Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 45 of 2025–26

Australian Taxation Office Management of Small Business Collectable Debt

Published

Tuesday 30 June 2026

Portfolio

Australian Taxation Office

Entity

Australian Taxation Office

Contact

Please direct enquiries through our contact page.

Activity

Regulation

Sector

Taxation

Audit snapshot

Why did we do this audit?

- Collecting the right amount of tax, including tax debts, enables the delivery of services to the Australian community.

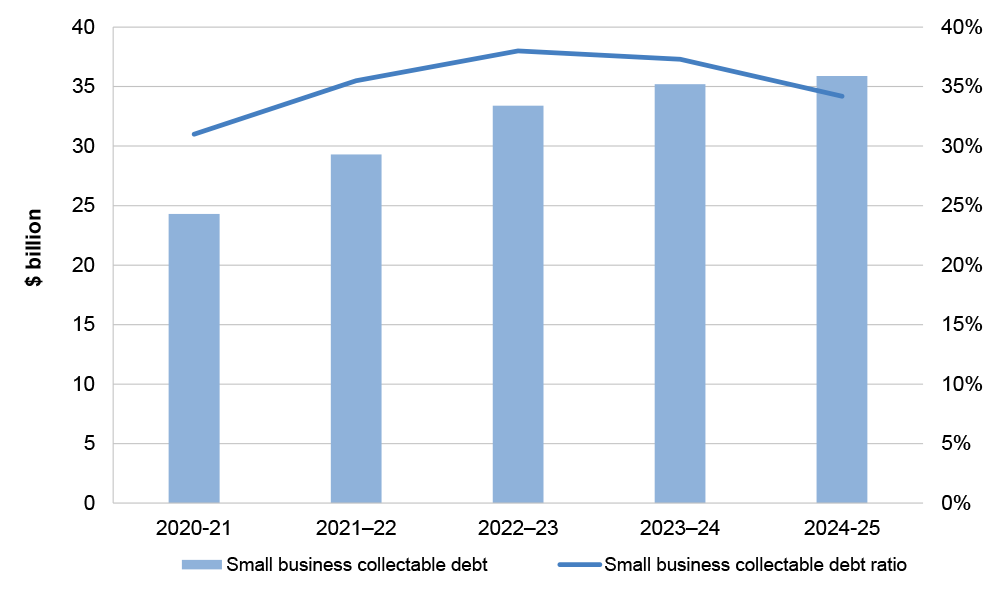

- Small business collectable tax debt was $35.9 billion of $54.2 billion total collectable debt in 2024–25. By comparison, age pension expenditure was $62.2 billion in 2024–25.

- The audit provides assurance to the Parliament that the ATO effectively manages small business collectable debt.

Key facts

- The ATO’s 2024–25 financial statements show there is a risk it will not collect $49.8 billion of the $98.4 billion total tax owing.

- Small business is the largest driver of overall tax debt, with 1,338,387 small businesses with an average of $26,797 in collectable debt in 2024–25.

- Small business collectable tax debt increased by $19.4 billion between 2018–19 to 2024–25. The ATO reduced debt collection measures to assist taxpayers in response to natural disasters, the COVID-19 pandemic and economic shocks.

What did we find?

- The ATO’s management of collectable small business debt risks is partly effective.

- The ATO’s self-assessment is that the risk of unacceptable levels of small business debt is out of tolerance.

- Internal targets to reduce debt volumes for small business are absent. The whole of collectable debt performance measure does not identify small business debt performance.

- Rising debt volumes create risks, including that some taxpayers obtain an unfair financial advantage over others.

- Pay As You Go Withholding and GST debt are the largest proportion of the overall collectable debt book.

What did we recommend?

- There were eight recommendations relating to performance measures, benchmarks, communication, and better use of data.

- The ATO agreed to all eight recommendations.

66.1%

The percentage of the ATO’s total collectable debt in 2024–25 belonging to small business.

34.2%

The small business collectable debt ratio in 2024–25, compared to the overall collectable debt ratio of 8.1%.

0.5%

The percentage of small business debt collection interactions in 2024–25 that were ‘firmer and stronger’ actions, down from 1.2% in 2018–19.

Summary and recommendations

Background

1. The Australian Taxation Office (ATO) is the principal revenue collection agency of the Australian Government. Its roles and responsibilities include administering legislation governing tax, superannuation and the Australian Business Register. The ATO’s corporate plan 2025–261 identifies ‘strengthening payment performance and debt collection’ as an enterprise priority.

Rationale for undertaking the audit

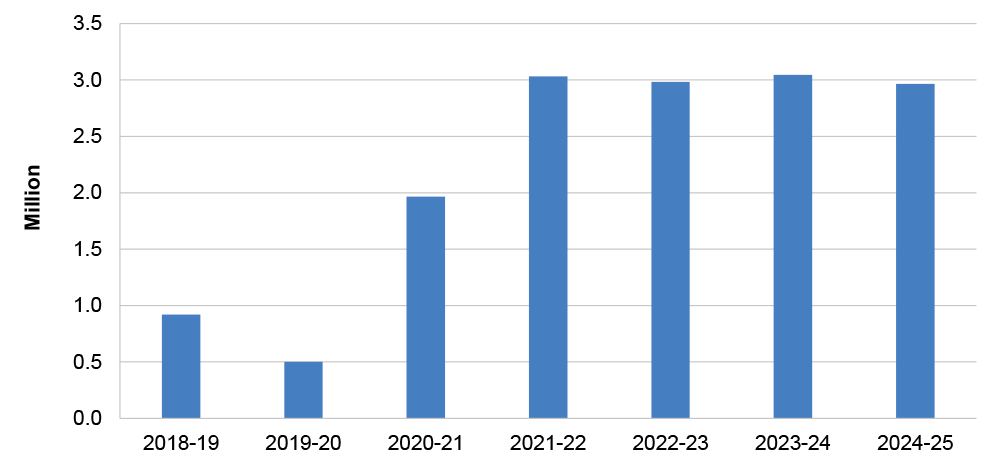

2. The ATO is responsible for managing the compliance of taxpayers in the Australian taxation and superannuation system, including pursuing tax debt. Debt that is undisputed, that is not subject to an objection, appeal, insolvency or not on hold, is considered collectable debt. Collectable tax debt from small business was $35.9 billion in 2024–25, an increase of $19.4 billion from 2018–19 and approximately two-thirds of the $54.2 billion total 2024–25 collectable tax debt.2

3. The ATO corporate plan 2025–26 identifies strengthening payment performance and debt collection as an enterprise priority.3 The key focus area of improving small business tax performance was removed from the corporate plan in 2024–25.4 After reducing collection activities during the COVID–19 pandemic, in 2023–24, the ATO recommenced the application of a range of firmer actions, including garnishee actions, directions to pay, director penalty notices and disclosure of business tax debt actions. Subsequent to the audit, in April 2026 the ATO introduced temporary assistance for businesses to assist in managing their tax obligations, which may include pauses to some compliance and debt collection actions in affected industries, in response to the increased economic impact of fuel costs arising from the conflict in the Middle East.

4. This audit provides assurance to the Parliament that the ATO effectively manages small business taxpayer debt.

Audit objective and criteria

5. The audit objective was to assess the effectiveness of the Australian Taxation Office’s management of small business collectable debt.

6. To form a conclusion against the objective, the following criteria were developed:

- Are the risks relating to small business collectable debt appropriately managed?

- Does the ATO have a sound strategic framework to manage small business collectable debt?

- Does the ATO effectively apply its strategic framework to manage small business collectable debt?

Conclusion

7. The ATO’s management of collectable small business debt is partly effective. Small business collectable tax debt increased by $19.4 billion, or 118 per cent, between 2018–19 and 2024–25. The ATO recognises that the risk of this debt rising to unacceptable levels is out of tolerance. The ATO does not use specific performance targets to reduce small business debt. Public reporting on performance does not provide Parliament with sufficient visibility of the risks and the ATO’s management of them. A continued rise in debt volumes creates a number of risks, including that some taxpayers obtain an unfair financial advantage over others.

8. The ATO’s management of collectable small business debt risks is partly effective. The ATO’s pausing of debt collection measures in response to natural disasters, the COVID-19 pandemic and global economic shocks resulted in rapid growth of the debt book. The ATO has assessed that its risk of unacceptable levels of unpaid debt remains out of tolerance, and will not be brought back into tolerance in the immediate future. The ATO considers its controls to reduce this risk to be partly effective. The ATO has not set specific internal targets to reduce debt volumes. The ATO reports publicly in its annual performance statements on a whole-of-collectable debt performance measure that does not enable identification of small business debt performance.

9. The ATO has a largely sound strategic framework for debt collection. This is a whole-of-debt strategy that is not specific to small business. Small business collectable debt makes up 66.1 per cent of total collectable debt. The ATO recognised that measures adopted during the COVID-19 pandemic ‘normalised into poor payment behaviours’ among taxpayers and commenced a Lodge and Pay Reset to return to business-as-usual recovery actions. The ATO has assessed that a significant behavioural shift by small business taxpayers is required to bring the collectable small business debt risk into tolerance. The ATO is able to measure payment behaviour, response rates, debt outcomes and changes in lodgment and payment compliance. The ATO has not fully incorporated best practice principles in communicating with taxpayers about debt. Given the continued increase in volumes of small business collectable debt there would be benefit in the ATO evaluating the effectiveness of each form of interaction and based on this, developing an approach specifically supporting its engagement with small business taxpayers.

10. The ATO’s application of its strategic framework is partly effective. The ATO effectively identifies taxpayers with debt, issues automated communications about debts, and identifies taxpayers for firmer and stronger actions. Inaccurate unit costs are used to determine cost effectiveness, meaning the ATO is unable to distinguish between firmer and stronger debt recovery actions. Resource prioritisation by the ATO results in a small proportion of all taxpayer groups (not just small businesses) identified for firmer and stronger actions directed to staff to progress. This limits the ATO’s effectiveness. Effectiveness is further reduced by not measuring how efficiently taxpayer debt is being recovered.

Supporting findings

Managing risks related to small business collectable debt

11. The ATO has established processes to manage both enterprise and business level risks. Risk assessments and treatment plans relating to small business debt at the enterprise and business line level have been created in accordance with ATO requirements. The ATO has assessed its controls to manage small business debt as partly effective. Risks to small business debt are generally managed in accordance with ATO requirements. Complete documentation evidencing formal endorsement of the enterprise level risk between 2020–21 and 2024–25 was not maintained, and the 2023 risk review occurred seven months late. (See paragraphs 2.2 to 2.19)

12. The ATO had 13 committees or groups considering small business debt between 2019–20 and 2024–25. The ATO Risk Committee has increased its focus since 2021–22 on the management of the payment risk. It has sought assurance over the effectiveness of controls and has requested the development of key performance indicators. The Risk Committee was advised in June 2024 that small business debt will likely remain out of tolerance for a further one to two years. Given the significant proportion of total collectable debt that is owed by small business, the collection of small business collectable debt should remain a focus of oversight and reporting. The small business collectable debt ratio is a major contributor to the ATO’s overall collectable debt ratio but public reporting is minimal. Recommendations from the Tax Ombudsman concerning public reporting of debt have not been fully implemented. Improved public reporting of the ATO’s performance in reducing collectable debt would improve transparency and oversight of risks and the ATO’s management of them. (See paragraphs 2.20 to 2.55)

13. Within its risk management framework, the ATO has a stated objective of reducing small business collectable debt. It measures its performance through the ratio of collectable debt to net tax collections. This ratio does not provide transparency on small business collectable debt as the debt ratio may be able to be reduced while the total volume of small business collectable debt continues to rise. The ATO does not set specific measurable targets regarding the reduction in the volume of small business collectable debt. Doing so would assist the ATO in its efforts to reduce small business collectable debt. (See paragraphs 2.56 to 2.66)

The ATO’s strategic framework to manage small business collectable debt

14. The ATO has a whole-of-debt framework. The framework is informed by a management-initiated review, and the ATO’s Risk Management Framework. It is also based on several OECD sources including the OECD Tax Debt Management Maturity Model. The ANAO’s assessment of the ATO against this model found less mature arrangements on risk management and performance indicators, and more mature arrangements on IT strategy relative to the ATO’s self-assessment. (See paragraphs 3.2 to 3.12)

15. The ATO has a broad engagement strategy for all taxpayers with debt. It does not have a specific engagement approach for small business. Aged debt continues to grow, making it less likely to be collected. The ATO seeks to engage with taxpayers primarily through SMS and letters. Direct taxpayer responses to SMS and letters have decreased over time. Financial resilience is assessed, and where taxpayers have the capacity to pay, the ATO offers various payment methods and encourages the use of payment plans. Taxpayer vulnerability is considered by the ATO. The ATO considers feedback from taxpayers to improve engagement. The ATO has largely implemented best practice principles when communicating to small business taxpayers with debt. (See paragraphs 3.13 to 3.57)

16. The ATO applies a whole-of-debt collection strategy for all taxpayers. The current strategy, implemented in 2024, is the Payment Strategy, a key aspect of which is segmentation to enable priority taxpayers to be identified for firmer debt collection activities. Implementation of segmentation by the ATO was underway as at February 2026. (See paragraphs 3.58 to 3.94)

Application of the ATO’s strategic framework to manage small business collectable debt

17. The ATO monitors taxpayers with debt and selects which debts to action using its analytic or machine-learning models, risk-based triggers, and defined business rules. It does not prioritise small business taxpayers with debt over other taxpayers. The ATO has processes for assessing and reviewing analytic models, including business verification processes, data and ethics assessment processes, and internal audits and reviews. When models were retrained in 2025, verification tests showed there had been a decline in performance over time. The ATO’s retraining schedule for analytic models, proposed in 2020, was not met until late in 2024. The ATO paused its firmer and stronger debt collection activities during the COVID-19 pandemic, which deprived the machine-learning models of up-to-date data. As at September 2025, the ATO did not have a monitoring model in place and ceased monitoring model performance in June 2025. (See paragraphs 4.2 to 4.23)

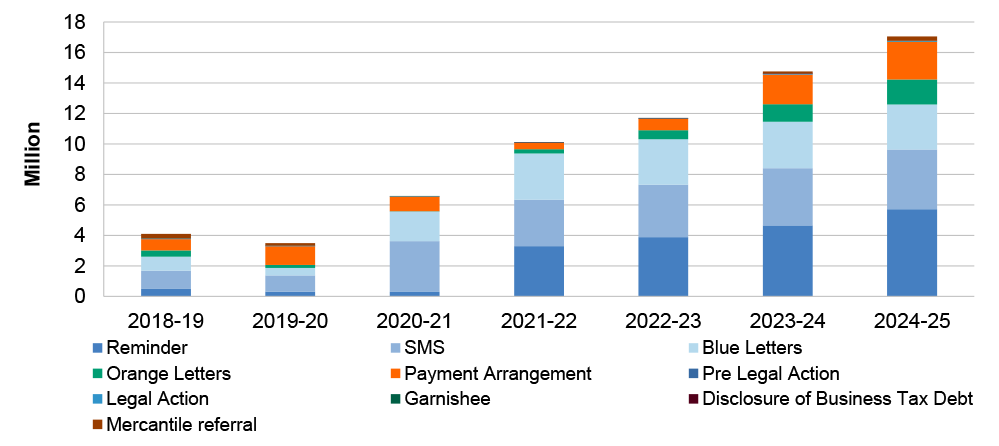

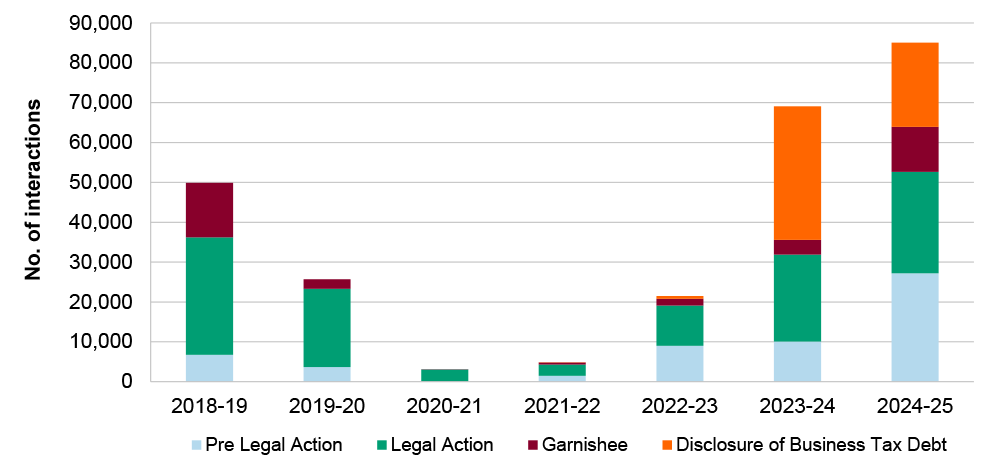

18. Overall, debt collection interactions with small business taxpayers increased from 4.1 million in 2018–19 to 17.0 million in 2024–25. Stronger actions comprise a small proportion of the total small business debt collection interactions. In 2024–25, garnishees, disclosures of business tax debts, pre-legal and legal actions combined comprised 0.5 per cent (or 85,078 interactions) of total small business debt collection interactions, down from 1.2 per cent in 2018–19. Firmer and stronger debt actions are resource intensive. The ATO has extensive internal data stores, data reports and visualisations which are not being fully utilised to analyse debt taxpayer interactions and measure payment behaviour, response rates, debt outcomes, and changes in lodgment and payment compliance. The ATO does not use its performance measures to routinely benchmark, monitor and report performance of its debt recovery interactions or changes over time. (See paragraphs 4.24 to 4.85)

Recommendations

Recommendation no. 1

Paragraph 2.36

The Australian Taxation Office, as part of its review of its enterprise governance framework, ensure clear accountabilities and reporting lines regarding small business taxpayer debt.

Australian Taxation Office response: Agreed

Recommendation no. 2

Paragraph 2.54

The Australian Taxation Office publicly report the current annual proportion of payments made on time, collectable debt ratio, disputed debt, debt non-pursued — uneconomical to pursue, and irrecoverable at law in a timely manner and on a recurring basis to increase transparency around the scale of small business taxpayer debt, and the effectiveness of the ATO’s strategies in reducing it.

Australian Taxation Office response: Agreed

Recommendation no. 3

Paragraph 2.66

The Australian Taxation Office:

- set a specific measurable target to reduce the volume of small business collectable debt; and

- assess the effectiveness of its actions to improve payment and debt outcomes.

Australian Taxation Office response: Agreed

Recommendation no. 4

Paragraph 3.26

The Australian Taxation Office review engagement with taxpayers with small business debt to determine the effectiveness of each form of interaction to assess taxpayer behaviour, and to inform its future small business debt approach.

Australian Taxation Office response: Agreed

Recommendation no. 5

Paragraph 4.23

The Australian Taxation Office establish a schedule for regular monitoring and retraining of the performance of Payment and Receivables Management analytic models and document monitoring outcomes and retraining changes.

Australian Taxation Office response: Agreed

Recommendation no. 6

Paragraph 4.56

Following implementation of relevant performance measures as outlined in Recommendation 3, the Australian Taxation Office establish business-level benchmarks for performance measures for its debt recovery interactions to enable regular monitoring over time.

Australian Taxation Office response: Agreed

Recommendation no. 7

Paragraph 4.60

The Australian Taxation Office develop a data reporting approach to enable understanding of whether debts are moving through the treatment pathway efficiently to reduce small business collectable debt. This may include measurement of the average time between interactions, or number of consecutive interactions a taxpayer may receive.

Australian Taxation Office response: Agreed

Recommendation no. 8

Paragraph 4.80

The Australian Taxation Office revise unit cost on a regular basis including the costs of using external collection agencies (mercantile referrals), to ensure accuracy when reporting on return on investment.

Australian Taxation Office response: Agreed

Summary of entity response

19. The proposed audit report was provided to the ATO. The ATO’s summary response is reproduced below, and its full response is at Appendix 1. Improvements observed by the ANAO during the course of this audit are listed in Appendix 2.

Australian Taxation Office

The Australian Taxation Office (ATO) welcomes the ANAO’s report and the finding that the ATO has a largely sound taxpayer debt management framework, and we agree to all recommendations.

Our core focus on collecting the right amount of tax owed to the Australian community has not changed, however our approach evolved in response to unprecedented impacts, such as COVID-19, which resulted in rapid growth in taxpayer debt. Further, the fuel response announced in April 2026 to support ABN holders experiencing difficulties arising from increased fuel costs demonstrates adaptation and responsible stewardship in a changing environment.

We continue to seek to collect all debt owed, balancing firm and timely action with community expectations. While small business debt is the largest contributor to collectable debt, we manage debt across all taxpayer groups, including individuals, private wealth and large businesses. We’re funded specifically under the Tax Avoidance Taskforce and the Tax Integrity Program to ensure large businesses pay their fair share of tax. In 2024–25 we collected $459.7 billion tax from them (72% of total collections) compared to $96.8 billion from small business.

We also assist in preventing debt by supporting small businesses through education, engagement and targeted initiatives, including the Getting It Right campaign. Preventing and reducing debt is critical to maintaining community confidence, supporting voluntary compliance and ensuring funding for essential government services.

Key messages from this audit for all Australian Government entities

20. Below is a summary of key messages, including instances of good practice, which have been identified in this audit and may be relevant for the operations of other Australian Government entities.

Group title

Governance and risk management

Key learning reference

Group title

Policy/program implementation

Key learning reference

Group title

Performance and impact measurement

Key learning reference

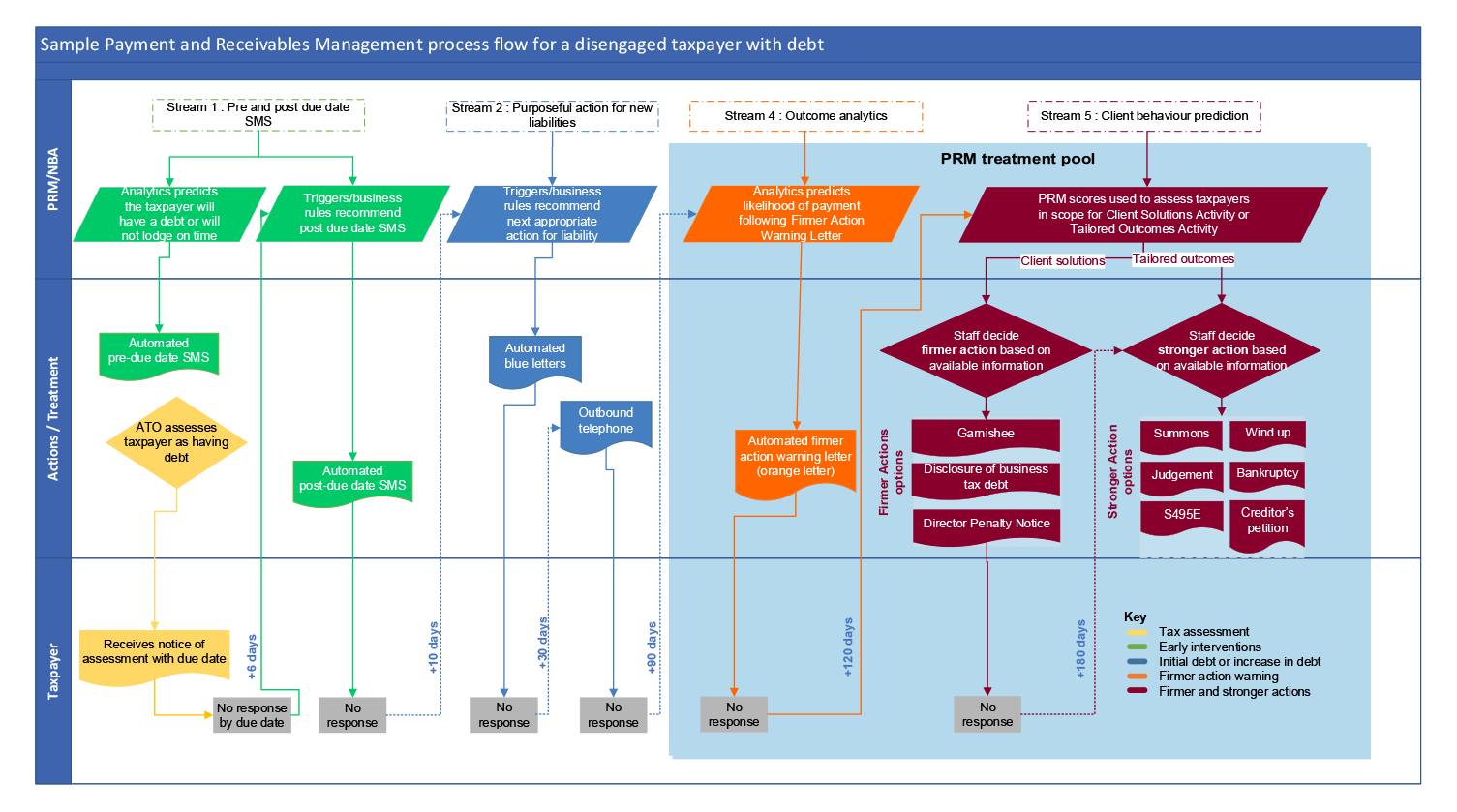

1. Background

Introduction

1.1 The Australian Taxation Office (ATO) is the principal revenue collection agency of the Australian Government. Its roles and responsibilities include administering legislation governing tax, superannuation and the Australian Business Register. As at 30 June 2025, it comprised 19,741 full time equivalent staff, and had an operating budget of $4.5 billion.5 The ATO’s corporate plan 2025–266 identifies ‘strengthening payment performance and debt collection’ as an enterprise priority.

1.2 The ATO defines small businesses as: any sole trader, company, trust, or partnership with annual business income of less than $10 million.7 As at July 2025, the ATO reported the number of active small businesses at 4.9 million, with an additional 2.6 million linked individuals.8 Around 71 per cent of these small businesses had an annual business income below $75,000 and 4 per cent had an annual business income between $1 million and $10 million. Of the 4.7 million active small businesses:

- 2.31 million (47.3 per cent) were sole traders, with an average annual business income of $60,000;

- 1.37 million (28.0 per cent) were companies, with an average annual business income of $412,000;

- 0.9 million (19.3 per cent) were trusts, with an average annual business income of $205,000; and

- 0.3 million (5.4 per cent) were partnerships, with an average annual business income of $204,000.

1.3 For 2023–24 the small business net income tax reported by the ATO was $91.6 billion, an increase from $76.4 billion in 2022–23.

1.4 ATO reporting categorises tax debt as: collectable debt, debt subject to objection or appeal (disputed debt), insolvent debt or debts on hold (debt that is uneconomical to pursue). Debt not pursued as irrecoverable at law is extinguished and not included in tax debt. Small business debt constitutes the majority of collectable debt. As at 30 June 2025, small business debt comprised 66.1 per cent of the value of collectable debt ($35.9 billion of $54.2 billion collectable debt) and small businesses contributed approximately 15 per cent of net tax collections. An average of 87 per cent of small business taxpayers lodged their income tax return via a tax or Business Activity Statements (BAS) agent between 2019–20 and 2024–25, while an average of 60 per cent of small business taxpayers lodged their activity statements via a tax or BAS agent between 2019–20 and 2024–25.

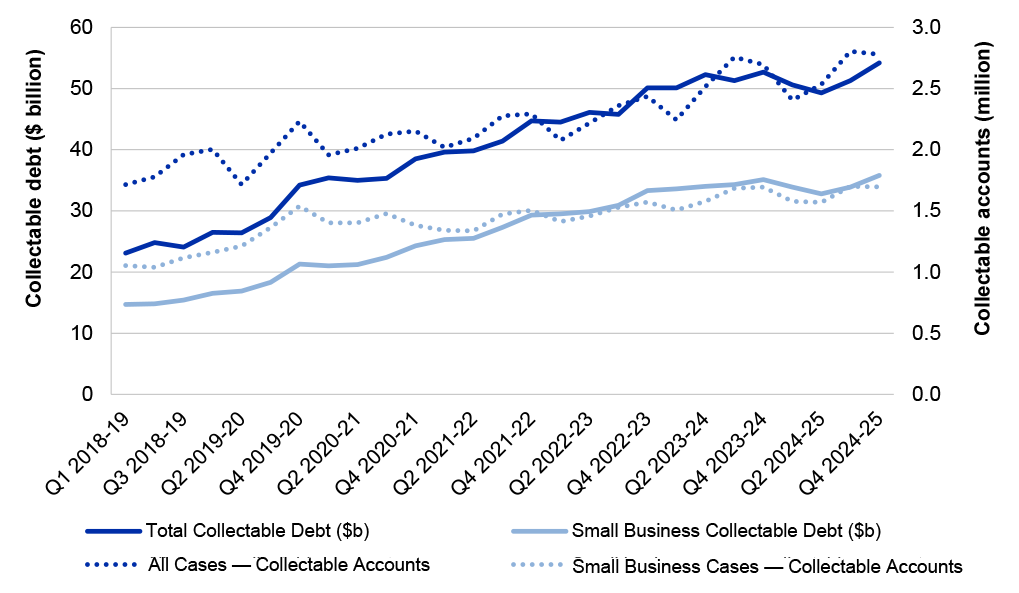

1.5 Figure 1.1 shows the growth of total collectable tax debt and small business collectable tax debt from July 2019 to June 2025.

Figure 1.1: Total collectable debt and accounts and small business collectable debt and accounts 2018–19a to 2024–25

Note a: Figure includes data from 2018–19 to provide pre-COVID-19 pandemic context.

Source: ANAO analysis of ATO data.

1.6 The 2024–25 ATO annual report indicates that $49.8 billion of the total $98.4 billion total tax owing is subject to an impairment allowance.9 The ATO states: ‘An impairment allowance is created when there is evidence that the ATO will not be able to collect all of the amounts due’.10

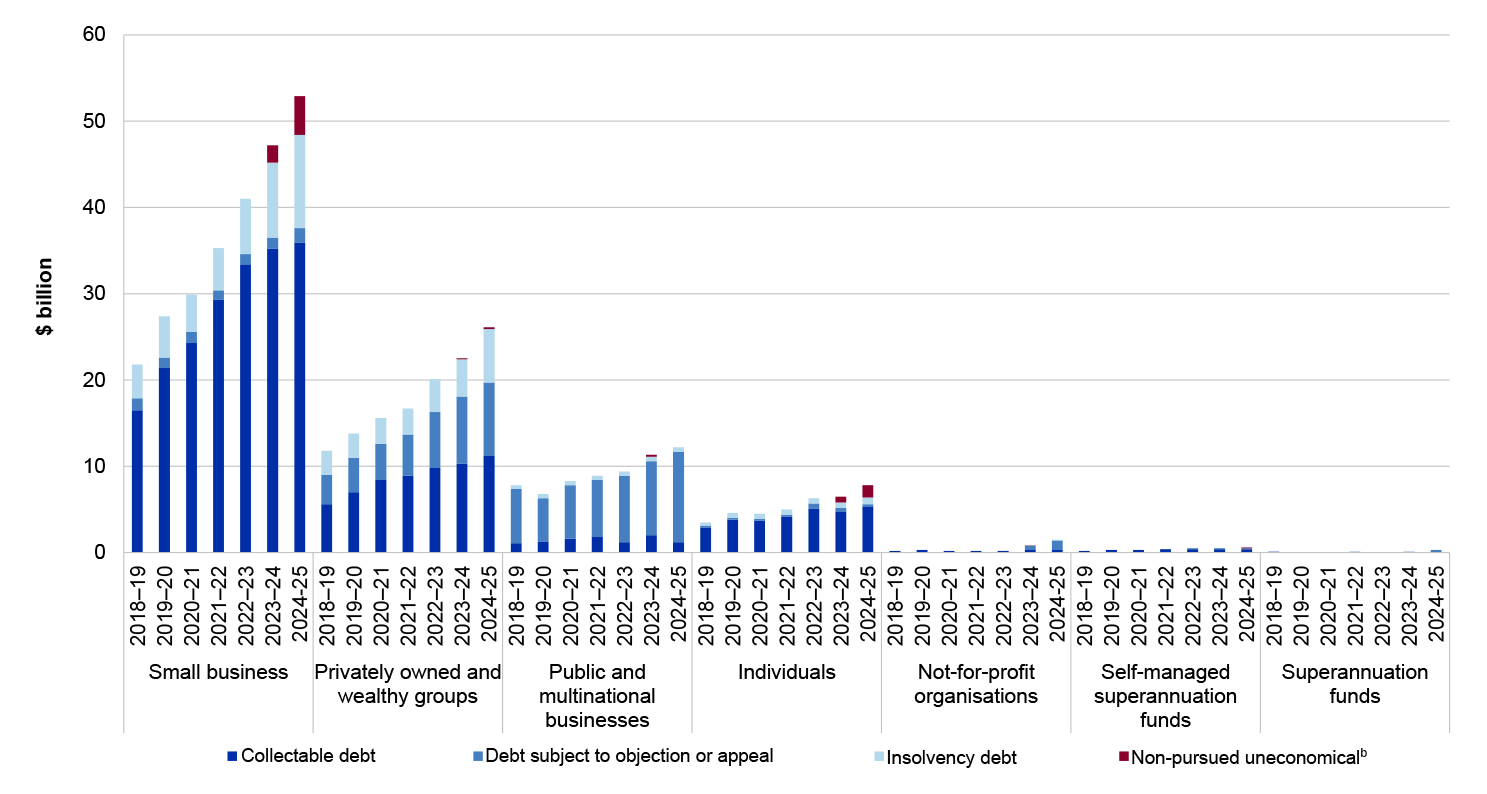

1.7 Figure 1.2 shows total tax debt owed by taxpayer group from 2018–19 to 2024–25. The ATO advised the ANAO in February 2026 that the impairment allowance was ‘not calculated in a manner that enables us to provide a breakdown by taxpayer groups.’

Figure 1.2: Total tax debt owed by group 2018–19a to 2024–25

Note a: Figure includes data from 2018–19 to provide pre-COVID-19 pandemic context.

Note b: The ‘non-pursued uneconomical debt type relates to debts placed on hold from November 2023 and is not a full representation of all non-pursued uneconomical debt. Amounts of non-pursued uneconomical debt prior to November 2023 are not visible on taxpayers’ accounts during the period of this graph and therefore not included.

Source: ANAO analysis of ATO data.

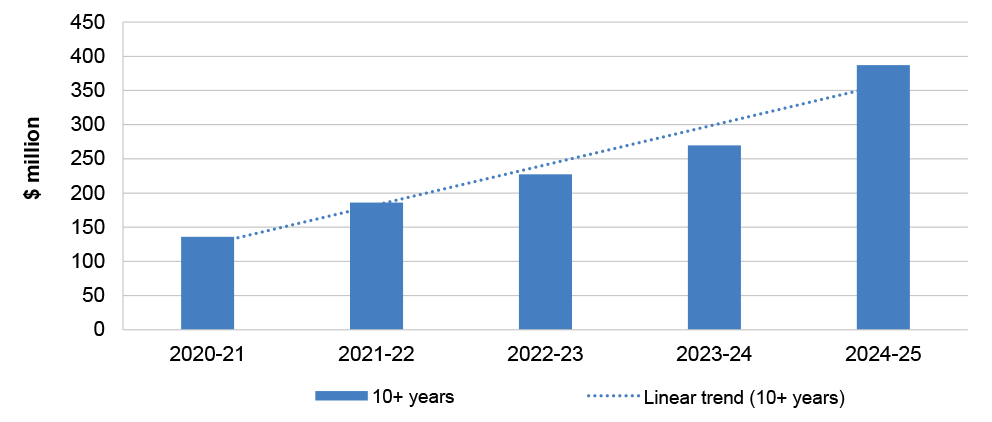

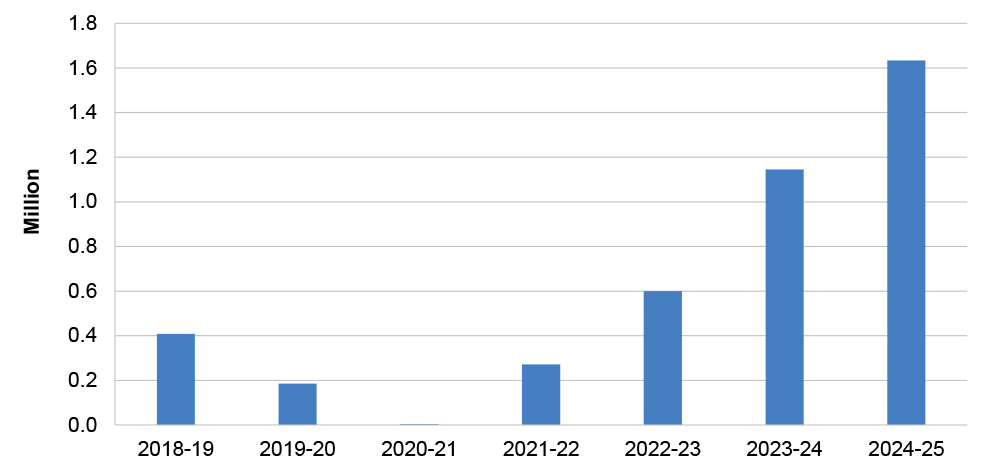

1.8 Figure 1.3 shows the growth in small business collectable tax debt aged over 10 years from 2020–21 to 2024–25.

Figure 1.3: Aged small business debt 10 years and over, and trend, 2020–21 to 2024–25

Note: In November 2025 the ATO advised: ‘In 2014, the ATO moved Super Guarantee Charge transactions from a legacy system (which was decommissioned in December 2015) into its Integrated Core Processing System. As a result, these old transactions will only be appearing in the greater than 10-year-old debt although the liabilities would have been more than 10 years old prior to 2025.

The introduction of the director penalty regime (in particular the introduction of GST DPNs in 2020) means that debts owed by insolvent and deregistered companies are now less likely to be non-pursued as irrecoverable at law as the ATO considers opportunities to pursue directors. This also impacts on the growth of aged debt.’

Source: ANAO analysis of ATO data.

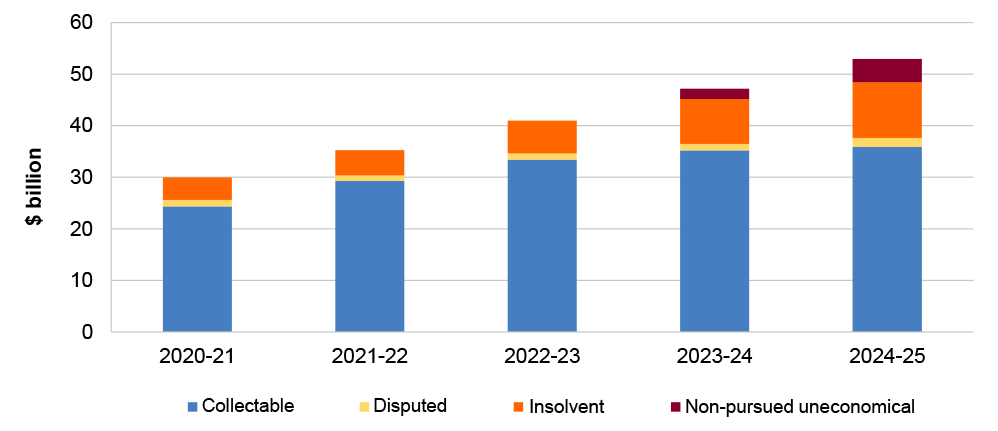

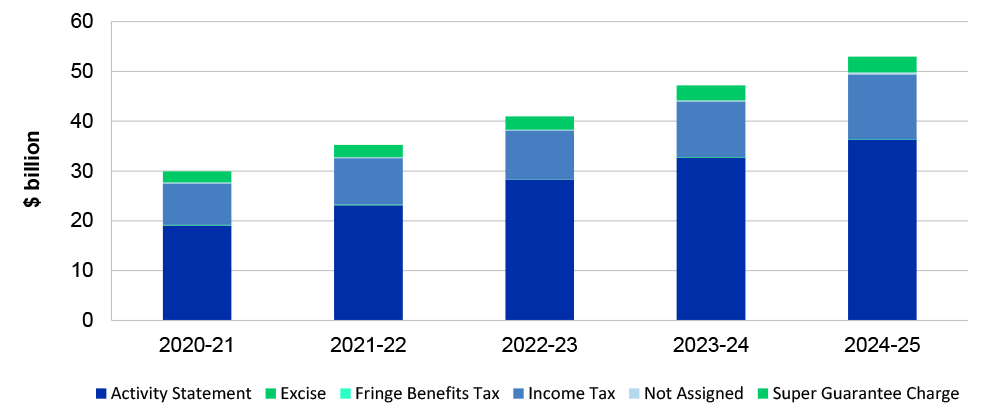

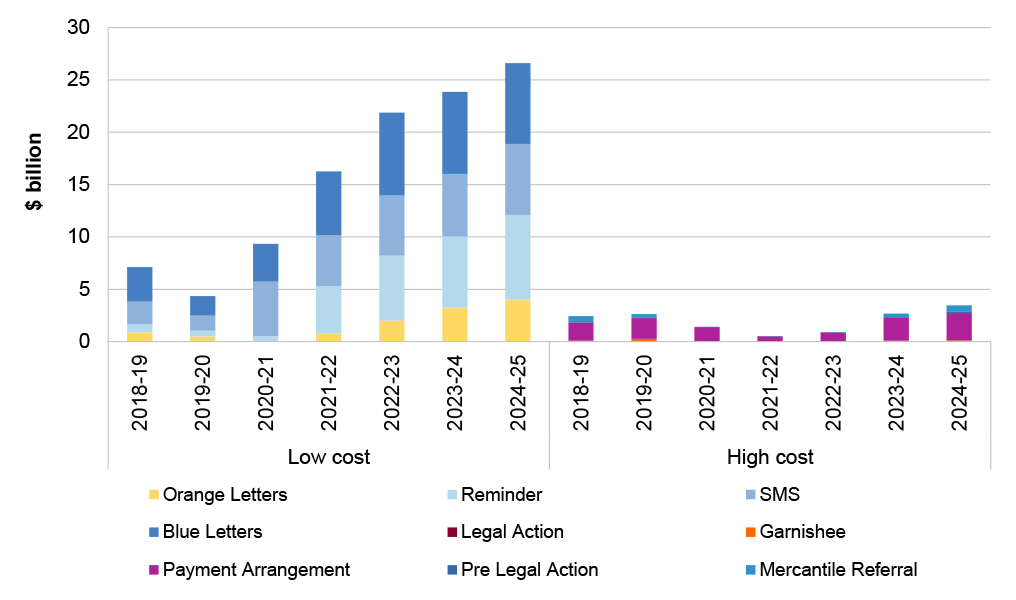

1.9 Figure 1.4 shows small business tax debt composition from 2020–21 to 2024–25.

Figure 1.4: Small business tax debt composition over time 2020–21 to 2024–25

Note: The ‘non-pursued uneconomical debt type relates to debts placed on hold from November 2023 and is not a full representation of all non-pursued uneconomical debt. Amounts of non-pursued uneconomical debt prior to November 2023 are not visible on taxpayers’ accounts during the period of this graph and therefore not included.

Source: ANAO analysis of ATO data.

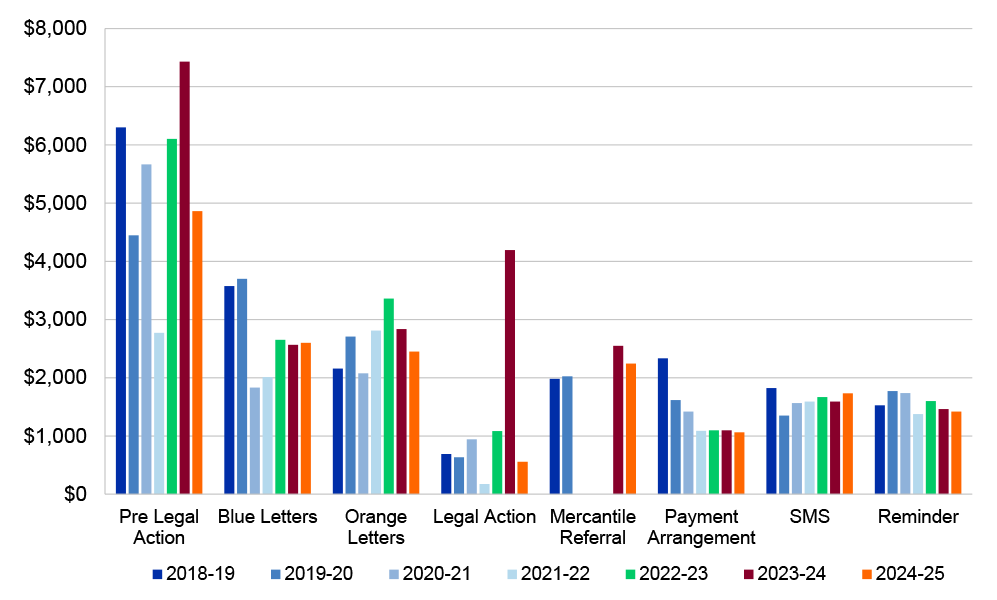

1.10 Figure 1.5 shows small business tax debt by debt source from 2020–21 to 2024–25.

Figure 1.5: Small business tax debt by tax debt source 2020–21 to 2024–25

Source: ANAO analysis of ATO data.

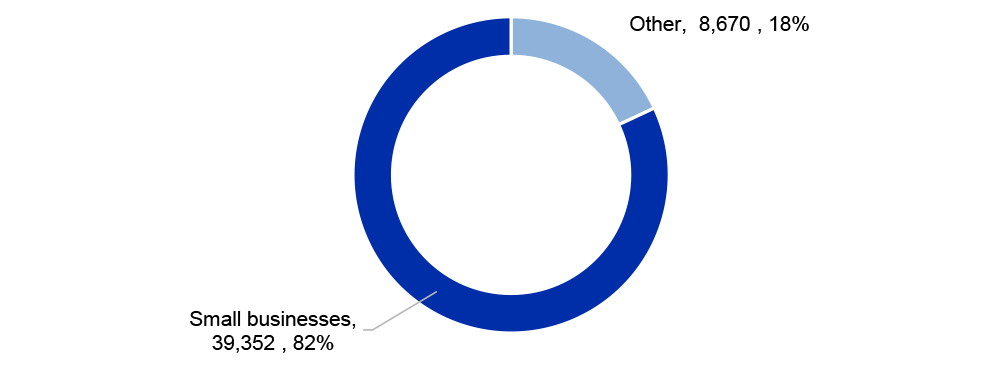

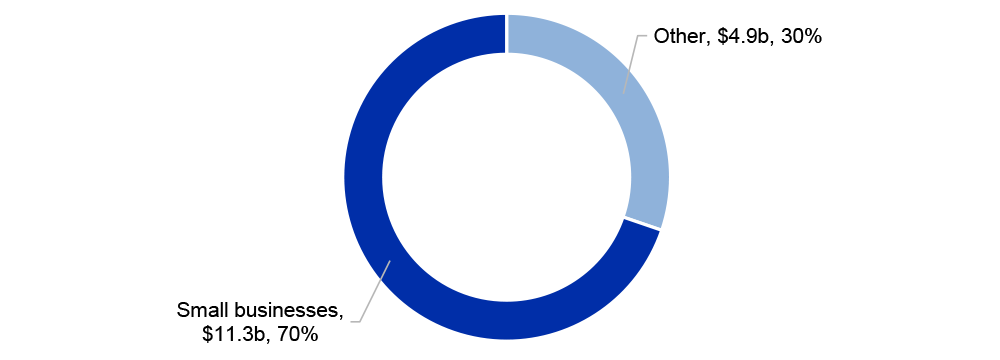

1.11 In 2024–25 the ATO identified 48,022 ‘disengaged taxpayers’ owing a total of $16.2 billion in collectable debt. The ATO defines disengaged taxpayers as those with collectable debts over $100,000 and older than 90 days that were not actively engaged with the ATO in respect of their debt. Of these disengaged taxpayers, 39,352 were small businesses owing $11.3 billion in collectable debt.11 Figure 1.6 and Figure 1.7 show the number and percentage of disengaged taxpayers with collectable small business debt and the value and percentage of disengaged small business taxpayer debt respectively.

Figure 1.6: Disengaged small business taxpayers with collectable debt 2024–25

Source: ANAO analysis of ATO data.

Figure 1.7: Value of disengaged small business taxpayers with collectable debt 2024–25

Source: ANAO analysis of ATO data.

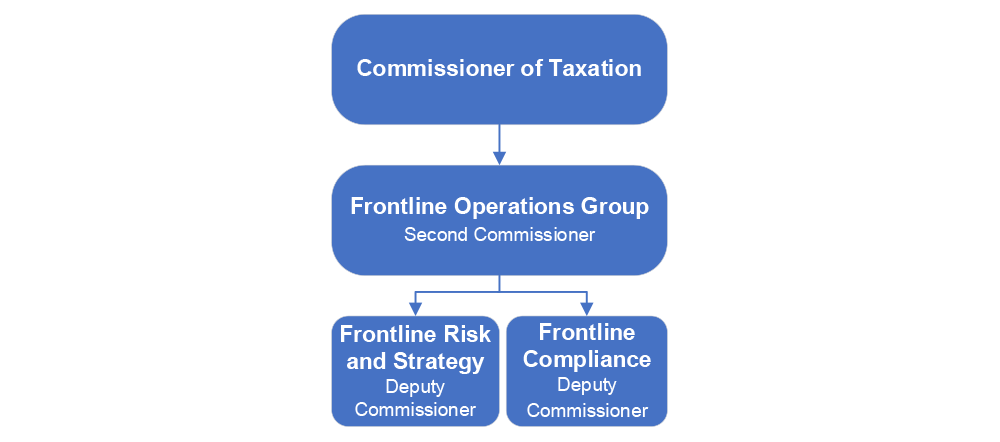

1.12 Figure 1.8 depicts the areas with accountability for the management of small business debt.

Figure 1.8: Areas in the ATO with accountability for small business debt

Note: This is not an exhaustive list of every area in the ATO with responsibility for small business debt.

Source: ANAO analysis of ATO data.

1.13 The Small Business line sits within the Compliance and Engagement group and is the business line within the ATO responsible for managing the taxation of small businesses. It seeks to ‘identify and treat risks, while delivering infrastructure, services and interventions to increase willing participation by small businesses in the tax and superannuation systems.’ Officers that manage cases in the Small Business line may refer debt matters to the Frontline Compliance12 business line if they are complex or high risk, require tailored solutions, further expertise or firmer action. Frontline Risk and Strategy is responsible for the delivery of the Payment Strategy to address tax debt through more effective and efficient debt recovery pathways. The Frontline Compliance business line is within Frontline Operations and is focused on addressing the collectable debt balance by resetting expectations and shifting taxpayers’ payment behaviour.

Support provided during natural disasters and the COVID-19 pandemic

1.14 At the direction of government, the ATO has taken action to implement relief measures for small business taxpayers due to natural disasters, the COVID-19 pandemic and global economic shocks. These impact the overall debt book. The ATO implemented several administrative measures to aid taxpayers impacted by the 2019 bushfires and the COVID-19 pandemic.13 The ATO reduced debt collection activities, offering taxpayers additional time to pay. The ATO attributed the 89 per cent increase in total collectable debt from June 2019 to June 2023 in part to these COVID-19 pandemic measures.

1.15 The ATO offered interest free payment plans and considered taxpayers’ circumstances when deciding to remit interest and penalties incurred on or after 23 January 2020 for taxpayers impacted by the COVID-19 pandemic. This was part of the ATO’s deliberate shift in focus from firmer debt collection actions to assist businesses through the pandemic.14

1.16 In a speech at the Tax Institute’s 2023 Tax Summit, the Lodge and Pay Deputy Commissioner stated that there has been an increased expectation amongst taxpayers that interest penalties will be remitted due to the ATO’s ‘lenient approach’ during the COVID-19 pandemic.15 At the 2024 Tax Summit, the Commissioner of Taxation stated that the ATO had ‘tightened up on payment plans and general interest charge remissions’.16

Actions taken since the COVID-19 pandemic

1.17 Following the peak of the COVID-19 pandemic the ATO resumed debt recovery actions. In October 2022 the ATO undertook an awareness program, contacting approximately 15,000 businesses and 18,000 directors17 with significant outstanding tax obligations totalling $1.4 billion.18 Over 5,000 taxpayers subsequently contacted the ATO and paid back $570 million. Over 4,000 of these taxpayers entered payment plans worth $492 million.19 The ATO escalated taxpayers that did not engage with awareness campaigns to enforcement actions.

1.18 In 2023–24, for all taxpayers, the ATO issued 35,774 director penalty notices20, 6,150 garnishees, 51,451 intent to disclose notices21 and 38,409 disclosures of business tax debts to credit reporting agencies.22 In 2024–25, the ATO issued 64,342 director penalty notices, 15,199 garnishees, and 29,049 intent to disclose notices and 24,533 disclosures of business tax debts to credit reporting agencies.

1.19 A small business lodgment penalty amnesty program operated from 1 June 2023 to 31 December 2023 in respect of unlodged forms. This led to over 14,000 small businesses lodging and to the remission of over $48 million failure to lodge penalties on lodgments originally due between 1 December 2019 and 28 February 2022.23 The ATO calculated that the amnesty program resulted in $344.3 million in additional liabilities being raised, with a $221.8 million net impact to the debt book due to forms that had a credit. $263.5 million in payments were received in relation to the $344.3 million of raised liabilities due to this amnesty program.

1.20 As a result of returning to business-as-usual collection activities, the growth of collectable debt decreased from 12 per cent ($5.4 billion) in 2022–23 to 5.2 per cent ($2.6 billion) in 2023–24 (see Figure 1.1).

1.21 On 14 May 2024, as part of the 2024–25 Federal Budget, the government announced it would provide the Commissioner of Taxation with the discretion not to apply refunds or credits owing to a taxpayer against debts that:

- were put on hold before 1 January 2017;

- the Commissioner is not currently pursuing recovery of; and

- are held by an individual, small business or not-for-profit entity.

1.22 This measure is not yet law.24

1.23 General Interest Charge (GIC) incurred in income years starting on or after 1 July 2025 are not tax deductible. GIC that was incurred before 1 July 2025 could be claimed as a tax deduction for the 2024–25 tax year.25

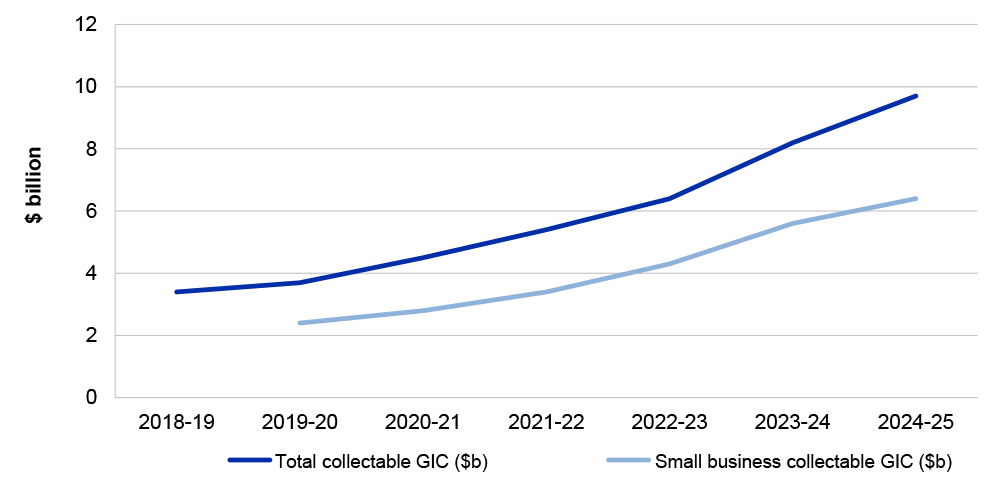

1.24 Figure 1.9 shows the value of collectable GIC for both small business and all taxpayers from 2018–19 to 2024–25.

Figure 1.9: Value of General Interest Charge on collectable debt 2018–19a to 2024–25

Note a: Figure includes data from 2018–19 to provide pre-COVID-19 pandemic context.

Small business data was not collected until 2019–20.

Source: ANAO analysis of ATO data.

1.25 In response to the increased economic impact of fuel costs arising from the conflict in the Middle East, in April 2026 the ATO introduced temporary assistance for businesses to assist in managing their tax obligations. Measures included changes to payment plans, remission of penalties and interest, varying Pay As You Go instalments, discretion not to offset debts using taxpayer credits or refunds, and may include pauses to some compliance and debt collection actions in affected industries.26

Previous audits and reviews

1.26 In March 2019 the Inspector-General of Taxation and Taxation Ombudsman27 released a Review into the Australian Taxation Office’s use of garnishee notices.28 The review concluded that the ATO’s garnishee policy generally sought to balance the ATO’s obligation of collecting debt and the need to take appropriate care in exercising garnishee powers. The review made four recommendations to which the ATO agreed including:

The IGTO recommends the ATO to develop a communication strategy for the Debt business line local site management and staff which includes a facility for direct communication from the Debt Executive for critical or complex messages where major changes to personnel resource deployment occur, particularly where personnel are new or are undertaking new work or expected to carry out work they have not engaged in for a period, so as to facilitate consistency of expectations between all levels of staff, including team working groups, at all site locations.29

1.27 Auditor-General Report No. 42 2018–19 Management of Small Business Tax Debt found that the ATO’s management of small business tax debt had been largely effective.30 The report considered the ATO’s arrangements and processes for managing small business tax debt arising from compliance activities, along with relevant monitoring and reporting activities. Recommendations were made regarding the ATO’s quality assurance framework for debt activities and performance framework for debt management. The ATO agreed to both recommendations.

1.28 The Inspector-General of Taxation and Taxation Ombudsman released an Investigation and Exploration of Undisputed Tax Debts in Australia report in 2021.31 The report found that the Australian tax system operates with a high level of voluntary compliance and that approximately 90 per cent of liabilities are paid by their respective due date and 3 per cent are unpaid after a year. The report found that collectable debt continues to grow and is the largest component of the ATO’s debt book. The ATO agreed to recommendations regarding stakeholder consultation, return on investment metrics, reporting debt past a benchmark, communication with and accessibility for businesses, and segmentation reporting. It disagreed to two recommendations regarding communication to taxpayers that their debts have passed benchmarks, and working with the Australian Bureau of Statistics to improve segmentation and reporting of industry data divisions and occupation codes.

1.29 In March 202432, the Commonwealth Ombudsman, the ACT Ombudsman, and the Inspector-General of Taxation and Taxation Ombudsman released How to tell people they owe the government money best practice principles. This best practice guide laid out five principles for contacting taxpayers and informing them about their debt status, noting that some agencies paused debt collection activities during the COVID-19 pandemic. The principles were:

- be transparent and accountable;

- tell people what the debt is and where it comes from;

- provide clear information for requesting review, debt waivers and repayment arrangements;

- provide contacts for people to find out more information; and

- learn and improve.

1.30 Actions taken by the ATO in relation to this better practice guide are explored further from paragraph 3.51.

Rationale for undertaking the audit

1.31 The ATO is responsible for managing the compliance of taxpayers in the Australian taxation and superannuation system, including pursuing tax debt. Debt that is undisputed, that is not subject to an objection, appeal, insolvency or not on hold, is considered collectable debt. Collectable tax debt from small business was $35.9 billion in 2024–25, an increase of $19.4 billion from 2018–19 and approximately two-thirds of the $54.2 billion total 2024–25 collectable tax debt.33

1.32 The ATO corporate plan 2025–26 identifies strengthening payment performance and debt collection as an enterprise priority.34 The key focus area of improving small business tax performance was removed from the corporate plan in 2024–25.35 After reducing collection activities during the COVID–19 pandemic, in 2023–24, the ATO recommenced the application of a range of firmer actions, including garnishee actions, directions to pay, director penalty notices and disclosure of business tax debt actions. Subsequent to the audit, in April 2026 the ATO introduced temporary assistance for businesses to assist in managing their tax obligations, which may include pauses to some compliance and debt collection actions in affected industries, in response to the increased economic impact of fuel costs arising from the conflict in the Middle East.

1.33 This audit provides assurance to the Parliament that the ATO effectively manages small business taxpayer debt.

Audit approach

Audit objective, criteria and scope

1.34 The audit objective was to assess the effectiveness of the Australian Taxation Office’s management of small business collectable debt.

1.35 To form a conclusion against the objective, the following criteria were developed:

- Are the risks relating to small business collectable debt appropriately managed?

- Does the ATO have a sound strategic framework to manage small business collectable debt?

- Does the ATO effectively apply its strategic framework to manage small business collectable debt?

1.36 The audit scope includes the ATO’s management of small business collectable debt (including interest and penalties) from June 2020 to June 2025. It does not include management of debt subject to objection or appeal, uneconomical to pursue, irrecoverable at law, or insolvent debt.

Audit methodology

1.37 The audit methodology included:

- review of relevant ATO documentation and walkthroughs of processes and procedures with ATO staff;

- review of publicly available ATO guidance for small businesses and taxpayers with debt;

- review of two public submissions; and

- meetings with relevant ATO staff.

1.38 The audit was conducted in accordance with ANAO Auditing Standards at a cost to the ANAO of approximately $915,500.

1.39 The team members for this audit were Shane Armstrong, Shannon Clark, Ally Cerritelli, Taylah Morgan, Jay Banpel, and David Tellis.

2. Managing risks related to small business collectable debt

Areas examined

This chapter examined whether the ATO has sound processes to manage small business collectable debt, whether these processes have occurred, whether oversight of these risks is fit for purpose, and whether the risks have been appropriately managed.

Conclusion

The ATO’s management of collectable small business debt risks is partly effective. The ATO’s pausing of debt collection measures in response to natural disasters, the COVID-19 pandemic and global economic shocks resulted in rapid growth of the debt book. The ATO has assessed that its risk of unacceptable levels of unpaid debt remains out of tolerance, and will not be brought back into tolerance in the immediate future. The ATO considers its controls to reduce this risk to be partly effective. The ATO has not set specific internal targets to reduce debt volumes. The ATO reports publicly in its annual performance statements on a whole-of-collectable debt performance measure that does not enable identification of small business debt performance.

Areas for improvement

The ANAO made three recommendations: to improve clarity of oversight of small business taxpayer debt, to improve transparency by increasing public reporting, and to set specific measurable targets regarding the reduction of the volume of small business collectable debt and assess the effectiveness of its actions to improve payment and debt outcomes.

2.1 The ATO’s corporate plan 2025–2636 identifies the following key activity: ‘Collect the right amount of tax in the most efficient way for government and the taxpayer’. Appropriate management of risks to payment is required to ensure that debt collection is efficient for both the government and the taxpayer.

Does the ATO have processes to manage risks to small business collectable debt, and are they managed in accordance with ATO requirements?

The ATO has established processes to manage both enterprise and business level risks. Risk assessments and treatment plans relating to small business debt at the enterprise and business line level have been created in accordance with ATO requirements. The ATO has assessed its controls to manage small business debt as partly effective.

Risks to small business debt are generally managed in accordance with ATO requirements. Complete documentation evidencing formal endorsement of the enterprise level risk between 2020–21 and 2024–25 was not maintained, and the 2023 risk review occurred seven months late.

The ATO’s risk management process

2.2 The documents that govern risk management at the ATO are the Risk Management Framework (RMF), and Risk Management Chief Executive Instructions (CEIs).

2.3 The RMF states that these documents ‘outline the components and arrangements that articulate the directions and approach for managing risks and expectations for all officials’. The ATO’s risk management process was developed to meet its obligations under the Commonwealth Risk Management Policy, and is based on the international standard.37

2.4 Guidance on risk management is made available to staff through internal risk management training courses, and risk management templates are provided on the ATO intranet. The ATO also uses a CEI on risk management, which outlines staff responsibilities for risk management.38

Risks relating to small business taxpayer debt

2.5 The ATO has identified risks to small business taxpayer debt at both the enterprise, and business levels.39

Enterprise level

2.6 The enterprise level risk Payment and Debt Performance has the objective of ‘[reducing] the collectable debt ratio using core strategies, enhanced through the Lodge and Pay Reset program.’ This enterprise level risk covers payment and debt management risk across all taxpayers with liabilities. The risk event as described is:

There is a risk that payment and debt performance declines to unacceptable levels, caused by volatility in economic conditions and/or ineffective ATO strategies. There is a risk ATO payment may decrease and/or debt will increase caused by taxpayers not meeting their payment obligations on-time and in full. This may result in revenue impacts for the Commonwealth, and reduced community services and broader levels of voluntary compliance.

2.7 Risk drivers identified by the ATO include taxpayers delaying payment, using delayed payment to gain a competitive advantage, using strategies to push boundaries in the tax system, potential fraud, ATO compliance treatment resulting in a debt the ATO knows the taxpayer has little or no capacity to pay, and reduced taxpayer and community sentiment towards paying tax and the benefits of taxation.

Business level

2.8 The business level risk, Small Business Client Experience Payment Risk has the objective of ‘reducing collectable debt in the small business client experience’. This risk was first endorsed in September 2024, and did not exist prior.

2.9 The risk event is identified as small businesses:

Paying tax liabilities late or not at all, trading while insolvent, using amounts withheld from employees or on behalf of the Commonwealth40 to artificially support cash flow, and prioritising payment of suppliers over the ATO.

2.10 Risk drivers identified by the ATO include: poor accounting practices, cash flow issues, prioritisation of payment of suppliers over the ATO, avoidance or delay in payment to gain a commercial advantage, broader economic conditions, and the inability of the ATO to collect tax debt early, resulting in insolvency.

2.11 The risk assessment identifies the risk likelihood as ‘even chance’, the consequence as ‘severe’, the overall risk as ‘high’, and the tolerance level as ‘medium’, noting:

We need to balance our approach with the government and community’s appetite to pursuing small business debt. Decreasing the current rating presents a challenge in the current economic environment.

Risk Management

Risk controls and treatments

2.12 Risk controls and treatments are considered at both the business and enterprise level to manage the identified risks. The business level treatment is identified as the Payment Strategy (see from paragraph 3.10). The enterprise level risk treatment notes the treatment identified in the business level risk assessment.

2.13 The ATO assesses its overall controls at the enterprise level as ‘partially effective’. Business level controls are also identified as ‘partially effective’. Table 2.1 outlines the ATO’s corrective controls at the business level.

Table 2.1: Corrective business level controls as at June 2025

|

Control name |

Control effectiveness |

|

Payment plans (see from paragraph 3.31) |

Partially effective |

|

Debt letters (see from paragraph 3.18) |

Partially effective |

|

Director Penalty Notices (DPNs) (see paragraph 4.25) |

Partially effective |

|

Garnishees (see paragraph 4.28) |

Partially effective |

|

ATO initiated insolvency/bankruptcy (see paragraph 4.31) |

Effective |

|

General Interest Charge (see paragraph 3.36) |

Partially effective |

|

Disclosure of business tax debt (see paragraph 4.28) |

Ineffective |

|

External Collection Agency (see from paragraph 3.69) |

Partially effective |

|

Dialler campaignsa |

Partially effective |

Note a: The ATO advised the ANAO in August 2025 that data was ‘not readily available’ for outbound telephony, so this control was not assessed by the ANAO.

Source: ANAO analysis of ATO documentation.

Management of risks in accordance with ATO requirements

2.14 The ATO assigns risk owners at both the enterprise and business levels to each risk. The role of risk owners is to take accountability for risks, provide direction on relevant risk management activities, oversee the status of risks, controls, and treatment strategies, and endorse risk assessments and treatment plans.

Enterprise level risk

2.15 The enterprise level risk owner is identified as the Frontline Risk and Strategy Deputy Commissioner.41 The enterprise level risk assessment and treatment plan was not appropriately endorsed by the risk owner on one occasion.

2.16 While the consequence of the enterprise level risk has consistently been considered ‘major’, the likelihood was considered ‘unlikely’ until 2023, when it was increased significantly to ‘almost certain’. This moved the risk from ‘within tolerance’ to ‘above tolerance’, with the ATO identifying the Lodge and Pay Reset (see from paragraph 3.8) and associated treatments as the way of bringing the risk back within tolerance.

2.17 The enterprise level risk plan notes that all treatments will be implemented by 30 May 2025. While initial implementation of Client Prioritisation and Segmentation was completed by May 2025, and initial implementation of data and analytics requirements were a month away from completion, implementation of an integrated treatment plan with enduring controls was scheduled for implementation in June 2026. As at February 2026, the ATO has commenced updating systems to enable segmentation, expected to be completed in the 2026 calendar year.

2.18 The enterprise level risk is scheduled for review every two years, with the review required to occur by 31 December 2023 occurring in July 2024 which is inconsistent with the required review schedule. The ATO next reviewed the risk in June 2025.

Business level risk

2.19 The business level risk owner is identified as the Assistant Commissioner, Lodgment, Payment and Data Strategy. The business level risk assessment and treatment plan was appropriately endorsed by the risk owner. The risk was reviewed in June 2025 by the Band 1 Frontline Risk and Strategy Committee, which concluded that while some risk controls had seen performance improvements, that there had been no material change in control effectiveness.

Is oversight of the management of small business collectable debt fit for purpose?

The ATO had 13 committees or groups considering small business debt between 2019–20 and 2024–25. The ATO Risk Committee has increased its focus since 2021–22 on the management of the payment risk. It has sought assurance over the effectiveness of controls and has requested the development of key performance indicators. The Risk Committee was advised in June 2024 that small business debt will likely remain out of tolerance for a further one to two years.

Given the significant proportion of total collectable debt that is owed by small business, the collection of small business collectable debt should remain a focus of oversight and reporting.

The small business collectable debt ratio is a major contributor to the ATO’s overall collectable debt ratio but public reporting is minimal. Recommendations from the Tax Ombudsman concerning public reporting of debt have not been fully implemented. Improved public reporting of the ATO’s performance in reducing collectable debt would improve transparency and oversight of risks and the ATO’s management of them.

Risk oversight bodies

2.20 The ATO stated in April 2025 that between 2019–20 and 2024–25, 13 committees or groups met to discuss small business taxpayer debt either exclusively, or as part of a broader conversation around ATO debt management.42

2.21 The Australian Public Service Commission’s capability review of the ATO, finalised in 2025 identified as a priority area for development: ‘Addressing the organisational strategy capability gaps identified … including streamlining internal governance and ensuring clear accountabilities.’43

Enterprise level

2.22 As outlined in paragraph 2.2, the ATO has a Risk Management Framework and Risk Management Chief Executive Instructions (CEIs), which establish that a Risk Owner is personally accountable for identified risks. The Frontline Risk and Strategy Deputy Commissioner is identified as the enterprise level risk owner (paragraph 2.15).44 The ATO Risk Committee, chaired by a Second Commissioner, and comprising four Deputy Commissioners, engages with enterprise level risks. Its engagement with the small business Payment and Debt Performance risk has increased between 2021–22 and 2024–25. Initial meetings were provided with high level information that generally mentioned small business without detail. This changed in 2024, with small business identified as a key driver of the overall debt problem. In September 2024, the ATO Risk Committee requested further evidence that the treatment strategy was driving progress. Minutes of the meeting noted:

Development of the treatment strategy was acknowledged, while the committee were [sic] encouraged by the approach, there hasn’t yet been enough progress to give the committee adequate assurance. On this basis, the Chair was not assured yet and has asked the risk owner to return to the committee to report on progress.

2.23 The issue of the efficacy of the treatment strategy was brought back to the Committee in February 2025, with the ATO summary of the meeting noting:

The Committee requested the key performance indicators to be prioritised, confirmation of timeframes to bring the risk within tolerance, and validation of the effectiveness of key controls.

2.24 The ATO Risk Committee was advised in June 2024 that:

it is expected the risk will continue to reduce towards in tolerance within the next 12 months.

While at an enterprise level the risk may expect to come back towards in tolerance within the next 12 months, it is likely that Small Business debt will remain out of tolerance for a further 1–2 years, noting the significant shift in behaviour required for this taxpayer segment.

2.25 The minutes of this meeting state that the Chair noted ‘the significant progress made to date with respect to this enterprise risk’, ‘that what in tolerance of this enterprise risk looks like is under review’, and ‘the feedback provided by the Committee on the measures and KPIs’ and ‘noted that the view of in tolerance of this enterprise risk is evolving.’

2.26 The Committee also queried the methodology applied to make assessments about the effectiveness of controls. The Committee also considered what ‘in tolerance’ would look like for this risk, with a Deputy Commissioner’s reply summarised as:

if we tie it to a number we may never be within tolerace [sic]. Tolerance needs to be determined for payment to ensure it is maximised, and for management of debt, to prevent significant growth. It was about strengthening controls to as good as they can be and demonstrating that those controls are effective in managing the risk.

2.27 The ATO has focused its reporting to the ATO Risk Committee on preventative measures rather than on measures to pursue outstanding debt, particularly aged debt.

2.28 The ATO advised the ANAO in February 2026 that it had commenced work on improving risk controls, and measurement and evaluation.

2.29 The Lodge and Pay Band 1 Risk Committee was established in August 2020 with a purpose of driving the identification and management of enterprise lodgement and payment risks. The Lodge and Pay Band 1 Risk Committee discussed small business taxpayer debt risk at nine of its thirteen meetings, with most mentions in relation to the proportion of small business debt to overall debt.

Business level

2.30 As outlined in paragraph 2.2, the ATO has a Risk Management Framework and Risk Management Chief Executive Instructions (CEIs), which establish that a Risk Owner is personally accountable for identified risks. The Assistant Commissioner, Lodgment, Payment and Data Strategy is the business level risk owner (paragraph 2.19). The ATO advised in October 2025 that Frontline Risk and Strategy (FRS) executives ‘held the primary responsibility for the payment and debt risk at the enterprise level, including the payment and debt risk for Small Business.’ Further, the ATO advised:

FRS inform and consult with a number of committees that have oversight of the payment and debt risk across the ATO. There are also specialist committees that deal specifically with Small Business issues (FRS inform, consult and engage with these committees).

2.31 The ATO stated that a number of committees were in operation at the business level, including:

- a Frontline Risk and Strategy Committee established following the merger of the Lodge and Pay Risk Committee and the Registration Risk Committee in May 2025, with ‘direct accountability for the governance and management of business-level payment risks’;

- a Registration, Lodgment and Payment Risk and Strategy Assurance Committee, established in September 2024, which the above Committee reports to. This Committee is intended to facilitate a whole-of-ATO response to relevant risks, and undertake a risk call-over process, risk assessments, and treatment plans. This committee has met twice between September 2024 and June 2025; and

- other specialist committees that deal specifically with small business issues.

2.32 While the ATO has several committees that discuss small business taxpayer debt, it is not clear that any of them have direct responsibility to monitor the measures used to reduce small business taxpayer debt, and to make recommendations on how to improve performance around debt reduction.

2.33 This is consistent with the findings of the Australian Public Service Commissioner’s 2025 Capability Review of the Australian Taxation Office:

The review observed that the ATO has an extensive governance architecture, but it is not always fit for purpose. Stakeholders said there are too many governance committees and some lack a clear purpose. At times they are treated as forums for consultation and consensus rather than making decisions and negotiating trade-offs.45

2.34 The Australian Public Service Commissioner also observed:

ATO leadership has plans to conduct a review of its enterprise governance framework. Such a review would provide a good opportunity to streamline the committee structure, consider ways to leverage these forums to facilitate agency-wide prioritisation, and ensure accountabilities are appropriately allocated and not diluted by committees.46

2.35 The Commissioner of Taxation formally responded to the Capability Review, stating that the ATO would ensure ‘effective internal collaboration’, and that everyone understands ‘their contribution, not just to their direct responsibilities and functional accountabilities, but to broader outcomes.’47

Recommendation no.1

2.36 The Australian Taxation Office, as part of its review of its enterprise governance framework, ensure clear accountabilities and reporting lines regarding small business taxpayer debt.

Australian Taxation Office response: Agreed

The ATO Executive, the Commissioner of Taxation and the Treasurer

2.37 The ATO Executive48 engages specifically with small business debt issues infrequently, and in a superficial manner. Where small business debt is mentioned in Executive meetings, it is part of a more general discussion on debt, including the proportion of small business debt in the total debt book, and in relation to the Lodge and Pay Reset (see paragraph 3.8). The ATO Executive is not provided with detailed data on the ATO’s performance in managing small business taxpayer debt.

2.38 The Commissioner was provided with a briefing on the ATO’s debt book as a whole in January 2024. The briefing contained high level information on small business debt, noting it comprised 65 per cent of total debt, that activity statement debt from small business had increased, and that insolvent small business debt from activity statements had driven increases in insolvent debt. Graphing also showed the collectable debt ratio for small business, and total small business debt.

2.39 The ATO’s Statement of Intent49 outlines the ATO’s undertaking to the Treasurer: ‘The ATO will keep the responsible Minister informed with accurate and timely advice on significant issues in its core area of business.’

2.40 Between 2022 and 2025, the ATO provided two submissions to the Treasurer relating to small business tax debt, both in 2025.

2.41 The first submission was in response to a request from the Treasurer in August 2025 for further information on measures to prevent small business debt. The response did not include information on the totality of small business debt, trends, or the issue of aged debt.

2.42 The second submission elaborated further on the preventative measures identified in the first submission.

ATO reporting

2.43 The publicly reported performance measures relating to taxpayer debt are:

- proportion of payments made on time;

- collectable debt ratio50;

- debt non-pursued — uneconomical to pursue; and

- debt non-pursued — irrecoverable at law.

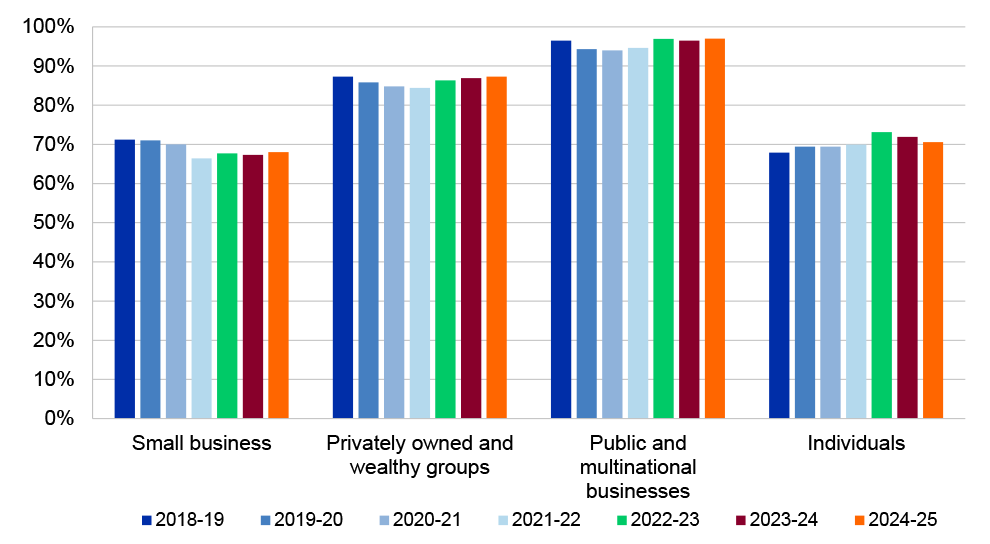

2.44 The ATO reports against these measures in its annual report51, reported in totality across all groups.52

2.45 Volumes of small business collectable debt, debt subject to objection or appeal, and insolvent debt are publicly reported in the ATO’s annual report.53

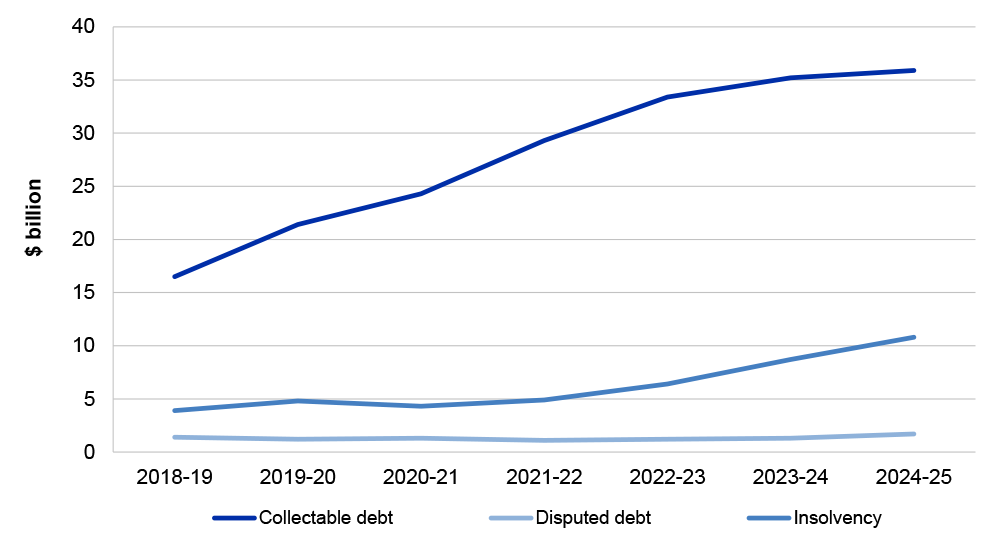

2.46 Figure 2.1 depicts collectable debt, disputed, and insolvent debt — all the publicly reported small business data contained in the ATO annual report between 2018–19 and 2024–25. It shows a rise in collectable debt, disputed debt and insolvency debt across the period.

Figure 2.1: Publicly reported small business debt data 2018–19a to 2024–25

Note a: Figure includes data from 2018–19 to provide pre-COVID-19 pandemic context.

Source: ANAO analysis of ATO data.

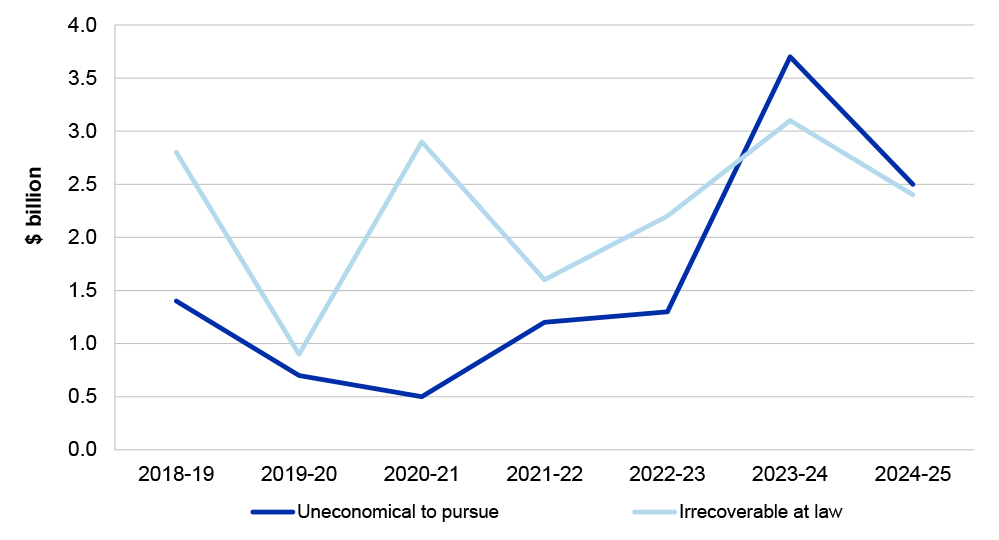

2.47 Figure 2.2 depicts debt considered uneconomical to pursue and irrecoverable at law across all taxpayer groups.54 There was a significant increase in debt deemed uneconomical to pursue between 2022–23 and 2023–24. The ATO annual report 2024–25 states: ‘The year-on-year decrease is a result of 2023–24 being an anomalous year that included the identification of debts uneconomical to pursue or irrecoverable following the COVID-19 pandemic.’55

Figure 2.2: Publicly reported debt uneconomical to pursue and irrecoverable at law (all groups), 2018–19a to 2024–25

Note a: Figure includes data from 2018–19 to provide pre-COVID-19 pandemic context.

Source: ANAO analysis of ATO data.

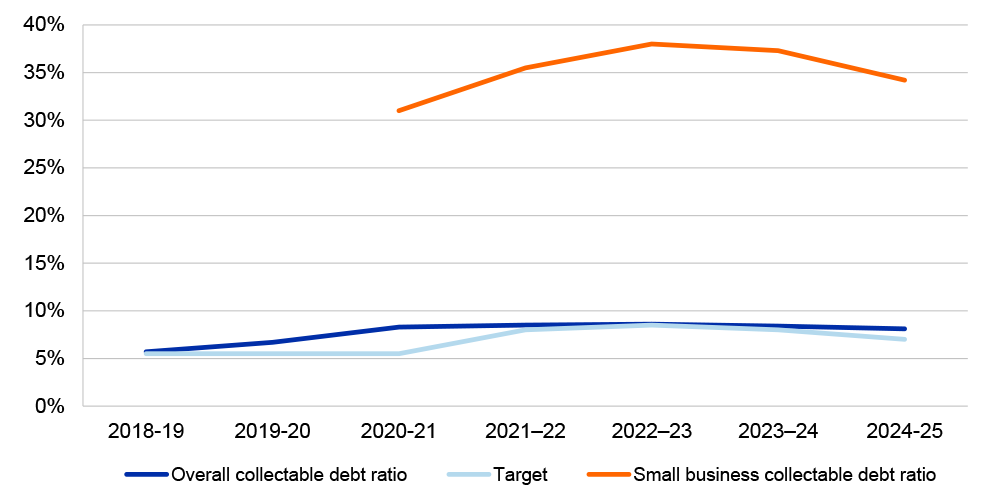

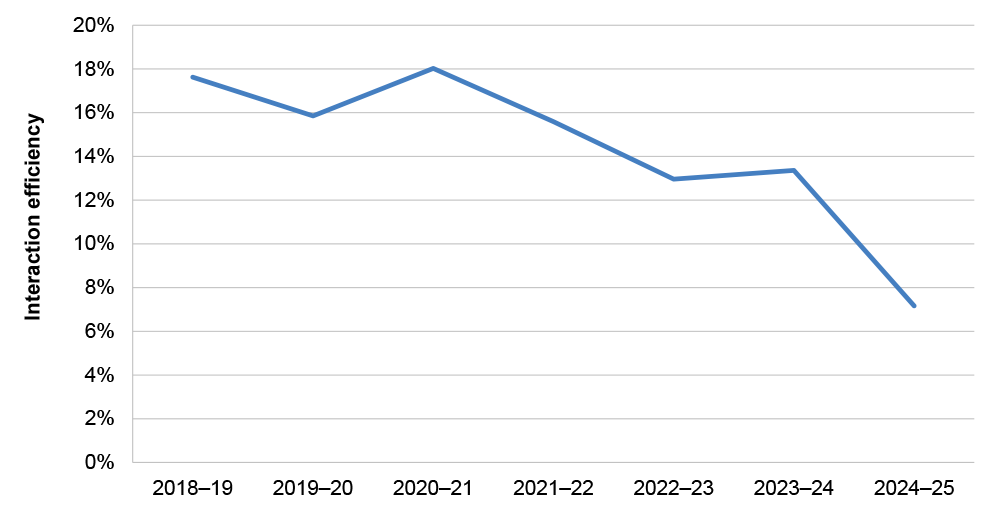

2.48 The collectable debt ratio is a measure of the effectiveness of the ATO’s debt prevention, collection, and management strategies, reflecting the proportion of collectable debt compared to net tax collections. A lower collectable debt ratio indicates that debt is being recovered relatively effectively. A higher ratio indicates lower effectiveness in recovery. The collectable debt ratio is used by the ATO as a performance measure to determine the effectiveness of the ATO’s debt prevention, collection and management strategies. Figure 2.3 depicts the overall collectable debt ratio, the small business collectable debt ratio, and the ATO’s target collectable debt ratio from 2018–19 to 2024–25.

Figure 2.3: Overall collectable debt to net tax collections ratio, small business collectable debt to small business net tax collections ratio, and ATO target collectable debt ratio 2018–19a to 2024–25

Note a: Figure includes data from 2018–19 to provide pre-COVID-19 pandemic context.

The ATO only started recording the small business collectable debt ratio from 2020–21.

Source: ANAO analysis of ATO data.

2.49 While the ATO reports on the overall collectable debt ratio, it does not publicly report on the small business collectable debt ratio. For more information on the collectable debt ratio, see from paragraph 2.60. The ATO’s annual report includes in an appendix small business debt broken down by collectable debt, debt subject to objection or appeal, insolvency debt, and from 2024–25, non-pursued uneconomical.56

2.50 The 2021 Inspector-General of Taxation and Taxation Ombudsman57 report An investigation and exploration of undisputed tax debts in Australia recommended that the ATO consult with key stakeholders to co-design enhanced reporting in relation to the debt book and debt recovery activities, and stated that the enhanced reporting ‘may be shared publicly or with discrete stakeholders, as appropriate’.58 The ATO advised the ANAO in June 2025 that all recommendations had been fully implemented. Following external consultation, the ATO identified its annual Taxation statistics publication as the best way to share data on tax debt. The information was planned for inclusion in 2024.

2.51 The ATO’s most recent Taxation statistics publication is for 2022–23 (published 27 June 2025).59 Information about tax debt is not included.60

2.52 The ATO advised the ANAO in September 2025 that:

Subsequent to endorsement of the recommendation the publishing of the data was paused. This was due to changes in the internal ATO operating environment and other external factors.

We remain committed to transparency with taxpayers and the community about debt and using this to inform. In light of our refreshed strategies and approaches to managing debt such as the payment strategy and making debts on hold visible we are reviewing the information we publish on debt.

2.53 It has been five years since the Tax Ombudsman made the initial recommendation about public reporting. The ATO has not publicly reported data as recommended and agreed. It should also be noted that the Taxation statistics publication publishes two years prior to the current financial year data to allow for sufficient lodgment to increase confidence that the statistics are accurate. More contemporary data would enable the Parliament and the general public to better understand the ATO’s performance in managing small business taxpayer debt.

Recommendation no.2

2.54 The Australian Taxation Office publicly report the current annual proportion of payments made on time, collectable debt ratio, disputed debt, debt non-pursued — uneconomical to pursue, and irrecoverable at law in a timely manner and on a recurring basis to increase transparency around the scale of small business taxpayer debt, and the effectiveness of the ATO’s strategies in reducing it.

Australian Taxation Office response: Agreed

2.55 Internally, the ATO monitors various aspects of its performance in managing small business taxpayer debt via the Payment Risk Performance Update, and Debt Segmentation Analysis dashboards. Data is also available for analysis in the ATO’s Debt Client Engagement Interactions Cube, which enables data to be analysed by numerous dimensions, including client experience (such as small business), industry group, interaction type, next interaction type and direction (inbound, outbound). For more information on these monitoring tools and how they are used by the ATO, see from paragraph 4.51.

Is the small business collectable debt risk appropriately managed?

Within its risk management framework, the ATO has a stated objective of reducing small business collectable debt. It measures its performance through the ratio of collectable debt to net tax collections. This ratio does not provide transparency on small business collectable debt as the debt ratio may be able to be reduced while the total volume of small business collectable debt continues to rise.

The ATO does not set specific measurable targets regarding the reduction in the volume of small business collectable debt. Doing so would assist the ATO in its efforts to reduce small business collectable debt.

2.56 As set out in paragraph 2.8 the mitigations of the Small Business Client Experience Payment Risk have the objective of ‘reducing collectable debt in the small business client experience’.

2.57 The ATO advised in November 2025 that:

It is unlikely small business collectable debt will reduce due to the legislative framework under which the ATO operates, including imposition of General Interest Charge, and the limited avenues that extinguish debt. Our focus is on containing the growth of debt.

2.58 The view that the reduction in small business debt is unlikely is not reflected in the ATO’s risk management documents.

2.59 Figure 2.4 depicts the volume of small business collectable debt, and the small business collectable debt ratio from 2020–21 to 2024–25. It indicates that while the small business collectable debt ratio has begun to trend downward, the volume of collectable debt continues to grow.

Figure 2.4: Small business collectable debt volume and ratio 2020–21 to 2024–25

Note: The collectable debt ratio is a measure of the effectiveness of the ATO’s debt prevention, collection, and management strategies, reflecting the proportion of collectable debt compared to net tax collections.

Source: ANAO analysis of ATO data.

2.60 While there has been a downward trend in the collectable debt ratio since 2022–23 the small business collectable debt ratio remains high. A document provided to the Frontline Risk and Strategy Committee in June 2025 stated:

As of 31 March 2024, the ratio of collectable debt to net tax collections for the small business client experience is 36.8% compared to the ATO [debt] ratio of 8.7%. The ATO performance target for the 2023–24 year is between 7.5% and 8.0%, indicating that small business is above this target with a 28% deviation. The consequence level is Catastrophic (> 25% variance) — severe impact on achievement of outcomes and performance.

2.61 The small business collectable debt ratio is a significant contributor to the overall collectable debt ratio, due to small business collectable debt representing a significant proportion of total collectable debt. The ATO advised in November 2025 that the 8.5 per cent collectable debt (monthly) ratio recorded for June 2025 would reduce to 3.8 per cent were small business to be excluded. While there are no clearly identified targets concerning the volume of small business collectable debt, reducing the small business collectable debt ratio is a measure that has been discussed within the ATO, though no target has been set.

2.62 The ATO’s goal to reduce the broader collectable debt ratio to six per cent by 2026–27 is part of its formal performance measures.61 The ATO’s documentation notes that it does not ‘have reliable modelling to predict the debt book response to our enhanced strategies’, but has outlined the following internal targets. Table 2.2 outlines the ATO’s ‘pathway to tolerance’, outlining desired net increases in collections, and the projected collectable debt ratio.

Table 2.2: ATO ‘pathway to tolerance’ 2024–25 to 2026–27

|

End of financial year |

Desired net increase in collections ($b) |

June collectable debt ratio targets (%) |

|

2024–25 |

3.2 |

6.5–7 |

|

2025–26 |

3.6 |

7 |

|

2026–27 |

3.9 |

6a |

Note a: The ATO stated in April 2026 that the six per cent target had been revised to seven per cent for 2026–27 in March 2026.

Source: ANAO analysis of ATO data.

2.63 ATO documentation stated:

Achieving [a] 6% ratio by [the] end of [the] 2027 financial year would require reducing the net collectable debt book by $10.7b to $40.6b. This is over and above the current collections achieved and requires a shift in strategy in terms of seeking to reduce the amount of debt incurred, as well as timely payment by clients who incur a debt and more timely exit62 of taxpayers without capacity to pay.63

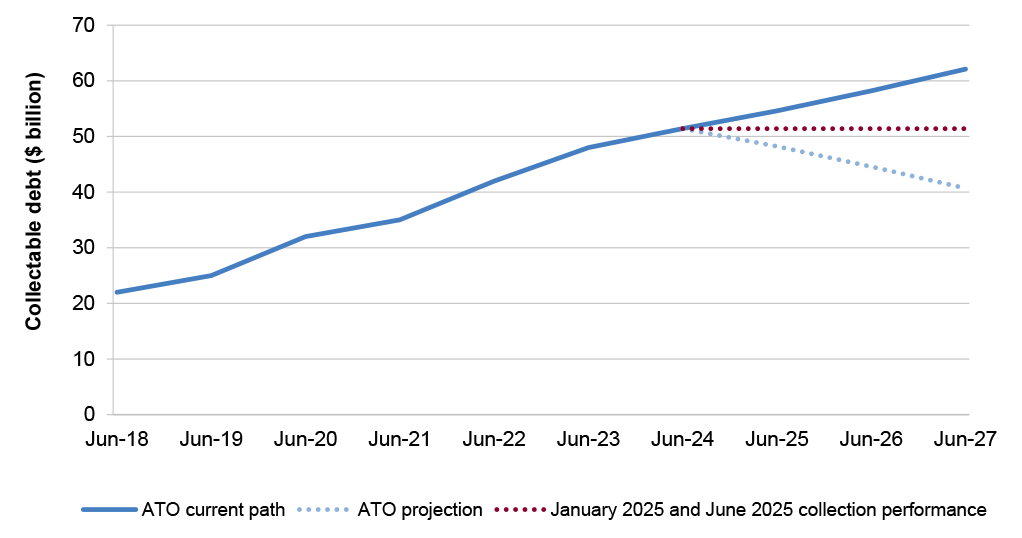

2.64 The ANAO analysed the ATO’s projection, applying six months of actual figures between January and June 2025 to assess progress against the ATO’s projection. Figure 2.5 depicts the ATO’s identified current trajectory as at January 2025, the ATO’s desired projection of the reduction in collectable debt to return to a six per cent collectable debt ratio by 2026–27, and progress should collection performance continue on the trajectory set between January 2025 and June 2025.

Figure 2.5: Collectable debt volumes and forward projections 2018–2027

Source: ANAO analysis of ATO data.

2.65 The absence of clearly defined targets or performance measures for each control designed to actively reduce the volume of small business debt and to reduce the small business collectable debt ratio means the ATO is unable to define what success looks like as it seeks to bring the overall collectable debt ratio back to six per cent. Without the inclusion of measurable targets, the ATO is unable to adequately evaluate its current performance.

Recommendation no.3

2.66 The Australian Taxation Office:

- set a specific measurable target to reduce the volume of small business collectable debt; and

- assess the effectiveness of its actions to improve payment and debt outcomes.

Australian Taxation Office response: Agreed

3. The ATO’s strategic framework to manage small business collectable debt

Areas examined

This chapter examined whether the Australian Taxation Office (ATO) has a sound strategic framework to manage small business collectable debt.

Conclusion

The ATO has a largely sound strategic framework for debt collection. This is a whole-of-debt strategy that is not specific to small business. Small business collectable debt makes up 66.1 per cent of total collectable debt. The ATO recognised that measures adopted during the COVID-19 pandemic ‘normalised into poor payment behaviours’ among taxpayers and commenced a Lodge and Pay Reset to return to business-as-usual recovery actions. The ATO has assessed that a significant behavioural shift by small business taxpayers is required to bring the collectable small business debt risk into tolerance. The ATO is able to measure payment behaviour, response rates, debt outcomes and changes in lodgment and payment compliance. The ATO has not fully incorporated best practice principles in communicating with taxpayers about debt. Given the continued increase in volumes of small business collectable debt there would be benefit in the ATO evaluating the effectiveness of each form of interaction and based on this, developing an approach specifically supporting its engagement with small business taxpayers.

Areas for improvement

The ANAO made a recommendation that the ATO determine the effectiveness of its engagement with small business taxpayers with debt by monitoring and reviewing taxpayer responses to inform its future small business debt management approach.

The ANAO also suggested that there were opportunities for the ATO to establish an engagement approach specifically for small business taxpayers with debt, and to incorporate the principles articulated in the Ombudsmen’s report How to tell people they owe the government money: Best practice principles for notifying people about debts.

3.1 The ATO’s corporate plan 2025–2664 identifies the following key activity: ‘Collect the right amount of tax in the most efficient way for government and the taxpayer’. A sound strategic framework is required to ensure that debt collection is efficient for both the government and the taxpayer.

Is the framework to manage small business taxpayer debt well designed?

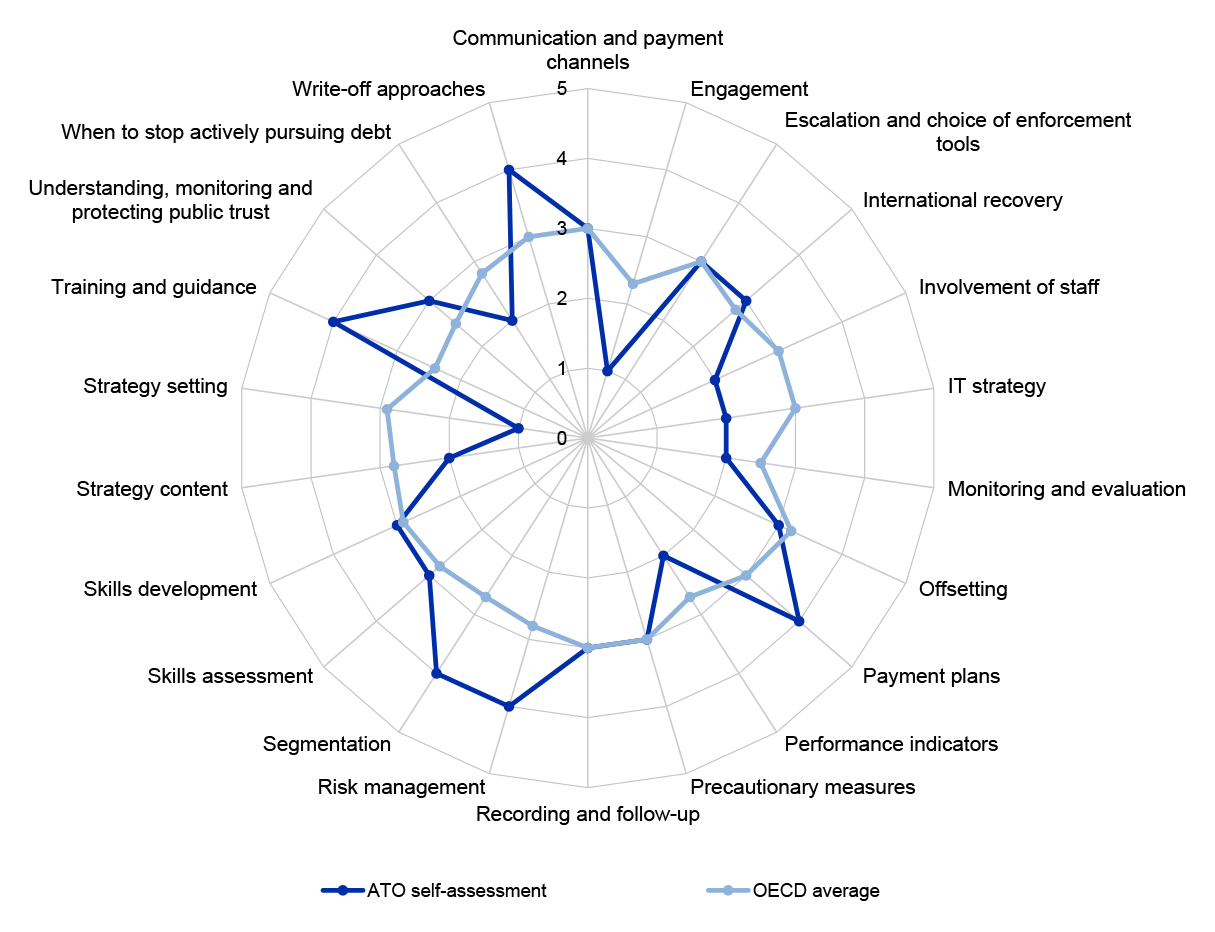

The ATO has a whole-of-debt framework. The framework is informed by a management-initiated review, and the ATO’s Risk Management Framework. It is also based on several OECD sources including the OECD Tax Debt Management Maturity Model. The ANAO’s assessment of the ATO against this model found less mature arrangements on risk management and performance indicators, and more mature arrangements on IT strategy relative to the ATO’s self-assessment.

3.2 As discussed in paragraph 1.14 the ATO reduced debt collection activities due to the 2019 bushfires and COVID-19 pandemic. Prior to 2023, the ATO’s debt and lodgment operational delivery plan consisted of three phases to recommence engagement.

- Prevention through communication.

- Educating and supporting taxpayers to meet their obligations.

- Firmer actions where appropriate and stronger actions for high-risk taxpayers.

3.3 In 2022 the ATO established the Lodge and Pay Engagement and Action Differentiated Framework. This framework categorised taxpayers by risk level and behavioural groups to determine the ATO’s approach to assist taxpayers in meeting their obligations. For medium and high-risk taxpayers, machine learning models drove the Next Best Action (NBA) framework (see from paragraph 3.78) which included warning letters and legal action.

2023 review of Tax Debt Management Strategy

3.4 As a result of the ‘out-of-pattern growth of collectable debt and deteriorating lodgement outcomes’ the ATO engaged McKinsey & Company (McKinsey Co.) to conduct a review of the ATO’s tax debt management strategy in January 2023.65 The resulting reports ‘ATO Lodge and Pay Strategy Part A: Assessment of the existing Lodge and Pay Strategy’ and ‘Part B: Opportunities for the future’ were finalised in April 2023.

3.5 Part A drew from five sources of insight interviews with the ATO Executives, an assessment of collections maturity, a data deep dive, interviews with taxpayers, and best practice case studies. McKinsey Co. found:

- the ATO is among the top five performers in the OECD on tax collection and performs well relative to peers on key debt collection metrics;

- the ATO needs to understand the outcomes of initiatives and the opportunity for segmentation of taxpayers;

- a significant proportion of taxpayers are likely to have capacity to pay;

- a significant portion of the ATO debt book is likely irrecoverable and consuming collections capacity;

- that taxpayers used avoidance as a coping mechanism when facing acute financial pressure; and

- opportunities existed for optimised channels for taxpayers.

3.6 Part B identified opportunities for the ATO to achieve its short-term goal of six per cent collectable debt ratio by June 2025, and its long-term goal of making lodgement and payment ‘just happen’ by 2030. McKinsey Co. determined three central themes to achieving these goals: enhanced ability to differentiate and target collections interventions; collect tax sooner and more frequently; and to enhance transparency of data and operation performance. McKinsey Co. recommended six priority initiatives66 to achieve the ATO’s short-term goals and provided a one year roadmap as guidance.

3.7 McKinsey Co. recommended 40 potential initiatives and 12 capabilities.67 The capabilities included:

- segmentation and analytics (see from paragraph 3.59);

- contact strategies (see from paragraph 3.18);

- collection/treatment strategies (see from paragraph 3.58);

- External Collections Agency management (see from paragraph 3.69);

- recovery (see from paragraph 4.24);

- frontline performance (see from paragraph 3.18); and

- advanced analytics (see from paragraph 4.5).

Lodge and Pay Reset

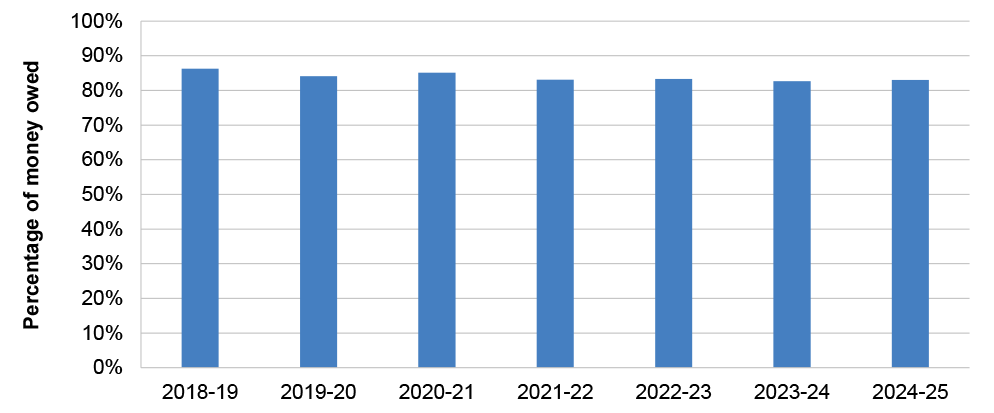

3.8 The ATO commenced a Lodge and Pay (LAP) Reset from September 2023.68 The purpose of the reset was to return to business-as-usual debt recovery actions after the ‘help and assist’ posture the ATO adopted during the COVID-19 pandemic ‘normalised into poor payment behaviours.’ The ATO adopted a firmer posture in response to the rapidly growing debt book and declining payment culture. The ATO developed a three-phase strategic communication approach. This was aligned with OECD Successful Tax Debt Management: Measuring Maturity and Supporting Change (Successful Tax Debt Management)69 strategic principle one.70 Phases one and two of this approach ended in 2023, and phase three commenced in 2024.71