Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 36 of 2025–26

Australian National University Financial Management

Published

Thursday 4 June 2026

Portfolio

Education

Entity

Australian National University

Contact

Please direct enquiries through our contact page.

Audit snapshot

Why did we do this report?

- Under the Higher Education Standards Framework (Threshold Standards) 2021, Australian universities are required to be financially sustainable.

- Sustainable financial management allows universities to support quality teaching and research.

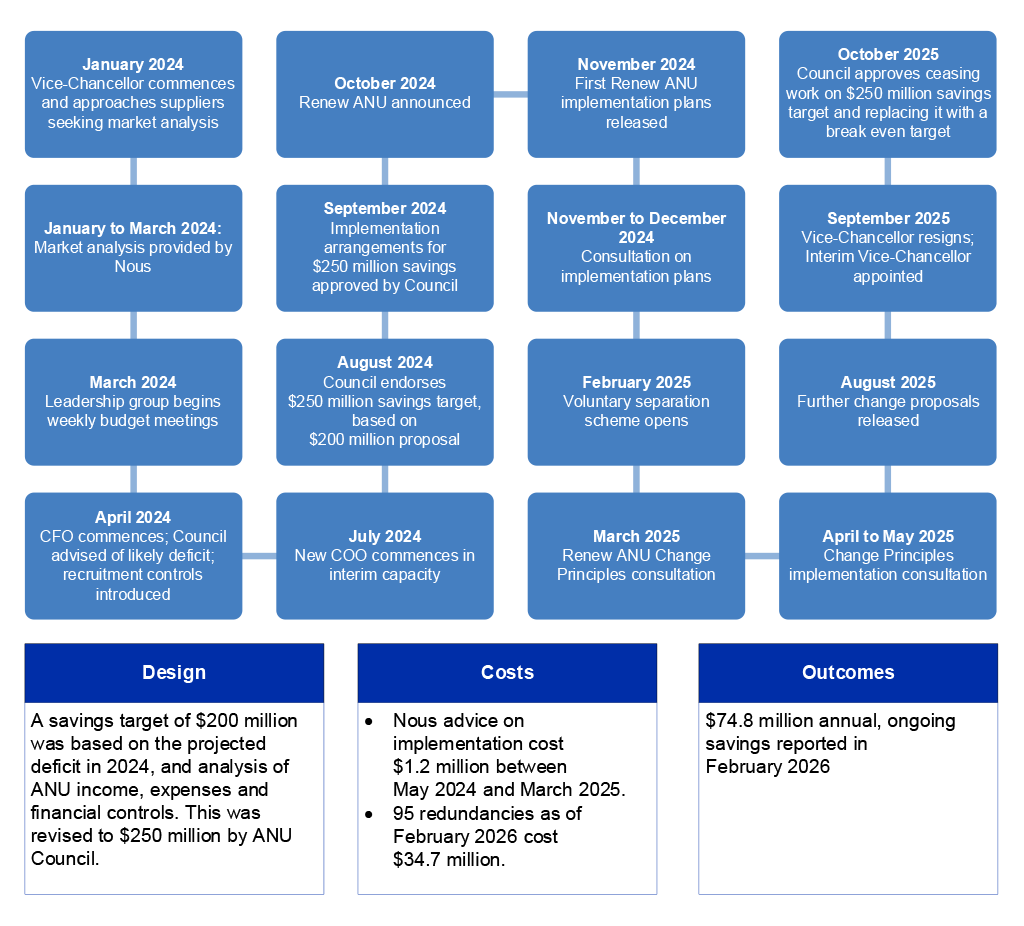

- In October 2024, the Australian National University (ANU) commenced implementation of Renew ANU, to restructure the university and reduce ANU’s annual operating budget by $250 million (16.5 per cent of total 2024 expenditure) by January 2026.

Key facts

- The ANU’s Accountable Authority under the Public Governance, Performance and Accountability Act 2013 is the ANU Council.

- The ANU Council is made up of the Chancellor (Chair), Vice-Chancellor, seven members appointed by the Education Minister, and six members representative of staff and students.

- The ANU Council is responsible for promoting the university’s purposes, financial sustainability, and proper use and management of public resources.

What did we find?

- The Renew ANU savings target was approved by ANU Council in August 2024 without sufficient understanding of the problem, the options available, or implementation risks.

- ANU Council approved the $250 million savings target without clear evidence it was needed, achievable, urgently required, or likely to have the intended impact.

- Council’s decision-making should have considered additional information, options, and perspectives.

Key messages

- Where an Accountable Authority is a collective decision-making body, operating protocols should ensure major change plans are subject to appropriate scrutiny before approval, including the evidence base, alternative options, feedback from meaningful consultation with those directly affected, and risks.

- The preparation of non-audited financial information should be based on an approved methodology and oversight.

- Council members should seek further information or assurance from management where targets are not met.

$74.8m

Annual salary savings reported as part of Renew ANU, as of February 2026.

$35.9m

Cost of Renew ANU as of February 2026.

$116.3m

Audited net operating result reported by ANU for 2025.

Guide to this report

Scope

1. The ANAO examined Australian National University (ANU) financial management, with a focus on Renew ANU — a cost saving and restructuring initiative announced by ANU in October 2024. Renew ANU aimed to achieve financial sustainability by January 2026 via:

- $100 million annual, ongoing savings from staffing expenses, including restructuring academic colleges, and reducing the number of colleges from seven to six.1

- $150 million annual, ongoing savings from non-salary expenses to be identified by an Expenditure Taskforce led by the Chief Operating Officer.

2. The ANAO addressed the following questions:

- What were the financial pressures and conditions that led to Renew ANU?

- What actions has ANU taken to address the financial pressures and conditions that led to Renew ANU?

Purpose

3. The Auditor-General is the ANU’s external auditor for its financial statements, with the audit opinion providing reasonable assurance that the financial statements present fairly the financial position and financial performance of the ANU.2 A separate financial statements audit report is provided each year in respect of the ANU’s financial statements.

4. In light of parliamentary and public interest in Renew ANU, analysis was conducted alongside the ANAO’s audit of the ANU’s 2025 financial statements. This report, tabled under section 25 of the Auditor-General Act 1997, consolidates independent analysis that provides transparency to the Parliament with respect to ANU’s financial management, and makes findings and recommendations where appropriate.

5. In preparing this report, the ANAO has conducted the same procedures to collect and corroborate evidence as we would use in a performance audit and has applied the same level of professional scepticism in analysing that evidence. The report presents facts and findings based on evidence.

Previous audits and reviews

6. While this report is distinguished by its focus on financial management, it contributes to a growing literature on university governance. Two previous ANAO performance audits have considered ANU:

- Auditor-General Report No. 11 2021–22 Australian National University’s Governance and Control Framework found the governance and control framework of the ANU was largely effective, except for deficiencies in systems of control and accountability, which were in the process of being remedied at the time of the audit.3

- Auditor-General Report No. 30 1996–97 Australian National University Administration found ANU had financial and control frameworks to assist the day-to-day administration of the university’s activities, including an appropriate three-year budget process, policies and procedures, and a sound internal review process, but that effectiveness could be improved in a range of areas including strategic and operational planning, performance information, and internal audit.4

7. Concern about the financial sustainability of higher education is common across Organisation for Economic Co-operation and Development countries, due to constraints on public finances, fewer young people leading to reduced growth in demand, and changing patterns of international mobility, geopolitical tensions and shifts in domestic immigration policies limiting income from international student fees.5 In Australia, recent work includes:

- the Australian Government Expert Council on University Governance, which recommended the adoption of a set of governance principles through annual reporting monitored by the higher education regulator, the Tertiary Education Quality and Standards Agency (TEQSA)6;

- the Parliamentary Inquiry into the quality of governance at Australian higher education providers, which recommended wide-ranging changes to university governance, including changes to TEQSA’s advice, monitoring, and reporting requirements in relation to university governance7;

- university-specific analysis8; and

- analysis by state and territory government audit offices, in whose remit all Australian universities except ANU fall.9

Key concepts

8. Under the Higher Education Standards Framework (Threshold Standards) 2021, a registered higher education provider is required to have the ability to manage their resources to support quality operations in both the short-term (financial viability) and over the longer-term (financial sustainability).10

9. Financial management involves systems and processes to achieve financial viability and sustainability, including budgeting, forecasting, internal controls, risk management, financial reporting, and performance monitoring to achieve an entity’s purpose.11 The Public Governance, Performance and Accountability Act 2013 (PGPA Act), requires public resources to be managed in an efficient, effective, economical and ethical manner, with care and due diligence (see paragraphs 1.4 and 1.7).

10. Financial performance is how well an entity uses its resources in achieving its purpose. It is generally measured using financial statements (operating result, balance sheet, and cash flow) and metrics like profit margin, revenue growth, assets to liabilities, and capital turnover.12 To effectively manage resources, universities must generate revenue and manage expenses to maintain appropriate levels of net assets and cash flows, without reducing essential services or borrowing money to fund sustained operational deficits.13

11. Australian Government entity financial statements are prepared in accordance with the Australian Accounting Standards, to record an entity’s financial activity, performance, and position over a specified reporting period. They are the means by which the entity’s Accountable Authority and Chief Financial Officer discharge their financial accountability responsibilities under the PGPA Act.

12. There are no Australian Government performance targets or benchmarks that could be used to assess entity financial management. In 2018–19, the Department of Finance established a portal which includes tools and guidance on financial ratios, which allow Australian Government entities to compare their performance. However, performance targets or benchmarks to assist users to understand whether these ratios indicate strong or weak financial performance have not been developed.14 The ANAO considers that there would be benefit in the Australian Government developing performance targets or benchmarks on financial sustainability.15 University performance against a selection of key performance indicators is provided at Appendix 4. Indicators are drawn from Department of Finance as well as Universities Australia, to ensure the information provided is appropriate to the Australian public university sector.

Methodology

13. This work drew on meetings with current and former ANU staff and Council members, sector experts, relevant Australian Government entities, review of ANU documents, analysis of ANU and publicly available data, and the ANAO’s financial statements audit work. As detailed in paragraph 5, the ANAO has conducted the same procedures to collect and corroborate evidence as we would use in a performance audit and has applied the same level of professional scepticism in analysing that evidence.

14. The report was produced at a cost to the ANAO of approximately $334,202.

15. The team members for this report were Hazel Ferguson, Renae Lowden, Kayla Lu, Lewis Passarelli, Rahul Tejani, and David Tellis.

16. Fieldwork was conducted between September 2025 and January 2026, with analysis focusing on the period from 2020 to 2025.

Summary of entity response

17. The proposed report was provided to ANU, TEQSA, and the Department of Education. The ANU provided a formal response. The ANU summary response is reproduced below and the full response is at Appendix 1.

Australian National University summary response

ANU Council thanks the ANAO for its recommendations, all of which have been accepted, and recognises the opportunity they provide to strengthen governance, financial advice and reporting practices.

Council acknowledges that documentation provided to it could have more clearly articulated the problem, options, risks and impacts in a single, integrated narrative, including both financial and non-financial considerations. However, Council does not accept the characterisation that the Renew ANU savings target was approved without an understanding of the nature, scale or urgency of the financial challenge.

Financial pressures developed over an extended period, reflecting structural changes in the University’s revenue and cost base, including sustained declines in government funding and volatility in student revenue, as noted in the ANAO report. These pressures were identified as early as 2023, with increasing scrutiny of cash flow, revenue sustainability and the cost base. By mid-2024, the scale and trajectory of the problem was clear.

The program was developed in a dynamic environment, with analysis, options, risks and impacts refined iteratively through engagement between the executive and Council, and subject to ongoing governance and oversight following approval.

Council acknowledges that consultation processes, articulation of non-financial risks, and consideration of community impacts should be strengthened. We commit to these actions which will further support ANU’s financial sustainability and governance, providing a clear platform for the University’s next Strategy.

ANAO comment on ANU’s summary response

18. In undertaking their PGPA Act duties as the Accountable Authority for the university, each ANU Council member is required to exercise the degree of care and diligence that a reasonable person would in the circumstances.16 In the case of decision-making with significant impacts, such as Renew ANU, members ‘should exercise more caution to inform themselves of all the circumstances to make a reasonable decision’.17

19. The specific circumstances detailed in this report show ANU Council members could not have relied on information provided over time to properly consider what became known as Renew ANU (see paragraphs 4.1 to 4.31). This is because:

- Information provided lacked key elements, including feedback from meaningful consultation with staff and students, and analysis to demonstrate that the $250 million savings target was both necessary, and achievable.

- As a multi-member accountable authority, sustained engagement with decision-making over time is affected by changes in membership. 22 ANU Council members either commenced or ceased between October 2023, when Council was advised ANU was not on track to break even by 2026, and October 2025, when the savings target was removed. Evidence of key decisions, supporting analysis and the rationale for choices made was lacking. Without sufficient documented evidence, continuity of understanding to support proper consideration of decisions cannot be sustained over a multi-year period during which membership changed.

Summary and recommendations

Executive summary

1. ANU’s key income is not keeping up with its costs without supplementation from other income sources.

Growth in Australian Government funding and student fees has slowed in recent years, and since 2018 they have not been enough to cover ANU’s expenses without supplementation from other income sources. This gap has been approximately 25 per cent since 2020, although there was some improvement in 2021 (to 12.0 per cent) and 2025 (to 20.3 per cent), due to declining expenses.

2. ANU’s long-term sustainability does require active management, but it is not in immediate financial crisis.

ANU still shows strong overall financial health on measures like audited net operating results, credit ratings and net assets. However, a trend of declining average five year surpluses raises questions about whether the current financial model is sustainable over the longer term.

3. Financial pressures built up between 2020 and 2024 due to optimistic revenue assumptions and limited spending control.

After a $317 million surplus in 2019, revenue fell sharply in 2020. ANU had some success in reducing spending and relied on investment income, which it determined was not sustainable. ANU forecasts were consistently incorrect as they related to international student numbers, indicating insufficient alignment between student recruitment and financial planning.

4. The ANU Council approved the $250 million Renew ANU savings target (16.5 per cent of total 2024 expenditure) without clear evidence it was needed, achievable, urgently required, or likely to have the intended impact.

The ANU Council approved Renew ANU without a clear understanding of the problem, the options available, implementation risks, or the expected impact of the program on the university’s purpose, financial sustainability, and people. Council’s decision-making should have considered additional information, options, and perspectives, including alternative ways to address identified financial problems across the university’s balance sheet (such as using one or more of revenue measures, borrowing, or the use of investment assets and/or investment income, in combination with savings efforts, to allow for a longer transition timeframe).

5. The Renew ANU program has delivered some savings, but with significant risks.

While some savings have been made from the implementation of Renew ANU, as of February 2026, the program has cost $35.9 million against reported annual salary savings of $74.8 million, and major risks remain — particularly around staff impacts and reliance on future growth in international student numbers, which has historically taken longer than planned.

Recommendations

Recommendation no. 1

The Australian National University formally capture and apply lessons learned from Renew ANU to future proposals involving major financial or organisational change, to ensure such proposals are supported by a documented business case that clearly sets out:

- the problem to be addressed;

- realistic, evidence-based options;

- implementation risks and dependencies;

- the expected impact on the university’s purpose, financial sustainability, and people; and

- oversight and reporting arrangements.

This information should be provided to Council prior to approval, to enable informed and robust decision-making.

Australian National University response: Agreed.

ANU agrees with the recommendation to strengthen how analysis, options, risks, and impacts are documented and presented in a structured business case format. Council considers that a body of analysis informed its deliberations, and that this recommendation appropriately focuses on improving how that material is consolidated and presented to support decision-making.

Recommendation no. 2

The Australian National University enhance the quality of financial advice and reporting to Council and its committees to ensure it is readily understood by its membership, including by:

- explaining the university’s full financial position, including audited net operating results, cash flows and liquidity, and assets, liabilities and investment funds;

- explaining the interaction between operating decisions and financial performance, including trend and trajectory analysis, reasons for any variance from budget, and longer term risks to financial sustainability; and

- commissioning independent assurance as to the effectiveness of financial control improvements introduced since 2020.

Reliance on income and expenditure measures alone should be avoided.

Australian National University response: Agreed.

Recommendation no. 3

The Australian National University establish and approve a documented methodology for the calculation and use of non-audited financial measures (including the underlying operating result and management operating result), including:

- clear definitions and permitted adjustments;

- reconciliation to audited financial statements; and

- consistent use in internal reporting and decision-making.

Council reporting should clearly identify which measure is being used and why.

Australian National University response: Agreed.

6. Implementation of these recommendations will be tracked as part of the ANAO’s financial statement audit work of ANU.

1. Background

The Australian National University

1.1 The Australian National University (ANU) is responsible for ‘undertaking research and teaching of the highest quality’.18 It is the only Australian university established under Commonwealth legislation, and has both ‘national and international roles’.19

1.2 In the 2025 calendar year (ANU financial reporting is by calendar year), ANU employed 4,644 people (measured in full time equivalent staff, or FTE), enrolled 16,960 students (measured in equivalent full time student load, or EFTSL), and generated $1.6 billion revenue against $1.5 billion operating expenses. In addition to its main campus in Canberra, Australian Capital Territory, the university maintains five other sites across Australia.20 As of 31 December 2025, its assets were valued at $5.7 billion.

Governance

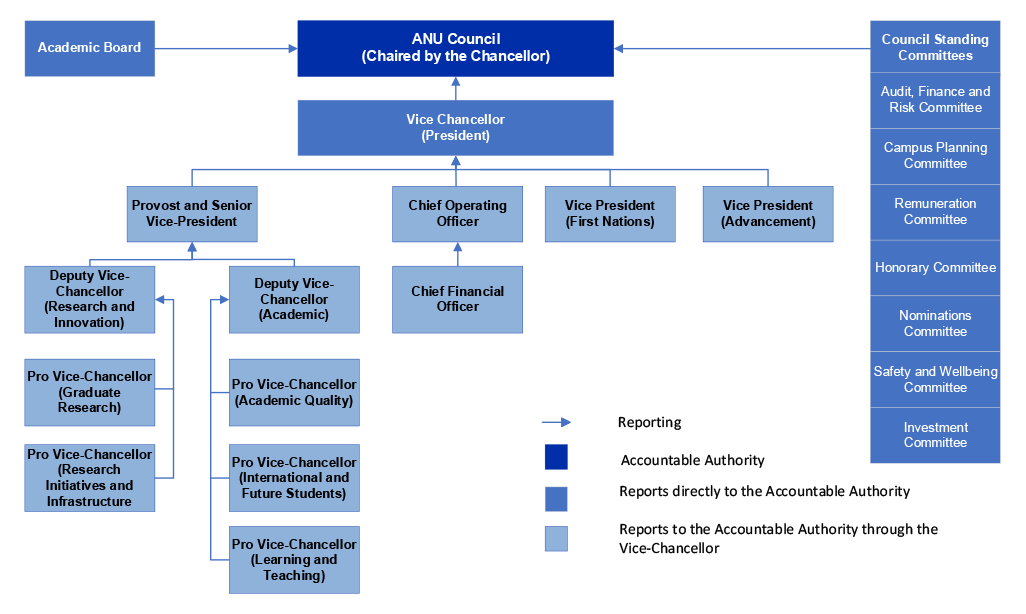

1.3 ANU’s governance structure is outlined in Figure 1.1. Broadly, there are three elements of Australian university governance:

- the university council, responsible for oversight of the university’s purpose, financial sustainability, legal obligations, risk frameworks, and overall delivery of outcomes;

- the academic board, responsible for maintaining academic excellence, and managing academic matters of the university; and

- the university executive, led by the Vice-Chancellor, responsible for the day-to-day operational management of the university.21

1.4 The Australian National University Act 1991 (ANU Act) provides the Council has ‘the entire control and management of the University’.22 As the governing body of a Commonwealth entity, the ANU Council is the Accountable Authority under the Public Governance, Performance and Accountability Act 2013 (PGPA Act). This means it is responsible for leading, governing and setting the strategic direction for the university, and promoting the university’s purposes, financial sustainability, and proper use and management of public resources.23 This includes establishing and maintaining appropriate systems of risk oversight and management, and internal controls for the entity.24

Figure 1.1: ANU governance structurea as of March 2026b

Note a: Academic Board is tasked with ensuring the University maintains the highest standards in teaching, scholarship and research. It consists of the Chair, Vice-Chancellor, Deputy Vice-Chancellors, Pro Vice-Chancellors, the head of Student Administration and Academic Services (University Registrar), the Dean of Each ANU College, the Dean of Students, the Vice-President, First Nations, the University Librarian, and at least 28 other members representative of academic and professional staff and students.

Note b: At the time of finalising this report (May 2026), a Special Governance Committee of Council was in place, with responsibility for the ANU’s response to ‘matters raised in the Senate Committee hearing on 12 August 2025’. The Special Governance Committee was established for a period of 12 months and therefore has not been included in this figure as a Council Standing Committee.

Source: ANAO based on ANU documents.

1.5 As a Corporate Commonwealth entity, ANU is legally separate from the Commonwealth, meaning that the Accountable Authority is not directly responsible to the executive.25 While the Prime Minister has the power to appoint and remove departmental secretaries under the Public Service Act 1999, the ANU Act provides that Council members’ legal accountability is to the Council itself, and the university.26 Under the ANU Act, once appointed, members may resign, are disqualified if they cease to be eligible to be a member of Council, or can be removed by resolution if Council forms the view that a member is unable to perform their duties or has breached their obligations.27 The ANU Council is also responsible for appointing and terminating the Chancellor and Vice-Chancellor of ANU, and determines the duration and conditions of these appointments.28

1.6 There is no external authority with legal power to direct or remove the ANU Council, but its operations can be affected by:

- the Education Minister’s appointment of seven of the 14 members29;

- the Finance Minister’s determination of the university’s borrowing limit30; and

- the higher education regulator, the Tertiary Education Quality and Standards Agency (TEQSA), which registers ANU as an Australian university and has discretion to impose conditions on registration, which could extend to imposing conditions impacting the functions of ANU Council.31

1.7 ANU Council members are required to exercise the degree of care and diligence that a reasonable person would in the circumstances, and act honestly, in good faith, and for proper purpose.32 They must ensure they regularly monitor and understand financial position, financial performance, and cash flow information, and obtain and use such ‘information and advice … as is necessary for informed and competent decision making and direction setting’.33 The Expert Council on University Governance — Final Report and Principles emphasises the need for ‘genuine inquisitiveness’, while ANAO performance audits of public sector boards have found board members should actively question and challenge management.34 These requirements are similar to expectations in other sectors. The board of directors of a company or not-for-profit must also exercise care and due diligence.35

1.8 The ANU Council is a collective decision-making body which affords the Chair and each member equal votes. The operational arrangements for ANU Council are detailed in Appendix 2.

2. Operating environment

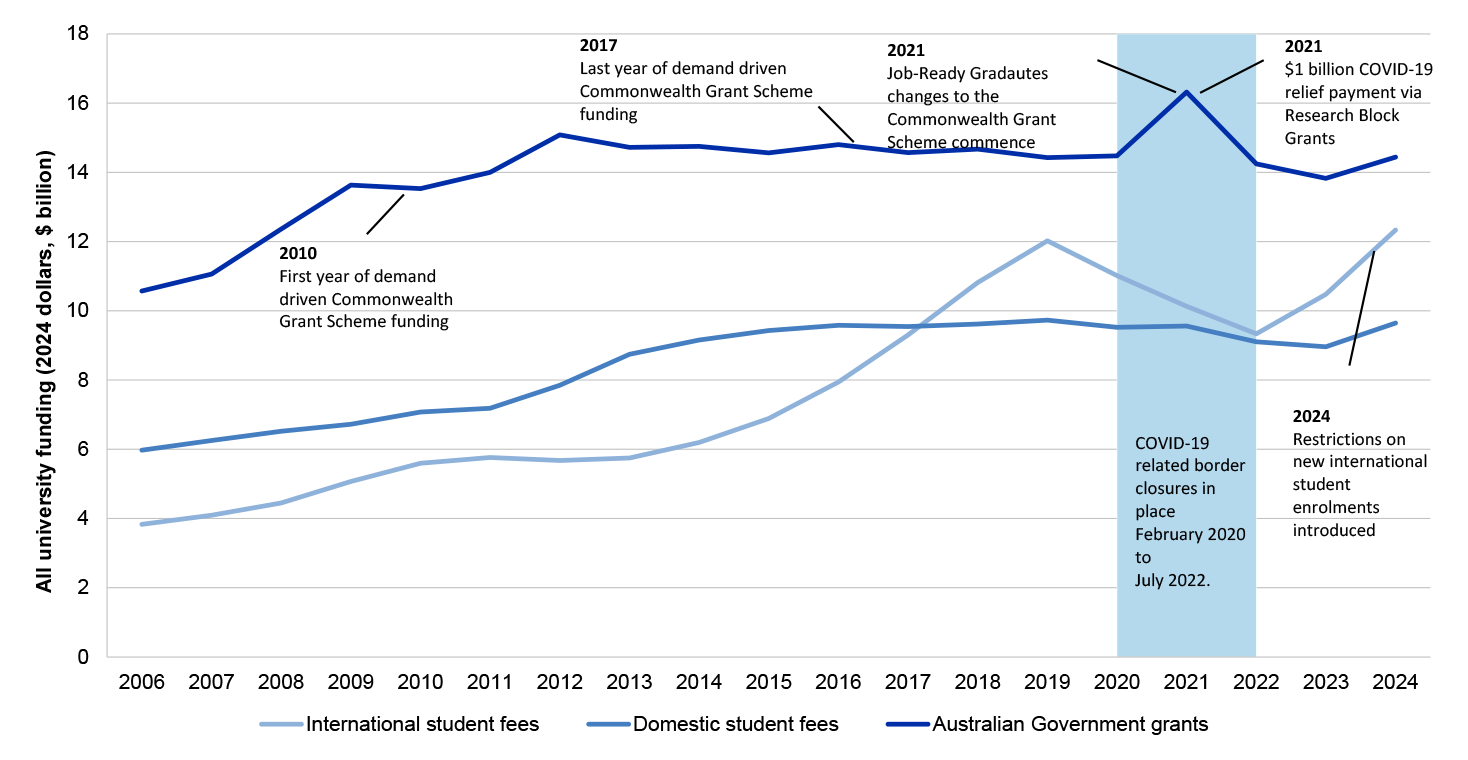

All Australian university income is primarily from Australian Government grants for teaching and research, and student fees. A range of policy and market changes since 2006 have resulted in revenue growth from these sources slowing for all universities — growth was 51.5 per cent in real terms between 2006 and 2015, and 12.6 per cent in real terms between 2016 and 2024.

For ANU, these income sources have not been sufficient to cover expenses since 2018, and the gap between total expenses and total key income has been approximately 25 per cent since 2020, although there was some improvement in 2021 (to 12.0 per cent) and 2025 (to 20.3 per cent), due to declining expenses.

Despite this, measures of financial performance for the university (including audited net operating results, credit ratings, and asset balance) have remained robust. ANAO analysis of ANU’s average audited net operating results from 2020 to 2025 indicates large but declining average surpluses, with some improvement in 2025. This means ANU is not at immediate financial risk, but it should raise financial sustainability questions for ANU requiring active management.

Australian higher education funding is primarily from Australian Government grants for teaching and research, and student fees

2.1 Australia’s higher education system provides education for approximately 1.7 million students (in 2024, up from 1.6 million in 2020) via 217 higher education providers, including 44 universities (up from 178 providers, including 42 universities, in 2020).36

2.2 The sector is regulated by the Tertiary Education Quality and Standards Agency (TEQSA). Australian universities are required to undertake teaching and research, and offer doctoral research degrees, as conditions of registration with TEQSA.37 Australian Government funding is administered by the Department of Education (Education), and is subject to registration with TEQSA, and conditions in the Higher Education Support Act 2003 (HESA).38

2.3 University income is primarily received from Australian Government grants for teaching and research, and student fees.39 Total university revenue from these sources grew by 51.5 per cent in real terms between 2006 and 2015, and by 12.6 per cent in real terms between 2016 and 2024 (Figure 2.1).

Figure 2.1: All university revenue from Australian Government grantsa and student fees, 2006 to 2024 (2024 dollars)

Note a: Australian Government grants include subsidies for domestic students through the Commonwealth Grant Scheme, research grants, and the National Institutes Grant. Domestic student fees include upfront student payments and student contributions, and advances on student loans by the Australian Government, and international student fees do not have any sub-components.

Source: ANAO analysis of Department of Education data.

Australian Government funding for learning and teaching is predominantly via the Commonwealth Grant Scheme

2.4 The largest component of Australian Government grants for universities is from the Commonwealth Grant Scheme (CGS), which subsidises course fees for eligible students (predominantly domestic undergraduates).40 CGS funding in the 2025–26 Budget was an estimated $8.4 billion in 2025–26.41

2.5 A subsidised place funded through the CGS is known as a Commonwealth supported place (CSP). Universities receive two payments for each CSP: a Commonwealth contribution, paid by the Australian Government through the CGS, and a student contribution, paid by the student, usually using an Australian Government student loan.42 Maximum Commonwealth contribution and student contribution amounts are set in HESA, and vary according to field of study.43 International students, and most domestic postgraduate students, are not eligible for CSPs.

2.6 The major variations in Australian Government funding for universities attributable to the CGS between 2006 and 2025 were:

- CGS funding was demand driven from 2010 to 2017, leading to growth in university funding and student numbers.44

- For most courses, CGS funding was capped from 2018 to 2025, but universities were allowed to enrol ‘unfunded’ students above the funding cap (for whom they received only the student contribution amount).45

- Average per student CGS funding was reduced from January 2021 under the Job Ready Graduates package.46

2.7 Further changes to the CGS commenced from 2026, when the ‘managed growth’ system began the process of capping student numbers, ending the practice of enrolling ‘unfunded’ students.47

2.8 Other grants are also made under HESA to higher education providers to support learning and teaching priorities.48

Australian Government funding for university research comes from a large number of different programs

2.9 The largest Australian Government research grants, the Research Support Program (RSP) and Research Training Program (RTP), referred to collectively as the research block grants (RBG), provide funding support for research and research training. 49 RBG funding in the 2025–26 Budget was an estimated $2.4 billion in 2025–26.50

2.10 RBG funding is allocated to each university based on research and development income and higher degree by research student completions.51 The major variation in Australian Government funding for universities attributable to the RBGs was in 2021, when the Government made a one-off $1.0 billion COVID-19 relief payment via the RSP.52

2.11 In addition to RBG funding, Australian universities also compete for access to nationally competitive grants (also referred to as ‘category 1’ funding), mainly from the National Health and Medical Research Council (NHMRC), the Australian Research Council (ARC), and the Medical Research Future Fund (MRFF). While these grants are awarded to the university, they are generally to support a specific researcher or group of researchers to complete a project. This means in some cases nationally competitive grants can move from one university to another if the lead researcher changes employers. Other Australian Government research grants support areas of investment need, such as research infrastructure and industry engagement.53

2.12 Some universities also receive other public sector research funding (also referred to as ‘category 2’ funding) that is not awarded on a nationally competitive basis, such as National Institutes Grants. The ANU is the majority recipient of National Institutes Grant funding, receiving 90.6 per cent of the total funding pool of $272.9 million in 2025, in recognition of the role the university plays in facilitating activities of national significance.

2.13 Some universities also receive Cooperative Research Centres (CRC) funding, which is for research application which links industry with government (‘category 4’ research funding) and research funding direct from industry and other non-government bodies (‘category 3’ research funding).

The major non-government source of income for Australian universities is full fee-paying students, predominantly international students

2.14 The major non-government source of income for Australian universities is full fee-paying students, predominantly international students. These fees are set by each institution according to market conditions and provide opportunities for revenue growth.

2.15 As shown in Figure 2.1, revenue from this source grew strongly to 2019, then fell from 2020 due to COVID-19 related border closures, reaching its lowest point in 2022. While overall sector income from this source grew again in 2023 and 2024, restrictions on international student enrolment growth were introduced in 2023 for 2024.54

Australian Government funding for ANU fell 24.4 per cent in real terms between 2006 and 2024 while other sources of income have grown

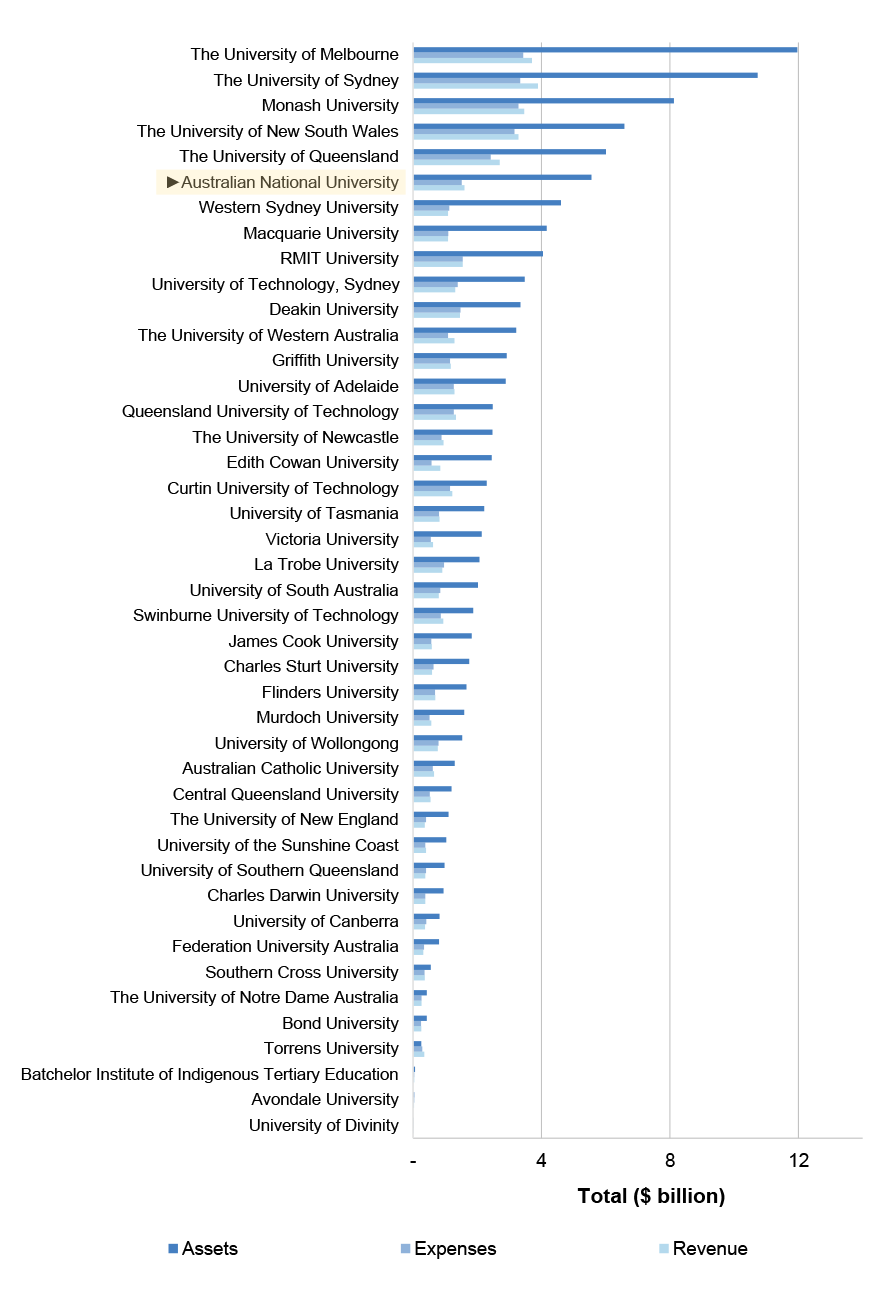

ANU’s reported total assets were sixth highest among Australian universities in 2024

2.16 The ANU, like other Australian universities, is a large not-for-profit enterprise, with annual revenue and expenses, and combined assets, in the billions of dollars (Figure 2.2).55 In 2024 (latest available comparative data), its reported total assets were sixth highest among Australian universities, despite being in the bottom half of universities in terms of student numbers (in 2024 ANU was the 27th largest Australian university based on student numbers, less than a quarter the size of the university with the largest student cohort, Monash University).

2.17 In 2024 (the comparison year in Figure 2.2) 92.3 per cent of ANU’s total assets were:

- property plant and equipment (PP&E), such as construction in progress, land, and buildings, which was valued at a total of $3.6 billion; and

- financial assets, which were valued at $1.5 billion (of which $1.4 billion was held in a ‘Long Term Investment Pool’ (LTIP)).

2.18 The ANU holds most of its financial assets in a LTIP, which includes domestic and overseas equity funds, infrastructure, term deposits, and government bonds. In 2024, the majority of the LTIP (72 per cent) was invested in equities (shares that could be sold) or term deposits (which funds can be withdrawn from, subject to interest penalties and fees), or held in cash. In practice, much of the LTIP is treated by ANU as ‘restricted’, because it is held to meet the cost of ANU’s Commonwealth Superannuation Scheme (CSS) liability, or it is from donations and bequests for scholarships, prizes, foundations and endowments. In 2024, $459.7 million (30.9 per cent) of ANU’s investment assets were unrestricted (paragraphs 3.14 to 3.15). Separately, ANU maintains a general cash float (paragraph 4.13).

2.19 Between 2016 and 2024, the ANU’s current assets exceeded its liabilities by more than double. Classification as a current or non-current asset is prescribed by Australian Accounting Standards. Current assets are those that are expected to be realised within 12 months or, in the case of investments, where the intent is that they are held for trading. As a result, this classification may not always reflect the actual ability to liquidate the asset to meet an entity’s obligations within a year. In 2025, ANU reclassified a portion of its investment assets from current to non-current. This reclassification rectified an error in the application of the requirements of the Australian Accounting Standards in prior years to accurately reflect the ANU’s investment policy that its investment pool is not held for trading and is managed on a long term basis. The reclassification does not change the fact that the majority of the assets are such that they could be readily realised to meet financial obligations, if required.

Figure 2.2: Australian university total assetsa, revenue and expenses, 2024

Note a: This chart is ranked by assets. Among Australian universities, ANU is sixth largest when ranked by assets, sixth largest when ranked by revenue, seventh largest when ranked by expenses, and 27th largest when ranked by student numbers.

Source: ANAO based on Department of Education data.

The ANU identifies its key income sources as Australian Government grants and student fees

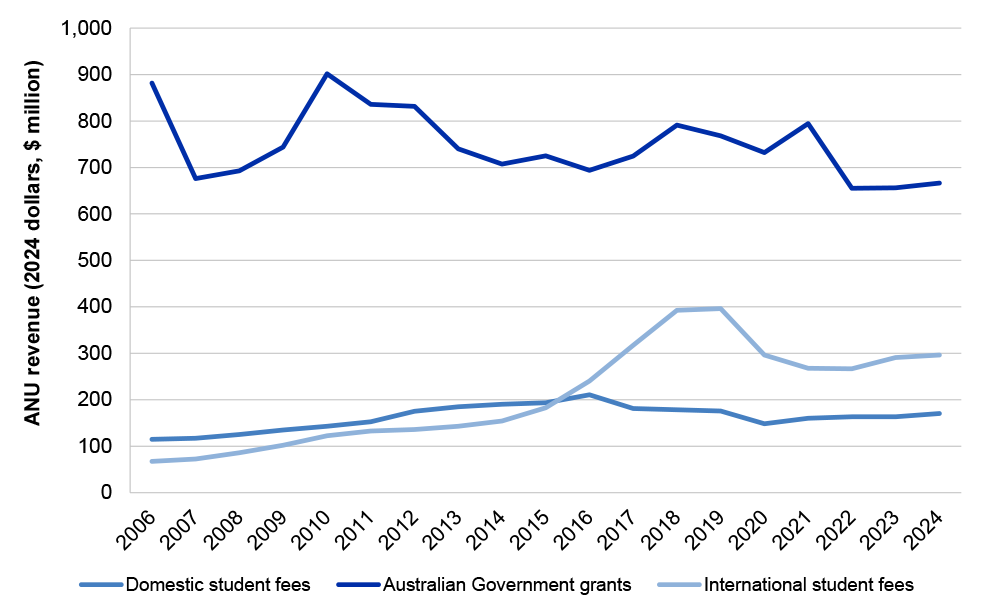

2.20 The ANU identifies its ‘key’ income sources as: Australian Government grants (including the National Institutes Grant) and student fees. While sector-wide income from these sources has grown by 78.7 per cent in real terms since 2006 (Figure 2.1), ANU income from these sources has grown by 6.5 per cent in real terms over the same period (Figure 2.3).

Figure 2.3: ANU revenue from key income sourcesa, 2006 to 2024 (2024 dollars)

Note a: Australian Government grants include subsidies for domestic students through the Commonwealth Grant Scheme, research grants, and the National Institutes Grant. Domestic student fees include upfront student payments and student contributions, and advances on student loans by the Australian Government, and international student fees do not have any sub-components.

Source: ANAO analysis of Department of Education data.

2.21 Australian Government grants to ANU fell 24.4 per cent in real terms between 2006 and 2024, while other sources of income grew over the same period. ANU achieved growth in international and domestic student fees between 2006 and 2015 (of 171.1 and 68.5 per cent respectively). International student fee growth continued between 2016 and 2019, while domestic student fee revenue fell. In 2024, ANU’s income from international student fees had recovered slightly to 23.4 per cent higher than in 2016, while income from domestic student fees was 19.1 per cent lower.

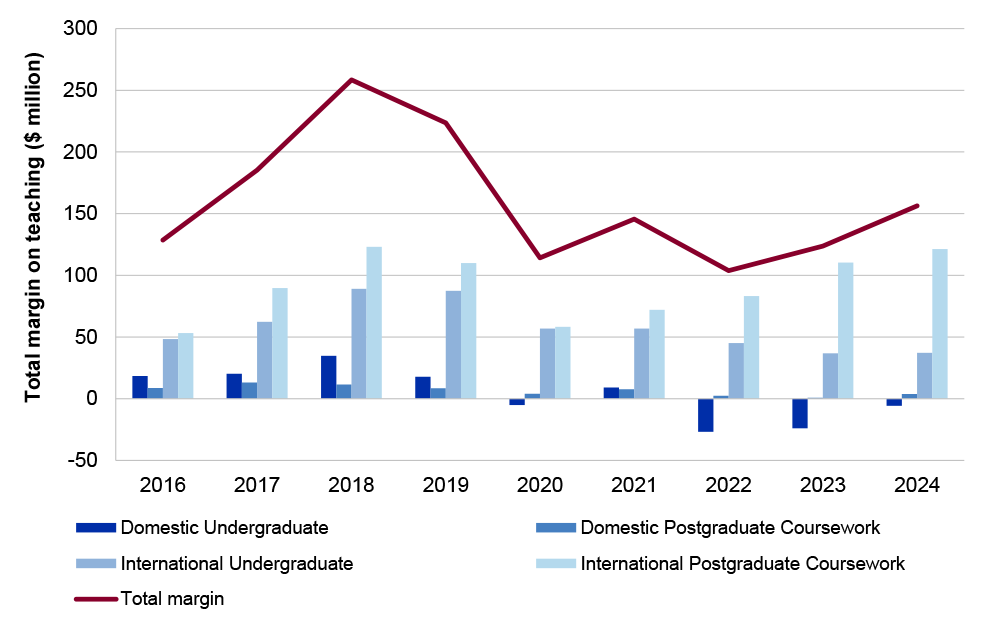

2.22 Growth in student numbers does not necessarily increase operating surplus.56 ANU has made a loss on domestic undergraduate teaching since 2022, but this is offset by strong profit margins on postgraduate and international undergraduate teaching (Figure 2.4).

Figure 2.4: ANU operating margina (EFTSL) by enrolment type, 2016 to 2024 ($ million)

Note a: Operating margin factors in teaching revenue (student fees and Australian Government grants) and direct and indirect costs of delivery, including teaching and support space utilisation, staff time, academic support services, and campus-wide overheads such as library and IT support.

Note: Data related to non-award, research, and ‘other’ study is not included in this figure.

Source: ANAO based on ANU data.

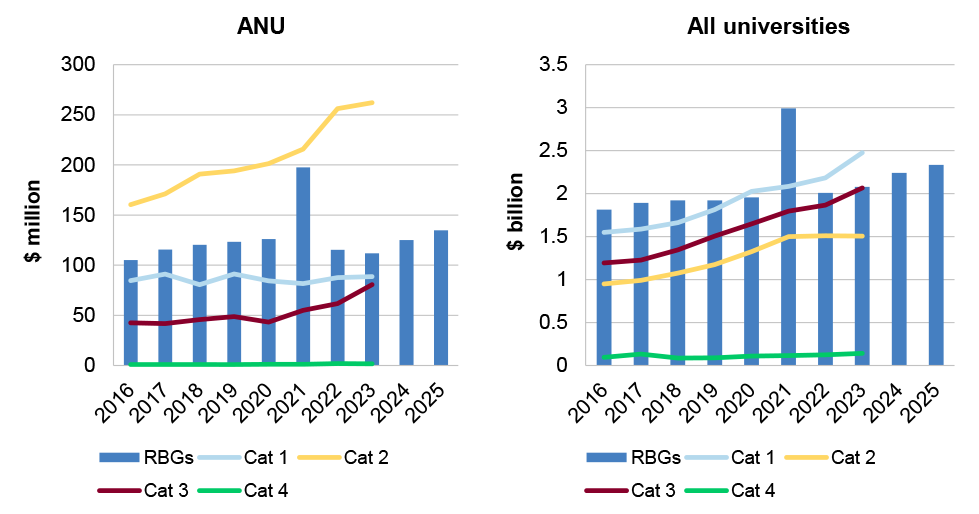

2.23 From 2016 to 2023 (latest available comparative data), the ANU increased its RBG income by 6.2 per cent, and other research income by 49.9 per cent, mainly due to growth in public sector research income outside nationally competitive programs, and industry and other research income (Figure 2.5).57 Over the same period, total university RBG funding grew by 14.6 per cent, and other research income grew by 63.5 per cent. This means ANU’s share of research funding decreased, largely driven by a decreased share of nationally competitive (category 1) research grants (from 5.5 per cent in 2016 to 3.6 per cent in 2023).58

Figure 2.5: University research income by categorya, and research block grant (RBG) allocationsb, ANU and all universities, 2016–2025c,d

Note a: For the purposes of reporting to the Department of Education, university research income is divided into four categories: Category 1: Australian competitive grants; Category 2: Other public sector; Category 3: Industry and other; and Category 4: Cooperative Research Centres.

Note b: Research block grants (RBGs) provide funding to eligible Australian higher education providers to support research and research training. RBG funding is allocated based on university research income data and higher degree by research student completions.

Note c: As of December 2025, the Higher Education Research Data Collection (HERDC) is only available up to 2023.

Note d: The 2021 increase in RBGs is due to a one-off COVID-19 relief payment made via a $71.6 million payment to the ANU (additional $1 billion across the sector) provided through the Research Support Payment.

Source: ANAO based on Department of Education data.

Australian Government grants and student fees are not sufficient to cover ANU expenses without supplementation from other income sources

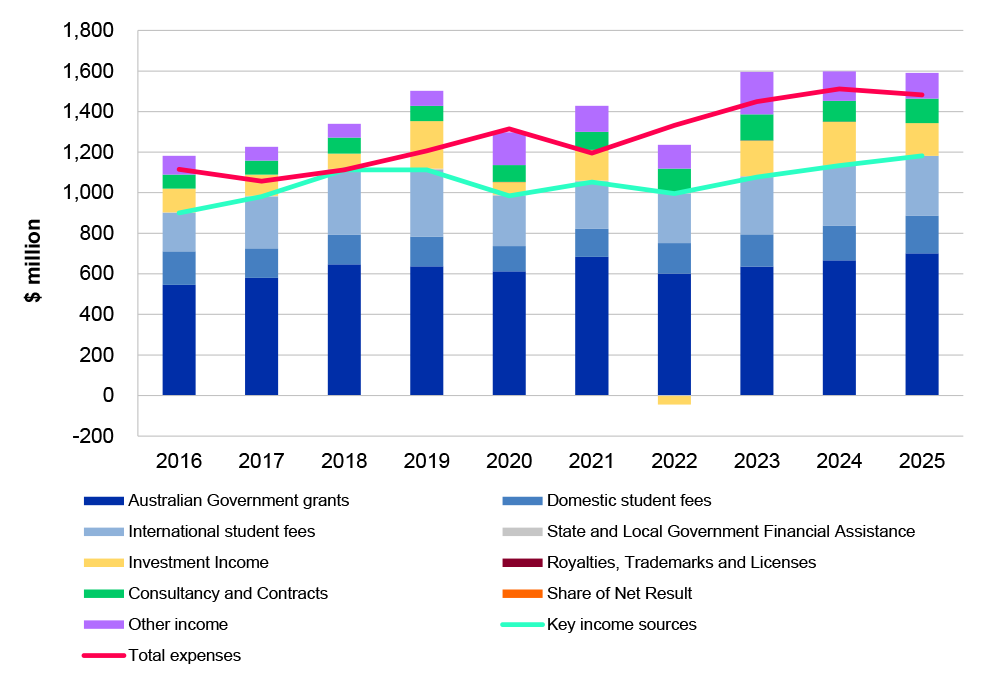

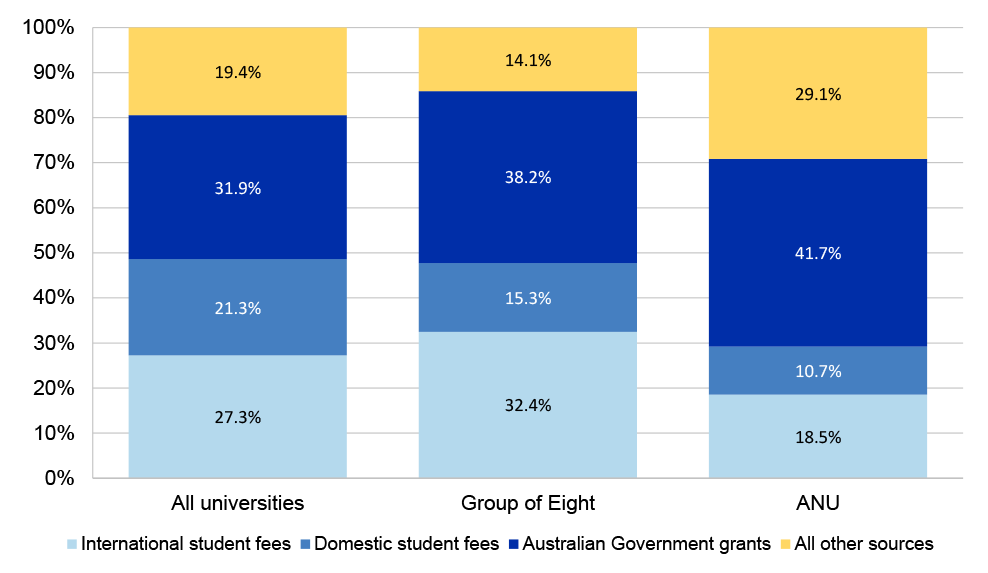

2.24 ANAO analysis shows that while ANU identifies Australian Government grants and student fees as its key income sources, these have not been sufficient to cover ANU’s expenses without supplementation from other income sources. The gap between total expenses and total key income has ranged from 25.0 to 25.7 per cent since 2020, except for improvements to 12.0 per cent in 2021, and 20.3 in 2025, due to declining expenses (Figure 2.6). This means that audited positive net operating results have usually (with the exception of 2018) relied on other income sources, such as investment income, consultancy and contracts, and other income.59 As of 2024 (latest available comparable data) ANU derives a higher proportion of its income from these sources than the sector average, or Group of Eight (Go8) research intensive universities, of which ANU is one (Figure 2.7).60 With the exception of significant declines in investment income in 2020 and 2022, which are attributable to unrealised losses in the value of financial assets (paragraph 3.13), income from these additional sources has been generally increasing.

Figure 2.6: ANU revenue by source, total of key incomea,b, and total expenditure, 2016 to 2025c

Note a: Key income includes Australian government grants (including subsidies for domestic students through the Commonwealth Grant Scheme, research grants, and the National Institutes Grant), and student fees, including domestic student fees (comprising upfront student payments and student contributions, and advances on student loans by the Australian Government) and international student fees.

Note b: Other income comprises: donations and bequests; scholarships and prizes; non-government grants; net gain on disposal of property, plant and equipment; net foreign investment gains; revenue related to service concession arrangements; and other revenue (not elsewhere classified).

Note c: The 2021 increase in Australian Government grants is due to a one-off COVID-19 relief payment made via the Research Support Program.

Source: ANAO analysis of Department of Education and ANU data.

Figure 2.7: Relative share of income by source of income, all universities, Group of Eight, and ANU, 2024

Source: ANAO analysis of Department of Education and ANU data.

The ANU has previously experienced and recovered from financial setbacks

2.25 Auditor-General Report No. 30 1996–97 Australian National University Administration states:

The main factors affecting current and future administrative operations of the ANU are reduced revenues and increased operating costs. The ANU is particularly dependent on the Commonwealth; with $266m or 67 per cent of all monies coming from the Commonwealth in 1995. In 1997 the funds available for teaching and research will be reduced by $30 million because:

- Commonwealth funding for universities generally, is being reduced in real terms;

- student enrolments are expected to decrease slightly. Local enrolments could fall because of increased Higher Education Contribution Scheme (HECS) charges while the University expects fewer fee paying students because of increasing competition from Australian and overseas universities; and

- operating costs have risen following an enterprise bargaining agreement negotiated late in 1996 which has led to salary increases that will not be met by increased Commonwealth funding.

As a consequence, academic, technical and administrative staffing levels are being reduced to enable the ANU to meet future budget requirements.61

ANU’s strong but declining financial position points to sustainability challenges

2.26 Financial performance is how well an entity uses its resources in achieving its purpose. Although there are no Australian Government performance targets or benchmarks setting out what good financial management looks like (paragraphs 9 to 12), financial performance is generally measured using financial statements (operating result, balance sheet, and cash flow) and metrics like profit margin, revenue growth, assets to liabilities, and capital turnover.

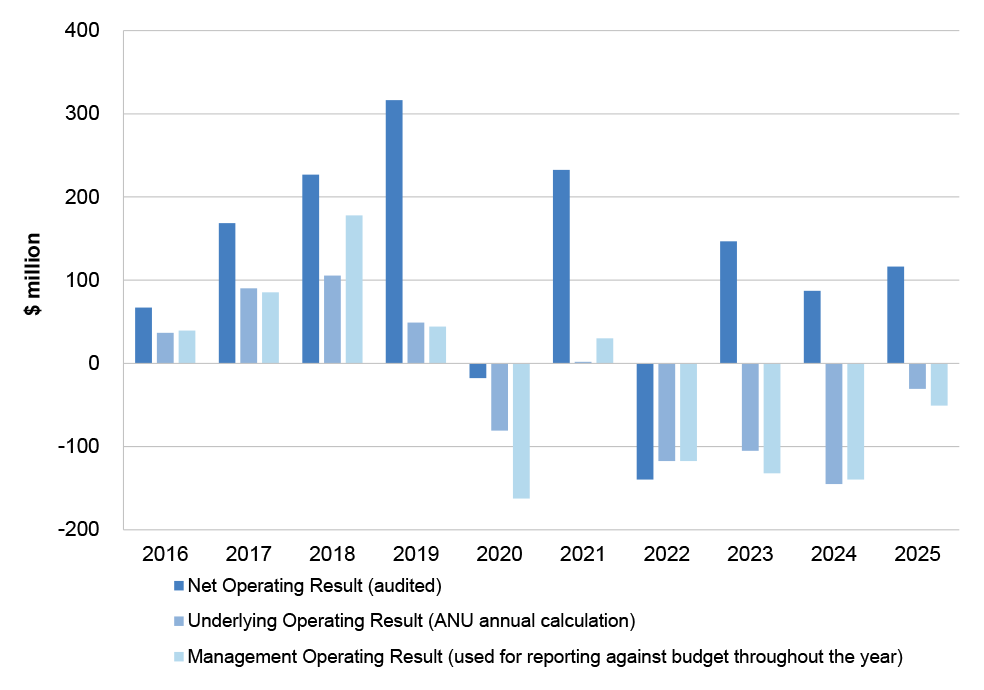

2.27 The ANU uses three measures to report on its finances (Table 2.1). Using these, ANU has reported eight audited positive net operating results and five unaudited positive underlying operating results since 2016 (Figure 2.8). The unaudited underlying operating results diverged from the audited positive net operating results in 2023, 2024, and 2025.

2.28 Year-to-year variations (as shown in Figure 2.8) are most attributable to changes in investment returns and one-off adjustments to the underlying operating result. There is no approved documented basis for one-off adjustments to ensure reporting validity or consistency.62 For example:

- in 2017, and each year from 2020 to 2024, staff separation expenses (and one year of savings in 2023) totalling $107.2 million were removed on the basis that they represent one-off restructuring costs63; and

- in 2021, $49.7 million of $71.0 million COVID-19 relief income, delivered via the ongoing RBGs, was excluded on the basis that the income was not ongoing, while the remaining amount was not excluded due to limitations in ANU’s ability to track expenditure by revenue source.

2.29 Although other Go8 universities report underlying operating result, ANU does not have assurance that other universities calculate the underlying operating result in the same way it does.

2.30 Reliance on these metrics for decision-making, in the absence of other financial information, creates risks associated with a lack of understanding of the university’s full financial position and performance. In particular, risks are that audited net operating results, cash flows and liquidity, and assets and liabilities, are not well understood by decision-makers (paragraphs 4.5 and 4.22).

Table 2.1: ANU measures of financial performance, as of December 2025

|

Measure |

Method |

Purpose |

Assurance |

|

Net operating result (audited; published in annual report) |

Net result after income tax from continuing operations, presented in accordance with the Australian Accounting Standards and rules made under the Public Governance, Performance and Accountability Act 2013 (PGPA Act). |

Prepared to meet the Accountable Authority’s responsibilities under the PGPA Act for the preparation and fair presentation of annual financial statements that comply with Australian Accounting Standards and the rules made under the PGPA Act. |

Independently audited by the ANAO. |

|

Underlying operating result (not audited; published in annual report) |

ANU adjusts its audited net operating result each year to arrive at an underlying operating result which excludes:

These adjustments are detailed in Appendix 3. |

ANU’s own adjusted measure of financial sustainability, the underlying operating result has been published in ANU annual reports since 2012. In 2015, draft advice (from Flagstaff Consulting Group) stated ANU’s financial statements should reflect its underlying financial performance and position. The underlying operating result is prepared annually, and performance against this measure is not monitored by Council during the year. |

No independent audit or assurance. The ANU documents the calculation of the underlying operating result each year in a single calculation spreadsheet. ANU has no methodology or process documentation to guide finance staff to complete this work consistently from year-to-year. This raises the risk of a lack of consistency in calculations and usage from year-to-year. |

|

Management operating result (not audited; not published) |

The management operating result is calculated monthly, and includes all revenue and expenses from continuing operations, subject to the same adjustments as the underlying operating result, except items which cannot be calculated until the end of the year (including most one-offs detailed in Appendix 3). |

Used to prepare the annual ANU budget and for regular reporting to Council and its committees. Reporting and budget documents provided to ANU Council between 2020 and 2025 did not consistently explain the reconciliation between the unaudited management operating result and audited net operating result, or specify which measure is being used. |

No independent audit or assurance. |

Note a: Investment fund expenses include borrowing costs, operational expenses of the investment office, endowment distributions and Commonwealth Superannuation Scheme (CSS) pension cost.

Source: ANAO based on ANU documents.

Figure 2.8: ANU reported net operating result, underlying operating result, and management operating result, 2016–2025a ($m)

Note a: The 2021 underlying operating result (ANU annual calculation), which is not visible in this chart, was $1.997 million.

Source: ANAO analysis of ANU data.

ANU had large net operating surpluses from 2020 to 2025, but declines between 2020 and 2024 indicate financial sustainability could be a challenge in the long term

2.31 The ANAO is ANU’s independent auditor of its financial statements. Since 2016, the ANAO has made 4 category B financial statements audit findings (poses moderate business or financial management risk to the entity) and 21 category C financial statements audit findings (poses a low business or financial management risk to the entity) (Table 2.2).64

Table 2.2: ANAO audit of ANU financial statements, 2016–2024a,b

|

|

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

|

New ANAO audit findings |

1 |

3 |

2 |

4 |

1 |

6 |

0 |

3 |

5 |

Note a: As of May 2026, the 2025 financial statements audit findings have not been finalised. These will be included in the ANAO Interim Report on Key Financial Controls of Major Entities, due to be released in June 2026.

Note b: The larger than usual number of findings in 2021 and 2024 reflect new IT findings identified, and one risk management finding. Whilst not having any risk of material misstatement for financial statements, this is a business risk.

Source: Financial Statements Audit Closing Letters 2016–2024.

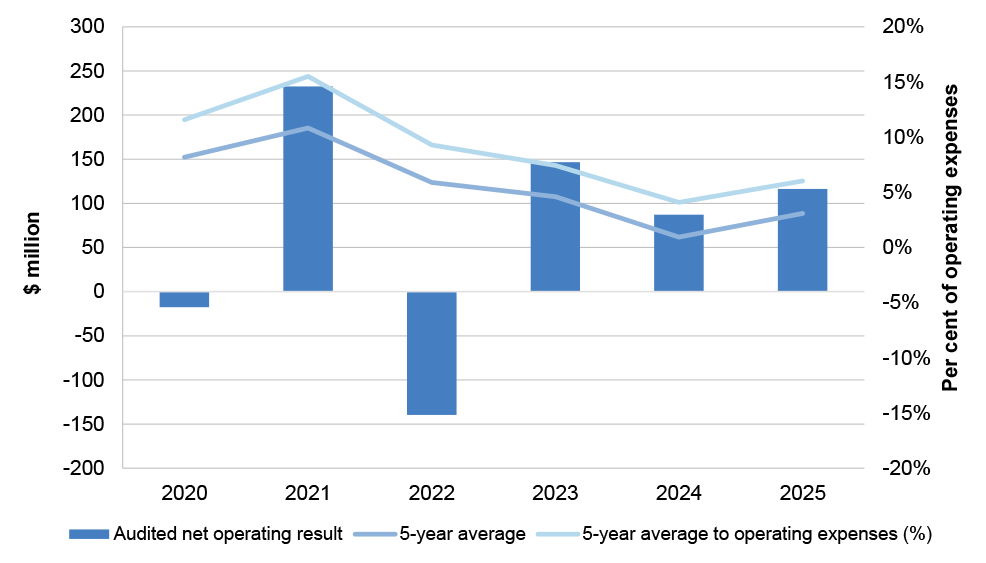

2.32 The ANAO produces analysis of material entities’ audited net operating results across the Government sector, based on averages over a five-year period.65 In this work, an average result greater than one per cent of total expenses over the previous five years is considered a large surplus.66 ANAO analysis of ANU audited net operating results based on this method (Figure 2.9) shows large average surpluses for the five years prior, albeit coupled with declining performance since 2020 and improvement in 2025 — the 2021 improvement evident in Figure 2.9 is associated with the one-off Australian Government COVID-19 relief payment provided through the RBGs. The decline between 2020 and 2024 indicates financial sustainability could be a challenge for ANU in the long term if these five-year trends are not well understood and addressed.

Figure 2.9: ANU audited net operating results and rolling five-year average, 2020 to 2025

Source: ANAO analysis of ANU data.

TEQSA financial risk assessment found ANU is a low financial sustainability risk

2.33 The ANU, like other universities, is required to provide audited financial statements to TEQSA. For each calendar year reporting period, financial reporting is due by the end of June the following year (i.e. data for 2024 was due by 30 June 2025).

2.34 TEQSA uses this data to assess financial risks. TEQSA’s most recent risk assessment of ANU recorded a low financial viability risk based on 2023 data for the calendar year 2022 (improved from moderate based on 2022 data), and a low financial sustainability risk. On 7 April 2026, TEQSA advised the ANAO that ‘TEQSA’s risk assessments are prepared for the purposes of informing TEQSA’s approach and are not intended to provide providers themselves with an assessment of their own risks’.

2.35 In December 2025, TEQSA announced it would be retiring its risk model of individual provider risk assessments, due to:

- its reliance on lagged data (for example, financial risk assessment in 2025 relied on 2023 data);

- the risk of over-stating or under-stating risk due to missing context; and

- a desire to rebalance the focus between individual providers and system-wide risks.

2.36 TEQSA intends to move towards a model that focuses on the provider’s own management of risks, and the use of data to monitor sector-wide risk trends over time.

ANU’s high level of available financial resources and low debt servicing needs means it has a AA+ credit rating

2.37 Since 2020, despite noting challenges in enrolments and operating margins, S&P, ANU’s credit rating agency, has not reduced ANU’s long term credit rating, which has consistently been AA+.

2.38 Credit ratings provide a forward-looking opinion about an issuer’s relative creditworthiness, from AAA (extremely strong capacity to meet financial commitments) to D (payment default, breach of imputed promise, or bankruptcy).67 S&P provides ratings to ANU and five other Australian universities. A high credit rating will generally provide access to debt at a lower interest rate, subject to the borrowing limit set by the Finance Minister (paragraph 1.6).

2.39 According to S&P analysis, the basis for ANU’s rating is:

- ANU’s high level of available financial resources and low debt servicing needs; and

- a high likelihood that the Australian Government would provide support to ANU if it were in financial distress.

ANU’s debt to equity ratio is comparable to other universities

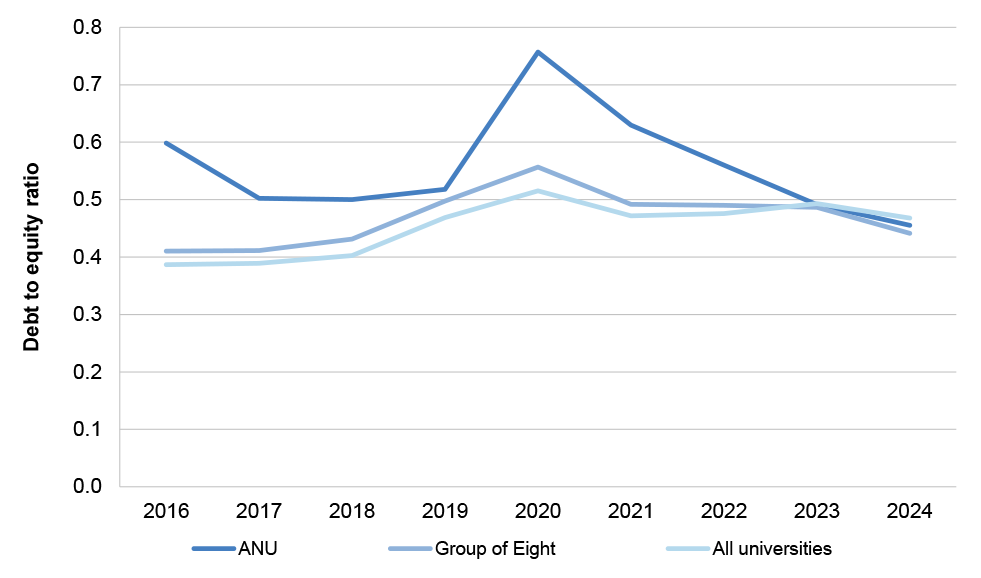

2.40 ANU’s debt-to-equity ratio has consistently exceeded the Go8 average since 2016 (partly due to ANU’s liability in relation to student accommodation service concession arrangements, as discussed in paragraph 3.23), but has improved since 2020, and has been in line with the Go8 since 2023 (Figure 2.10).

Figure 2.10: ANU, Group of Eight, and all university debt to equity ratio, 2016–2024

Source: ANAO analysis of Department of Education data.

2.41 ANU’s performance against other commonly used financial indicators, in comparison with all other Australian universities (as of 2024) is provided at Appendix 4. ANU’s performance was in some cases stronger than, and in other cases weaker than, the average of all universities against these indicators.

3. Financial pressures and conditions leading to Renew ANU

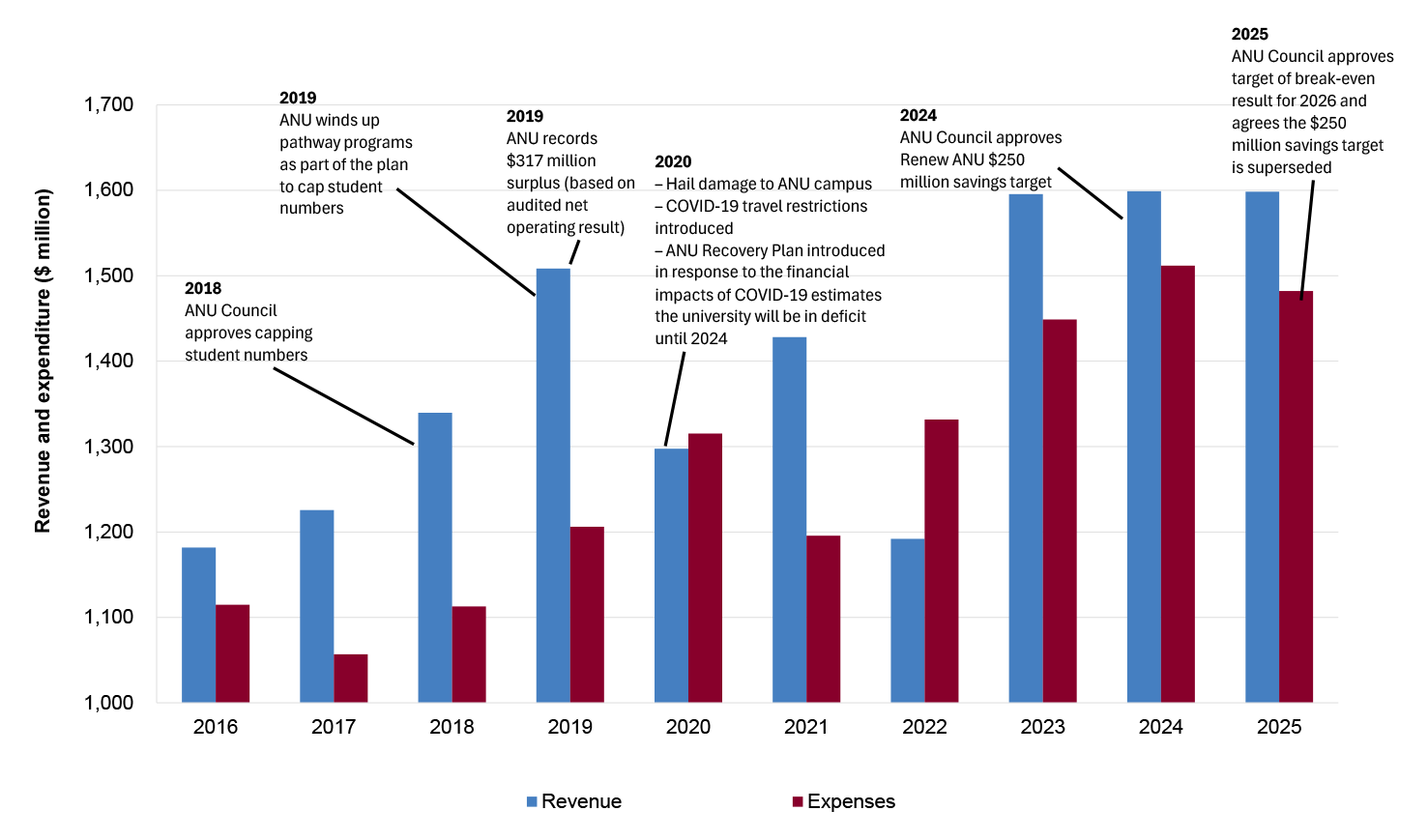

ANU ended 2019 with a $317 million surplus according to its audited financial statements. After revenue declined by 13.6 per cent in 2020, ANU analysis shows that it lacked the mechanisms required to control spending. The university pursued savings and drew down on its investment income for temporary support, but judged this was not sustainable in the longer term.

Despite repeatedly basing budget estimates on revenue growth from international student fees, ANU did not achieve planned growth, and ended 2023 with a focus on reducing spending. This is indicative of a misalignment between forecasts and international student recruitment.

In 2018, ANU adopted a vision for a ‘human scale’ university

3.1 In the three years to 2018, ANU student numbers grew by 18.7 per cent to 20,281 equivalent full time student load (EFTSL), driven primarily by increases in international student enrolments.68 In February 2018, ANU Council considered the impact of this growth, which had occurred without a strategic decision to become a larger institution, and approved a proposal from the Vice-Chancellor to cap enrolments for a ‘human scale’ university. In a public mid-year update to staff and students in July 2018, the Vice-Chancellor explained:

For those people coming to ANU from every walk of life, I want ANU to continue to provide a unique personal education experience for our students. But to do that, we need to remain relatively small.

3.2 In July 2018, implementation arrangements were agreed by Council, including a target of 19,204 EFTSL by 2022. Planned reductions were targeted by student cohort to:

- reduce undergraduate student numbers, including domestic undergraduate students, as the Australian Government had announced a cap on Commonwealth Grants Scheme (CGS) funding in December 2017;

- increase domestic postgraduate coursework and higher degree research students;

- diversify source countries for postgraduate international coursework students;

- improve the university’s student to staff ratio; and

- increase student numbers in the College of Engineering and Computer Science.

3.3 The decision was supported by a five-year financial scenario model, stress testing of the model against geopolitical and Australian Government funding changes, and modelling of the financial impact of the change, which was expected to reduce the university’s operating margin to 3.0 per cent (or a $37.0 million unaudited underlying operating result) in 2020.

3.4 Implementation of the plan began in 2019 with winding up pathway programs, which accounted for 35.7 per cent of international students admitted to ANU in 2018. Broadly, ‘pathway programs’ for university entry for international students consist of Foundation Studies (six to twelve months study to meet the academic requirements for entry to university study) and English Language Intensive Courses for Overseas Students (ELICOS, five weeks to 12 months study to meet English language requirements for entry to university study).69 A conditional offer allows an international student to enter Australia to undertake either Foundation or ELICOS study for up to a year, then (on successful completion) advance to the first year of an undergraduate degree.70

3.5 ANU ended 2019 with a $317 million surplus (based on audited net operating result, Figure 2.8), and the expectation that its 2020 operating margin would be reduced to 3.0 per cent due to planned reductions in student numbers (paragraph 3.3).

ANU reported a $17.7 million loss in 2020, driven largely by the economic effects of the pandemic on investment earnings

3.6 By the end of 2020, total ANU revenue had declined 13.6 per cent compared with 2019, and ANU reported a $17.7 million loss (based on audited net operating result) for that calendar year.

3.7 The reduction compared with 2019 was driven by declines across government grants, investment income, and student fee revenue with the largest decline being a $172.9 million decline in investment income in 2020, compared with 2019 (Table 3.1).

Table 3.1: Change in ANU income by source of fundsa, 2019 to 2020

|

Year |

State and local government financial assistance ($) |

Australian Government grants ($m) |

Domestic student fees ($m) |

International student fees ($m) |

Investment income ($m) |

All other ($m) |

|

2019 |

6.3m |

637.6 |

146.0 |

328.9 |

234.4 |

149.1 |

|

2020 |

6.1m |

613.0 |

124.0 |

248.1 |

61.5 |

244.9 |

|

Difference from 2019 to 2020 |

-151,000 |

-24.6 |

-21.9 |

-80.9 |

-172.9 |

95.7 |

Note a: All other comprises: royalties, trademarks and licenses; consultancy and contracts; share of net result; donations and bequests; scholarships and prizes; non-government grants; net gain on disposal of property, plant and equipment; net foreign investment gains; revenue related to service concession arrangements; and other revenue (not elsewhere classified).

Source: ANAO based on Department of Education and ANU data.

COVID-19 border closures reduced ANU’s student fee income beyond the reduction planned in 2018

3.8 Beginning in February 2020, COVID-19 border closures reduced international student numbers across Australia, undermining a key source of revenue for universities. ANU’s choice to wind up pathway arrangements in 2019 (paragraph 3.4) meant most international students commencing the first year of undergraduate study at ANU in semester one 2020 were expected to enter the country that year, whereas in 2018 around one third of commencing international undergraduate students would have already been in Australia.

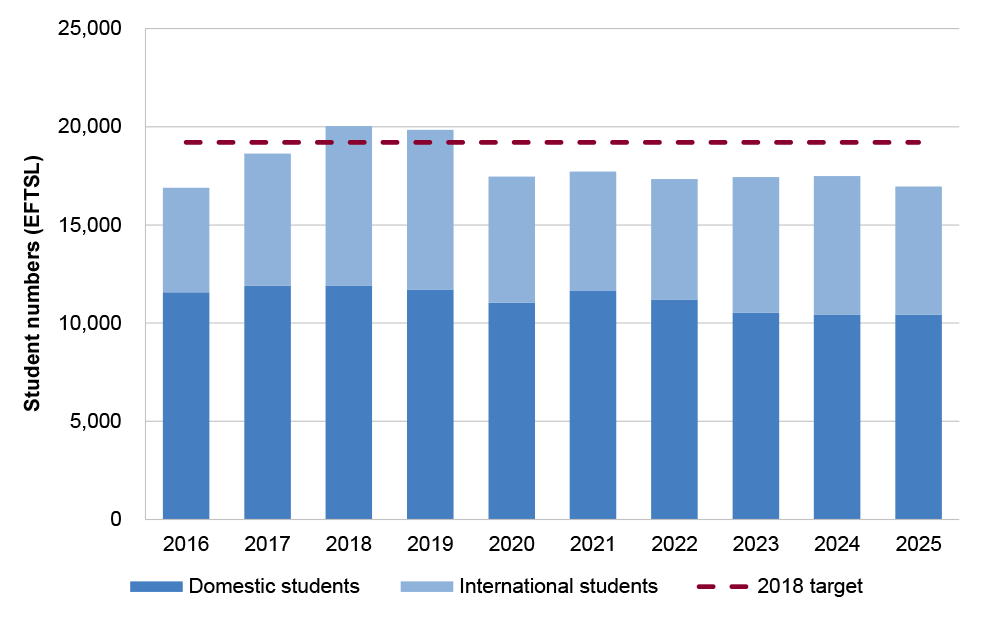

3.9 ANU student load fell by 2,380 EFTSL from 2019 to 2020 (Figure 3.1), more than double the multi-year reduction of 782 EFTSL by 2022 targeted by the 2018 decision to cap student numbers. The actual reduction from 2019 to 2020 comprised:

- 1,707 international students — the plan to cap student numbers was based on 8,291 international EFTSL in 2020, so actual EFTSL of 6,423 was 1,868 EFTSL below expectations; and

- 673 domestic students — the plan to cap student numbers was based on 11,190 domestic EFTSL in 2020, so actual EFTSL of 11,039 was 151 EFTSL below expectations.

Figure 3.1: ANU equivalent full time student load (EFTSLa), 2016 to 2025

Note a: Equivalent full time student load (EFTSL) is a standardised measure of a student’s academic study load over a year. An EFTSL of 1.0 represents the full annual workload for a full-time student.

Source: ANAO based on Department of Education data.

3.10 The difference between planned and actual reductions in student numbers in 2020 equated to an approximately $32.2 million shortfall in the ANU budget.71 This was the approximate size of the ANU’s expected unaudited underlying operating result for 2020, estimated in the ANU Budget approved in December 2019 (paragraph 3.3). This means that if the 2020 ANU Budget had been otherwise correct, the university would have broken even on an underlying operating result basis, despite the larger than expected fall in student numbers.

The economic consequences of COVID-19 reduced ANU’s reported investment income, largely due to changes in the fair value of financial assets

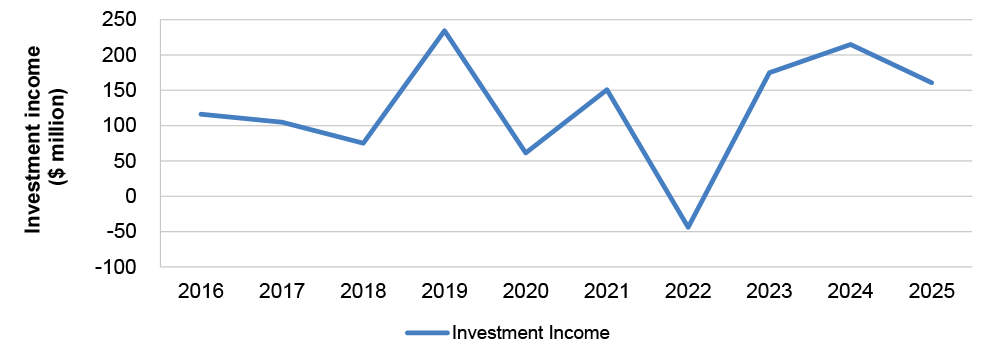

3.11 While primarily a public health emergency, the introduction of public health measures such as border closures in early 2020 significantly reduced economic activity.72 Australia’s Gross Domestic Product (GDP) fell, unemployment increased, and inflation declined.73 The broader economic effects of the pandemic had a much larger immediate effect on ANU’s income than the fall in student numbers, via the university’s investment earnings (Figure 3.2), which fell by $172.9 million, from $234.4 million in 2019 to $61.5 million in 2020.

3.12 This occurred in the context of ANU’s greater reliance on non-teaching and non-grants income than comparable universities (Figure 2.7), and represented a decrease in investment income as a share of ANU income from 15.6 per cent in 2019, to 4.7 per cent in 2020. In contrast, the total fall from all other sources from 2019 to 2020, including state and territory government and Australian Government grants, and domestic and international student fees (including planned reductions due to the 2018 decision to cap student numbers) was $127.6 million.

3.13 While investment income has a large apparent effect on ANU’s income, including the fall in income as a consequence of COVID-19 (Table 3.1), an investment income gain or loss as reported in ANU’s financial statements is not necessarily an increase or decrease in the cash immediately available to the university. In 2019 to 2020, $153.4 million of ANU’s fall in investment income (88.7 per cent) is attributable to the loss in the fair value of financial assets. Similarly, in 2022, ANU reported a $43.9 million loss from changes in asset valuations and investment returns. In both cases, the assets continued to be held, meaning the loss was recorded, but not realised.

Figure 3.2: ANU investment incomea, 2016 to 2025

Note a: ‘Income’ here refers to a gain or loss reported in ANU financial statements. This is not necessarily an increase or decrease in the cash immediately available to the university. Of the two large decreases shown in the chart: in 2020, ANU’s reported investment income fell by $172.9 million compared with 2019, of which $153.4 million was attributable to changes in asset valuations. In 2022, ANU reported a $43.9 million loss from changes in asset valuations and investment returns. In both cases, the assets continued to be held, meaning the loss was recorded, but not realised.

Source: ANAO based on Department of Education data.

ANU drew on investment income to fund operational expenses during the first year of the pandemic

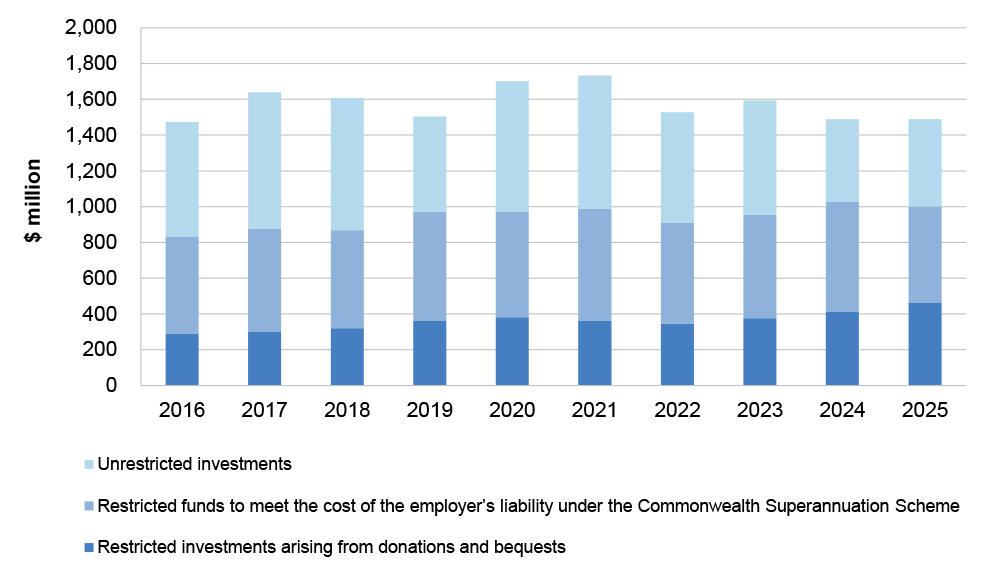

3.14 ANU maintains investment funds (Figure 3.3) to manage donations and bequests designated for scholarships, prizes, foundations, and endowments, and to meet employer liabilities under the Commonwealth Superannuation Scheme (CCS). It treats investments for the purposes of CCS and donations and bequests (where there was an expressed purpose for which the donor provided the funds) as ‘restricted’, but does not have any legal structure in place to formalise this, such as a trust.74

3.15 Since 2016, ANU has reported at least $833 million in ‘restricted’ funds annually in its financial statements. The value of ‘unrestricted’ funds during the 2016 to 2025 period ranged from $459.7 million to $762.0 million. On 11 June 2020, the Finance Committee (now known as the Audit, Finance and Risk Committee) approved withdrawal of $200 million (unrestricted) investment proceeds to use for operational costs as part of ANU’s response to COVID-19. ANU advised the ANAO on 27 November 2025 that smaller withdrawals were completed, including revising of investment fund accounts, to be used for operational expenses. There was no evidence of smaller withdrawals or outcomes of investment fund account reviews being reported to Council or Finance Committee. Paragraph 4.13 discusses the sustainability of this approach.

Figure 3.3: ANU’s investment balance by classification, 2016 to 2025

Source: ANAO analysis of ANU data.

ANU international student numbers did not recover when borders reopened

3.16 ANU student numbers reached 17,462 EFTSL in 2020, including 6,423 international enrolments, well below the 2018 target of 19,204 EFTSL by 2022 (paragraphs 3.2 and 3.9). The ANU Recovery Plan, released in October 2020 in response to COVID-19, acknowledged that the downturn in student numbers meant ANU would need to grow towards its target for a ‘human scale’ university, rather than reducing student numbers to achieve it.

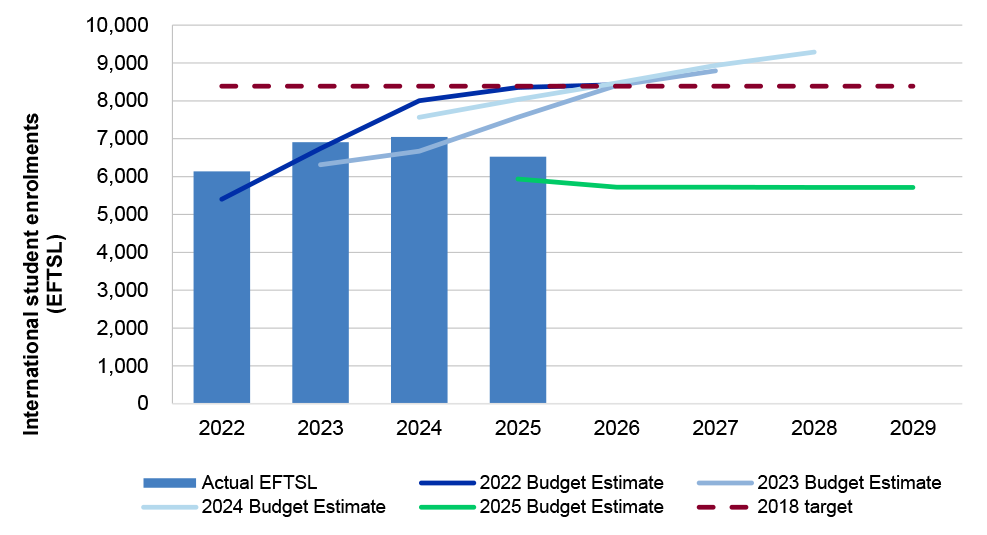

3.17 In 2021 (for the 2022 Budget), ANU began looking at recovery from the 2020 financial shock of the pandemic. The 2022 budget (Figure 3.4) assumed growth would resume in 2023. At the end of 2022 (for the 2023 ANU Budget) assumptions about when growth would resume were revised to 2025.

3.18 ANU exceeded its targets for international enrolments in 2022 and 2023, and by the end of 2023, the data suggested recovery could be in progress. In 2023, sector-wide international enrolments had recovered to near 2019 levels, and although ANU enrolments were still well below its 2019 level, applications had increased by over 7,000 compared with the previous year, to 28,728 (Figure 3.5). On 1 December 2023, ANU Council approved the 2024 ANU Budget, which included an increased target for international enrolment growth in 2024 of 7,566 EFTSL. The 2024 target was not achieved, and assumptions for 2025 were revised down (Figure 3.4).

3.19 Between 2021 and 2024 (for the 2022 to 2025 budgets), ANU forecasts were consistently incorrect as they related to international student numbers, suggesting insufficient alignment between student recruitment and financial planning.

Figure 3.4: ANU international student enrolment budget estimates and actuals, 2022 to 2029 (EFTSLa)

Note a: Equivalent full time student load (EFTSL) is a standardised measure of a student’s academic study load over a year. An EFTSL of 1.0 represents the full annual workload for a full-time student.

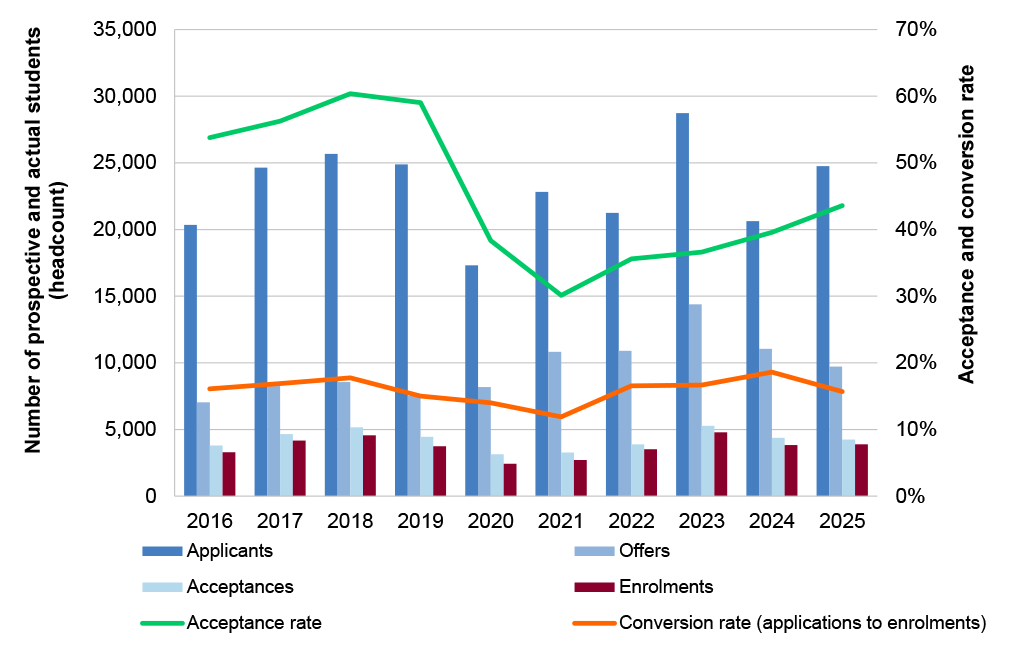

Source: ANAO analysis of ANU data.

Figure 3.5: International applicationa, offerb, and acceptance count, and acceptance ratec, compared with actual enrolments, 2016 to 2025

Note a: Includes applications by international students already enrolled at ANU.

Note b: Offers are offers made for the relevant year to historical applicants.

Note c: Acceptance rate is the number of acceptances over the number of offers.

Source: ANAO based on ANU data.

Spending rapidly resumed after the financial shock of the pandemic

3.20 In July 2020, in response to the impact of COVID-19, the ANU Council approved a revised 2020 ANU Budget, which forecast a deficit of $219 million for 2020 (actual audited net operating result in 2020 was a $17.7 million loss). ANU’s detailed COVID-19 response, the ANU Recovery Plan, was then released in October 2020. The Plan indicated ANU would need to reduce ongoing expenditure by $103 million per year, take on more debt to fund capital investment projects that were already underway, and cash requirements, run a deficit from 2021 to 2023, and use these years to ‘make the changes necessary to support our ongoing financial health’. The target break-even point was set at 2024, but in 2022 this was revised to break even by 2026.

3.21 Although spending fell in 2021, it began increasing again from 2022 (Figure 3.6). This was largely driven by:

- the fact that the 2021 decrease in spending relied on temporary measures, such as pauses on recruitment and travel, and deferred pay rises and senior executive pay cuts;

- rehiring staff, such that between 2021 and 2024, academic staff numbers grew by 7.4 per cent, and professional staff numbers grew by 21.0 per cent, while student numbers fell; and

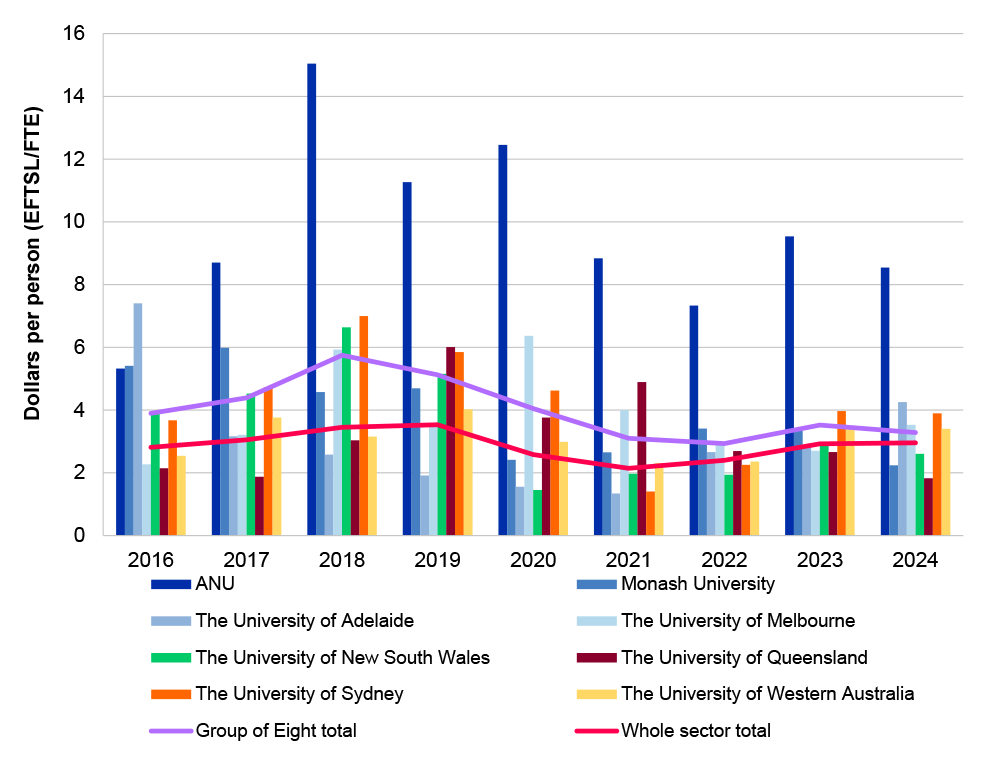

- spending on property, plant and equipment (PP&E), such that between 2016 and 2024 ANU considerably outspent the Group of Eight (Go8) and the sector, spending an average of $9.67 per person (students and staff) compared with the Go8 average of $4.01, and sector average of $2.87 (see Figure 3.7).

3.22 In 2004, long before Council’s approval of the plan to cap enrolment growth in February 2018, ANU had committed to invest in campus redevelopment. Between 2011 and 2016, ANU faced increasing pressure to address demand for student accommodation, and poor student experience of the campus environment. In response, ANU Council committed to:

- new student accommodation projects in August and September 2016 and December 2018, which were completed in 2018, 2019 and 2023; and

- a $262.9 million redevelopment of its central precinct, to create new and redeveloped educational and retail spaces, in April 2016, with construction starting in July 2017, and completion in 2019.

3.23 Between 2016 and 2022, ANU recovered some of its investment in PP&E by entering into agreements with third-party operators (that is, an independent company or entity that operates the business on behalf of the owner) to provide ANU student accommodation on its behalf. ANU received upfront financial contributions of $772 million in exchange for granting the operators the rights to the student accommodation revenue. As a condition of these agreements, ANU is required to maintain occupancy levels of 85 per cent or more to avoid financial penalties. No penalties were deducted in 2025, due to occupancy rates above 85 per cent. As of March 2026, one penalty of $149,449 has been deducted from ANU’s student accommodation-related income in 2026, due to occupancy below 85 per cent in March.

Figure 3.6: ANU revenue and expenditure and key milestones, 2016 to 2025

Source: ANAO analysis of ANU data.

Figure 3.7: Property, plant, and equipment (PP&E)a payments per personb, 2016–2024

Note a: Payments for PP&E include construction in progress, land, buildings, infrastructure, leasehold improvements, library, operational assets, and non-operational assets such as artworks.

Note b: Persons include students (measured in EFTSL) and staff (measured in full time equivalence).

Note: The 2026 Tertiary Education Facilities Management Association produces normalised reports of university facilities and maintenance costs using a range of measures, including (but not limited to) operating costs per EFTSL. ANAO analysis of PP&E payments includes staff (FTE) and students (EFTSL) to account for universities with a high proportion of research only staff and associated investment in non-teaching PP&E.

Source: ANAO analysis of Department of Education data.

ANU lacked mechanisms to control spending when the 2020 financial shock of the pandemic occurred

3.24 ANU analysis shows that it lacked the mechanisms required to control spending when the 2020 financial shock occurred. In 2020, ANU’s control environment was characterised by:

- lack of forecasting and projections in the annual enterprise budget;

- no framework to apply ANU Budget efficiency dividends or other reductions to College spending;

- lack of cash and debt management strategy;

- delayed, incomplete, and poor or variable quality financial reporting;

- lack of hiring controls;

- lack of oversight of the Vice-Chancellor’s Strategic Fund;

- lack of ledger integrity at college and school level; and

- lack of internal purchase and procurement controls.

3.25 The areas targeted for financial control improvements from 2020 are summarised in Table 3.2, which shows ANU activities in response to deficiencies it identified between 2020 and 2025. As shown in the table, action on financial controls since 2020 can be divided between:

- 2020 to 2023 changes implemented as part of the COVID-19 response, including the ANU Recovery Plan; and

- 2024 and 2025 changes implemented as part of Renew ANU (see Chapter 4).

3.26 ANU has reported the major changes introduced from 2020 to 2023 (Table 3.2) were:

- The Expenditure Control Framework (ECF) budget was introduced in 2020 for the COVID-19 response and 2021 Budget. The ECF replaced the former budget ‘allocation model’ (where colleges and portfolios plan and spend based on their earned revenue from key activities, such as teaching and research, minus a contribution for central services). Under the ECF, which was still in place as of December 2025, a set amount is allocated to each college and central portfolio. This provided a framework to introduce efficiency dividends and other reductions in spending. On 15 October 2025, ANU staff advised the ANAO that the former activity-based approach had the benefit of directly linking planned activities within Colleges (such as course growth and emerging areas of research strength) with planned revenue and associated costs.

- The Financial Health Strategy approved by Council in May 2020 set out minimum cash-based ratios and thresholds, which guided the initial response to the impacts of COVID-19 in 2020. The thresholds included a minimum of $250 million in cash, which was equivalent to six month’s salary.

- ANU’s debt limit is set by the Finance Minister. In March 2020, the ANU Vice-Chancellor wrote requesting a borrowing limit of $800 million be granted. The request was approved on 29 March 2020.

- To avoid ‘another round of major University-wide job reductions’, the 2022 ANU Budget used the ‘top down’ ECF to introduce annual efficiency targets of $80 million from salary related costs savings (two per cent in 2023 and a further one per cent in 2024) and $80 million from non-salary related efficiencies (three per cent in 2023 and a further two per cent in 2025). To allow time for these to have their intended impact, the target to break even by 2024 was revised to 2026.

- Reporting and record keeping improvements were introduced from 2022, to provide a single source of truth for the presentation of financial results (there were previously seven different reporting approaches, which produced different results), and align the classification of income, expenses, assets, liabilities and equity in internal reporting with ANU’s statutory obligations for its financial statements.

- From March 2023, excess leave balances were recognised in divisional budgets, therefore forming part of the expenditure of local areas within the university.

3.27 Changes continued throughout 2024 and 2025, and these have also been included in Table 3.2.

Table 3.2: Financial management improvements reported by ANU, by year and issue, 2020 to 2025a

|

Issue |

Improvements reported by year |

|||||

|

|

2020 |

2021 |

2022 |

2023 |

2024 |

2025 |

|

Annual enterprise budget |

Expenditure Control Framework (ECF) Budget introduced |

Forward estimates of revenue and expenses |

No action reported |

No action reported |

No action reported |

No action reported |

|

Framework to apply reductions to spending |

Spending limits |

No action reported |

Annual efficiency targets |

Annual efficiency targets applied to business areas |

Additional mid-year reductions applied to business areas |

No action reported |

|

Cash and debt management strategy |

Council approved minimum cash ratios and thresholds |

No action reported |

No action reported |

No action reported |

Council approved revised minimum cash threshold |

No action reported |

|

Financial reporting |

No action reported |

No action reported |

New financial reports |

No action reported |

Real-time financial dashboards |

Student recruitment reporting |

|

Human resources (HR) controls |

No action reported |

No action reported |

No action reported |

Excess leave balances recognised in area budgets |

HR centralised; Recruitment Approval Committee |

Policy covering re-hiring after redundancy |

|

Financial oversight and accountability |

No action reported |

No action reported |

No action reported |

No action reported |

Vice-Chancellor’s Strategic Fund ended |

No action reported |

|

Financial record keeping |

No action reported |

No action reported |

No action reported |

New guidance |

Additional delegation requirements |

Policy and methodology clarifications |

|

Purchase and procurement |

No action reported |

No action reported |

No action reported |

No action reported |

No action reported |

Purchase card guidance and controls |

Note a: Activity over multiple years (for example, reporting changes) indicates successive changes, and is not necessarily indicative that work has been completed. The ANAO has relied on ANU reporting of improvements to develop this table. ANAO has not assessed if the changes constitute improvements against a framework.