons. Most critically, at the times of the various procurement activities, the posture of the ATM [approach to market] was in the context of the potential for high arrival rates, rather than the lows.

Figure 3.7: Actual band usage shown against the value of the Transfield bid relative to the benchmark

Note: The benchmark is represented at zero dollars.

Source: ANAO presentation of DIBP data.

3.63 A contract for consolidated services was signed by DIBP on 24 March 2014. The Minister was advised (24 March 2014) that the department had negotiated a 5.9 per cent saving overall, valued at some $121 million, as compared to the benchmark constructed by KPMG. The Minister was also advised that:

Greater savings against benchmark costs have been achieved at higher occupancy levels…

The Transfield contract bid has been compared against the Department of Finance’s Offshore Demand Driven Model (DDM) funding allocations for Transfield, G4S and The Salvation Army. Comparing the cost under the contract to the funding allocations using the forecast occupancy levels in the DDM, the cost of the contract is approximately $44 million less over the 20 month contract period…

Given the operation of the DDM, the Financial Strategy and Services Division has agreed with the Department of Finance to hand back savings of $25 million across the contract period…

3.64 The Minister was not advised that the resulting contract with Transfield—with a reported (AusTender) value of $2.1 billion over 19 months—would require the Commonwealth to pay a significant premium over and above the historical costs of services. The Minister was not advised that under the contract actual capacity levels (at the time) represented significant additional expense. The Minister was not advised of the contract price on a per head basis. As discussed at paragraph 3.35, the Prime Minister had expressed an expectation that both total costs and per head costs would be reduced as a result of re-tendering the contracts.

3.65 Subsequent Mid-year Economic and Fiscal Outlook modelling by the Department of Finance of average per head costs, using DIBP’s detention network population forecasts, indicated that the per head cost under the consolidated contract was $573 111 (based on actual numbers of asylum seekers held) at the end of December 2015. This equated to a daily rate of over $1570 per asylum seeker.

3.66 Calculating per person costs would have enabled the department to more accurately advise its Minister of the cost implications of the consolidated contract. It would also have assisted the department to advise the Minister on the placement of asylum seekers to minimise expense to the Commonwealth. The ANAO estimated per person costs (as reflected in the bid), for each facility and capacity band. The ANAO’s analysis indicates that accommodating transferees on Nauru, until it reached full capacity prior to accommodating any transferees on Manus Island, would have lowered the overall expense. The reason for this is that the cost per person was lower in Nauru than on Manus Island. A cost comparison is set out below in Table 3.5.

Table 3.5: Per person costs, for 12 months, based on contract rates

|

1

|

$696 480

|

$463 100

|

|

2

|

$482 440

|

$327 610

|

|

3

|

$431 200

|

$300 390

|

|

4

|

$385 980

|

$272 190

|

|

5

|

$360 290

|

$255 490

|

|

6

|

$330 440

|

$241 510

|

|

7

|

$322 920

|

$234 340

|

|

8

|

$308 670

|

$244 010

|

|

9

|

$318 490

|

$217 320

|

|

10

|

$299 990

|

$211 330

|

|

11

|

$300 110

|

$205 400

|

|

12

|

$292 140

|

$199 100

|

|

13

|

$284 010

|

$195 390

|

|

14

|

$273 230

|

$191 520

|

Source: ANAO analysis.

Save the Children

3.67 The department’s documentation on negotiations with Save the Children for the provision of welfare services to families, children and single women in Nauru, is limited. The available documents indicate that negotiations were protracted and the department sought significant price reductions after determining that the proposal did not represent value for money. In the course of negotiations with Save the Children, the department proposed to the Minister that DIBP seek an alternative quote from Transfield for this work. The Minister expressed a preference to retain the services of Save the Children.

3.68 DIBP records indicate that the department subsequently sought an informal quote from Transfield to conduct this work. Transfield’s quote was found to be 28 per cent higher than Save the Children’s final costs.

3.69 In response to departmental requests, Save the Children submitted four pricing revisions. In May 2014, Save the Children wrote to DIBP declining an invitation to submit a further contract change proposal in the terms the department had requested. Save the Children advised that the reductions proposed by the department (which were in the order of 20 to 50 per cent) would change the service offering fundamentally and expose the department, Save the Children, asylum seekers and employees to an unacceptable level of risk:

As an organisation whose mission is to protect and promote the rights and safety of children and their families, and for the reasons outlined above, SCA [Save the Children] cannot in good conscience submit a revised contract change proposal as requested. SCA remains committed to working with the Department to ensure the best possible conditions and services for asylum seeker children and families in Nauru. We would welcome the opportunity to further discuss our contract change proposal and identify additional cost reductions which do not compromise our ability to safeguard the physical, mental and emotional wellbeing of the people in our care.

3.70 The department’s records differ from Save the Children’s in relation to initial price and negotiated savings. The department’s approval record shows a price reduction of $112.4 million —down from an initial bid of $196.4 million. Save the Children’s documentation shows that the initial bid for services was around $300 million and the negotiated reduction was around $150 million. The value of the contract as reported on AusTender was $100 million.

Probity and conflict of interest

3.71 The department engaged an internal probity adviser to oversee the Request for Quote (RFQ) process between late December 2013 and the end of January 2014. The adviser provided an unqualified sign off for the process.

3.72 KPMG declared its role as Transfield’s external auditor and declared that it had also provided other services including tax, financial due diligence and accounting advisory services to the Transfield Group. KPMG did not consider that the provision of such services to Transfield raised any conflict of interest issues and advised the department that no team member who was providing services to DIBP in relation to this project would be involved in the Transfield audit or advisory engagements. KPMG also provided conflict of interest declarations for specific staff in January 2014. In engaging KPMG the department noted in its approvals that no conflicts of interest existed.

3.73 The ANAO’s review indicates that there is no available record of specific conflict of interest declarations having being made by departmental officers who were responsible for the procurement. Mr Martin Bowles provided his personal declaration of interest for 2013 to the ANAO on request.

3.74 Good procurement practice involves entities undertaking due diligence of potential tenderers. The department’s Risk Management Plan (for the Offshore Processing Programme) stated that a control in place during the procurement process was that all service providers had undergone due diligence investigations.

3.75 No evidence was found of the department having conducted due diligence checks in relation to the engagement of Transfield or Save the Children. The ANAO found that had due diligence checks been undertaken at the time of consolidation (January 2014), the department would have identified that Transfield’s subcontractor (Wilson Parking Australia, trading as Wilson Security) had a Director who had been charged with bribery in Hong Kong in 2012 and that these charges were pending. The person was acquitted of all charges in December 2014. Had DIBP performed due diligence checks it may not have changed the outcome of the procurement, however DIBP would have made an informed decision and would be better positioned to mitigate any associated risk.

")