Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 37 of 2025–26

Support and Regulation of Indigenous Corporations

Published

Tuesday 9 June 2026

Portfolio

Prime Minister and Cabinet

Entity

National Indigenous Australians Agency; Registrar of Aboriginal and Torres Strait Islander Corporations

Contact

Please direct enquiries through our contact page.

Activity

Regulation

Sector

Prime Minister & Cabinet

Indigenous

Audit snapshot

Why did we do this audit?

- The Corporations (Aboriginal and Torres Strait Islander) Act 2006 (CATSI Act) is a ‘special measure’ under the Racial Discrimination Act 1975 to give First Nations peoples access to the same opportunities to form and manage corporations as everyone else.

- Corporations registered under the CATSI Act have billions of dollars in income and assets, employ tens of thousands of people and play a critical role in delivering community services.

- The Office of the Registrar of Indigenous Corporations (ORIC) regulates Aboriginal and Torres Strait Islander (Indigenous) corporations. The Chief Executive Officer of the National Indigenous Australians Agency (NIAA) is the accountable authority for ORIC under the Public Governance, Performance and Accountability Act 2013.

Key facts

- As at 30 June 2025, there were 17,636 directors and 243,016 members of Indigenous corporations.

- 2023–24 total revenue for Indigenous corporations was at least $4.5 billion.

- Between 2022–23 and 2024–25, ORIC received 1,067 reports of concern, and completed 127 examinations, eight special administrations and 27 investigations.

What did we find?

- ORIC’s support and regulation of Indigenous corporations under the CATSI Act is partly effective.

- ORIC has largely fit-for-purpose governance arrangements, provides largely effective support to corporations to encourage compliance with the CATSI Act, and is increasing its regulatory response to non-compliance.

- Effectiveness is diminished by declining annual reporting compliance.

What did we recommend?

- There was one recommendation to the Australian Government to issue a statement of expectations (noted by the NIAA); one recommendation to the Department of Finance to improve the whole-of-government guidance (agreed); and one recommendation to the NIAA about performance reporting (agreed in principle). There were two recommendations to the NIAA and ORIC about consideration of risk in compliance planning and evaluation. The NIAA agreed in principle to these two recommendations and the Registrar of Aboriginal and Torres Strait Islander Corporations agreed.

3,284

Number of Indigenous corporations as at 30 June 2025.

29%

Indigenous corporations compliant with the reporting deadline for 2024–25 annual reports.

48

Indigenous corporations referred for prosecution for non-compliance with annual reporting requirements between 2022–23 and 2024–25.

Summary and recommendations

Background

1. The Corporations (Aboriginal and Torres Strait Islander) Act 2006 (CATSI Act) is a special measure under the Racial Discrimination Act 1975 ‘for the advancement and protection of Aboriginal peoples and Torres Strait Islander peoples’, aimed at giving First Nations peoples access to the same opportunities to form and manage corporations as everyone else.1

2. The CATSI Act establishes an incorporation framework for Aboriginal and Torres Strait Islander groups and organisations wishing to incorporate. There are benefits to incorporating under the CATSI Act rather than other incorporation frameworks, including corporation rules that are relevant to cultures and communities; no fees to lodge forms, documents and reports; and access to information and support including training.2

3. The Registrar of Aboriginal and Torres Strait Islander Corporations (the Registrar) is an independent statutory office holder appointed under the CATSI Act by the Minister for Indigenous Australians. The Office of the Registrar of Indigenous Corporations3 (ORIC) is established under the CATSI Act within the National Indigenous Australians Agency (NIAA).4

4. The aims established for the Registrar include facilitating and improving the effectiveness, efficiency, sustainability and accountability of Indigenous corporations; having regard to Aboriginal and Torres Strait Islander tradition and circumstances; and administering functions and powers effectively and with a minimum of procedural requirements.

5. The total number of Aboriginal and Torres Strait Islander corporations (Indigenous corporations) registered under the CATSI Act as at 30 June 2025 was 3,284.

Rationale for undertaking the audit

6. Australian governments have stated that in a broad range of service delivery areas including health, housing and education, Aboriginal and Torres Strait Islander organisations achieve better results for their communities and should be empowered to make decisions about and deliver the critical services on the ground.5 Corporations registered under the CATSI Act have billions of dollars in income and assets and employ tens of thousands of people. The NIAA states that Indigenous corporations ‘play a critical role in delivering services and supporting economic development in Indigenous communities, particularly in rural and remote Australia’.6 The CATSI Act is a ‘special measure’ under the Racial Discrimination Act 1975 to give First Nations peoples access to the same opportunities to form and manage corporations as everyone else.7

7. This audit provides assurance to the Parliament that ORIC is appropriately supporting and regulating Indigenous corporations to:

- meet the aims of the CATSI Act, which includes that First Nations peoples have access to the same opportunities to form and manage corporations as everyone else; and

- ensure that Indigenous corporations are well placed to deliver services and support economic development in Indigenous communities, particularly in remote Australia.8

Audit objective and criteria

8. The objective of the audit was to assess whether Indigenous corporations are being effectively supported and regulated under the CATSI Act.

9. To form a conclusion against the objective, the following high-level criteria were applied:

- Are there fit-for-purpose governance arrangements for the support and regulation of Indigenous corporations?

- Have Indigenous groups been effectively supported to incorporate and Indigenous corporations to operate in compliance with the CATSI Act?

- Have regulatory powers been used effectively to respond to, correct, penalise and deter non-compliance with the CATSI Act?

Conclusion

10. ORIC’s support and regulation of Indigenous corporations under the CATSI Act is partly effective. ORIC has largely fit for purpose governance arrangements, provides largely effective support to corporations to encourage compliance with the CATSI Act, and is increasing its regulatory response to non-compliance. One indicator of effectiveness is Indigenous corporations’ compliance with annual reporting requirements, which benefits a corporation’s members, communities, creditors, investors, government agencies and ORIC. Effectiveness is diminished by a worsening outcome — as at 31 December 2025, reporting compliance was less than 30 per cent and was declining over time.

11. ORIC’s governance arrangements for the support and regulation of Indigenous corporations are largely fit for purpose. A regulatory framework includes a clear articulation of the Registrar’s regulatory posture, however priorities and activities could be more explicitly linked to higher rated non-compliance risks, risk treatments and data. There is no contemporary statement of intent or ministerial statement of expectations. ORIC publishes performance information and has established largely effective performance monitoring and reporting arrangements. While the Chief Executive Officer of the NIAA is the accountable authority for ORIC under the Public Governance, Performance and Accountability Act 2013 (PGPA Act), the NIAA does not report on the performance of ORIC through its corporate plan and annual report. Although ORIC lacks a stakeholder engagement plan, it has established external accountability mechanisms and identifies and acts on opportunities to improve its performance.

12. The Australian Government’s Regulatory Policy, Practice and Performance Framework could be clearer about expectations and requirements for statutory office holders such as the Registrar of Aboriginal and Torres Strait Islander Corporations.

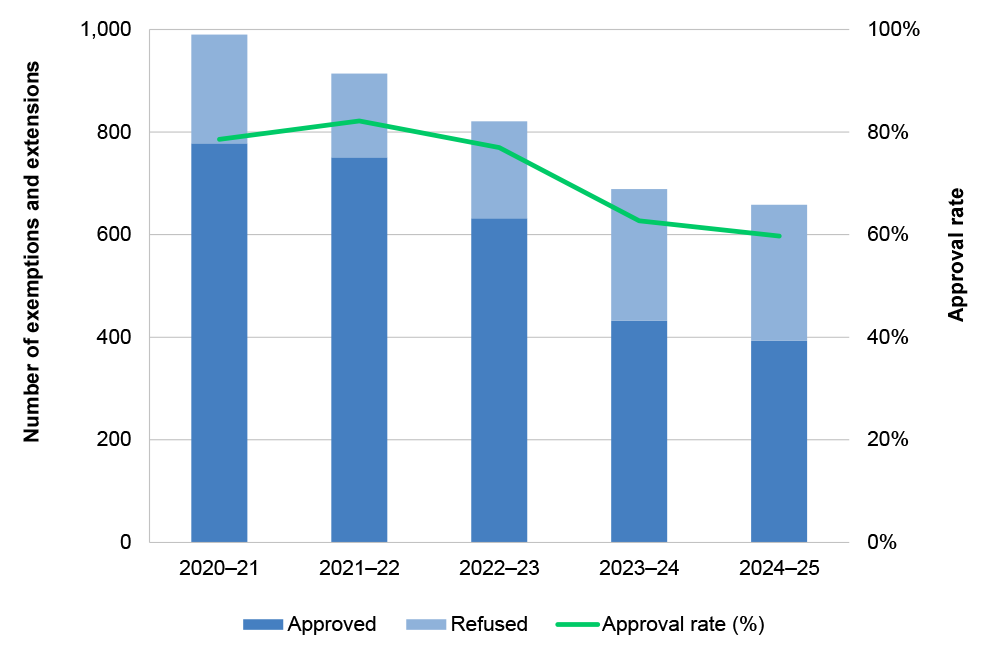

13. ORIC’s support for Indigenous corporations to incorporate and operate is largely effective. Guidance, support, and training to facilitate incorporation and promote compliance with the CATSI Act are largely fit for purpose. Inquiries are dealt with in a timely manner. ORIC’s support activities could be more strategic and consistently targeted to risk. Over 600 exemption or extension applications were made and considered in 2024–25. Exemption decision-making could be more consistently undertaken.

14. ORIC’s use of its regulatory powers to respond to, correct, penalise and deter non-compliance is partly effective. ORIC has increased the use of regulatory tools in recent years. Compliance with annual reporting — a key requirement under the CATSI Act — is declining for small, medium and large-sized corporations and was less than 30 per cent overall for 2024–25. To some extent this is attributed to a decision not to deregister non-compliant and disengaged corporations that hold assets because this is resource intensive. Non-compliance with annual reporting impedes ORIC’s ability to use data to understand the drivers of non-compliance. Due to a lack of evaluation, ORIC does not have a full understanding of the drivers of and harm caused by non-compliance. Without this full understanding, ORIC cannot be certain planned regulatory activity is responding to the greatest risks and harms.

Supporting findings

Governance arrangements

15. Implementation of the Registrar’s functions is supported by appropriate line management arrangements, delegations, governance committees and memoranda of understanding with other regulators. ORIC has a publicly available, detailed and contemporary regulatory framework that includes the Registrar’s regulatory posture and priorities. ORIC describes its regulatory approach as ‘proportionate’ to the nature of the non-compliance and potential for harm. The framework could be improved with an up-to-date statement of ministerial expectations and intent; and by better reflecting several aims of the Registrar established in the CATSI Act relating to cost-effectiveness and regulatory burden. ORIC identifies non-compliance risks, which are regularly reviewed. The regulatory framework is informed by business intelligence; however it could be more clearly and explicitly linked to the more highly rated non-compliance risks, data and evidence. An updated approach to risk assessment in 2025 did not establish risk appetite, tolerances or ratings, which impacts on ORIC’s ability to effectively prioritise risk treatments and activities to achieve objectives. (See paragraphs 2.2 to 2.31)

16. The NIAA, whose CEO is the accountable authority for ORIC under the PGPA Act, does not include performance information about ORIC in its annual performance statements. This is inconsistent with the principle of transparency and accountability for regulator performance established in the Regulatory Policy, Practice and Performance Framework. There could be greater clarity in whole-of-government guidance on requirements for accountable authorities to publicly report through corporate plans and annual reports, on the functions of statutory authorities and office holders that are financially and administratively supported within a PGPA Act entity.

17. ORIC has published performance information and developed a performance framework for its regulatory functions, which has improved over time and has appropriate oversight from a senior management committee. The framework identifies a large set of input, activity, output, outcome and timeliness performance measures, which are linked to the Registrar’s objectives. There is public reporting against the measures, although, as at March 2026 results for some measures had not been reported. Publicly reported measures would be strengthened by documented methodologies and targets. ORIC publishes statistical information about the Indigenous corporations it regulates. In its advice to the Minister, ORIC has provided limited information about its performance. (See paragraphs 2.32 to 2.52)

18. ORIC does not have a stakeholder management plan and does not analyse themes from internal reviews and complaints about its staff for the purposes of continuous improvement. ORIC has established external accountability mechanisms including a service charter, systems to receive and respond to complaints about its staff and stakeholder surveys. ORIC has undertaken or commissioned business reviews and ex-post reviews of regulatory decisions. ORIC could improve the procedures and processes associated with its internal review process for regulatory decisions. It has identified areas for improvement and improved aspects of its processes and services. (See paragraphs 2.53 to 2.67)

Support to incorporate and operate

19. ORIC has some support and education planning artefacts that are informed by user research. ORIC does not have an overarching strategic plan for its support and education activities. The Registrar publishes guidance about incorporation under the CATSI Act, including its unique benefits, and responds to registration inquiries. ORIC has developed guidance materials to assist Indigenous corporations to comply with their obligations under the CATSI Act. It resolves approximately 7,000 inquiries each year in a timely manner and provides training. It has three specialised support services. Some support is targeted to riskier corporation types, such as new corporations or those exiting special administration, however this targeted support has been inconsistently and partly implemented. (See paragraphs 3.2 to 3.27)

20. The CATSI Act allows the Registrar to grant exemptions and extensions for certain requirements in certain circumstances, to assist Indigenous corporations to comply. ORIC has policies and procedures for some but not all exemption types and in 2024 developed materials that signalled a more restrictive approach to the granting of exemptions and extensions. Over 600 exemption or extension applications were made and considered in 2024–25. Consideration and approval of exemption applications in 2024–25 was not always consistent with the more restrictive requirements. (See paragraphs 3.28 to 3.36)

Using regulatory powers to respond to, correct, penalise and deter non-compliance

21. ORIC has established reactive (reports of concern and targeted examinations) and proactive (rolling examinations and data analytics and monitoring) detection methods for non-compliance. ORIC has developed procedures, guidance and systems to support reactive detection activities and these are aligned with a proportionate, risk-based approach to detection. Proactive detection activities are less well supported by procedures, guidance and systems and are less clearly risk based. Reports of concern are well managed. (See paragraphs 4.4 to 4.6)

22. ORIC appropriately considered and responded to a sample of reports of concern from October 2024 to June 2025 examined by the ANAO. ORIC improved its timeliness in ‘resolving’ reports of concern from an average of 28 working days in 2022–23 to 13 working days in 2024–25. All rolling program and targeted examinations commenced in 2024–25 and completed by August 2025 resulted in a regulatory response of some form. Non-compliance in corporation reporting identified through monitoring (approximately 80 to 300 in each year between 2021–22 and 2024–25) resulted in a total of 48 corporations being referred for minor regulatory prosecution between 2021–22 and 2024–25. ORIC could do more to monitor Indigenous corporation directors’ uptake of director IDs. (See paragraphs 4.7 to 4.18)

23. Decision-makers for matter escalation and regulatory responses are largely supported by internal procedures and guidance, however there are some gaps. Risk factor criteria and thresholds for decisions and escalations are set out for some types of matters and not for others. The number of lower intervention responses have largely remained static or increased over the three years to 2024–25. The number of special administrations commenced and completed has remained broadly constant over the period 2022–23 to 2024–25. After not concluding any investigations in 2021–22 in part due to the COVID-19 pandemic, ORIC recommenced investigations in 2022–23. ORIC recommenced referrals for minor regulatory prosecutions in 2023–24 after making no referrals between 2019–20 and 2022–23 due to the COVID-19 pandemic. There were five successful minor regulatory prosecutions in 2023–24 and 21 in 2024–25. Over the period 2022–23 to 2024–25, two non-minor prosecutions were successful. (See paragraphs 4.19 to 4.38)

24. ORIC undertakes a range of activities that seek to deter non-compliance. Despite these activities, compliance with reporting requirements has steadily declined over ten years for small, medium and large corporations. Fewer than 30 per cent of corporations overall were compliant with requirements to lodge 2024–25 reports by 31 December 2025. Non-compliance with reporting requirements reduces transparency and information for corporation members, communities, creditors, investors and government agencies as well as for ORIC. There is a general lack of evaluation to identify the key drivers of non-compliance to inform risk-based targeted compliance activities and to understand harm caused by non-compliance. ORIC developed a project plan in January 2026 aimed at increasing small corporations’ compliance with reporting obligations. (See paragraphs 4.39 to 4.46)

Recommendations

Recommendation no. 1

Paragraph 2.9

The Australian Government issue the Minister for Indigenous Australians’ statement of expectations for the Registrar of Aboriginal and Torres Strait Islander Corporations, which should include a requirement for a responding statement of intent.

National Indigenous Australians Agency response: Noted

Recommendation no. 2

Paragraph 2.22

The Office of the Registrar of Indigenous Corporations ensure that key regulatory framework documents, such as the Compliance Framework and Registrar’s Regulatory Posture, more clearly demonstrate the link between regulatory priorities and activities and compliance risks.

National Indigenous Australians Agency response / Registrar of Aboriginal and Torres Strait Islander Corporations response: Agreed in principle / Agreed

Recommendation no. 3

Paragraph 2.39

The National Indigenous Australians Agency ensure that its performance reporting for the Office of the Registrar of Indigenous Corporations, including annual performance statements and regulator performance reporting, is consistent with the principles and requirements of the Public Governance, Performance and Accountability Act 2013 (PGPA Act), PGPA Rule, Department of Finance resource management guides and other guidance designed to support PGPA Act entities to meet the requirements of the PGPA framework.

National Indigenous Australians Agency response: Agreed in principle

Recommendation no. 4

Paragraph 2.42

The Department of Finance:

- clarify, in its relevant guidance, how the requirements and guidance apply to statutory office holders that perform regulatory functions; and

- provide guidance for Public Governance, Performance and Accountability Act 2013 (PGPA Act) entities to report, in their annual performance statements, on the functions of statutory authorities and office holders that are not a separate PGPA Act entity and are financially and administratively supported within a PGPA Act entity.

Department of Finance response: Agreed

Recommendation no. 5

Paragraph 4.47

The Office of the Registrar of Indigenous Corporations undertake an evaluation of the key drivers of reporting and annual general meeting non-compliance and the relative impact of its support activities and regulatory responses in relation to non-compliance in these two areas.

National Indigenous Australians Agency response / Registrar of Aboriginal and Torres Strait Islander Corporations response: Agreed in principle / Agreed

Summary of entity response

25. The proposed audit report was provided to the NIAA and the Registrar. An extract of the proposed audit report was provided to the Department of Finance. Summary responses are reproduced below. Full responses are in Appendix 1. Improvements observed by the ANAO during the course of the audit are listed at Appendix 2.

National Indigenous Australians Agency

The National Indigenous Australians Agency (NIAA) welcomes the findings of the audit on Support and regulation of Indigenous corporations.

First Nations businesses are a major driver of economic development that also support the cultural and social wellbeing of Aboriginal and Torres Strait Islander communities. The Registrar of Aboriginal and Torres Strait Islander Corporations (the Registrar) is the office holder who supports and regulates corporations that are incorporated under the Corporations (Aboriginal and Torres Strait Islander) Act 2006 (CATSI Act).

The NIAA supports the two audit recommendations made jointly to the Office of the Registrar of Indigenous Corporations (ORIC) and the NIAA, noting that implementation of those recommendations will be for the Registrar to lead. The NIAA will continue to ensure that its performance reporting for ORIC is consistent with relevant principles and requirements, in line with current and any future Department of Finance guidance.

Registrar of Aboriginal and Torres Strait Islander Corporations

The audit highlights ORIC’s extensive change program since my appointment. Changes to ORIC’s systems, policies and procedures aimed at better supporting corporations incorporated under the CATSI Act. This includes helping members to exercise their rights in owning and controlling their corporations — the CATSI Act’s purpose.

ORIC’s strategic, performance and reporting frameworks go above what the legislation requires, or is expected for a regulator of 43 staff.

The report shows ORIC has been expanding its use of my regulatory powers to target non-compliance with all aspects of the CATSI Act. When applying these powers we consider each corporation’s circumstances which is necessary when regulating a population of such diversity.

While the report highlights some areas for improvement that ORIC is already addressing, it will still inform ORIC’s commitment to continuous improvement.

Overall, the report found ORIC partially effective at supporting and regulating corporations which is inconsistent with findings against 2 of the 3 audit criteria. Furthermore, the ANAO’s narrow use of reporting compliance to measure our regulatory effectiveness fails to recognise the CATSI Act imposes many obligations on corporations — all of which we regulate.

We regulate in a complex environment, and it was disappointing to see some findings are premised on an incorrect perception that regulating Indigenous corporations is linear or formulaic — not recognising social, cultural and human factors.

Department of Finance

The Department of Finance notes the findings in the report extract.

Key messages from this audit for all Australian Government entities

26. Below is a summary of key messages, including instances of good practice, which have been identified in this audit and may be relevant for the operations of other Australian Government entities.

Group title

Regulation, governance and risk management

Key learning reference

Group title

Performance and impact measurement

Key learning reference

1. Background

Introduction

1.1 The Corporations (Aboriginal and Torres Strait Islander) Act 2006 (CATSI Act) is a special measure under the Racial Discrimination Act 1975 ‘for the advancement and protection of Aboriginal peoples and Torres Strait Islander peoples’, aimed at giving First Nations peoples access to the same opportunities to form and manage corporations as everyone else.9 The CATSI Act establishes an incorporation framework for Aboriginal and Torres Strait Islander groups and organisations wishing to incorporate.

1.2 Incorporation enables groups to establish a legal entity separate to its members. The main benefits of incorporating are: protection from liabilities for members; taxation benefits; improved reputation due to the requirement to meet certain governance standards; access to capital; improved succession processes; and more effective management processes that come from decision-making powers being given to a smaller group with oversight from another.10

1.3 There are additional benefits to incorporating under the CATSI Act rather than other incorporation frameworks, including corporation rules that are relevant to cultures and communities; no fees to lodge forms, documents and reports; and access to information and support including training.11

Office of the Registrar of Indigenous Corporations

1.4 The Registrar of Aboriginal and Torres Strait Islander Corporations (the Registrar) is an independent statutory office holder appointed under the CATSI Act by the Minister for Indigenous Australians. The Office of the Registrar of Indigenous Corporations12 (ORIC) is established under the CATSI Act within the National Indigenous Australians Agency (NIAA).13

1.5 ORIC staff are based in offices in Canberra, Adelaide, Alice Springs, Broome, Brisbane, Cairns, Coffs Harbour, Darwin, Perth and Sydney. ORIC’s annual budget and staffing between 2020–21 and 2024–25 is shown in Table 1.1.

Table 1.1: Annual resourcing, 2020–21 to 2024–25

|

|

2020–21 |

2021–22 |

2022–23 |

2023–24 |

2024–25 |

|

Full-time equivalent staffa |

34.5 |

41.1 |

41.4 |

39.6 |

43.0 |

|

Base funding ($’000) |

8,380 |

8,561 |

8,948 |

9,023 |

9,373 |

|

Non-ongoing funding excluding projects ($’000)b |

0 |

0 |

3,547 |

4,736 |

4,769 |

|

Projects ($’000)c |

0 |

0 |

4,110 |

3,883 |

2,845 |

|

Total budget ($’000) |

8,380 |

8,561 |

16,605 |

17,642 |

16,987 |

Note a: As at 30 June.

Note b: Includes funding for initiatives such as leadership and governance activities. ORIC advised the ANAO in May 2026 that this funding ceases on 30 June 2026.

Note c: Includes funding for initiatives such as ORIC’s IT upgrades and the implementation of director identification requirements. ORIC advised the ANAO in May 2026 that this funding ceases on 30 June 2026.

Source: ORIC and NIAA yearbooks and annual reports and ORIC data and advice. Budget figures reported in NIAA annual reports in 2023–24 and 2024–25 and the ORIC 2022–23 yearbook do not include amounts related to projects. The ANAO did not validate the resourcing data.

1.6 The NIAA is an executive agency as defined by section 65 of the Public Service Act 1999 and is a non-corporate Commonwealth entity under the Public Governance, Performance and Accountability Act 2013 (PGPA Act). The 2019 Executive Order to establish the NIAA specifies that the functions of the NIAA include to lead and coordinate Commonwealth policy development, program design and implementation, and service delivery for Aboriginal and Torres Strait Islander people; and analyse and monitor the effectiveness of programs and services for Aboriginal and Torres Strait Islander people, including programs and services delivered by bodies other than the NIAA.

1.7 The NIAA Chief Executive Officer is the accountable authority for ORIC under the PGPA Act. The PGPA Act imposes duties on accountable authorities including: to govern the entity; to establish and maintain systems relating to risk and control; to encourage cooperation with others; and to keep the responsible Minister and Minister for Finance informed about the entity and its activities.14 The accountable authority is also obliged to observe and consider rules and guidance under the PGPA Act framework, which give effect to the PGPA Act. This includes the Commonwealth Procurement Rules, Commonwealth Grant Rules and Principles, and Department of Finance resource management guides such as RMG 128 Regulator Performance. In addition to providing staff to assist the Registrar, funding for ORIC’s operations (including the engagement of contractors and consultants) are included in the NIAA’s appropriations through the Department of the Prime Minister and Cabinet.15

1.8 The CATSI Act establishes the Registrar’s functions, powers and aims. Functions include making available to the public information about the registration of Aboriginal and Torres Strait Islander corporations (Indigenous corporations) and the administration of the CATSI Act, providing advice, conducting public education programs, assisting with the resolution of disputes and complaints and conducting research. The Registrar also has a number of powers to regulate Indigenous corporations. The aims established for the Registrar include facilitating and improving the effectiveness, efficiency, sustainability and accountability of Indigenous corporations; having regard to Aboriginal and Torres Strait Islander tradition and circumstances; and administering functions and powers effectively and with a minimum of procedural requirements. The Registrar may delegate their functions and powers to ORIC staff, who must comply with the Registrar’s directions.

1.9 Indigenous corporations play a role in providing services to communities, including through funds received from governments through grants. ORIC advised the ANAO in January 2026 that total 2024–25 grant funding reported by Indigenous corporations as at January 2026 was $1.9 billion, which represented 54 per cent of total reported income for those corporations receiving grant funding. The Registrar has stated that ORIC has a continued focus on strengthening:

- Indigenous people’s trust and confidence in their corporations and the continued protection of a self-determining right to govern, represent, deliver services and protect their inherent rights and interests

- the broader public, government and funders’ trust and confidence in Indigenous corporations.16

1.10 Auditor-General Report No. 3 2017–18 Supporting Good Governance in Indigenous Corporations concluded that:

ORIC supports good governance in Indigenous corporations by maintaining public registers, monitoring and enforcing compliance, and providing information, advice and education, consistent with the CATSI Act.17

1.11 The ANAO made three recommendations to: review and update its guidance and procedures for assessing applications for registration as an Indigenous corporation; establish procedures to ensure that persons disqualified by a court or the Registrar are promptly listed on the Register of Disqualified Officers, relevant documents are stored on the register, and such disqualified persons do not continue to hold the positions of director or secretary in Indigenous corporations; and refine its risk rating system in its client relationship management system to better support its regulatory program.18

Corporations (Aboriginal and Torres Strait Islander) Act 2006

1.12 The CATSI Act was established as an alternative to incorporation under the Corporations Act 2001 (Corporations Act); different state and territory incorporated association laws; or state, territory and national cooperatives laws.19 Most Aboriginal and Torres Strait Islander groups seeking to incorporate can choose to incorporate under the Corporations Act or the CATSI Act.20

1.13 The CATSI Act was designed to ‘[maximise] alignment with the Corporations Act where practicable, but [provide] sufficient flexibility for corporations to accommodate specific cultural practices and tailoring to reflect the particular needs and circumstances of individual groups’.21 Differences between the CATSI Act and Corporations Act include membership arrangements, regulatory assistance and reporting requirements (see Appendix 3).

1.14 The CATSI Act was last reviewed in 2020.22 Amendments to the CATSI Act were introduced to the Parliament in August 2021, which proposed changes to the Registrar’s regulatory powers including the power to issue infringement notices. The Bill lapsed at the end of the 46th Parliament in July 2022. The NIAA advised the ANAO in May 2026 that it did not plan to seek amendments to the CATSI Act and that its priority was remaking the Corporations (Aboriginal and Torres Strait Islander) Regulations 2017 (CATSI Regulations), which will sunset in October 2027.

Corporations registered under the Corporations (Aboriginal and Torres Strait Islander) Act 2006

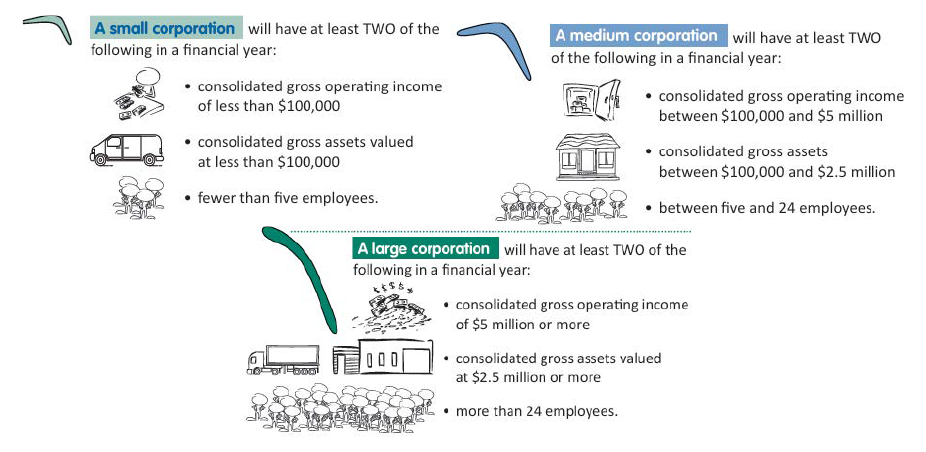

1.15 The CATSI Act classifies Indigenous corporations as small, medium or large (Figure 1.1).

Figure 1.1: Classification of small, medium and large Indigenous corporations

Source: Adapted from ORIC, Fact sheet: Corporation size and reporting, available from https://www.oric.gov.au/ [accessed 7 November 2025].

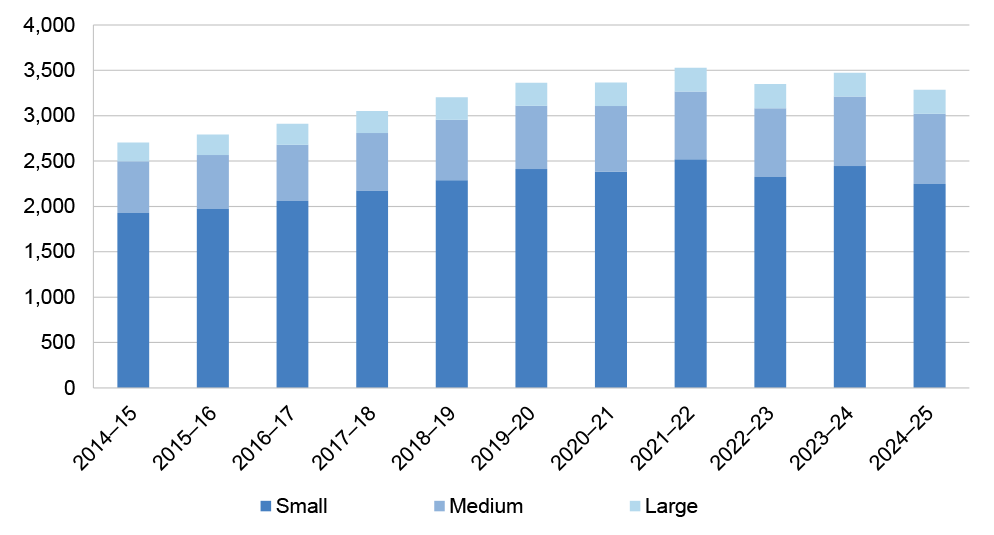

1.16 The total number of Indigenous corporations registered under the CATSI Act was 2,706 as at 30 June 2015 (Figure 1.2) and 3,284 as at 30 June 2025. The 3,284 corporations were led by 17,636 directors and comprised of 243,016 members and:

- 2,252 (69 per cent) were classified as small, 767 (23 per cent) were classified as medium and 265 (eight per cent) were classified as large;

- 1,312 (40 per cent) were registered charities; and

- 284 (nine per cent) were Registered Native Title Bodies Corporate.

1.17 ORIC began publishing data about individual corporations on the Australian Government’s central source of open government datasets data.gov.au in November 2021, which included the corporation size. Between November 2021 and November 2025, the proportion of Indigenous corporations classified as small declined from 74 to 69 per cent, medium increased from 20 to 23 per cent and large increased from six to eight per cent. In total, between November 2021 and November 2025, for the 2,662 corporations that were registered in November 2021 and still registered in November 2025, 309 changed size classification, with 242 of these corporations growing larger.

Figure 1.2: Indigenous corporations by sizea, 2014–15 to 2024–25

Note a: As at 30 June. Size is based on a corporation’s consolidated gross income, gross assets and number of employees, which can change over time. Due to a lack of reporting on size prior to November 2021, while total number of corporations shown in this graph is based on data from www.data.gov.au for all years shown, size classification was derived by the ANAO from the corporation’s most recent size classification in ORIC systems as at 30 September 2025 (including for de-registered corporations). As stated in paragraph 1.18, a small proportion of corporations change size over time, including some large and medium-sized corporations becoming smaller and some small corporations become larger. For these corporations, size classifications will not be accurate for all years shown in the graph.

Source: ANAO analysis of data from www.data.gov.au as at September 2025 and ORIC, State of the sector — January to June 2025, October 2025, available from https://www.oric.gov.au/corporations-and-registers/data-about-corporations/state-sector-reports [accessed 4 March 2026]. There are minor variations between the data published by ORIC and the data on www.data.gov.au.

1.18 The 3,284 corporations registered as at 30 June 2025 operated in the following major sectors23: community services (33 per cent); education and training (27 per cent); health care and health promotion (20 per cent); heritage and culture (20 per cent); land and waters management (19 per cent); and employment (15 per cent). Indigenous corporations exist in all parts of Australia, with the largest number in Queensland (26 per cent), Western Australia (24 per cent) and the Northern Territory (20 per cent).

Corporation obligations under the Corporations (Aboriginal and Torres Strait Islander) Act 2006

1.19 Directors of Indigenous corporations have duties to act with reasonable care and diligence, act in good faith in the best interests of the corporation, not improperly use their position or information, disclose material personal interests, and not trade while insolvent.

1.20 The CATSI Act and Regulations require Indigenous corporations to:

- following the end of the reporting period, lodge reports within six months, which is usually by 31 December (unless exempted or extended) (Table 1.2);

- following the end of the corporation’s financial year, hold an annual general meeting within five months, which is usually by 30 November (unless exempted or extended);

- maintain up-to-date financial records and registers of members and former members;

- keep ORIC informed of relevant changes to the corporation; and

- follow rules set out in the corporation’s rule book, such as a dispute resolution process.

Table 1.2: Annual reporting requirements

|

Registered size |

Consolidated gross operating income |

Required reports |

|

Small |

Less than $100,000 |

|

|

$100,000 to less than $5 million |

|

|

|

Medium |

Less than $5 million |

|

|

Small or medium |

$5 million or more |

|

|

Large |

n/a |

|

Note a: A general report includes the names and addresses of members, directors, and contact person or secretary; total financial year income; total value of assets at year end; number of employees at year end; and whether any director, contact person or secretary is also an employee.

Note b: A financial report contains financial statements for the financial year, which must be audited.

Note c: Eligibility is that at least 90 per cent of income is from government funding; the corporation is required to lodge annual reports with funders as a condition of this funding; and the corporation is not required to provide consolidated financial statements.

Note d: A directors’ report contains a detailed overview of the corporation’s business performance over the year.

Source: ANAO based on ORIC, Fact sheet Corporation size and reporting, 2018, available from https://www.oric.gov.au/ [accessed 16 October 2025].

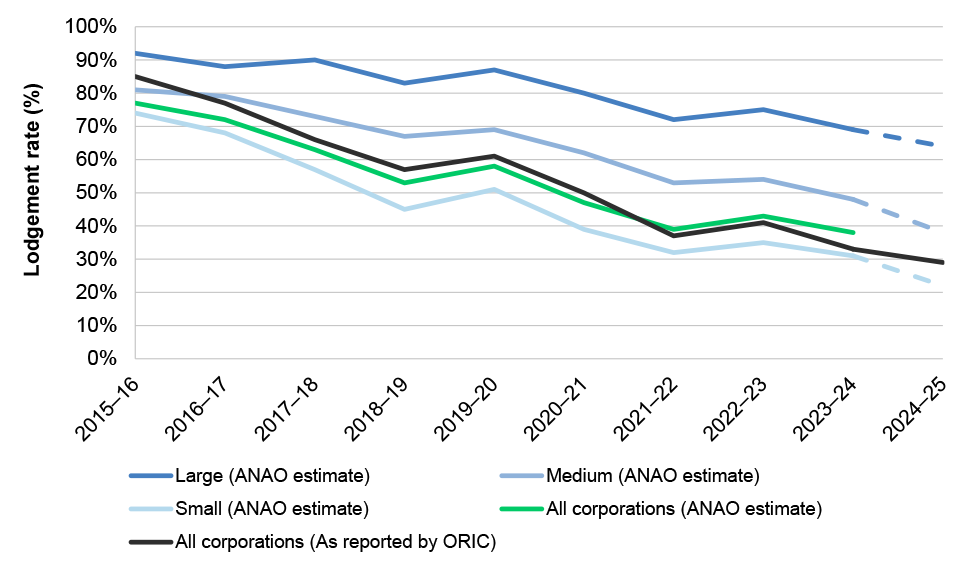

1.21 Compliance with lodging all required annual reports by December was 33 per cent for 2023–24 and 29 per cent for 2024–25 (see paragraph 4.42).

1.22 As at 30 June 2025 2,939 corporations were required to lodge annual reports for 2023–24. The 1,816 corporations that had lodged their 2023–24 general reports to ORIC by July 202524 reported $4.5 billion in revenue, $6.4 billion in assets and 22,687 employees.25 Figures will underestimate total revenue, assets and employees due to late or non-reporting.

Rationale for undertaking the audit

1.23 Australian governments have stated that in a broad range of service delivery areas including health, housing and education, Aboriginal and Torres Strait Islander organisations achieve better results for their communities and should be empowered to make decisions about and deliver the critical services on the ground.26 Corporations registered under the CATSI Act have billions of dollars in income and assets and employ tens of thousands of people. The NIAA states that Indigenous corporations ‘play a critical role in delivering services and supporting economic development in Indigenous communities, particularly in rural and remote Australia’.27 The CATSI Act is a ‘special measure’ under the Racial Discrimination Act 1975 to give First Nations peoples access to the same opportunities to form and manage corporations as everyone else.28

1.24 This audit provides assurance to the Parliament that ORIC is appropriately supporting and regulating Indigenous corporations to:

- meet the aims of the CATSI Act, which includes that First Nations peoples have access to the same opportunities to form and manage corporations as everyone else; and

- ensure that Indigenous corporations are well placed to deliver services and support economic development in Indigenous communities, particularly in remote Australia.29

Audit approach

Audit objective, criteria and scope

1.25 The objective of the audit was to assess whether Indigenous corporations are being effectively supported and regulated under the CATSI Act.

1.26 To form a conclusion against the objective, the following high-level criteria were applied:

- Are there fit-for-purpose governance arrangements for the support and regulation of Indigenous corporations?

- Have Indigenous groups been effectively supported to incorporate and Indigenous corporations to operate in compliance with the CATSI Act?

- Have regulatory powers been used effectively to respond to, correct, penalise and deter non-compliance with the CATSI Act?

1.27 The audit focused on the period 1 July 2022 to 30 June 2025.

Audit methodology

1.28 The audit methodology included:

- analysis of ORIC and NIAA records and walkthroughs of ORIC systems and processes;

- meetings with regulators (Australian Charities and Not-for-profits Commission, Australian Securities and Investments Commission, Australian Taxation Office and National Native Title Tribunal), agencies that provide grant funding to Indigenous corporations (Department of Health, Disability and Ageing and NIAA) and stakeholders (Central Land Council, Australian Indigenous Governance Institute, Indigenous Business Australia and the office of the Commonwealth Director of Public Prosecutions);

- a survey of registered corporation representatives in October 2025, which received 207 responses30; and

- reviewing two contributions to the audit from individuals involved with Indigenous corporations.

1.29 The audit was conducted in accordance with ANAO Auditing Standards at a cost to the ANAO of approximately $654,000.

1.30 The team members for this audit were Kai Swoboda, Mahkaila Sansom, Yoann Colin, Ewan McPherson, Lily Engelbrethsen, Tomislav Kesina and Christine Chalmers.

2. Governance arrangements

Areas examined

This chapter examines whether the Office of the Registrar of Indigenous Corporations (ORIC) has fit-for-purpose governance arrangements for the support and regulation of Aboriginal and Torres Strait Islander corporations (Indigenous corporations).

Conclusion

ORIC’s governance arrangements for the support and regulation of Indigenous corporations are largely fit for purpose. A regulatory framework includes a clear articulation of the Registrar’s regulatory posture, however priorities and activities could be more explicitly linked to higher rated non-compliance risks, risk treatments and data. There is no contemporary statement of intent or ministerial statement of expectations. ORIC publishes performance information and has established largely effective performance monitoring and reporting arrangements. While the CEO of the National Indigenous Australians Agency (NIAA) is the accountable authority for ORIC under the Public Governance, Performance and Accountability Act 2013, the NIAA does not report on the performance of ORIC through its corporate plan and annual report. Although ORIC lacks a stakeholder engagement plan, it has established external accountability mechanisms and identifies and acts on opportunities to improve its performance.

The Australian Government’s Regulatory Policy, Practice and Performance Framework could be clearer about expectations and requirements for statutory office holders such as the Registrar of Aboriginal and Torres Strait Islander Corporations.

Areas for improvement

The ANAO made one recommendation to the Australian Government regarding finalising a statement of expectations and intent for ORIC, and one recommendation to the Department of Finance aimed at improving guidance. The ANAO made one recommendation to the National Indigenous Australians Agency (NIAA) about regulator performance reporting and one recommendation to ORIC about improving the link between risk analysis and a compliance strategy. The ANAO suggested four areas for improvement relating to governance committee terms of reference; documenting performance measure methodologies; developing a stakeholder engagement plan; and improving processes and procedures for internal reviews.

2.1 Resource Management Guide 128: Regulator Performance (RMG 128) establishes best practice principles for regulators. This includes:

- taking a risk-based approach to operational policy development, administration, compliance and enforcement activities, that is informed by data, evidence and intelligence;

- setting, actioning and reporting against expectations for regulatory functions and performance measures to provide transparency and accountability; and

- taking into account and responding to community expectations.31

Is there a fit-for-purpose regulatory framework?

Implementation of the Registrar for Aboriginal and Torres Strait Islander Corporations’ functions is supported by appropriate line management arrangements, delegations, governance committees and memoranda of understanding with other regulators. ORIC has a publicly available, detailed and contemporary regulatory framework that includes the Registrar’s regulatory posture and priorities. ORIC describes its regulatory approach as ‘proportionate’ to the nature of the non-compliance and potential for harm. The framework could be improved with an up-to-date statement of ministerial expectations and intent; and by better reflecting several aims of the Registrar established in the CATSI Act relating to cost-effectiveness and regulatory burden. ORIC identifies non-compliance risks, which are regularly reviewed. The regulatory framework is informed by business intelligence; however it could be more clearly and explicitly linked to the more highly rated non-compliance risks, data and evidence. An updated approach to risk assessment in 2025 did not establish risk appetite, tolerances or ratings, which impacts on ORIC’s ability to effectively prioritise risk treatments and activities to achieve objectives.

Line management, committee arrangements and relationships with regulators

2.2 Implementation of the Registrar of Aboriginal and Torres Strait Islander Corporations’ (the Registrar) functions is supported by line management arrangements for ORIC’s 43 full-time equivalent staff (see Table 1.1), delegations and governance committees. The Registrar has established a delegation framework for various functions and powers. The Senior Management Group (SMG), which comprises 10 senior ORIC staff and the Registrar, is required to oversee and monitor ORIC’s regulatory approach. SMG terms of reference are dated 9 August 2022 and have not been revised to take account of February 2024 changes to the regulatory framework (see Table 2.1) and retain references to outdated ORIC documentation. The Regulatory Case Committee, which comprises four senior ORIC staff and the Registrar, is required to oversee ORIC’s response to matters of serious non-compliance. The terms of reference for the Regulatory Case Committee are dated 13 July 2023 and have also not been revised to take account of changes to the regulatory framework.

Opportunity for improvement

2.3 ORIC could review the terms of reference for key governance committees to ensure accuracy and alignment with the contemporary regulatory framework.

2.4 ORIC established memoranda of understanding (MOUs) with other regulators comprising the National Native Title Tribunal (18 May 2017); the Australian Securities and Investments Commission (ASIC) (24 August 2010); the Australian Charities and Not-for-profits Commission (ACNC) (3 June 2024); and the Australian Taxation Office (ATO) and Australian Business Registry Services (ABRS) (26 June 2024). The MOUs with ASIC and the National Native Title Tribunal are published on the ORIC website32 and the MOU with the ACNC is published on the ACNC’s website.33 MOUs with the ACNC and ATO/ABRS are more detailed than those with ASIC and the National Native Title Tribunal about data sharing, meetings and regular review of MOUs. ORIC has exchanged data and met regularly with the ACNC, the ATO/ABRS, and National Native Title Tribunal. ORIC does not have scheduled, regular engagement with ASIC and engages on an ad hoc basis to discuss specific issues.

Regulatory framework

2.5 Table 2.1 shows the artefacts making up ORIC’s regulatory framework that were in effect and made publicly available between August 2021 and November 2025.

Table 2.1: Regulatory framework, as at November 2025

|

August 2021 to January 2024 |

February 2024 to November 2025 |

|

Corporations (Aboriginal and Torres Strait Islander) Act 2006 (CATSI Act) and Corporations (Aboriginal and Torres Strait Islander) Regulations 2017 (CATSI Regulations)

|

|

|

Ministerial statement of expectations / statement of intent

|

|

|

Policy Statements and Position Statementsa

|

|

|

2021–2024 ‘corporate plan’ (August 2021)

|

Registrar’s Regulatory Posture (February 2024, updated February 2025 and February 2026)

|

|

Compliance Framework (February 2024)

|

|

|

2024–2027 ‘corporate plan’ (June 2024)

|

|

Note a: ORIC also developed for internal use 15 standard operating procedures and 27 system ‘task cards’ between May 2016 and November 2025.

Note b: As at November 2025: 01, Providing information advice and comment, June 2018. 04, Registration under the CATSI Act, March 2018. 05, The Registrar’s powers to intervene, 28 March 2017. 06, Change of corporation size, February 2013. 07, Exemptions, February 2013. 08, Corporation names, February 2013. 09, Member approval for related party benefits, February 2013. 10, Registered native title bodies corporate, 6 March 2025. 12, Registers and use and disclosure of information held by the Registrar, October 2019. 14, Review of reviewable decision, February 2013. 15, Privacy, January 2020. 16, Change to corporation details by telephone, email or Registrar’s initiative, January 2024. 17, Deregistration and reinstatements, February 2013. 18, Property of deregistered corporations, March 2024. 19, Transferring registration in and out of the CATSI Act, February 2013. 20, Special administrations, February 2017. 21, No-action letters, February 2013. 23, Review of fees charged by RNTBCs for certain native title functions, February 2013. 24, Applications for permission to deny a members’ request for a general meeting, February 2013. 25, Examinations, October 2016. 26, Compliance notices, 11 February 2013. 27, suspension of members and directors, 21 October 2013. 28, Additional or increased reporting requirements, March 2017. 29, Disqualified person and the Register of Disqualified Officers, October 2017. 30, Effect of invalid appointment of directors, 23 October 2018.

Note c: Extensions to annual general meeting and reporting deadlines, February 2024. Director terms, December 2024. Indigeneity, May 2025. Confidentiality of information provided to the Registrar, September 2025.

Note d: The five areas of regulatory action for 2024 were: reporting of assets and income; corporations providing housing or accommodation services; directors and officers meeting their duties; examinations with narrowed scope; and member rights.

Source: ANAO analysis of Regulatory compliance framework, Canberra, 2024, available from https://www.oric.gov.au/about-us/regulatory-approach [accessed 17 November 2025]; Registrar’s regulatory posture 2024, Canberra, 2024, available from https://webarchive.nla.gov.au/ [accessed 17 November 2025]; Registrar’s regulatory posture 2025, Canberra, 2025, available from https://www.oric.gov.au/about-us/regulatory-approach/registrars-regulatory-posture [accessed 17 November 2025].

2.6 ORIC’s Regulatory Compliance Framework and the Registrar’s Regulatory Posture do not incorporate references to the requirement for corporation directors, including of Indigenous corporations since November 2022, to have, or have applied for, a director identification number (see paragraph 4.15).34

Ministerial statements of expectations and regulator statements of intent

2.7 RMG 128, issued by the Department of Finance in December 2022, states that ministerial statements of expectations are issued by the responsible Minister to a regulator or an entity with regulatory functions, to provide greater clarity about government policies and objectives relevant to the regulator’s statutory objectives and how it conducts its operations. The regulator responds with a Regulator Statement of Intent that identifies how it will deliver on the expectations. RMG 128 states that statements of expectations should be issued or refreshed every two years for all Commonwealth entities with regulatory functions, or earlier if there is a change in Minister, change in regulator leadership, or significant change in Commonwealth policy or objectives. Lack of up-to-date statements of expectation and intent makes it more difficult for the regulator to have clarity about government objectives and priorities and impairs transparency and accountability given the statements are meant to be publicly available and provide the basis for regulator performance reporting.35

2.8 The Minister for Indigenous Affairs issued a statement of expectations to the Department of the Prime Minister and Cabinet (PM&C), to which PM&C responded, in 2017. In February 2021 the Minister for Indigenous Australians issued a statement of expectations to the Registrar which did not ‘anticipate’ a statement of intent, inconsistent with the requirements of RMG 128. As at November 2025, there was no contemporary statement of expectations or intent. This is not aligned with the requirement that statements are refreshed every two years or when there is a change in minister (which occurred in June 2022 and July 2024), or when there is a change in regulator leadership (which occurred in December 2021 and May 2022). In May 2025 the Registrar provided a draft statement of expectations and intent to the Minister for Indigenous Australians. As at May 2026 these had not been finalised.

Recommendation no.1

2.9 The Australian Government issue the Minister for Indigenous Australians’ statement of expectations for the Registrar of Aboriginal and Torres Strait Islander Corporations, which should include a requirement for a responding statement of intent.

National Indigenous Australians Agency response: Noted

2.10 The National Indigenous Australians Agency will brief the Government on the findings and recommendations of this report.

Alignment with risk

2.11 RMG 128 states that risk-based and data-driven regulation means, in part, that regulators manage risks proportionately and that regulators leverage data and digital technology to identify risks.

2.12 In October and November 2022 ORIC prepared risk assessments for ‘environmental and strategic’, ‘corporate and operational’ and ‘regulated population’ risks. The five regulated population risks included: serious non-compliance or undetected fraud in Indigenous corporations (rated medium after controls applied); ‘[Chief Executive Officer (CEO)] burnout’ leading to corporation failure and loss of services to communities (high); Prescribed Bodies Corporate disputes36 leading to loss of services to communities and impact on native title rights (high); and the failure to provide relevant services to Indigenous corporations that require them (medium). The risks were accepted with existing controls, except for the failure to provide relevant services to corporations. Additional treatments were developed for all the risks, regardless of their acceptance, which lowered the risk ratings to medium. Treatments included ORIC staff training, policy reviews, governance training, support to corporations, and timely prosecutions.

2.13 The three risk assessments were reconsidered in April to July 2023, at which time the regulated population risks and risk ratings identified in 2022 were retained.

2.14 In April 2025 ORIC adopted a ‘strategic risk framework’, which replaced the previous approach and states that it is used to guide ORIC’s administration of the CATSI Act, priority setting and operational decisions. The framework again categorised risks in three areas: ‘environmental’; to ORIC’s operations; and to Indigenous corporations. The framework listed risks, sources and treatments. A September 2025 assessment listed seven risks to Indigenous corporations, which comprised serious non-compliance, inaccuracy of the public register, CEO performance expectations, corporation disputes, issues outside of ORIC’s jurisdiction (which included underperforming or corrupt CEOs), failure to provide relevant support, and adopting a digital first approach. Risk sources and 17 treatments were listed. While an introduction to the ‘strategic risk framework’ states that ORIC considers controls, likelihood, consequences, risk ratings, risk acceptance authority, due dates, and accountable officers, the September 2025 framework did not identify controls, assess the risks, indicate tolerance levels, state whether the risks were accepted, or assign treatment owners.

2.15 Element two of the Commonwealth Risk Management Policy states that an entity’s risk management framework should include a risk appetite statement supported by risk tolerance statements. These establish the overarching amount and types of risk an entity is willing to accept in order to achieve its objectives and, combined with risk ratings, help entities prioritise activities to achieve objectives in a resource-constrained environment. Element four of the Commonwealth Risk Management Policy states that responsibility for managing risks should be clearly defined and should include at a minimum control and treatment owners. Establishing owners creates accountability for implementing and monitoring the effectiveness of controls and treatments. Element five is that the controls must be periodically reviewed.

2.16 RMG 128 states that:

Strategic management of risk can also improve efficiency by prioritising resources to the areas of highest risk, and increase compliance by focusing limited resources on the areas of the greatest risk of non-compliance. It can also reduce the overall compliance and cost burden by minimising government intervention where the risks are relatively low..37

2.17 ORIC’s regulatory framework describes its approach as ‘proportionate’ to the nature of the non-compliance and potential for harm. The ‘proportionate’ approach intends that:

- corporations are given the opportunity to resolve lower-risk compliance matters themselves without the need for regulatory action;

- the risk of harm to the corporation, members or stakeholders is minimised;

- when responding to non-compliance, the Registrar takes into account whether the corporation has the capacity to resolve the issues itself and if other avenues of support, guidance, and direction from ORIC have not been successful; and

- regulatory intervention is considered for corporations with a history of intentionally providing incomplete or inaccurate information and that: ignore or do not meet statutory timelines for routine requirements, do not respond to ORIC’s efforts to engage them, disregard the mandate of members, do not cooperate and fix non-compliance after being given the opportunity to do so, and demonstrate wilful or deliberate non-compliance.

2.18 The February 2024 Compliance Framework includes a ‘response continuum’, which specifies actions ranging from providing help and support where a corporation is committed to doing the right thing (described as low risk) through to enforcement action and deterrence where there is deliberate non-compliance (described as high risk).

2.19 The Compliance Framework does not explicitly refer to the specific regulated population risks identified in 2022 or 2023, and has not been updated since February 2024 to reflect the April 2025 ‘strategic risk framework’. There is no direct line of sight between the risk assessments in the strategic risk framework and the Compliance Framework, in that the same words and structure are not re-used and there is no prioritisation in the Compliance Framework that is consistent with the risk ratings. The Compliance Framework does not draw any links to data or evidence. The ANAO determined that the Compliance Framework indirectly addresses the key risks or risk treatments identified in 2022 and 2023, in that the Compliance Framework discusses issues that are broadly related to the identified risks and treatments.

2.20 Informed by business group reporting, the SMG considered drafts of the Registrar’s Regulatory Posture (which includes regulatory priorities and focus areas) in July 2023, September 2023, October 2023 and February 2024. In February 2024 the SMG was advised that focus areas were either key responsibilities under the CATSI Act or ‘based on identified trends and risks’ but that there was a risk that ‘[s]horter term focus areas do not represent [the] most significant risks to ORIC’. The five focus areas were presented without a specific risk-based rationale explicitly linked to the risks to corporations identified in 2022 and 2023 assessments, and there was no explicit link made to data and evidence. The update to the Registrar’s Regulatory Posture in February 2025 also did not include these explicit links, however it was updated after consideration by the SMG in December 2024 and February 2025, and review by ORIC managers.38

2.21 Element seven of the Commonwealth Risk Management Policy is that entities must implement arrangements for identifying, managing and escalating emerging risks and element nine is that an entity’s risk management approach must be regularly reviewed, to ensure that the approach and controls are relevant, effective, address emerging risks, and address changes in the entity’s operating environment. After its establishment in April 2025, ORIC reviewed the ‘strategic risk framework’ in June 2025, September 2025 and February 2026. The next review of the ‘strategic risk framework’ by the SMG is due in June 2026.

Recommendation no.2

2.22 The Office of the Registrar of Indigenous Corporations ensure that key regulatory framework documents, such as the Compliance Framework and Registrar’s Regulatory Posture, more clearly demonstrate the link between regulatory priorities and activities and compliance risks.

National Indigenous Australians Agency / Registrar of Aboriginal and Torres Strait Islander Corporations response: Agreed in principle / Agreed

2.23 National Indigenous Australians Agency: The NIAA supports improvements being made in relation to the link between the Registrar’s regulatory priorities and activities and compliance risks.

2.24 Registrar of Aboriginal and Torres Strait Islander Corporations: ORIC has tailored the manner in which it presents its regulatory documents with the aim of increasing corporations’ understanding of and engagement in the regulatory environment they operate in.

2.25 It supports this recommendation recognising opportunity for continued improvement. ORIC will take further steps to establish clearer and more explicit links between identified risks, our available suite of regulatory responses and regulatory priorities, and better articulate these in our regulatory framework documents. For example, my annual Registrar’s Posture will include a discussion of current and emerging sector risks and better explain how consideration of these risks has informed the development of our key regulatory focus areas.

Focus on cost-effectiveness and regulatory burden

2.26 Aims established for the Registrar in the CATSI Act include facilitating and improving the efficiency and sustainability of Indigenous corporations; and administering functions and powers with a minimum of procedural requirements (see paragraph 1.8).39 RMG 128 states that:

The Government expects regulators to weigh the efficiency and cost-effectiveness of their regulatory actions, seeking to impose the least burden on those that are regulated while maintaining essential safeguards.

2.27 In May 2023 ORIC commissioned research from Ernst & Young on the compliance costs for Indigenous corporations.40 The purpose of the research was to analyse costs associated with CATSI Act compliance requirements such as holding annual general meetings and reporting, and compare compliance costs under the CATSI Act and Corporations Act 2001 (Corporations Act). The final report was provided to ORIC in August 2025. ORIC advised the ANAO in January 2026 that the study was complex and, consequently, took longer than expected to complete. Ernst & Young found that, based on its assumptions and methodology, it was generally less expensive to operate under the Corporations Act than the CATSI Act. ORIC advised the ANAO in October 2025 that it did not agree with all of the assumptions and was considering further work.

2.28 The Compliance Framework does not include consideration of regulatory cost and burden despite this being an aim for the Registrar under the CATSI Act. ORIC has established priorities and deliverables in its 2024–2027 ‘corporate plan’ aimed at reducing burden, including a new website portal in March 2025 that included ‘straight through processing’ of corporate information41 and pre-populated general reports. Arrangements with the ACNC provide that registered charities also registered under the CATSI Act do not need to update their information on the ACNC register. In lieu of standard reporting obligations, ORIC will accept reporting provided to funding bodies in certain circumstances (see Table 1.2).

2.29 An ANAO survey of Indigenous corporations conducted in October and November 2025 (see paragraph 1.28) examined corporations’ views about how ORIC has delivered against the aims established for the Registrar in the CATSI Act and demonstration of regulator best practice principles established in RMG 128. The survey found:

- 56 per cent agreed that the Registrar’s/ORIC’s support and regulatory activities have regard to Aboriginal and Torres Strait Islander tradition and circumstances and 23 per cent disagreed;

- 56 per cent agreed that the Registrar/ORIC facilitates the efficiency of Aboriginal and Torres Strait Islander corporations and 26 per cent disagreed;

- 55 per cent agreed that the Registrar’s/ORIC’s support and regulatory activities are administered with a minimum of procedural requirements and 20 per cent disagreed;

- 53 per cent agreed that the Registrar/ORIC facilitates the sustainability of Aboriginal and Torres Strait Islander corporations and 24 per cent disagreed;

- 53 per cent agreed that ORIC demonstrate managing risks proportionately and maintaining essential safeguards while minimising regulatory burden and 24 per cent disagreed; and

- 53 per cent agreed that the Registrar/ORIC facilitates the effectiveness of Aboriginal and Torress Strait Islander corporations and 27 per cent disagreed.

2.30 Themes raised by the minority of respondents who disagreed that ORIC has effectively delivered against the aims established for the Registrar included concerns about a perceived lack of responsiveness to non-compliance; a perceived lack of respect for traditional culture; regulatory burden; and perceived poor usability and quality of systems.

2.31 Across the full survey, respondents from smaller corporations registered in New South Wales and operating in the arts, community services, health and agriculture sectors tended to be more positive about ORIC’s performance, while respondents from medium to large-sized corporations, Registered Native Title Bodies Corporate, corporations providing land and water management and corporations registered in South Australia and Western Australia tended to be less positive.

Is there effective monitoring and reporting on whether regulatory aims are being achieved?

The NIAA, whose CEO is the accountable authority for ORIC under the PGPA Act, does not include performance information about ORIC in its annual performance statements. This is inconsistent with the principle of transparency and accountability for regulator performance established in the Regulatory Policy, Practice and Performance Framework. There could be greater clarity in whole-of-government guidance on requirements for accountable authorities to publicly report through corporate plans and annual reports, on the functions of statutory authorities and office holders that are financially and administratively supported within a PGPA Act entity.

ORIC has published performance information and developed a performance framework for its regulatory functions, which has improved over time and has appropriate oversight from a senior management committee. The framework identifies a large set of input, activity, output, outcome and timeliness performance measures, which are linked to the Registrar’s objectives. There is public reporting against the measures, although, as at March 2026 results for some measures had not been reported. Publicly reported measures would be strengthened by documented methodologies and targets. ORIC publishes statistical information about the Indigenous corporations it regulates. In its advice to the Minister, ORIC has provided limited information about its performance.

Public performance reporting through a corporate plan

2.32 As stated at paragraph 1.7, as the accountable authority for ORIC, the NIAA CEO has duties under the PGPA Act in relation to ORIC, including, under section 19, to keep the responsible Minister and Minister for Finance informed about the entity and its activities and to observe and consider rules and guidance under the PGPA Act framework, which give effect to the PGPA Act. This includes the Commonwealth Procurement Rules, Commonwealth Grant Rules and Principles, and Department of Finance resource management guides such as RMG 128 Regulator Performance and RMG 131 Developing performance measures. RMG 128 states that regulators are expected to be consistent with the Regulatory Policy, Practice and Performance Framework and should refer to RMG 128 for guidance. RMG 128 applies to all Commonwealth entities that perform regulatory functions, including both standalone regulators and those located within departments.

2.33 Entities that perform regulatory functions should consider developing performance measures for these functions and publicly report performance results through corporate plans.42 RMG 128 states:

As better practice, regulator performance reporting can be incorporated into an entity’s non-financial corporate reporting to provide transparency and accountability. Where there are established performance measures set out in the corporate plan that relate to regulatory activities, these are reported on in the annual performance statements. This supports transparency and accountability of regulator performance by requiring the inclusion of this information in a consistent location for all regulators, and in reports subject to the scrutiny of the Parliament and the Auditor General. It also reduces duplication in regulator performance reporting.

2.34 The regulator performance reporting requirements are principles based. RMG 128 states that it applies to PGPA Act ‘entities and companies’ that perform regulatory functions and does not explicitly contemplate statutory office holders or bodies separately established within entities. Nonetheless RMG 128 states that ‘regulatory functions are exercised across a range of government arrangements and structures’, refers to regulation as ‘any rule endorsed by government where there is an expectation of compliance’, assumes that regulators would publish a corporate plan as defined in Part 2–3 of the PGPA Act, and promotes principles and requirements that are designed to improve accountability and transparency of regulator performance.

2.35 RMG 128 advises regulators to refer to RMG 131 Developing performance measures for guidance on designing and reporting performance measures.43 As a non-corporate Commonwealth entity, the NIAA must comply with the PGPA Act by including annual performance statements in annual reports that are consistent with the requirements and RMG 131 guidance.44 The PGPA Act does not require ORIC to develop its own corporate plan as it is not a listed entity.45

2.36 As a regulator of over 3,000 corporations with billions of dollars in income and assets and employing tens of thousands of people, some of which provide essential services to communities, public transparency on ORIC’s performance through a corporate plan and performance statement is important and aligned with the principles of RMG 128.

2.37 While the NIAA has included some statistical information on ORIC’s activities in an appendix to its annual reports since the NIAA was established in 201946, the NIAA’s corporate plans and annual performance statements do not include any performance measures for ORIC. The NIAA advised the ANAO that it did not consider the functions of ORIC as sufficiently material to include in its annual performance statements. Lack of reporting is not consistent with the principle of transparency and accountability for regulator performance established in the Regulatory Policy, Practice and Performance Framework.

2.38 ORIC advised the ANAO in December 2025 that, in the interests of being transparent and accountable, it publishes a ‘corporate plan’ and publicly reports on its performance despite not being required to do so.

Recommendation no.3

2.39 The National Indigenous Australians Agency ensure that its performance reporting for the Office of the Registrar of Indigenous Corporations, including annual performance statements and regulator performance reporting, is consistent with the principles and requirements of the Public Governance, Performance and Accountability Act 2013 (PGPA Act), PGPA Rule, Department of Finance resource management guides and other guidance designed to support PGPA Act entities to meet the requirements of the PGPA framework.

National Indigenous Australians Agency response: Agreed in principle

2.40 The NIAA will continue to comply with relevant requirements, as well as observing any updated guidance from the Department of Finance as foreshadowed in Recommendation 4.

2.41 More generally, Auditor-General Report No. 22 of 2025–26 Performance Statements of Major Australian Government Entities — Outcomes from the 2024–25 Audit Program stated that:

The 2024–25 audits identified a potential gap regarding whether, and in what manner, PGPA Act entities should report on the functions of such statutory authorities and office holders. This is particularly relevant for measuring and assessing the achievement of an entity’s purposes, given that many such authorities or office holders have separate reporting obligations outside the PGPA Act, while the accountable authority of the PGPA Act entity remains responsible for performance reporting under the Act.

Recommendation no.4

2.42 The Department of Finance:

- clarify, in its relevant guidance, how the requirements and guidance apply to statutory office holders that perform regulatory functions; and

- provide guidance for Public Governance, Performance and Accountability Act 2013 (PGPA Act) entities to report, in their annual performance statements, on the functions of statutory authorities and office holders that are not a separate PGPA Act entity and are financially and administratively supported within a PGPA Act entity.

Department of Finance response: Agreed

2.43 The Department of Finance regularly reviews and updates Resource Management Guides to support entities meet a range of requirements including those relating to performance reporting. The department will consider Recommendation 4 as part of broader updates to support accountable authorities and officials in determining whether, and in what manner, the functions of statutory office holders that are not separate Commonwealth entities but are financially and administratively supported by an entity, are accommodated in the performance reporting prepared by their entity.

2.44 Between 2006–07 and 2024–25, ORIC has publicly reported on its performance in different ways.

- Between 2006–07 and 2022–23, ORIC published a ‘yearbook’ that included performance information.

- ORIC’s 2021–2024 ‘corporate plan’ (published August 2021) included six performance measures. Results for the measures were not reported.

- The ORIC 2024–2027 ‘corporate plan’ listed 45 ‘deliverables’ and 86 unique47 performance measures, which it intended to report on publicly through three performance reports each year: ‘what ORIC has achieved’ (November); ‘the impact of ORIC’s work’ (February); and ‘how well ORIC is performing’ (July).

- ORIC published reports in November 2024, February 2025, July 2025 and November 2025, in accordance with its stated intention.48 The four reports relating to November 2024 to November 2025 reported results for 65 of 86 performance measures established in the ‘corporate plan’ (or of 80 excluding measures that related to initiatives that had not yet been implemented, such as an online training module).49 Of 43 ‘pathway deliverables’ due to be completed by July 2025, completion or ongoing progress was reported for 33.